Alternative Structural Models for E-Bank - Tiếng anh chuyên ngành | Đại học Lâm Nghiệp

Alternative Structural Models for E-Bank - Tiếng anh chuyên ngành | Đại học Lâm Nghiệp được sưu tầm và soạn thảo dưới dạng file PDF để gửi tới các bạn sinh viên cùng tham khảo, ôn tập đầy đủ kiến thức, chuẩn bị cho các buổi học thật tốt. Mời bạn đọc đón xem!

Môn: Tiếng anh chuyên ngành(DHLN) 14 tài liệu

Trường: Trường Đại học Lâm nghiệp 286 tài liệu

Tác giả:

Preview text:

Alternative Structural Models for E-Banking Adoption in Vietnam

Long Pham, Minot State University, USA

Nhi Y. Cao, National Economics University, Vietnam

Thanh D. Nguyen, Ho Chi Minh City University of Technology, Vietnam

Phong T. Tran, National Economics University, Vietnam ABSTRACT

E-banking is seen as the newest delivery channel of banks in many developed countries and is

believed to have a significant impact on the bank market. It is contended that e-banking is

providing numerous opportunities for banks and non-bank financial institutions to add a low

cost distribution channel to their existent distribution channels in order to better serve their

customers by offering various products and services with high quality. Little research on factors

influencing the adoption of e-banking has been implemented in countries that are emerging as

new potential markets (such as Vietnam) with very high economic growth rates. Thus, this study

has, based on an extensive review of literature on e-banking benefits for both banks and their

customers and relevant theories on innovation adoption, proposed alternative models (including

both moderator and mediating effects) of e-banking intention to use by customers in Vietnam.

Furthermore, a set of model hypotheses presenting relationships among factors influencing e-

banking intention to use have been set up. Practical implications and future studies were also discussed.

Keywords: E-banking; E-banking Adoption; Theory of Reasoned Action; Theory of Planned

Behavior; Decomposed of Theory of Planned Behavior; Technology Acceptance; Extension of

Technology Acceptance; Diffusion of Innovation. Introduction

Banking can be considered as an intensive information activity based on communication and

information technologies for the purpose of gaining, processing and distributing information to

users involved. Such technologies play an important role not only in the three stages of

information, but also in making favorable conditions for banks to differentiate their products and

services from their rivals. In order to be successful in a highly competitive banking market,

banks are required to innovate and update their products/services offered in an attempt to retain

their demanding and discerning customers. Facing challenges related to gaining a larger share of

the banking market, a number of banks have been making significant investments in building

more brick and mortar branches to expand their geographical penetration, while others have been

utilizing a breakthrough approach to the distribution of banking products/services to customers

through a new medium, namely, the Internet. Recently, the Internet has been rapidly gaining

popularity as a potential medium for electronic commerce (Crede, 1995). Such a rapid growth of

the Internet has brought about numerous new opportunities as well as threats to businesses.

Today, the Internet is believed to be a full-fledged delivery and distribution channel supporting 64

consumer-oriented applications aimed at effectively and efficiently providing financial products

and services to customers in the banking sector (Pham, 2010).

In the US, banks have been offering their services/products to customers via the Internet and a

number of Internet banks, such as Bank of Internet, have emerged. In addition, the Internet is

viewed as a strategic weapon that is expected to bring about new comparative advantages for

banks, especially when competitive advantages of traditional branch networks are rapidly

eroding (Seitz & Stickel, 1998) and brick and mortar only banks may largely disappear.

Indeed, the emergence of e-banking has induced many banks to rethink their information

technology strategies in order to stay competitive. Customers are today increasingly demanding

with respect to the quality of banking services. They want better levels of convenience and

flexibility with banking products and services that traditional retail banking could not offer

(Lagoutte, 1996). E-banking has made favorable conditions for banks and other financial

institutions to offer such products and services by taking advantage of an extensive public

network infrastructure (Ternullo, 1997). However, in spite of such potential benefits, there still

exist a number of problems that need to be dealt with before e-banking can become widely adopted.

Up to now, a great deal of literature has identified key factors influencing the adoption of e-

banking in developed countries

– North America and Europe and to a lesser extent in other

regions including a mix of developed and developing countries, such as Singapore, Taiwan,

Malaysia, and Thailand. However, little research on factors influencing the adoption of e-

banking has been implemented in countries that are emerging as new potential markets with very

high economic growth rates. Among these countries is Vietnam where its average economic

growth rate (GDP) was over 7% during the 1990s and early 2000s, and more than 8% in 2006,

which made it one of the highest growing economies in the World (World Bank, 2006). Together

with Vietnam’s entry into the World Trade Organization dated on 7 November 2006, its banking

sector is increasingly being deregulated in accordance with the requirements set up by the World

Trade Organization. These moves suggest that fierce competition among local banks and foreign

banks in the Vietnamese banking sector have been occurring, and Vietnamese banks may have to

adopt the Internet as a primary service delivery channel in order to survive. Thus, the objectives of this study are as follows:

1. Investigate e-banking benefits for both banks and customers.

2. Conduct an extensive review of literature on relevant theories on adoption of an innovation; and

3. Construct alternative structural models based on integration of the innovation

theories, trust, and perceived benefit for e-banking adoption in Vietnam. 65 Background E-Banking

E-banking can be considered as a high-order construct comprising several distribution channels.

E-banking is a larger concept than just banking conducted by the Internet. Nonetheless, the most

popular kind of e-banking is today believed to be banking through the Internet - Internet banking.

There are a number of ways to describe the e-banking term. In its simplest sense, it is viewed as

the provision of information or services by a bank to its customers based on a computer,

television, telephone, or mobile phone (Daniel, 1999). For instance, under the view of Jun and

Cai (2001), Internet banking is seen as an electronic connection between banks and customers

aimed at preparing, managing, and controlling numerous financial transactions. By utilizing e-

banking, it is very convenient for consumers to access their banks and accounts to implement

their banking transactions. At its sophisticated sense, e-banking is named transactional online

banking due to the fact that it embeds the provision of facilities, such as accessing accounts,

transfer of funds, and buying financial products or services online (Sathye, 1999). In this paper,

without loss of generality, the term e-banking and online banking (or even Internet banking) are

interchangeably utilized with the same meaning.

E-banking is seen as the newest delivery channel of banks in many developed countries and is

believed to have a significant impact on the banking market (Jayawardhena & Foley, 2000).

Nehmzow (1997) contends that e-banking is providing numerous opportunities for banks and

non-bank financial institutions to add a low cost distribution channel to their existent distribution

channels in order to better serve their customers by offering various products and services with

high quality. However, he further contends that e-banking also brings about challenges to

traditional banks due to the fact that it neutralizes competitive advantages rooted in a traditional banking network.

