NCKH ABCXYC ABCIEJJSDFHGDSKJHFDSH

TÀI LIỆU HAY VÀ CUNG CẤP THÔNG TIN VỀ KHÍ HẬU RỦI O

Môn: Quản trị dự án 40 tài liệu

Trường: Trường Đại học Kinh Tế Quốc Dân 8.9 K tài liệu

Tác giả:

Preview text:

Received: 5 February 2023 Revised: 8 September 2023 Accepted: 25 November 2023 DOI: 10.1002/bse.3649 R E S E A R C H A R T I C L E

Climate change disclosure and evolving institutional investor

salience: Roles of the Principles for Responsible Investment Kentaro Azuma 1 | Akira Higashida 2

1Ritsumeikan University, Osaka, Japan 2 Abstract

Meijo University, Nagoya, Japan

This study investigates the relationship between climate change disclosure and insti- Correspondence

tutional investors. A particular focus of the present study is the question of if and

Kentaro Azuma, College of Business

Administration, Ritsumeikan University, 2-150

how the relationship is affected by the Principles for Responsible Investment (PRI). A

Iwakura, Ibaraki, Osaka 567-8570, Japan.

relevant context to the question is shareholder engagement, where institutional

Email: kentaro@fc.ritsumei.ac.jp

investors' legitimacy affects the outcomes. Thus, this study examines Japan, where Funding information

shareholder engagement is the main pathway for institutional investors to convey

Kakenhi, Grant/Award Numbers: 19H01547, 22K01824

their ESG-related influence to investee companies. Using the stakeholder salience

theory as a theoretical framework, the empirical results of analyzing 17,604 firm-year

eXtensible Business Reporting Language (XBRL) documents of listed Japanese com-

panies provide evidence for the following. First, institutional stakeholders' holding

ratio has positively influenced corporate climate change disclosure (power). Second,

the positive influence of institutional investors is more significant when PRI-signed

institutional investors are present (legitimacy). Third, the aforementioned relations

gained statistical significance gradually during the analysis period (urgency). Funda-

mentally, this study shows that the stakeholder salience theory contributes to a dee-

per understanding of the relationship. K E Y W O R D S

climate change disclosure, ESG investment, institutional investors, PRI, shareholder

engagement, stakeholder salience theory 1 | I N T R O D U C T I O N

significant financial effects. The capital market needs corporate disclo-

sure about risks and opportunities related to climate change (hereafter

As the threat of climate change to human beings becomes more evi-

climate change disclosure), and the practice is currently under expan-

dent and real (IPCC, 2022), associated risks and opportunities are

sion. Prompted by the rise of ESG (Environment, Social, and Gover-

becoming more acute for corporate activities. How companies

nance) investing, initiatives including the Task Force on Climate-

address the problems of climate change potentially generates

Related Financial Disclosures (TCFD), the Sustainability Accounting

Standards Board (SASB), and the International Sustainability Standards

Board (ISSB) are engaged in establishing frameworks for climate

Abbreviations: CSR, Corporate Social Responsibility; ESG, Environment, Social, and change disclosure (Amir & Serafeim, 2018; O'Dwyer &

Governance; PRI, Principles for Responsible Investment; XBRL, eXtensible Business Reporting Language. Unerman, 2020).

This is an open access article under the terms of the Creative Commons Attribution-NonCommercial-NoDerivs License, which permits use and distribution in any

medium, provided the original work is properly cited, the use is non-commercial and no modifications or adaptations are made.

© 2024 The Authors. Business Strategy and The Environment published by ERP Environment and John Wiley & Sons Ltd.

Bus Strat Env. 2024;33:3669–3686.

wileyonlinelibrary.com/journal/bse 3669

10990836, 2024, 4, Downloaded from https://onlinelibrary.wiley.com/doi/10.1002/bse.3649 by Readcube (Labtiva Inc.), Wiley Online Library on [07/03/2026]. See the Terms and Conditions (https://onlinelibrary.wiley.com/terms-and-conditions) on Wiley Online Library for rules of use; OA articles are governed by the applicable Creative Commons License 3670 AZUMA and HIGASHIDA T A B L E 1

The six principles for responsible investment. (1)

We will incorporate ESG issues into investment analysis and decision-making processes. (2)

We will be active owners and incorporate ESG issues into our ownership policies and practices. (3)

We will seek appropriate disclosure on ESG issues by the entities in which we invest. (4)

We will promote acceptance and implementation of the Principles within the investment industry. (5)

We will work together to enhance our effectiveness in implementing the Principles. (6)

We will each report on our activities and progress toward implementing the Principles. Note: Emphasis by authors.

