Auditing & Assurance 1 Audit practice - Auditing (AA123) | Đại học Hoa Sen

Auditing & Assurance 1 Audit practice - Auditing (AA123) | Đại học Hoa Sen được sưu tầm và soạn thảo dưới dạng file PDF để gửi tới các bạn sinh viên cùng tham khảo, ôn tập đầy đủ kiến thức, chuẩn bị cho các buổi học thật tốt. Mời bạn đọc đón xem

Môn: Auditing (AA123) 55 tài liệu

Trường: Trường Đại học Hoa Sen 5.3 K tài liệu

Tác giả:

Preview text:

Auditing & Assurance 1 AUDIT PRACTICE CASE STUDY 1. Introduction

(1) Hoan Cau Auditing and Consulting Limited Company (HCC) is one of

Vietnam's 20 largest auditing companies. In 2015, its sales were VND 52 billion,

the total number of employees was 147 of which 12 have CPAVN. The company

provides a wide range of financial services in three areas: assurance services, tax

consulting services, and corporate consulting services. Revenue mainly comes

from the service of auditing financial statements. The company has expanded

corporate consulting and tax consulting services since 2015.

(2) You are an auditor who has 6-year experience in the field of financial

statement auditing. You have just received the CPA certificate in 2015 and were

appointed Head of Audit Department. In October 2015, you and Mr. Hung, the

company's deputy general director, joined the meeting with GoldEquip. On the

way to the GEC office, Mr. Hung told you that GEC is a US high-grade paint

manufacturing and supply company in Vietnam. GEC shares are currently traded

on HOSE. The company contacted HCC and asked HCC to provide auditing

services for its 2015 financial statements. Mr. Hung met Mr. Thanh, GEC's CEO at

a seminar in July 2015. Mr. Thanh has complained a lot about their current

auditing company. Therefore, Hung said that this is a potential client.

(3) At the meeting with HCC, Mr. Thanh said that GEC had terminated the

contract with their auditor and wished to seek a new auditing firm, which could

provide GEC with more professional audit services to meet the requirements of

UOB Bank, a bank in Singapore that they are looking for a large loan in 2016 to

use for their investment. In addition, he revealed that GEC intends to acquire a

company in the same industry and expects the new auditing firm to offer

financial advisory services. GEC is a company with many complex tax obligations.

Mr. Thanh also suggested HCC review its tax obligations and identify risks and

mistakes that would have been made.

(4) After the meeting, on the way back to the company, Mr. Hung told you that

he is very interested in this customer, as HCC not only has a large audit service

revenue but also may sign consultancy service contracts. In addition, HCC is also

seeking to increase its clients that are listed joint-stock companies. Mr. Hung

asks you to help him complete the audit procedures for risk assessment and

accept new clients. He also reminds you to carefully evaluate the risks when

deciding to accept this customer. 1

2. Information Provided

Gold Equip Corporation (GEC)

(5) GEC is one of the largest suppliers of premium paint in Vietnam. The

company was established in 2003 as a limited liability company. In 2008, the

company was equitized, and then in 2012, it was listed on Ho Chi Minh Stock

Exchange (HOSE) with the code GEC. GEC produces paints based on American

technology, with a technology transfer contract signed for 20 years with GEC

USA. GEC USA currently holds 42% of GEC Vietnam shares and is the largest shareholder.

(6) GEC paint products are of various types, divided into two groups,

construction paints, and specialized paints. The specialized paint products are

mainly sold to automobile, motorcycle, marine, and high-end furniture

companies. Because this is a high-end paint line, its price is very high in

comparison to common industrial paint products. GEC owns a company in Ho Chi

Minh City, a plant in Binh Duong, and 3 branches in Hanoi, Da Nang, and Can

Tho. Inventories are kept in the plant warehouse and 3 branch warehouses.

GEC's raw materials are 75% imported. GEC's products are sold directly to

automobile and motorcycle manufacturers in Vietnam. Other products are

distributed through dealers. GEC has 25% of its revenue in 2015 (an increase of

5% over 2014) from exports to several foreign clients, including GEC Malaysia and GEC China.

(7) Currently, due to the difficulties of the high-end paint market, GEC is

negotiating to buy ABB Paint Company to expand the market, seeking customers

in the mid-range segment. GEC wants to appoint your company as an auditor of

its financial statements for 2015. GEC is proposed to borrow $3 million from

UOB to finance the acquisition of ABB. Since 2015 is the first year GEC applied

Circular 200/2014/TT-BTC for its accounting, GEC also wants HCC to advise GEC

on some changes and effects to its financial statements. In 2015 there are many

changes in corporate income tax law, GEC expects that once its financial

statements are audited by a large and reputable auditing firm like yours, the tax

obligations for the state are satisfactory, if any errors, the audit firm will point

out and GEC is ready to adjust.

Industrial Paint Market in Vietnam

(8) The paint industry in Vietnam is in a period of fierce competition between

foreign and Vietnamese enterprises. In addition, paint products made in China

and Taiwan, with low prices and diversity are being imported with increasing

volume in Vietnam. As for the construction paint industry, the real estate market

is heating up, creating a boost for growth.