It is predicted that e-banking will continue mushrooming in the times to come. When e-banking

is widely utilized and becomes more popular, it is very interesting to forecast the future of

traditional banks operating based on their branches. According to Wah (1999), it is not

reasonable to say that such traditional banks are likely to disappear in the near future. Rather,

they will be placed on a new level of banking services/products with the support of new and

modern distribution channel technologies. Furthermore, Wah (1999) argues that traditional banks

can take advantage of new and modern technologies and they are very likely to effectively and

efficiently serve their customers. Finally, Wah (1999) concludes that e-banking is really

beneficial to customers and that e-banking and traditional banking can coexist. E-Banking’s Benefits For Banks

E-banking can bring about various benefits for banks and their customers. Cost savings,

efficiency, gaining new segments of customers, improvement of the bank’s reputation and better

customer services and satisfaction are primary benefits to banks (Jayawardhena & Foley, 2000). 66

Booz-Allen and Hamilton (1997) argue, based on their global survey, that setting up a

specialized e-banking infrastructure costs about US$1

– 2 million, which is much lower than

setting up a banking branch. In addition, the authors conclude that costs for running a traditional

bank account for 50% to 60% of its revenues.

Under the view of Robinson (2000), relevant costs for conducting a banking transaction via

online are much lower than via a brick and mortar branch. Moreover, Sheshunoff (2000)

contends that one of the most important factors influencing the adoption of e-banking by banks is

the need to build up strong barriers to customer exiting. Under the view of the author, once

customers become familiar with the utilization of full service e-banking, it is unlikely that they

will change to another financial institution. Such an argument can be supported by the consumer

behavior theory that switching costs are often very high in terms of time and efforts by

consumers. Finally, the author emphasizes that the implementation of e-banking can bring about

many competitive advantages for banks in today’s highly competitive banking market.

Research on e-banking has been carried out in Denmark by Mols (1998). The author argues that

e-banking can play an important role in enhancing cross-selling and price differentiation. E-

banking can make favorable conditions for banks to provide customers numerous services 24

hours a day and 7 days a week. E-banking can improve customer satisfaction with the bank due

to the fact that it makes customers less price sensitive, and improves their intention to

repurchase, and more loyalty to the bank via providing more positive words of mouth about the bank. For Customers

E-banking not only brings about benefits to banks but also to their customers. Thanks to the

emergence of the Internet, banking transactions are no longer limited to time and geography. It is

very easy for consumers throughout the world to have access to their bank accounts 24 hours per

day and seven days a week. Customers can enjoy a variety of services, especially services which

are not provided by traditional bank branches. It is argued that one of the greatest benefits that e-

banking brings about is that it is not expensive or may even be free for customers to utilize e-

banking products/services. However, some people believe that prices appear to be one factor that

is impedimental to the diffusion of e-banking (Sathye, 1999). The price debates often revolve

around geographical differences and disparities between costs of Internet connections and

telephone call pricing. It has also been believed that e-banks have been changing to respond to

customers’ increasingly changing demands (Jun & Cai, 2001). There has been a tendency that

customers don’t want to travel to or from a bank branch to conduct some banking transactions. In

other words, they want to utilize e-banking to save time and money. E-banking can bring about

convenience and accessibility, and have positive effects on customer satisfaction and loyalty

(Karjauloto, Mattila, & Pento, 2002; Pham, 2010). It is possible for customers to manage their

banking transactions whenever they want and to enjoy improved privacy in their interactions

with the bank. In addition, customers can enjoy more benefits at lower cost levels by utilizing e- banking (Mols, 1998).

It is contended by Turban, Lee, King and Chung (2000) that e-banking is really beneficial to

customers in terms of cost savings, no limit on time and space, quick response to customer 67

complaints, and better services/products. Such benefits are believed to elevate customer

satisfaction. In a word, e-banking offers many benefits to both banks and their customers (Pham, 2010).

Alternative Structural Models for E-Banking Adoption in Vietnam

International Studies of Consumer Adoption of E-Banking

The banking market has become highly competitive along with the emergence of new banking

technology which is believed to have strong effects on consumer behavior. Hence, banks

implementing e-banking services are required to better understand their customers regarding

attitudes of customers towards technology. If banks are successful in doing so, it makes

favorable conditions for them to positively impact and even determine consumer behavior.

Impacting and determining consumer behavior in an effective and efficient manner will, in turn,

make a significant contribution to creating a competitive advantage for banks in the future.

Interactions between the adoption and marketing of new electronic delivery channels through

relationships between banks and their customers have been establishing new environments in

which customers are better served (Mols, 1998). There have been so far a significant number of

discussions in the literature about the adoption process of e-banking services. Appendix 1

summarizes the results of such studies.

A Conceptual Model for E-Banking Adoption in Vietnam

Figure 1. A Conceptual Model for E-banking Adoption in Vietnam Bank Image Perceived Risk Perceived Intention to Use Benefit Subjective Perceived Ease Norms of Use Trust Perceived Behavioral Control

The following are theoretical support and resulting hypotheses that elicit causal relationships postulated in the model. 68

Corporate image refers to the extent to which reputational knowledge of an organization has

been accumulated and developed by customers. Such a reputational knowledge is rooted in the

minds of the customers. Specifically, reputational knowledge can be represented by a distinctive

reputation by a firm in offering products/services with very high quality (Olavarrieta &

Friedmann, 1999). Gronroos (1984) argues that corporate image is very likely to make

significant contributions to the development of service quality. Image is believed to function well

to overcome complexities generated by distinct attributes of service and when small problems

occur from functional and technical aspects of quality. In addition, the results of a study

conducted by Kang and James (2004) revealed that corporate image plays as a mediator between

service quality dimensions and the overall service quality, and the overall service quality is

positively related to customer loyalty.

Furthermore, corporate image can be understood as customers’ affective preconceptions towards

the service provider, accumulated and developed via continuous service experiences (Zins,

2001). Based on this definition, a bank image plays a vital role in the adoption of e-banking. Thus, under -

Vietnam’s e banking setting, we hypothesize that:

H1. Bank image will have a positive direct relationship with intention to use e- banking.

An e-banking transaction is considered as a mode of trusting behavior due to the fact that

customers are themselves engaging in vulnerable situations regarding such e-banking

transactions. Customers are willing to utilize e-banking as long as they believe that e-banking

functions well and performs what they expect it to do.

In e-settings, people from almost everywhere in the world are easily to get access to documents

stored on computers and in the same vein, information is easily to be transferred through e-

technologies with computer networks. That is why under the security perspective, e-banking is

considered as being risky. In addition, e-banking is characterized by highly uncertain

transactions since people who make such transactions very often come from different places in

the world. The utilization of e-banking can be considered as a new information and

communication technology and under the marketing perspective, it is also viewed as a new

distribution channel technology based on which customers can easily contact with their bank. In

the marketing field, a number of empirical studies have been conducted to show that perceived

risk is a very important construct (Gefen, 2004). In such studies, perceived risk is shown to have

significant effects on customer loyalty. Thus, under Vietnam’s e-banking setting, we hypothesize that:

H2. Perceived risk will have a negative direct relationship with intention to use e- banking.

Perceived benefit is, in the literature of technology acceptance, defined as an individual’s

positive or negative evaluation of performing a type of behavior (Chau & Hu, 2001). Hansen,

Jensen and Solgaard (2004) found that there is a significantly positive association between

perceived benefit and behavioral intention to use online shopping for groceries. In a same vein, 69

other prior research has indicated that perceived benefit has strong impacts on behavioral

intention to utilize an innovation, for example, word processing software (David, Bagozzi, &

Warshaw, 1989) or spreadsheet software (Mathieson, 1991). If someone has a feeling that

utilizing e-banking will bring about positive outcomes, then such a person will have more

intention to adopt e-banking. In contrast, if someone has a negative feeling of outcomes resulting

from utilizing e-banking, he or she will have a lower adoption intention. Thus, under Vietnam’s

e-banking setting, we hypothesize that:

H3. Perceived benefit will have a positive direct relationship with intention to use e-banking.