Regarding climate change disclosure, previous literature has

2021; Jaggi et al., 2018; Liesen et al., 2015; Stanny & Ely, 2008),

explored diverse perspectives. The drivers, which had previously been

addressing the following research gaps.

explored, include institutional settings (Kolk et al., 2008) such as emis-

First, the Principles for Responsible Investment (PRI), an influential

sion trading schemes (Comyns & Figge, 2015), local greenhouse gas

platform for institutional investors in engaging with ESG investing, has

regulations (Reid & Toffel, 2009), and non-mandatory disclosure guid-

not been considered in the relationship between climate change disclo-

ance (Tauringana & Chithambo, 2015). The literature also points to

sure and institutional investors. As of January 2022, 3826 signatories

firm-specific drivers such as independence and diversity of board

with a total of US$121.3 trillion assets under management have joined

directors (Bui et al., 2020; Liao et al., 2015), explicit Corporate Social

the initiative.1 The PRI states its six principles as presented in Table 1.

Responsibility (CSR) practices (Hsueh, 2019), board effectiveness

The third principle explicitly articulates the goal of seeking ESG disclo-

(Ben-Amar & McIlkenny, 2015), environmental committees (Peters &

sure, of which climate change disclosure is a significant component.

Romi, 2014), internal organizations (Rankin et al., 2011), corporate vis-

Expecting that the PRI is playing a considerable role in the recent growth

ibility (Dawkins & Fraas, 2011), and greenhouse gas performance

of climate change disclosure, this study aims to capture its effect. Studies

(Cong et al., 2020; Giannarakis et al., 2017; Luo & Tang, 2014).

have demonstrated that signing the PRI has a significant effect on institu-

Following such studies, institutional investors are gradually arising

tional investors, such as facilitating their collective actions (Gond &

as an additional determinant for climate change disclosure. Practically,

Piani, 2013), enhancing their ESG performance (Bauckloh et al., 2021),

the strengthening of climate change-related policies (Pfeifer &

and improving their investees' ESG performance (Brandon et al., 2022;

Sullivan, 2008) and urges from environmental Non-Governmental

Dyck et al., 2019). Adding to the PRI literature, this study addresses the

Organizations (NGOs) such as CDP (Cotter & Najah, 2012; Kolk et al.,

empirical question of “whether institutional investors' signing the PRI will

2008) made institutional investors keen on climate risks and opportu-

affect their influence on climate change disclosure,” which has not been

nities (Krueger et al., 2020; Solomon et al., 2011). Institutional

explored in previous studies to the best of our knowledge.

investors have more experience and resources than non-institutional

To understand how the PRI moderate the relationship between

investors and are more likely to influence corporate disclosure

climate change disclosure and institutional investors, we leverage (Velte, 2022).

stakeholder salience theory (Mitchell et al., 1997), a derivative of

Theoretically, the literature provides two lines of explanation on

stakeholder theory (Freeman, 1984). We posit that this theory aptly

the mechanisms behind institutional investors' influence on climate

addresses the identified research gap. Within the realm of shareholder

change disclosure. One approach is voluntary disclosure theory

engagement, institutional investors influence managerial decisions

(Verrecchia, 1983); institutional investors have resources for higher

through private dialogs. Their legitimacy stands pivotal for effective

levels of scrutiny, and their monitoring increases companies' costs for

communication (Gifford, 2010; Wagemans et al., 2018). By signing the

not disclosing climate change-related information (Stanny & Ely, 2008).

