Sample Questions case study sample answer - Auditing (AA123) | Đại học Hoa Sen

Sample Questions case study sample answer - Auditing (AA123) | Đại học Hoa Sen được sưu tầm và soạn thảo dưới dạng file PDF để gửi tới các bạn sinh viên cùng tham khảo, ôn tập đầy đủ kiến thức, chuẩn bị cho các buổi học thật tốt. Mời bạn đọc đón xem

Môn: Auditing (AA123) 55 tài liệu

Trường: Trường Đại học Hoa Sen 5.3 K tài liệu

Tác giả:

Preview text:

Sample Questions:

1. Over 1,000 subscribers to Morningstar.com completed an online survey that

included the following three questions:

A. How would you rate the return on the stock of your employing firm over the last

five years versus the return of the overall stock market?

B. What is your best estimate of the future return on the stock of your employing

firm over the next five years versus the return of the overall stock market?

C. In your opinion, is the stock of your employing firm more or less likely than the

overall stock market to lose half of its value over the next five years?

The responses show that the answers to questions A and B are highly and positively

correlated. The responses to question C indicate that 83.6% of the respondents

believed that their employing firm’s stock price had an equal or less chance of

losing half of its value compared to the overall market. What psychological biases do these responses suggest? Suggested answer:

The responses to questions A and B demonstrate that investors fall victim to

representativeness bias by extrapolating past performance into the future.

Employees whose employing firm outperformed the market in the past are

predicting it to do so again in the future. Firms that under performed in the stock

market are predicted to continue under performing by their employees. The belief

by employees that their employer’s stock is safer than a diversified portfolio is

consistent with overconfidence. Such overconfidence in their employer is probably

caused by familiarity bias. Employees appear to believe that which is familiar to

them (their company’s stock) is better and less risky than that with which they are

less familiar (other stocks). However, a large amount of firm-specific risk is

diversified away in a carefully selected portfolio like the S&P 500, making the

investment of retirement funds in a widely diversified portfolio far less risky than a

similar investment in a single stock. Only 16.4% of the respondents in the

Morningstar.com survey seem to have realized this. Representativeness bias and

familiarity bias can influence employees to invest heavily in their employer when

that stock has exhibited high historical returns. This can be a disastrous mistake, as

witnessed in the case of Enron, WorldCom, Tyco and other spectacular corporate blowups.

2. Suppose an investor made a spectacular gain on BioSpecifics Technologies Corp.

(BSTC) and subsequently invested the proceeds in a highly speculative

biotechnology startup. What psychological bias might have caused this bet?

Suggested answer: The house money effect (gambler’s fallacy) 3. CASE STUDY

Victoria Jourdan, CFA, works for an investment firm that manages private client

accounts. Both Jourdan and the Inger family reside in a politically stable country

whose currency trades at a fixed exchange rate of 1:1 with the Euro. Real GDP

growth and inflation both average about 3 percent annually, resulting in nominal

annual growth of approximately 6 percent. The country in which the Ingers reside

maintains a flat tax of 25 percent on all personal income and a net capital gains tax

(based on the sale of price-appreciated assets) of 15 percent, with no distinction

between short- and long-term holding periods. Also incorporated into the tax code is

a wealth transfer tax. Any asset transfer between two parties, whether as a gift or

family inheritance, is taxed at the flat rate of 50 percent. The country maintains a

national pension plan, but that plan’s long-term viability has been called into

question because of an unfavorable demographic trend toward older, retirement-

age recipients. Public debate has grown about how to assure the financial security

of future retirees, and among this debate’s chief outcomes has been the creation of

self-contributory, tax-advantaged investment accounts for individuals. Taxpayers

may annually contribute up to €5,000 of after-tax income to a Retirement Saving

Account (RSA), which they then control. RSA investment returns are exempt from

taxation, and participants may begin making tax-free withdrawals of any amount at age 62. The Inger Family

Jourdan has been asked to manage the Inger family account, which is a new

relationship for her firm. Jourdan observes that the Inger family has no stated

investment policy or guidelines, and she arranges for a meeting with Peter and

Hilda Inger, who have been married for 37 years, plus their two children, Christa

and Hans, aged 25 and 30, respectively. Peter, Hilda, and Hans accept the

invitation, but Christa, who currently resides a considerable distance away from her parents, cannot attend.