Subjective norms refer to the person’s perception that most people who are important to him

think that he should or should not perform the behavior in question (Ajzen & Fishbein, 1980).

Several theories suggest that subjective norms are important in shaping user behavior. For

example, TPB suggests that subjective norms influence a person’s behavioral intention.

Venkatesh and Davis (2000) explain the effect of subjective norms on behavioral intention to use

in the way that potential users may choose to use the technology if the people who are important

to them say that they should use it. Thus, under Vietnam’s e-banking setting, we hypothesize that:

H4. Subjective norms will have a positive direct relationship with intention to use e-banking.

A person’s sense of self-efficacy in terms of the utilization of an innovation is positively related

to his or her behavioral intention to utilize such an innovation (Chau & Hu, 2001). That is why if

people are confident in their ability to effectively utilize an innovation, their intention to use such

an innovation will substantially increase since they will not feel timid about using the innovation.

Perceived behavioral control can be defined as the general ability that a person feels that he or

she has to participate in a certain behavior (Ajzen, 1985; Ajzen & Madden, 1986).

Under the view of Chau and Hu (2001), perceived behavioral control is very likely to have

strong impacts on behavioral intention. In a same vein, prior research (e.g., Benhan & Raymond,

1996; Riemenschneider, Harrison, & Mykytn, 2003) have found that there is a significantly

positive relationship between perceived behavioral control and behavioral intention in a variety

of settings. Thus, it can be inferred that under the e-banking setting, a person’s behavioral

intention to utilize e-banking is very likely to be influenced by the confidence that such a person

has in his or her general ability to utilize e-banking. Thus, under Vietnam’s e-banking setting, we hypothesize that:

H5. Perceived behavioral control will have a positive direct relationship with intention to use e-banking.

Trust has been shown to have a mediating role in IS adoption models (Gefen, Karahanna, &

Straub, 2003; Ribbink, Liljander, & Streukens, 2004; Chen & Dhillon, 2003; Jarvenpaa,

Tractinsky, & Vitale, 2000; Rotter, 1971). Trust plays an important role in many transactional 70

buyer-seller relationships, especially in settings containing risks (McKnight, Cummings, &

Chervany, 1998). It is argued that trust has been serving as a critical role under online business

settings at which it is almost impossible to have physical touching and interaction with staff. In

general, trust can be defined as an expectation one chooses to trust in others who are believed to

not behave opportunistically or trust can be defined as one’s belief that others are going to

behave in a dependable, ethical, and socially desirable manner (Rousseau, Sitkin, Burt, &

Camerer, 1998). Moreover, trust can be conceptualized as a combination of such factors as

trustworthiness, integrity, honesty, and benevolence of e-vendors that are expected to escalate

behavioral intentions via reduced risks among potential but inexperienced customers (Jarvenpaa

& Todd, 1996; Gefen, Karahanna, & Straub, 2003). Thus, under Vietnam’s e-banking setting, we hypothesize that:

H6. Trust will have a positive direct relationship with intention to use e-banking.

The relationship between trust and perceived benefit has been widely discussed in a variety of

contexts including online based business settings (Gefen, Karahanna, & Straub, 2003; Pavlou,

2003; Saeed, Hwang, & Yi, 2003; Gefen, 2004). Specifically, trust and TAM is well integrated

in the online shopping setting (Gefen, Karahanna, & Straub, 2003). Such an integration showed

that trust is an antecedent of perceived benefit. Trust is contended to serve as an important

determinant of perceived benefit, especially in the online environment due in part to the

guarantee that consumers expect the perceived benefit from the website with the sellers behind it.

Furthermore, trust is strongly believed to have positive impacts on perceived benefit on the

ground that trust make favorable conditions for consumers to be vulnerable to e-vendor to ensure

that they achieve expected useful interactions and services (Pavlou, 2003). While consumers

initially trust their e-vendors and have a feeling that online service adoption is efficient to their

job performance, they intend to believe that such online services are useful (Gefen, Karahanna,

& Straub, 2003). Thus, under Vietnam’s e-banking setting, we hypothesize that:

H7. Trust will have a positive direct relationship with perceived benefit

Many studies have been conducted and found that there is a strongly positive correlation between

users’ and IS units’ mutual trust and mutual influence (Nelson & Cooprider, 1996). Moreover, it

is elicited by Decomposed TPB that users can be influenced by their peers and superiors in

determining subjective norm towards the IS utilization (Taylor & Todd, 1995). To put it another

way, it is very possible that trust in peers and superiors regarding their beliefs of the IS

utilization plays an important role in determining subjective norm. In a similar vein, trust in e-

vendors regarding their reputation, brand name, and service might have positive impacts on

subjective norm over online transactions’ behavior. Additionally, aspects of reputation, brand

name, and service might elicit certain relationships between trust in peers and superiors and trust

in vendors. Hence, whatever types of trust are with direct and indirect impacts on subjective

norm, they are all serving as important antecedents of subjective norm in the online setting.

Thus, under Vietnam’s e-banking setting, we hypothesize that:

H8. Trust will have a positive direct relationship with subjective norms. 71

The relationship between trust and perceived behavioral control has been investigated with

regards to numerous aspects where trust is found as a common antecedent of perceived

behavioral control (Bandura, 1986; David, Bagozzi, & Warshaw, 1989; Hosmer, 1995;

McKnight & Chervany, 2002; Pavlou, 2003). Trust is very likely to escalate perceived

behavioral control over online transactions due to the fact that such virtual interactions between

customers and e-vendors turn out to be more expectable (Pavlou, 2002).

Specifically, trust has impacts on perceived behavioral control via factors such as self-efficacy

and increased favorable conditions. Based on many psychological reports, self-efficacy in

personal relationships is built on self-confidence and mutual trust (Matsushima & Shiomi, 2003).

So, mutual trust embedded in such relationships between customers and e-vendors is expected to

escalate customer self-efficacy and in turn escalate perceived behavioral control. In addition,

trust is viewed as a perceptual resource that makes favorable conditions for customers to achieve

their control over e-transactions (Pavlou, 2002). Thus, under Vietnam’s e-banking setting, we hypothesize that:

H9. Trust will have a positive direct relationship with perceived behavioral control.