PRI, institutional investors can potentially augment their legitimacy

Thus, companies are more likely to respond with climate change disclo-

(Bauckloh et al., 2021; Majoch et al., 2017)—a point further elucidated

sure when institutional investors are involved with the claims despite

in the theoretical framework section. Given the growing roster of PRI

the potential revelation of vulnerabilities (Flammer et al., 2021).

signatories in recent years, it is prudent to span our analysis over this

Another approach is stakeholder theory, which this study is based

period to capture shifts in investors' legitimacy. This extended time-

on. This approach views social and environmental disclosure as deter-

frame also illuminates the evolving urgency of their claims. Prior litera-

mined, among others, by stakeholders' power, that is, degree of con-

ture on institutional investors' impact on climate change disclosure

trol over the resource required by the company (Deegan, 2002;

(Cotter & Najah, 2012; Depoers et al., 2016; Jaggi et al., 2018; Liesen

Roberts, 1992; Ullmann, 1985). Capturing the relative extent of the

et al., 2015) and the broader nexus between stakeholders and CSR

power by ownership ratio, the line of literature evidences the positive

disclosure (Deegan, 2002; Roberts, 1992; Ullmann, 1985) primarily

relationship between institutional investors' power and climate change

highlighted stakeholders' power as the sole determinant. By utilizing

disclosure (Cotter & Najah, 2012; Depoers et al., 2016; Jaggi et al.,

stakeholder salience theory—which encompasses legitimacy and 2018; Liesen et al., 2015).

urgency alongside power, previously the sole focus of earlier studies—

This study aims to extend the body of the literature investigating

this research seeks to broaden the scope of analysis.

the relationship between institutional investors and climate change

disclosure (Cotter & Najah, 2012; Depoers et al., 2016; Flammer et al.,

1https://www.unpri.org/pri/about-the-pri (last accessed on January 4, 2022).

10990836, 2024, 4, Downloaded from https://onlinelibrary.wiley.com/doi/10.1002/bse.3649 by Readcube (Labtiva Inc.), Wiley Online Library on [07/03/2026]. See the Terms and Conditions (https://onlinelibrary.wiley.com/terms-and-conditions) on Wiley Online Library for rules of use; OA articles are governed by the applicable Creative Commons License AZUMA and HIGASHIDA 3671

Stakeholder salience theory has been widely applied to share-

emerges as the predominant mechanism. It is within this unique land-

holder activism (David et al., 2007), secondary stakeholder actions

scape that enhancing institutional investors' legitimacy via PRI signing

(Eesley & Lenox, 2006), natural environment (Haigh & Griffiths, 2009),

may further bolster their sway over climate change disclosure.

ESG disclosure (Aluchna et al., 2022), and corporate social and sustain-

While the EU and Japan share similarities in their subordinate use

ability reports (Weber & Marley, 2012) (see Joos, 2019, for a review).

of shareholder proposals, they markedly differ in the format and avail-

Adding to these lines of research, we apply this theory to the relation-

ability of disclosure data for analyses. In the European context, disclo-

ship between institutional investors and climate change disclosure.

sure documents, which include annual reports and CSR reports, are

Second, previous studies investigating institutional investors'

typically available in discretionary formats like PDF or HTML on indi-

influence on climate change disclosure are geographically unevenly

vidual corporate websites. Consequently, prior studies exploring the

distributed. The majority of the studies have investigated the US

European setting often relied on datasets manually assembled from

(Flammer et al., 2021; Stanny & Ely, 2008), European (Depoers et al.,

corporate reports (Depoers et al., 2016; Liesen et al., 2015) or sourced

2016; Jaggi et al., 2018; Liesen et al., 2015), and global settings

from third-party organizations such as CDP (Jaggi et al., 2018).

(Cotter & Najah, 2012), but analogous studies have not been con-

Japan's setting, on the other hand, presents a distinct methodo-

ducted in Asian settings. In general, climate change disclosure has

logical opportunity: the application of digitally assisted text analysis

been rarely studied in Asian settings except for China (Li et al., 2018),

using a web-scraped dataset. In the Japanese context, listed compa-

and the topics in Japanese settings have been addressed only in a few

nies are mandated to file Annual Securities Reports (ASR: Yukashoken

studies such as Saka and Oshika (2014) and Nishitani and Kokubu

Hokokusho). These reports are centrally archived on the EDINET por-

(2012). We aim to narrow this gap by studying the relationship in

tal,5 overseen by Japan's Financial Service Agency (FSA). What's piv- Japanese settings.