(9) Vietnamese economy has many signs of recovery and development.

However, cheap products are still easier to be accepted by the market. High-end

product lines become picky, especially when financial markets are unstable. 2

Therefore, in order to increase product competitiveness, in 2015, GEC has

strengthened the technical support system for companies using GEC paint.

GEC Development Strategy

(10) GEC's traditional products are top-quality products in the US, providing for

high-end markets such as high-end cars, motorbikes, and construction materials.

From 2014, GEC expanded the supply of powder coatings paint for wood and

furniture companies, mainly targeting high-end exporters to the fastidious

markets in the US and Europe. In March 2015, the company recruited a new

sales manager in charge of this market. He has 15 years doing business in the

field of furniture export. However, sales of this market accounted for only 5% of

total revenue in 2015 and did not meet the board's target.

(11) Recognizing the price constraints of current products, GEC's CEO proposed

to buy a Vietnamese paint manufacturer, in the middle segment. The CEO said

that after acquiring the company, GEC would be able to expand this segment

without affecting the brand of existing brands. GEC has contacted potential

buyers and is looking for a financial services company to assist them in this deal.

Currently, this information has not been disclosed so it has not impacted GEC stock prices yet. Accounting Policy

(12) GEC chief accountant stated that GEC has implemented its accounting

policies in accordance with Circular 200/2014/TT-BTC. Some policies are described as follows:

(13) Depreciation policy: GEC applies straight-line depreciation for all fixed

assets. Depreciation is applied according to the Group's guidelines for consolidation.

(14) Credit policy: Because most of the sales are subject to 30-60 days of debt

termination, the company's receivables are quite large. Some of the company's

traditional clients have overdue debt. They have sent their written request to ask

GEC to extend the 90-day deferred payment since GEC rivals have raised their

credit term to 90-120 days. However, GEC did not set up allowances for bad debt

for these accounts at the end of the year as the CFO said that it was possible to collect these debts.

(15) Sales policy: GEC has domestic and export sales. For domestic customers,

the goods are delivered at customers' warehouses, with delivery times generally

no more than 24 hours. Export contracts are commonly FOB Sai Gon prices,

except for contracts signed with GEC Malaysia and GEC China which are EXW

prices. The chief accountant indicates the time to record revenue is when the

goods are out of GEC warehouses.

(16) Purchasing policy: 75% of GEC purchases are from GEC USA and GEC China

at CIF prices. Shipping time is usually 10 days (for GEC China) to 30 days (for GEC 3

USA). The purchases are recorded after they are checked and put into the warehouses.

Internal Control System

(17) The Internal Audit Director told that GEC Vietnam's policy of control is in full

compliance with the Group policies. The internal audit department consists of

one director and four staff members. In addition, there is 1 internal auditor at

each plant and branch. The report of the internal audit department is sent

directly to the CEO every month. In addition, the quarterly consolidated report

will be sent to the Board of Supervisors, which will be the basis for the Board of

Supervisors to check and review at the beginning of the following quarter. Every

year, the Group's internal audit team will visit Vietnam to audit

policies. The year-end audit report of the internal audit department only

recorded a minor error of the warehouse division. After investigation, it was

determined that the lack of goods was due to

while checking the goods. Because this is the first violation and the amount is

not large so the storekeeper was only reprimanded.

(18) The Internal Audit Director also indicated that the risk of fraud at GEC is very

low because the company had a rigorous control process and operational cycles

were subdivided into specialized divisions. The company policy also requires

cross-checking and cross-reconciling between departments every month. All of

the reconciliations are documented and stored in the department.

(19) GEC currently uses Oracle's ERP system for all departments. The Internal

Audit Director is very proud of the modern software system the company has

recently invested nearly $100,000 in 2015. He said the system can handle and

control automation at multiple stages, It has helped the company reduce input,

provide information quickly, and support decision-making. He believes that with

the rigorous controls of this system, the risk of error and fraud is very low, if not

impossible. However, applying a new system, the work of the internal audit

department is overloaded. The Internal Audit Director thinks that he needs an

additional staff member with information technology expertise but the HR

department disagreed even though he had suggested several times. Upon

hearing this information, the CEO said that he was completely unaware of this

and that he would consider and direct the department for additional recruitment.

3. Financial Statements of 2015:

(20) Including the Balance Sheet and the Income Statement. QUESTIONS: 1.

accepting a new customer. Given the current professional ethics regulations,

should HCC accept this customer? 4

2. Based on the information provided about the internal control system, evaluate

3. Use the financial information provided by GEC, present the initial analytical

procedures by applying trend analysis and calculating ratios including liquidity,