The relationship between perceived ease of use and perceived benefit can be explained in the

manner that if other things are equal, the easier the technology is to use, the more beneficial it

can be (Venkatesh & Davis, 2000). If using the technology is easy, potential users do not have to

spend too much time to learn how to use the technology; this may influence the performance of

the user. Besides, TAM has verified the effects of perceived ease of use on perceived benefit

(Davis, 1989; David, Bagozzi, & Warshaw, 1989). Extensive research has shown significant

effects of perceived ease of use on perceived benefit (e.g., Chan & Lu, 2004). Thus, under

Vietnam’s e-banking setting, we hypothesize that:

H10. Perceived ease of use will have a positive direct relationship with perceived benefit

Perceived ease of use is, in many studies, found to have positive impacts on trust since perceived

ease of use is very likely to escalate customers’ favorable impressions towards e-vendors in the

online service initial adoption and lead customers to be willing to make investments and

commitments in buyer-seller relationships (Gefen, Karahanna, & Straub, 2003). Under the view

of social cognitive theory, perceived ease of use is strongly contended to have positive impacts

on an individual’s favorable outcome expectation towards an innovative technology adoption

(Bandura, 1986). Such a contention is based on the fact that cognition-based trust, as mentioned

above, is primarily constructed on the first impression of the individual towards a certain

behavior. Specifically, perceived ease of use under the online service setting is viewed as the

first feeling or expectation set up for continued online transactions. Thus, under Vietnam’s e-

banking setting, we hypothesize that:

H11. Perceived ease of use will have a positive direct relationship with trust 72

Theories of reasoned action (TRA) and planned behavior (TPB) and their derivatives have been

utilized to predict possible adoption of information technology (Benbasat & Barki, 2007). While

such studies have escalated our understanding of how the theories’ main contructs have effects

on IT adoption, they ignore nonlinear relationships among the constructs. The fact that ignoring

the nonlinear effects is very likely to either understate or overstate the main effects which might

lead to erroneous, partial, or incomplete interpretations (Ping, 2002). That is the reason Ping

(2002) strongly argue that investigating complicated and contingent relationships among the

main constructs will bring about finer grained knowledge about determinants of individual IT

adoption. Thus, under Vietnam’s e-banking setting, we hypothesize that:

H12. The relationship between perceived benefit and intention to use e-banking

will be positively moderated by perceived ease of use.

H13. The relationship between perceived benefit and intention to use e-banking

will be positively moderated by trust.

H14. The relationship between perceived benefit and intention to use e-banking

will be positively moderated by subjective norm.

H15. The relationship between perceived benefit and intention to use e-banking

will be positively moderated by perceived behavioral control.

Formal Representation of the Conceptual Model

The research hypotheses can be integrated to form a set of structural equations. Since the

moderator effects of perceived ease of use, trust, subjective norm, and perceived

behavioral control on the relationship between perceived benefit on intention to use have

not been clearly tested in the literature, we create five competing structural models from

the conceptual model illustrated in Figure 1. Model A is without any moderator effects.

Model B is Model A plus the moderator effect of perceived ease of use on the

relationship between perceived benefit and intention to use. Model C is Model B plus the

moderator effect of trust. Model D is Model C plus the moderator effect of subjective

norm. Model E is Model D plus the moderator effect of perceived behavioral control. The

following abbreviations are used for simplicity: bank image (BI), perceived risk (PR),

perceived ease of use (PEU), perceived benefit (PB), trust (T), subjective norm (SN),

perceived behavioral control (PBC), and intention to use (IU).

Model A can be represented by Eqs. (1)-(5):

IU = β1(BI) + β2(PR) + β3(PB) + β4(SN) + β5(PBC) + β6(T) + e1 (1)

PB = β7(PEU) + β8(T) + e2 (2) T = β9(PEU) + e3 (3) SN = β10(T) + e4 (4) PBC = β11(T) + e5 (5) 73

To represent Model B, we modify Eqs. (1):

IU = β1(BI) + β2(PR) + β3(PB) + β4(SN) + β5(PBC) + β6(T) + α1(PEU*PB) + e1 (6)

Eqs. (2)-(5) are kept unchanged

By the same token, Model C can be represented:

IU = β1(BI) + β2(PR) + β3(PB) + β4(SN) + β5(PBC) + β6(T) + α1(PEU*PB) + α2(T*PB) + e1 (7)

Eqs. (2)-(5) are kept unchanged

Model D can be represented:

IU = β1(BI) + β2(PR) + β3(PB) + β4(SN) + β5(PBC) + β6(T) + α1(PEU*PB) + α2(T*PB) + α3(SN*PB) + e1 (8)

Eqs. (2)-(5) are kept unchanged

Model E can be represented:

IU = β1(BI) + β2(PR) + β3(PB) + β4(SN) + β5(PBC) + β6(T) + α1(PEU*PB) + α2(T*PB) +

α3(SN*PB) + α4(PBC*PB) + e1 (9)

Eqs. (2)-(5) are kept unchanged

We suggest that these alternative structural models (Model A, Model B, Model C, Model

D, and Model E) need to be tested independently and their results need to be compared and contrasted.

Conclusion and Directions for Future Research

Up to now, a great deal of literature has identified key factors influencing the adoption of e-

banking in developed countries

– North America and Europe and to a lesser extent in other

regions including a mix of developed and developing countries, such as Singapore, Taiwan,

Malaysia, and Thailand. To put it another way, little research on factors influencing the adoption

of e-banking has been implemented in countries that are emerging as new potential markets with

very high economic growth rates. Among these countries is Vietnam where its average economic

growth rate (GDP) was over 7% during the 1990s and early 2000s, and especially more than 8%

in 2006, which made it one of the highest growing economies in the World (World Bank, 2006).

Together with Vietnam’s entry into the World Trade Organization dated on 7 November 2006,

its banking sector is increasingly being deregulated in accordance with the requirements set up

by the World Trade Organization. These moves seem to indicate that fierce competition among

local banks and foreign banks in the Vietnamese banking sector have been occurring, and

Vietnamese banks have to adopt the Internet as a primary service delivery channel in order to

survive. However, there are no comprehensive models or frameworks to explain the e-banking

adoption by customers in Vietnam. 74

This study has, based on an extensive review of literature on e-banking benefits for both banks

and their customers, trust, perceived risk, corporate image, and relevant theories on innovation

adoption, proposed alternative structural models (including both moderator and mediating

effects) for e-banking adoption in Vietnam. Furthermore, a set of model hypotheses presenting

relationships among factors influencing e-banking adoption have been set up.

The next step in the development of such models is to statistically test the aforementioned

hypotheses in the Vietnamese setting. Each of the factors identified in the previous discussion

will form the basis for analysis in the empirical study of e-banking adoption in such a new

context. The models presented in this paper are unique as at present, there are no comprehensive

theoretical and practical models for analyzing e-banking adoption in newly emerging countries

such as Vietnam. None of the prior models have taken into account the interactions between

innovation theories, trust, perceived risk, corporate image, intention to use, and actual use

regarding e-banking. These models can provide an impetus for future research, structuring them

along the lines of interactions between such above theories and factors that will expand the

frontiers of knowledge in e-banking adoption. References

Ajzen, I. (1985). From intentions to actions: a theory of planned behavior: in action control:

From cognition to behavior. Kuhland, J., & Beckman, J. (Eds), Springer, Heidelberg, 11 – 39.

Ajzen, I., & Fishbein, M. (1980). Understanding Attitudes and Predicting Social Behavior.

Englewood Cliffs, New Jersey: Prentice-Hall.

Ajzen, I., & Madden, T. (1986). Prediction of goal-directed behavior: attitudes, intentions, and

perceived behavioral control. Journal of Experimental Social Psychology, 22, 453 474. –

Alhudaithy, A., & Kitchen, P. (2009). Rethinking models of technology adoption for Internet

banking: the role of website features. Journal of Financial Services Marketing, 14(1), 56 – 69.

Bandura, A. (1986). Social foundations of thought and action. Technology Studies, ( 2 2), 285 – 309.

Benbasat, I., & Barki, H. (2007). Quo Vadis, TAM. Journal of the AIS, 8(4), 211-218.