otal is the standardization in the format of these reports. The original

The empirical focus on Japan in this study offers unique insights

files are uniformly stored in XBRL (eXtensible Business Reporting into the literature, especially when juxtaposed against the

Language),6 a digital language that enables mass downloads via an

United States and the EU. Distinctly in Japan, institutional investors'

Application Programming Interface (API). This technological infrastruc-

engagement can be seen as the primary means of influencing climate

ture in Japan provides a conducive environment for quantitative anal-

change disclosure. Broadly speaking, institutional investors' influence

ysis involving larger datasets (Bai et al., 2014).

on their investee companies manifests in two main ways: through the

Furthermore, Japan has yet to regulate ESG (non-financial) disclo-

often distant and adversarial tactics of shareholder activism and

sures directed at investors in contrast to Europe. ESG disclosure in

through more engaged, collaborative relationships with companies,

ASR, the main disclosure document for investors, has remained free

known as shareholder engagement (Majoch et al., 2012; McNulty &

from specific non-financial reporting regulations. The Ministry of the

Nordberg, 2016). In the US context, the former typically manifests as

Environment pioneered the “Guidelines for Environmental Reports”7

shareholder proposals, addressing a range of social and environmental

in 2000. This initiative catalyzed an uptick in environmental disclo-

issues (O'Rourke, 2003). Prior research has delved into how such pro-

sures among prominent Japanese corporations. However, such

posals influence US firms' disclosures on climate change strategies

disclosures have predominantly been confined to voluntary public

(Reid & Toffel, 2009), associated risks (Flammer et al., 2021), and

communications, such as CSR/sustainability reports. In contrast, the

broader CSR initiatives (Michelon et al., 2020).

incorporation of ESG disclosure within the ASR is still in the delibera-

In stark contrast, Japan rarely employs this adversarial pathway.

tion phase for the regulatory establishment, leading to continued vari-

Japanese shareholder proposals often adopt a narrower focus, rarely

ability in disclosure practices among companies regarding both the

encompassing ESG matters (Saito, 2012).2 Emphasis on the signifi-

decision to disclose and the extent of the disclosure related to climate

cance of ESG-related shareholder engagement in Japan has been

change. It is only after the financial years concluding after March

highlighted in scholarly works (Clark et al., 2015; Solomon et al.,

2023 that such ESG disclosures in ASR are expected to be

2004). This approach aligns with initiatives such as the “Principles for

incorporated, which remains beyond the purview of this research. This

Responsible Institutional Investors, Japan's Stewardship Code.”3

contrasts with European settings with a structured approach to non-

Notably, during our study period (2017–2022), ESG-related share-

financial disclosure, especially following the advent of the Non-

holder proposals were seldom put forth in Japan.4 This marks Japan's

Financial Reporting Directive 2014/95/EU (NFRD). This particularity

distinct approach from the United States: Shareholder engagement

in the Japanese framework provides scholars with an environment

where the regulatory effect on climate change disclosures can be dis-

2Anti-nuclear proposals submitted to the power companies as a notable exception tinctly excluded. (Saito, 2012).

The remainder of this paper is organized as follows. Section 2

3An English version of the Code is available under the following link: https://www.fsa.go.jp/

presents the theoretical background and hypotheses development.

en/refer/councils/stewardship/20140407/01.pdf (last accessed on October 13, 2022).

4According to our search in Nikkei Shimbun, a leading Japanese business newspaper, the first

Section 3 describes the research methods. Section 4 presents the

shareholder proposal explicitly related to climate change submitted by a Japanese company

empirical results. Finally, Section 5 concludes the paper by

was the climate change case of Mizuho Financial Group in June 2020. https://www.nikkei.

com/article/DGXMZO60766070V20C20A6EE9000/?type=my#QAAKAgAqMA (last

accessed on July 10, 2023). This is significantly different from the dataset used in previous

5https://disclosure2.edinet-fsa.go.jp/WEEK0020.aspx (last accessed on July 10, 2023)

studies; Michelon and Rodrigue (2015), for instance, stated that the first climate change-

6https://www.xbrl.org (last accessed on August 16, 2022).

related shareholder proposal was found as early as 2001 with international data.