Peter Inger, 59, is a successful entrepreneur who founded a boat manufacturing

business, IngerMarine, when he was 23 years old. He has worked compulsively to

build the company into a producer of luxury pleasure boats sold worldwide, but he is

now considering a business succession plan and retirement. Peter is eager to

“monetize” his equity stake in IngerMarine and believes he will be able to sell his

company within the next three months. He is already evaluating three separate bids

that indicate probable proceeds, net of taxes on gains, of approximately €55 million

to the Inger family in total. The four Inger family members are the sole IngerMarine

shareholders, and any sale proceeds will accrue to the four family members in

proportion to their percentage ownership in IngerMarine. Peter believes that

everyone in his family is financially secure and wishes to preserve that security; he

recognizes the family’s need for a coherent investment plan. Hilda Inger, 57, comes

from a wealthy family. Since her marriage to Peter, she has been a housewife and

mother to Christa and Hans. Hilda is the beneficiary of a trust established by her

family. Throughout her lifetime, the trust will distribute to her an inflation-indexed

annual payment (currently €75,000), which is taxed as personal income. At her

death, payments will stop, and the trust’s remaining assets will be transferred to a

local charity. Both Hans and Christa are unmarried. Hans currently works as a senior

vice president at IngerMarine and specializes in boat design. Peter has tried to

involve Christa in the family business but she has resisted, instead achieving

moderate recognition and financial success as an artist. Christa has a 5-year-old

son, Jürgen, whom she has chosen to raise alone. The meeting with Peter, Hilda, and

Hans and several telephone discussions with Christa result in the following financial

and personal details for the Inger family.

A distinguishing characteristic of private asset management is the wide range of

personal concerns and preferences that influence the decision-making process Step 1:

Peter Personality: Peter is a perfectionist and likes to maintain control. Now that

he has attained financial success, he seems intent on preserving his wealth. He has

consistently been averse to risk, leverage, and change, both in his company and in

his personal life. IngerMarine has followed policies of low debt and slow growth,

focusing on earnings stability. Like many of his countrymen, Peter holds a portion of

his liquid assets in gold bullion. He believes that gold provides a viable hedge

against catastrophic economic surprises and plans to maintain his current holding

(€500,000) for the foreseeable future. By his own admission, Peter has been slow to

adopt a succession plan—he has always believed that he was the best person to run

IngerMarine. Although he now wants to sell IngerMarine and retire, in the past he

resisted various purchase offers for the company.

Goals: Peter wants to maintain the standard of living that he and Hilda currently

enjoy. In fact, he is actively investigating real estate for a second home, and he

desires that the new home “make a statement.” Hilda hopes the home will

ultimately be featured in a magazine and anticipates that it will cost approximately

€7 million. Peter also wants to get to know his grandson better. Since Jürgen’s birth,

Peter has been estranged from his daughter and he wants to restore the

relationship. He would like to provide financial support for Jürgen’s health- and

education-related expenses, and he plans to begin a gifting program for Jürgen next

year; the gifts will be €15,000 per year, increasing with inflation. Finally, Peter also

has a strong desire to ensure his family’s financial security and feels he will have

accumulated enough wealth through the sale of IngerMarine to realize this goal. He

does not, however, have a formal estate plan for transferring assets to his children and grandchildren. Step 2: Psychological Profiling