Benhan, H., & Raymond, B. (1996). Information technology adoption: evidence from a voice

mail introduction. Computer Personnel, ( 13 3), 3 25. –

Black, N. J., Lockett, A., Winklhofer, H., & Ennew, C. (2001). The Adoption of Internet

Financial Services: A Qualitative Study. International Journal of Retail & Distribution

Management, 29(8), 390–398. 75

Booz-Allen., & Hamilton. (1997). Internet banking in Europe: A survey of current use and future

prospects. Black Enterprise, New York.

Chan, S., & Lu, M. (2004). Understanding Internet banking adoption and use behavior: a Hong

Kong perspective. Journal of Global Information Management, 12(3), 21 – 43.

Chau, P., & Hu, P. (2001). Information technology acceptance by individual professionals: a

model comparison approach. Decision Sciences, 32(4), 699 719. –

Chen, S., & Dhillon, G. (2003) ‘Interpreting dimensions of consumer trust in e-commerce.

Information Technology and Management, 4, 303 318. –

Crede, A. (1995). Electronic commerce and the banking industry: the requirement and

opportunities for new payment systems using the Internet. Journal of Computer-Mediated

Communication, 1(3), 1 – 17.

Daniel, E. (1999). Provision of electronic banking in the UK and the Republic of Ireland.

International Journal of Bank Marketing, 17(2), 72 82. –

David, F. (1989). Perceived usefulness, perceived ease of use, and user acceptance of

information technology. MIS Quarterly, ( 13 3), 318 339. –

David, F., Bagozzi, R., & Warshaw, P. (1989). User acceptance of computer technology: a

comparison of two theoretical models. Management Science, 35(8), 982 – 1003.

Eriksson K., Kerem K., & Nilsson D. (2005). Customer acceptance of internet banking in

Estonia. Int. J. Bank Mark, ( 23 2), 200-216.

Fink, F., Eriksson, K., Kerem, K., & Nilsson, D. (2005). Customer acceptance of Internet

banking in Estonia. International Journal of Bank Marketing, 23(2), 200 – 216.

Gefen, D. (2004). What makes an ERP implementation relationship worthwhile: linking trust

mechanisms and ERP usefulness. Journal of Management Information Systems, 21(1), 263 288. –

Gefen, D., Karahanna, E., & Straub, D. (2003). Trust and TAM in online shopping: an integrated

model. MIS Quarterly, 27(1), 51 90. –

Gronroos, C. (1984). A service quality model and its marketing implications. European Journal

of Marketing, 18(4), 36 – 44.

Hansen, T., Jensen, J., & Solgaard, H. (2004). Predicting online grocery buying intention: a

comparison of the theory of reasoned action and the theory planned behavior.

International Journal of Information Management, 24(6), 539 – 550. 76

Hosmer, L. (1995). Trust: the connecting link between organizational theory and philosophical

ethics. Academy of Management Review, ( 20 2), 379 403. –

Hussein, A., & Zolait, S. (2010). An examination of the factors influencing Yemeni bank users’

behavioral intention to use Internet banking services. Journal of Financial Services Marketing 15 , (1), 76 – 94.

Jarvenpaa, S., & Todd, P. (1996). Consumer reactions to electronic shopping on the WWW.

International Journal of Electronic Commerce, 1(2), 59 88. –

Jarvenpaa, S., Tranctinsky, N., & Vitale, M. (2000). Consumer trust in an Internet store.

Information Technology and Management, 1, 45 – 71.

Jayawardhena, C., & Foley, P. (2000). Changes in the banking sector t – he case of Internet

banking in the UK. Internet Research: Electronic Networking Applications and Policy, 10(1), 19 – 30.

Jun, M., & Cai, S. (2001). The key determinants of internet banking service quality: a content

analysis. International Journal of Bank Marketing, ( 19 7), 276-91.

Kang, G., & James, J. (2004). Service quality dimensions: an examination of Gronroos’s service

quality model. Managing Service Quality, ( 14 4), 266 – 277.

Karjaluoto, H., Mattila, M., & Pento, T. (2002). Factors underlying attitude formation towards

online banking in Finland. International Journal of Bank Marketing, ( 20 6), 261 – 272.

Lagoutte, V. (1996). The Direct Banking Challenge. Unpublished Honor Thesis: Middlesex University.

Liao, S., Shao, Y., Wang, H., & Chen, A. (1999). The adoption of virtual banking: an empirical

study. International Journal of Information Management, ( 19 1), 63 74. –

Mathieson, K. (1991). Predicting user intentions: comparing the technology acceptance model

with the theory of planned behavior. Information Systems Research, ( 2 3), 173 191. –

Matsushima, R., & Shiomi, K. (2003). Developing a scale of self-efficacy in personal

relationships for adolescents. Psychological Reports, ( 92 1), 967 985. –

McKnight, D., & Chervany, N. (2002). What trust means in e-commerce customer relationships:

an interdisciplinary conceptual typology. International Journal of Electronic Commerce, 6(2), 35 – 72.

McKnight, D., Cummings, L., & Chervany, N. (1998). Initial trust formation in new organization

relationships. Academy of Management Review, 23(3), 472 – 490. 77

Mols, K. (1998). The behavior consequences of PC banking. International Journal of Bank Marketing 16 , (5), 195 – 201.

Ndubisi, N., & Sinti, Q. (2006). Consumer attitudes, system’s characteristics and Internet

banking adoption in Malaysia. Management Research News, 29(½), 16 27. –

Nehmzow, C. (1997). The Internet will shake banking medieval foundations. Journal of Internet

Banking and Commerce, 2(2), 19 25. –

Nelson, K., & Cooprider, J. (1996). The contribution of shared knowledge to IS group

performance. MIS Quarterly, ( 20 4), 409 432. –

Olavarrieta, S., & Friedmann, R. (1999). Market-oriented culture, knowledge-related resources,

reputational assets and superior performance: a conceptual framework. Journal of

Strategic Marketing, 7, 215 228. –

Ozdemir, S., & Trott, P. (2009). Exploring the adoption of a service innovation: a study of

Internet banking adopters and non-adopters. Journal of Financial Services Marketing, 13(4), 284 – 299.

Pavlou, P. (2002). What drives electronic commerce? A theory of planned behavior prespective.

Best Paper Proceedings of the Academy of Management Conference, Denver, CO, 9 – 14.

Pavlou, P. (2003). Consumer acceptance of electronic commerce i

– ntegrating trust and risk with

the technology acceptance model. International Journal of Electronic Commerce, 7(3), 69 103. –

Pham, L. (2010). A conceptual framework for e-banking service quality in Vietnam. The

Business Studies Journal, 2(1), 81-95.

Pikkarainen, T., Pikkarainen, K., Karjaluoto, H., & Pahnila, S. (2004). Consumer acceptance of

online banking: an extension of the technology acceptance model. Internet Research, 14(3), 224 – 235.

Ping, R.A. (2002). Interpreting latent variable interactions. American Marketing Association

(Winter) Educator’s Conference Proceedings, Austin, TX, February, 22-25, 213-220.