7https://www.env.go.jp/policy/report/h12-02/index.html (last accessed on July 10, 2023).

10990836, 2024, 4, Downloaded from https://onlinelibrary.wiley.com/doi/10.1002/bse.3649 by Readcube (Labtiva Inc.), Wiley Online Library on [07/03/2026]. See the Terms and Conditions (https://onlinelibrary.wiley.com/terms-and-conditions) on Wiley Online Library for rules of use; OA articles are governed by the applicable Creative Commons License 3672 AZUMA and HIGASHIDA

summarizing the findings and discussing the contributions and limita-

understanding, empirical studies have predominantly adopted the tions of this study.

ownership ratio as an indicator to gauge the power exerted by institu-

tional investors (Cotter & Najah, 2012; Depoers et al., 2016; Liesen

et al., 2015; Pfeifer & Sullivan, 2008). 2 |

T H E O R E T I C A L F R A M E W O R K A N D

A substantive body of literature underscores that the positive H Y P O T H E S E S

influence of institutional investors' power on corporate sustainability

(for a comprehensive review, see Velte, 2022). Empirical investiga-

This research is anchored in stakeholder theory, which envisions a

tions illustrate that higher ownership ratios by institutional investors

corporation not as a solitary unit but as an entity interwoven within

often lead to enhanced environmental and social performance (Dyck

a nexus of diverse stakeholder groups (Freeman, 1984). The broad

et al., 2019), as well as improved CSR ratings (Chen et al., 2020;

applicability of stakeholder theory is evident across multifarious busi-

Motta & Uchida, 2018). Interestingly, the positive correlation between

ness research areas (refer to Mahajan et al., 2023, for a comprehen-

institutional investors' shareholding and social performance is found

sive review), with CSR disclosure being one prominent domain (Gray

to be further amplified when investors actively engage in activism

et al., 1995a). A descriptive branch of the stakeholder theory (Neubaum & Zahra, 2006).

(Deegan, 2011) accentuates the power of stakeholders as a pivotal

Furthermore, the proportion of shares held by institutional inves-

driver for CSR disclosure (Roberts, 1992; Ullmann, 1985). In line with

tors has been linked to better greenhouse gas performance (Benlemlih

this perspective, prior research probing the sway of institutional

et al., 2023), a higher likelihood of employing sustainability assurance

investors over climate change disclosure predominantly focused on

services (García-Sánchez et al., 2022), adoption of robust environmen-

their power, which is often manifested as ownership proportions

tal strategies (Wahba, 2010), and an inclination toward eco-innovation

(Cotter & Najah, 2012; Depoers et al., 2016; Liesen et al., 2015). This

(García-Sánchez et al., 2020). Recognizing that institutional investors

research aligns with and expands the framework delineated by these

are not a monolithic group and encompass entities with diverse inter- antecedent studies.

ests and incentives, several studies have delved deeper to distinguish

Beyond the foundational stakeholder theory that emphasizes

effects based on subcategories. For instance, differences are dis-

stakeholders' power, this research integrates the stakeholder salience

cerned based on the specific type of financial institution (Johnson &

theory (Mitchell et al., 1997). This theory suggests that managerial

Greening, 1999; Garcia-Sanchez et al., 2020) or the duration for which

reactions to stakeholder demands are governed by the perceived

they hold onto their investments (Cox et al., 2004; Li & Lu, 2016).

salience of these stakeholders, a salience derived from a triad of attri-

However, the consensus about the role of institutional investors'

butes: power, legitimacy, and urgency. Each of these attributes will be

power on corporate sustainability is far from universal. A set of stud-

elaborated upon in subsequent sections.