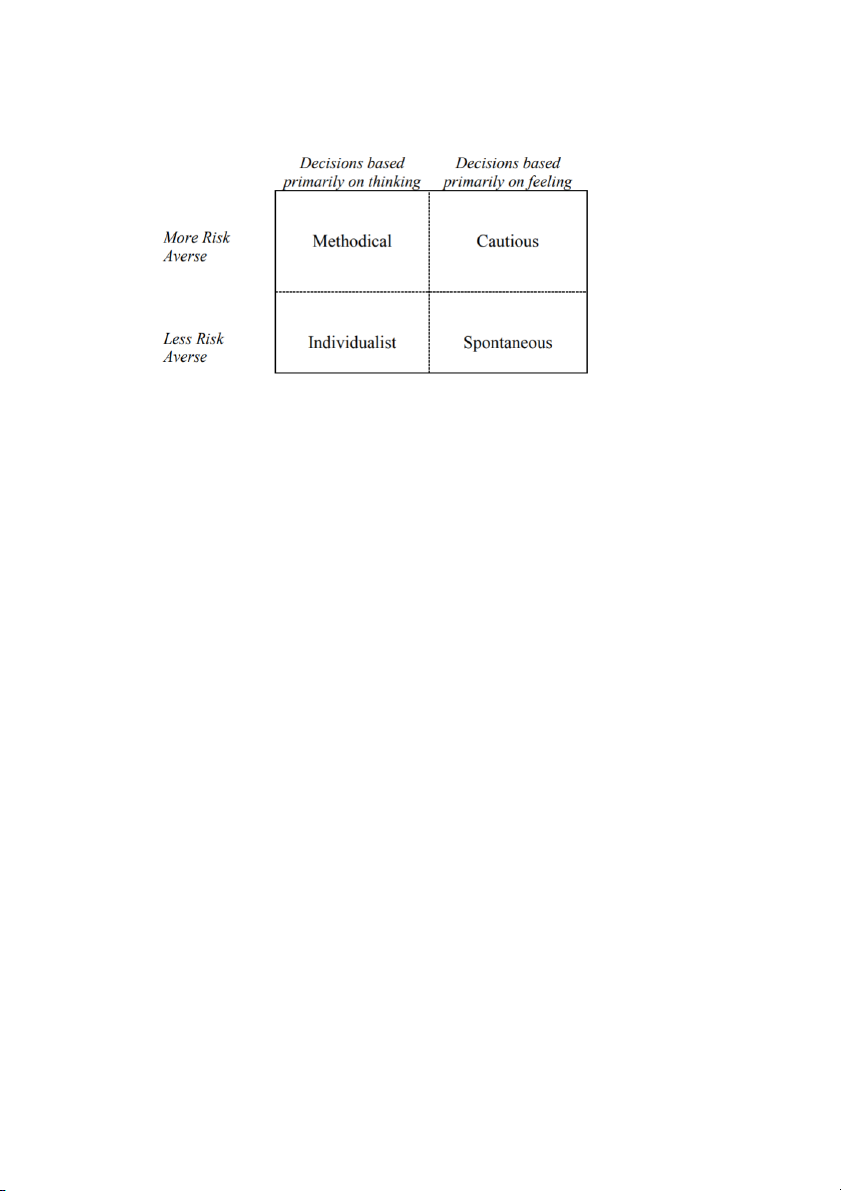

A determinant of individual investing that has generally received less focus than

other, more objective influences is the psychological process by which an individual

establishes his or her investment preferences. C Step 3:

Construct an IPS (Investment policy Statement) presents the investor’s financial objectives, the degree of risk

In the case of Peter and Hilda, it appears that their current needs are being met by

Peter’s salary of €500,000. If IngerMarine is sold, they may require a return that

replaces Peter’s salary (a critical objective) and desire a return that will

accommodate their major acquisitions and still leave their children financially

secure (important but less critical objectives).

Peter and Hilda Ingers’ investment objectives are primarily short to intermediate term in nature:

• Support for current lifestyle

• Construction of second home

• Support for Jürgen’s education

Longer term, Peter and Hilda wish to preserve the financial security that their family

currently enjoys. Preserving purchasing power is apparently more important to them than creating further wealth.

Peter’s risk-taking has clearly centered on the business risk of IngerMarine. He has

retained ownership of the company for many years, demonstrating tolerance for

business risks that he may feel he controls. In other areas, including company debt

policy and expansion plans, Peter has shown less willingness to take risk. His

personal debt policy and low volatility investment portfolio also indicate a

conservative approach to finances.

Tài liệu liên quan:

-

A Checklist For The Consumer Products Industry - Advanced Business English (ABE1) | Đại học Hoa Sen

321 161 -

CFA Institute Chartered Financial Analyst ExaminationA - Auditing (AA123) | Đại học Hoa Sen

251 126 -

Phân tích hiệu quả tài chính dự án đầu tư - Auditing (AA123) | Đại học Hoa Sen

566 283 -

Auditing and Assurance 1 - Chap 1 - Auditing (AA123) | Đại học Hoa Sen

302 151