Ribbink, B., Liljander, A., & Streukens, S. (2004). Comfort your online customer: quality, trust,

and loyalty on the Internet. Management Service Quality, ( 14 6), 446 456. –

Riemenschneider, C., Harrison, D., & Mykytn, P. (2003). Understanding IT adoption decisions

in small businesses: integrating current theories. Information and Management, ( 40 4), 269 285. – 78

Robinson, T. (2000). Internet banking s

– till not a perfect marriage. Information Week, ( 17 4), 104 106. –

Rotter, J. (1971). Generalized expectancies of interpersonal trust. American Psychologist, ( 26 5), 443 452. –

Rousseau, D., Sitkin, S., Burt, R., & Camerer, C. (1998). Not so different after all: a cross-

discipline view of trust. Academy of Management Review, ( 23 3), 276 – 286.

Saeed, K., Hwang, Y., & Yi, M. (2003). Toward an integrative framework for online consumer

behavior research: a meta-analysis approach. Journal of End User Computing, ( 15 4), 1 – 26.

Sathye, M. (1999). Adoption of Internet Banking by Australian Consumers: an empirical

investigation. International Journal of Bank Marketing, ( 17 7), 324 – 334.

Seitz, J., & Stickel, E. (1998). Internet banking: an overview. Journal of Internet Banking and

Commerce, 3(1), 169 - 185.

Sheshunoff, A. (2000). Internet banking a

– n update from the frontlines. ABA Banking Journal, 92(1), 51 55. –

Shih, Y., & Fang, K. (2003). The use of decomposed planned behavior to study Internet banking

in Taiwan. Internet Research, ( 14 3), 213 223. –

Suh, B., & Han, L. (2002). Effect of trust on consumer acceptance of Internet banking.

Electronic Commerce Research and Application, 1, 297 363. –

Tan, M., & Teo, T. (2000). Factors influencing the adoption of Internet banking. Journal of the

Association for Information System, 1(5), 1 - 42.

Taylor, S., & Todd, P. (1995). Understanding information technology usage: a test of competing

models. Information System Research, ( 6 2), 144 – 176.

Ternullo, G. (1997). Banking on the Internet: new technologies, new opportunities and new risks.

Boston Regional Outlook, Second Quarter: http://www.fdic.gov/index.html.

Turban, E., Lee, J., King, D., & Chung, H. (2000). Electronic Commerce: A Managerial

Perspective. Pretence Hall International Inc.

Venkatesh, V., & Davis, F. (2000). A theoretical extension of the technology acceptance model:

four longitudinal studies. Management Science, 46(2), 186 204. –

Wah, L. (1999). Banking on the Internet. American Management Association, ( 88 11), 44 48. – 79

Wang, Y., Lin, H., & Tang, T. (2003). Determinants of user acceptance of Internet banking: an

empirical study. International Journal of Service and Industrial Management, ( 14 5), 501 – 519.

World Bank. (2006). Vietnam Development Report 2007: Pillars of Development. Report No.

20018-VN, Washington, DC: World Bank.

Yousafzai, S., Pallister, J., & Foxall, G. (2009). Multi-dimensional role of trust in Internet

banking adoption. The Service Industries Journal, ( 29 5), 591 605. –

Zins, H. (2001). Relative attitudes and commitment in customer loyalty models: some

experiences in the commercial airline industry. International Journal of Service Industry

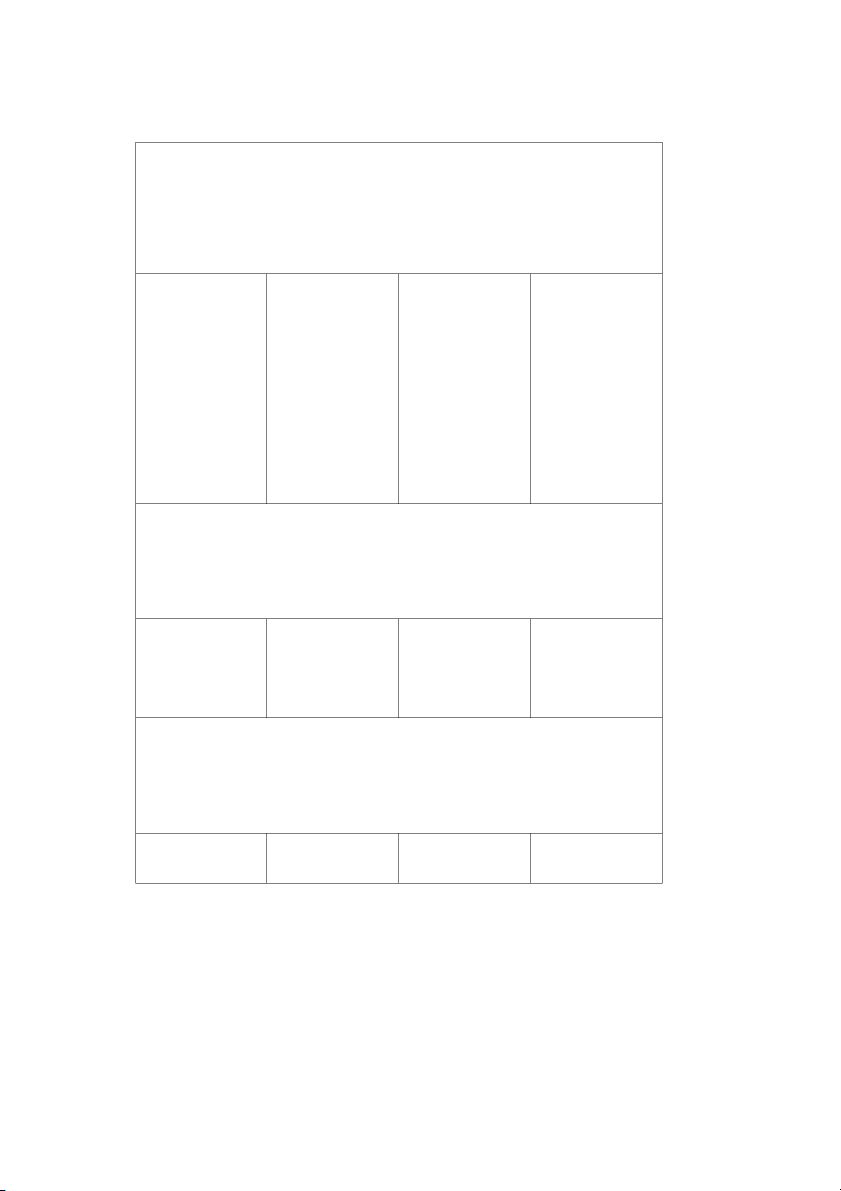

Management, 12(3), 269 – 294. APPENDIX 1

International studies on e-banking adoption Authors Name of study Models utilized Determinants Hussein and Zolait, An examination of TPB (theory of + Attitude 2010 the factors planned behavior) + Subjective norm influencing Yemeni TRA (theory of +Perceived bank users’ reasoned action) behavioral control behavioral intention + Ease of use to use Internet + Awareness banking services + Advantage + Media

This study, based on a self-administered survey involving a convenience sample of 369

Yemeni bank customers, investigates the potential prominent factors relating to the

adoption and use of the financial services of Internet banking in Yemen. The authors of

this study show that the overall prominent predictors include Relative

Advantage/Compatibility, User's Informational-Based Readiness, Attitude, Observability,