turnover, profitability, and solvency (as forms below). What does this procedure

mean for an auditor? Point out abnormal items in GEC financial statements the

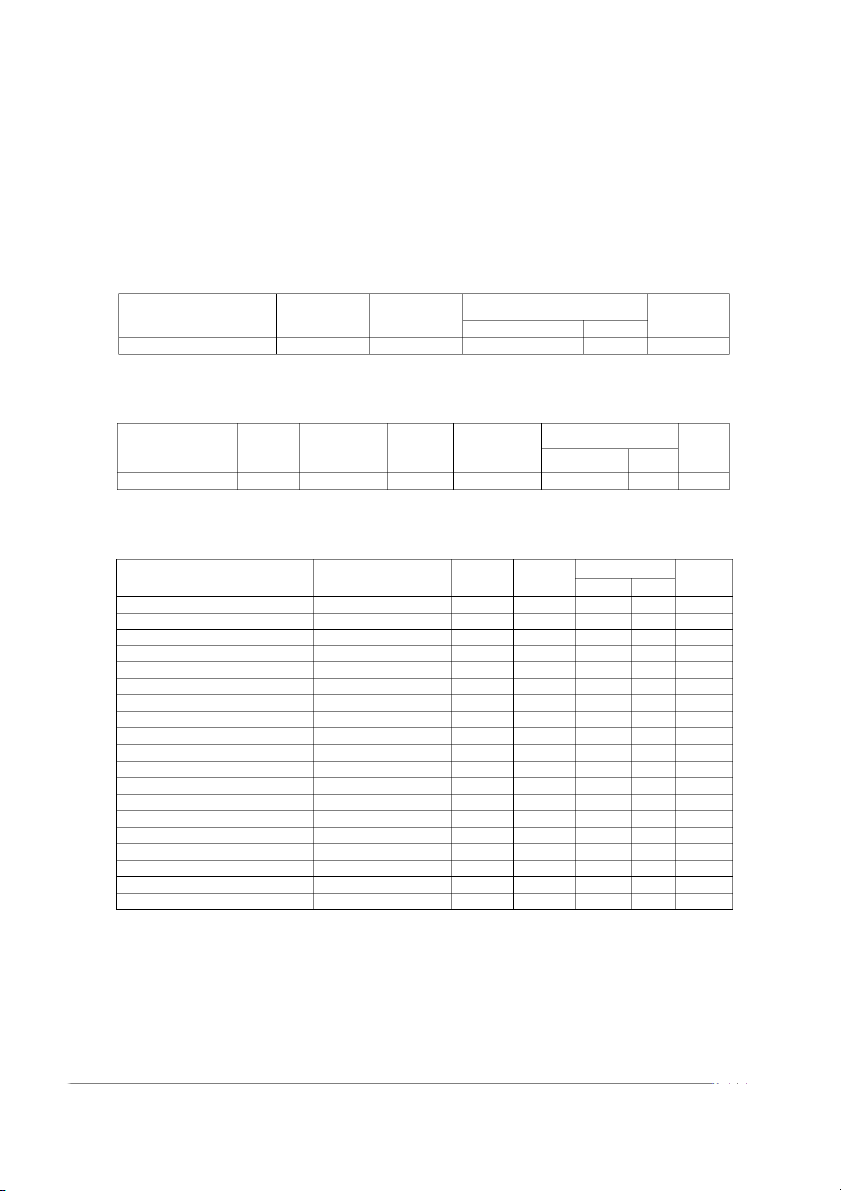

auditor should have an intensive investigation. BALANCE SHEET Variation Items Year 2015 Year 2014 VND % Notes INCOME STATEMENT Percentage Percentage Variation Year of net Year of net Items 2015 revenue 2014 revenue VND % Notes RATIO ANALYSIS Year Year Variation Common ratios Formulas 2015 2014 VND % Notes Liquidity ratios Current ratio Quick ratio Cash ratio Activity ratios Receivable turnover Inventory turnover Working capital turnover Profitability ratios Gross margin Net profit margin Revenues on total assets Return on assets Return on equity Solvency ratios

Long-term liabilities to equity Total liabilities to equity

Long-term liabilities to asset

Total liabilities to total assets

4. Risk assessment is a very important procedure, often reviewed by an auditor and

a member of the board of directors of an audit firm. From the information given

above, identify GEC's risks and determine the audit risk. Calculate planning and

performance materiality in your audit plan. 5

5. Accepting a new client is a complex process based on the audit assessment

of the company's risk. Explain procedures performed by the auditor to make a

decision whether to receive GEC client?

6. From the results of the risk assessment above, prepare an audit program for the identified risks. REQUIRED:

1) All groups must do the work (answer the 6 questions above). Submit your work

on m-learning. Each group, each file only. Deadline: Week 15. (20% of formative

assessment, 10% of marks deducted for each day late)

2) Presentation topics are assigned using your random choices. Produce a video clip

for your presentation, upload it on YouTube, then submit the link on m-learning

in Week 15. (20% of formative assessment, 10% of marks deducted for each day late) 6

Tài liệu liên quan:

-

A Checklist For The Consumer Products Industry - Advanced Business English (ABE1) | Đại học Hoa Sen

327 164 -

CFA Institute Chartered Financial Analyst ExaminationA - Auditing (AA123) | Đại học Hoa Sen

255 128 -

Sample Questions case study sample answer - Auditing (AA123) | Đại học Hoa Sen

305 153 -

Phân tích hiệu quả tài chính dự án đầu tư - Auditing (AA123) | Đại học Hoa Sen

575 288 -

Auditing and Assurance 1 - Chap 1 - Auditing (AA123) | Đại học Hoa Sen

305 153