ies, especially from the early 1990s, failed to observe a significant

impact of institutional ownership on various aspects of corporate

responsibility. For instance, no significant effect was found on charita- 2.1 | Power

ble contributions (Coffey & Fryxell, 1991) or broader measures of cor-

porate social performance (Graves & Waddock, 1994). Contemporary

The concept of power as a pivotal determinant is well-established

findings still echo some of these reservations. Researchers have

in the literature, especially when applying stakeholder theory

observed that institutional ownership did not necessarily drive the

(Freeman, 1984) to CSR disclosure (Gray et al., 1995a; Roberts, 1992;

adoption of CSR practices (Ducassy & Montandrau, 2015), nor did it

Ullmann, 1985). This literature identifies power as the capacity to

stimulate the implementation of robust carbon management strate-

command resources upon which a company depends, drawing insights

gies (Yunus et al., 2020) or encourage environmental proactivity

from Salancik and Pfeffer (1974). In articulating the stakeholder

(Calza et al., 2014). Moreover, David et al. (2007) made a contention

salience theory, Mitchell et al. (1997) referenced a taxonomy pro-

that shareholder activism might even be counterproductive for corpo-

posed by Etzioni (1964) that delineates three forms of power: coer-

rate social performance. The argument is that addressing activism

cive, normative, and utilitarian.

could potentially divert critical organizational resources away from

While coercive power is exercised through physical means, sustainability objectives.

encompassing force, and even violence, normative power taps into

Yet, a more consistent narrative emerges when it comes to the

societal symbols, invoking notions of prestige and esteem. Utilitarian

narrower domain, i.e., climate change disclosure. The prevalent view

power is of particular relevance to institutional investors. Rooted in

in recent studies is that institutional investors' power, as quantified by

financial mechanisms of control, this form of power is often quantified

ownership percentages, exerts a positive influence. Empirical evidence

in terms of share ownership within a company. A substantial owner-

from Cotter and Najah (2012) underscores that the ownership ratio of

ship percentage signifies a higher capital infusion into the company

institutional investors enhances climate change disclosure, especially

and endows the investor with amplified voting privileges (voice

through communication channels like the CDP. This positive correla-

options). Equally, a higher ownership percentage implies a potent

tion retains its hold even in specialized contexts, such as disclosures

threat of capital withdrawal through divestments, exerting indirect

around GHG emissions (Liesen et al., 2015) or sectors known for their influence (exit options) (Hirschman, 1970). Reflecting this

significant environmental footprint (Jaggi et al., 2018).

10990836, 2024, 4, Downloaded from https://onlinelibrary.wiley.com/doi/10.1002/bse.3649 by Readcube (Labtiva Inc.), Wiley Online Library on [07/03/2026]. See the Terms and Conditions (https://onlinelibrary.wiley.com/terms-and-conditions) on Wiley Online Library for rules of use; OA articles are governed by the applicable Creative Commons License AZUMA and HIGASHIDA 3673

In line with this body of research, our study posits that the power

investing, mainly after the 2010s (Alda, 2021). Climate change disclo-

vested in institutional investors is best mirrored by their ownership

sure, which is one of the major areas of disclosure needed for ESG

stakes in the firms they invest in. Drawing upon these insights and

investing, is a new domain for institutional investors (Krueger et al.,

building upon prior research, we posit that institutional investors'

2020), and therefore, institutional investors may be inclined to man-

power will act as a catalyst in promoting climate change disclosure.

age their legitimacy in the area. Particularly in the context of share-

This leads us to our first hypothesis:

holder engagement, where institutional investors hold private

communications and dialogs with corporate managers to elicit their

Hypothesis 1. Institutional investors' holding ratio posi-

demands from the companies they invest in, their legitimacy is essen-

tively affects climate change disclosure.

tial in determining the outcome (Gifford, 2010; Wagemans et al.,

2018). This setting is particularly important for Japan, which is an

empirical setting of this study. 2.2 | Legitimacy

Signing the PRI is one way for institutional investors to extend

their legitimacy. Since its launch in 2005, the PRI has constantly been

If we take Hypothesis 1 as a given, then it suggests that there are fac-

expanding its presence in the global sustainable financial system

tors beyond mere power that shape the extent of institutional inves-

under the support of the United Nations. The PRI is an institutional

tors' impact. Based on the framework of Mitchell et al. (1997), we

infrastructure that has successfully encouraged institutional investors

posit that institutional investors with extended legitimacy generate

to undertake responsible investment (Sievänen et al., 2013). The PRI

more significant influence than those without. Specifically, this study

signing may enhance institutional investors' legitimacy from substan-

focuses on the legitimacy extension of institutional investors' signing

tive and symbolic perspectives. From the substantive viewpoint, sign- the PRI.