Technology Facilitating Condition, Perceived Behavioural Control and Self-efficacy. The

model accounted for 75 per cent of the variation of an individual's behavioural intention to use IB. Ozdemir and Trott, Exploring the TAM (technology + Socioeconomic 2009 adoption of a acceptance model) factors service innovation: Diffusion of + Situational factors a study of Internet Innovation + Perception factors banking adopters

Theory of perceived related to Internet and non-adopters Risk banking use + Related experiences Findings:

The authors show that Internet banking adopters and non-adopters have different

perceptual, experience-related, socioeconomic and situational characteristics. In addition, 80

besides the perceptual factors related to Internet banking use, perceptual factors in

relation to the banks in Turkey have significant impacts on Internet banking adoption. Alhudaithy and Rethinking models TAM + Website features Kitchen, 2009 of technology TRA adoption for Internet TPB banking: the role of website features Findings:

The authors show that website features have significant impacts on technology adoption,

and specifically Internet banking. Yousafzai, Pallister Multi-dimensional Model of trust for + Trust and Foxall, 2009 role of trust in Internet banking + Perceived risk Internet banking adoption Findings:

The authors show that trust and perceived risk are direct antecedents of intention, and

trust is a multi-dimensional construct with three antecedents: perceived trustworthiness,

perceived security, and perceived privacy. Ndubisi and Sinti,

Consumer attitudes, Decomposed TPB + Banking needs 2006 system’s + Compatibility characteristics: an + Complexity internet banking + Trainability adoption in + Risk Malaysia + Utilitarian orientation + Hedonic orientation Findings:

The authors show that attitudinal factors play an important role in explaining the e-

banking adoption. In addition, utilitarian orientation of the website, not hedonic

orientation, has significant impacts on adoption. Fink, Eriksson, Internet banking Decomposed TPB + Features of the Kerem and Nilsson, adoption strategies web 2005 for a developing + Perceived country: the case of usefulness Thailand + Risk and privacy + Personal preference + External environment + Culture Findings:

The authors reveal that the attitudinal factors, such as features of the website and

perceived usefulness, are very likely to have positive impacts on the e-banking adoption

in Thailand, while the most salient impediment to the e-banking adoption is a perceived 81

behavioral control, or external environment. Besides such above factors, the important

moderating factors are gender, educational level, income, internet experience and internet

banking experience, but not age. Eriksson, Kerem Customer TAM + Trust and Nilsson, 2005 acceptance of + Perceived internet banking in usefulness Estonia + Ease of use + Use Findings:

The authors indicate that the utilization of e-bank is very likely to elevate if customers

perceive e-banking as useful. Specifically, the perceived usefulness is very important due

to the fact that it determines if the perceived ease of use of e-bank results in increased use

of e-bank. In other words, e-banking services which are well-designed and easy to use

might not be realized if they are not perceived as useful. Hence, the authors conclude that

the perceived usefulness of e-banking plays an important role in motivating customer

usage. Moreover, the authors contend that technology acceptance models need to be

redesigned with more emphasis placed on the importance of the services’ perceived

usefulness offered by the technology. Pikkarainen, Consumer TAM and focus + Perceived Pikkarainen, acceptance of online group usefulness Karjaluoto and banking: an + Perceived ease of Pahnila, 2004 extension of use technology + Perceived acceptance model enjoyment + Information on online banking + Security and privacy + Quality of internet connection Findings:

The authors conclude that perceived usefulness and information on online banking of the

Website are viewed as the primary factors that are very likely to have impacts on the acceptance of online banking. Wang, Lin and Determinants of TAM + Trust/Perceived Tang, 2003 users acceptance of credibility internet banking + perceived usefulness + Ease of use + Computer self- efficacy + Intention Findings:

Based on the results of the study, the authors conclude that individual difference variables

such as computer self-efficacy have significant effects on behavioral intention via 82

perceived ease of use, perceived usefulness, and perceived credibility. In addition, the

authors show that users with a higher computer-self efficacy are likely to have more

positive usefulness and ease of use beliefs, but have more negative credibility beliefs in

e-banking. Such results are in line with that of the prior studies which have indicated that

there is a significant direct e-banking relationship between computer-self efficacy and

perceived ease of use of e-banking. Finally, the authors show that computer-self efficacy

has a negative impact on perceived credibility; however, its total impact on behavioral intention is positive.

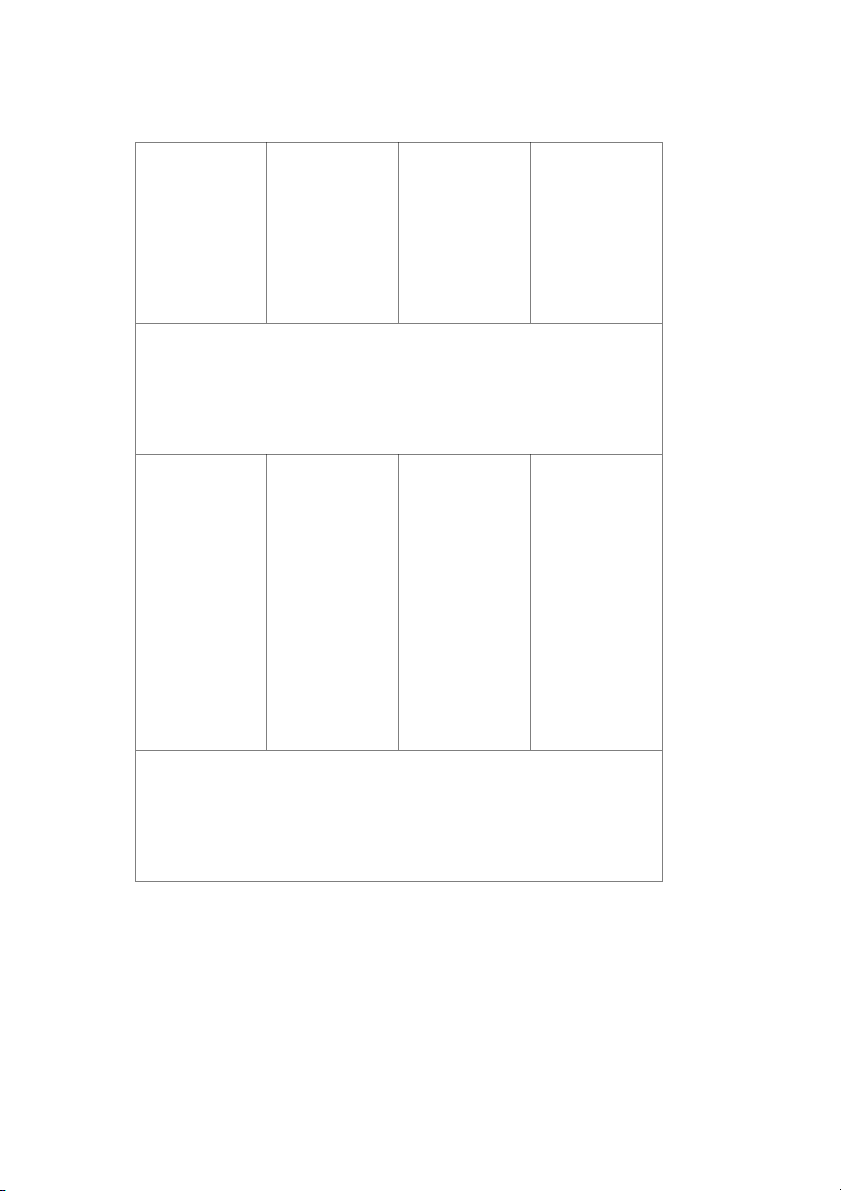

Shih and Fang, 2003 The use of TPB and + Behavior intention decomposed theory Decomposed TPB + Actual usage of planned behavior + Attitude to study internet + Subjective norms banking in Taiwan + Perceived advantage + Relative advantage + Compatibility + Complexity + Normative influences + Efficacy + Facilitating Findings:

It is, based on the decomposed TPB model, shown in this study that only relative

advantage and complexity are related to attitude, but compatibility is not related to

attitude. In terms of subjective norm, the causal path starting from subjective norm to

intention is not statistically significant. Nevertheless, self-efficacy is found to be a

significant determinant of PBC. Finally, the authors show that facilitating conditions do

not have impacts on perceived behavioral control. Suh and Han, 2002 Effects of trust on TAM + Trust customer acceptance + Perceived of internet banking usefulness + Ease of use + Attitude + Intention to use Findings:

It is shown in this study that trust plays the most important role in explaining a

customer’s attitude towards utilizing e-banking. In line with TAM, in this study,

customer perception of the usefulness and ease of use also have significant impacts on

attitude. Moreover, behavioral intention to use e-banking is significantly related to

attitude, perceived usefulness, and trust. Such findings elicit that trust is much

emphasized by customers in e-environments with a lot of sensitive information. Karjaluoto, Mattila Factors underlying TAM + Prior computer and Pento, 2002 attitude formation experience towards online + Prior 83 banking in Finland technological experience + Prior banking experience + Reference group influences Findings:

It is shown in this study that prior computer experience, prior technology experience,

personal banking experience, reference group and computer attitudes have significant

impacts on attitude and behavior towards e-banking. In addition, there is a significantly

positive relationship between personal banking experience and attitude. Black, Lockett, The adoption of Decomposed TPB + Relative Winklhofer and internet financial advantage Ennew, 2001 service: a qualitative + Compatibility study + Trainability + Observability + Complexity Findings:

The authors of this study concentrate on innovations related to delivery of financial

services via the e-channels and on reassessment of Rogers’ (1983) model’s applicability.

The data was colleted via the focus group members based on their usage of the internet.

There are differences between people who utilize the internet to buy financial services

(S3) and people who utilize the internet to buy goods/services (not financial services)

(S2) in terms of income and the utilization of information technology (higher levels for

S3). When S2 is compared with S1 (people who utilize the internet without buying

anything over the internet), there are also differences in terms of income and the product

related environment (higher levels for S2).

Based on such comparisons among the three groups, it is shown that considering factors

of Rogers’ model, similar attitudes exist in S1 and S2 regarding their perceived

advantages by utilizing e-banking compared to utilizing bank branches and risks

involved. S1 and S2 attitudes are much less positive than that of S3. In addition,

compatibility with a person’s values and previous experience with the product category is

proved to be one of the most important factors affecting the adoption of the internet to

carry out financial transactions. Trialability is considered important for the future

adoption, but its availability needs to be better communicated. In spite of the fact that

Rogers’ model utilized to assess an innovation’s perceived attributes is thought of as a

useful starting point, there are still other issues emerged that should be taken into

consideration, such as societal issues and the sense of fatalism. It seems that the former

may have a negative effect on the adoption, while the latter may have a positive effect on the adoption. Tan and Teo, 2000 Factors influencing TPB and Diffusion + Relative the adoption of of Innovation advantages internet banking + Compatibility with values + Internet 84 experiences + Banking needs + Complexity + Trialability + Risk + Self efficacy + Government support + Technology support + Social norms Findings:

The findings from the study uncover that factors such as attitudinal and perceived

behavioral control factors, not social influence, have a significant role in influencing the

intention to adopt e-banking. Specifically, perceptions of relative advantage,

compatibility, trialability, and risk towards utilizing the internet have impacts on

intentions to adopt e-banking services. Furthermore, the confidence in utilizing e-banking

services and perception of government support for e-commerce also have impacts on

intentions to adopt e-banking services. Liao, Shao, Wang The adoption of TPB and Diffusion + Attitude and Chen, 1999 virtual banking: an of Innovation + Relative empirical study advantage + Ease of use + Compatibility + Result demonstrability + Perceived risks + Subjective norms + Belief of image + Belief of visibility + Critical mass + Perceived behavioral control + Voluntariness + Trialability + Support + Learning Findings:

In this study, TPB is partially utilized for the prediction of the adoption of e-banking.

Nevertheless, there are four major relationships of TPB presented as the four hypotheses

and three of them were tested. The first hypothesis stated that attitude towards virtual

banking was dependent on relative advantage, compatibility, ease of use, result

demonstrability, and perceived risk. Reliable measures on perceived risk could not be

obtained and only the first four constructs were tested. The hypothesis was supported but

the two factors found were not clear cut. One of them was a combination of ease of use, 85

compatibility and result demonstrability whereas the other was a mixture of relative

advantage, compatibility and result demonstrability. The explanation power of this

relationship is 0.56. The second hypothesis claimed that subjective norms about virtual

banking were dependent on image, visibility and critical mass. Visibility was not used as

no reliable measure was available. The hypothesis was also supported. However, the R

square value was only 0.29, which meant that image and critical mass alone could not

provide a powerful explanation of subjective norms.

The third hypothesis was that perceived behavioral control about virtual banking was

dependent on voluntariness, trialability, support and organizational learning. However,

this hypothesis could not be tested in this study due to an unavailable reliable measure.

The last hypothesis stated that intention to use virtual banking was determined by

attitude, subjective norms and perceived behavioral control. Dependency on subjective

norms could not be tested due to the absence of reliable measure. Dependency on the

other two factors was founded statistically significant. Nevertheless, the low R square

value of 0.056 indicated very low explanation power. Sathye, 1999

Adoption of internet TPB and Diffusion + Security concerns banking by of Innovation + Ease of use Australian + Awareness of consumers service and its benefits + Reasonable price + Resistance to change + Availability of infrastructure Findings:

The author of this study reveals that security concerns and lack of awareness about e-

banking and its benefits are considered as the main impediments to the adoption of e- banking in Australia. 86

Copyright of Academy of Business Research Journal is the property of Academy of Business

Research and its content may not be copied or emailed to multiple sites or posted to a listserv

without the copyright holder's express written permission. However, users may print,

download, or email articles for individual use.

Copyright of Academy of Business Research Journal is the property of Academy of Business

Research and its content may not be copied or emailed to multiple sites or posted to a listserv

without the copyright holder's express written permission. However, users may print,

download, or email articles for individual use.

Tài liệu liên quan:

-

Critical Success Factors for the Adoption of e-Banking in Malaysia - Tiếng anh chuyên ngành | Đại học Lâm Nghiệp

274 137 -

Multiple choice - Vocabulary and grammar - Tiếng anh chuyên ngành | Đại học Lâm Nghiệp

269 135 -

Bitis Hunter - Tiếng anh chuyên ngành | Đại học Lâm Nghiệp

297 149 -

Chapter 4 The value of common stocks - Tiếng anh chuyên ngành | Đại học Lâm Nghiệp

349 175