ing the PRI creates real and material changes. To be qualified as a

Mitchell et al. (1997) proposed that more legitimate stakeholders

signatory, the institutional investor must meet the minimum require-

are likelier to prompt positive firm responses. They define legitimacy

ments set by the PRI, and failing to meet the requirement results in

as “a generalized perception or assumption that the actions of an

delisting.8 Previous literature reports that signing the PRI generates

entity are desirable, proper, or appropriate within some socially

substantive changes in institutional investors, such as facilitation of

constructed system of norms, values, beliefs, and definitions”

collective actions (Gond & Piani, 2013), improvement of their ESG

(Suchman, 1995). The concept is applied to the legitimacy of organiza-

performance (Bauckloh et al., 2021), and investment in companies

tional standing and the legitimacy of their claims (Eesley &

with better ESG performance (Brandon et al., 2022; Dyck et al.,

Lenox, 2006; Gifford, 2010). While the main emphasis of this study is

2019). From the symbolic viewpoint, organizations use signing the PRI

on the legitimacy of an organization's standing, it is intrinsically linked

to portray themselves as consistent with social values and expecta-

to the legitimacy of its claims. Consequently, both forms are pertinent

tions. Being labeled as “PRI signatories,” the signed institutional inves- to this investigation.

tors can “borrow legitimacy” (Mattingly & Westover, 2015) from the

Organizations strategically manage their legitimacy (Dowling &

PRI, which is backed by a globally well-known organization in environ-

Pfeffer, 1975), and one context in which they attempt to extend their

mental protection, the United Nations (Bernstein, 2004). Consistently,

legitimacy is when entering new domains of activities (Ashforth &

Majoch et al. (2017) indicated that institutional investors' motivation

Gibbs, 1990). Extending legitimacy, managers typically lean toward the

to sign lies in the PRI's organizational legitimacy. Thus, institutional

flexibility and economy of symbolic management, whereas their stake-

investors are expected to extend their legitimacy by signing the PRI.

holders tend to favor more substantive actions (Suchman, 1995). One

In summary, institutional investors have incentives to sign the PRI

concrete path to enhancing organizational legitimacy is an endorse-

that will result in their legitimacy extension on substantive and sym-

ment of the commitment by a reputable third party (Doh et al., 2010),

bolic levels. Corporate managers perceive the extended legitimacy of

which is a mechanism used in numerous ways in sustainability issues.

the PRI-signed institutional investors because of their endorsed com-

The most widely known example is “certification” such as eco-label

mitment to ESG investing that their signing of the PRI signals. As

(Darnall et al., 2018) and sustainability certifications (Richards et al.,

stakeholders with extended legitimacy will generate greater influence

2017). Further examples are social indexes (Doh et al., 2010),

on companies (Mitchell et al., 1997), especially in engagement-

voluntary agreement with the government (Delmas & Montes-

oriented settings (Gifford, 2010; Wagemans et al., 2018) like Japan

Sancho, 2010), and participation in self-regulatory codes of conduct

(Clark et al., 2015; Solomon et al., 2004), this study predicts that the (Perez-Batres et al., 2012).

presence of PRI-signed institutional investors strengthens the rela-

This study aims to add institutional investors' signing the PRI to

tionship between institutional investors' power and climate change

the line of the literature about legitimacy extension by reputable third

disclosure. Our second hypothesis is presented below.

parties' endorsements. During the initial period when social and envi-

ronmental issues began to be considered on the stock market, in the

8The minimum requirements include setting out a responsible investment policy covering

latter half of the 1900s, only SRI funds with particular social interests

over 50% of AUM (Assets Under Management), senior-level oversight, and internal/external

staff implementing responsible investment. https://www.unpri.org/reporting-and-

were involved in this relatively limited wave. Mainstream institutional

assessment/minimum-requirements-for-investor-membership/315.article (last accessed on

investors started joining this stream along with the rise of ESG August 3, 2022).

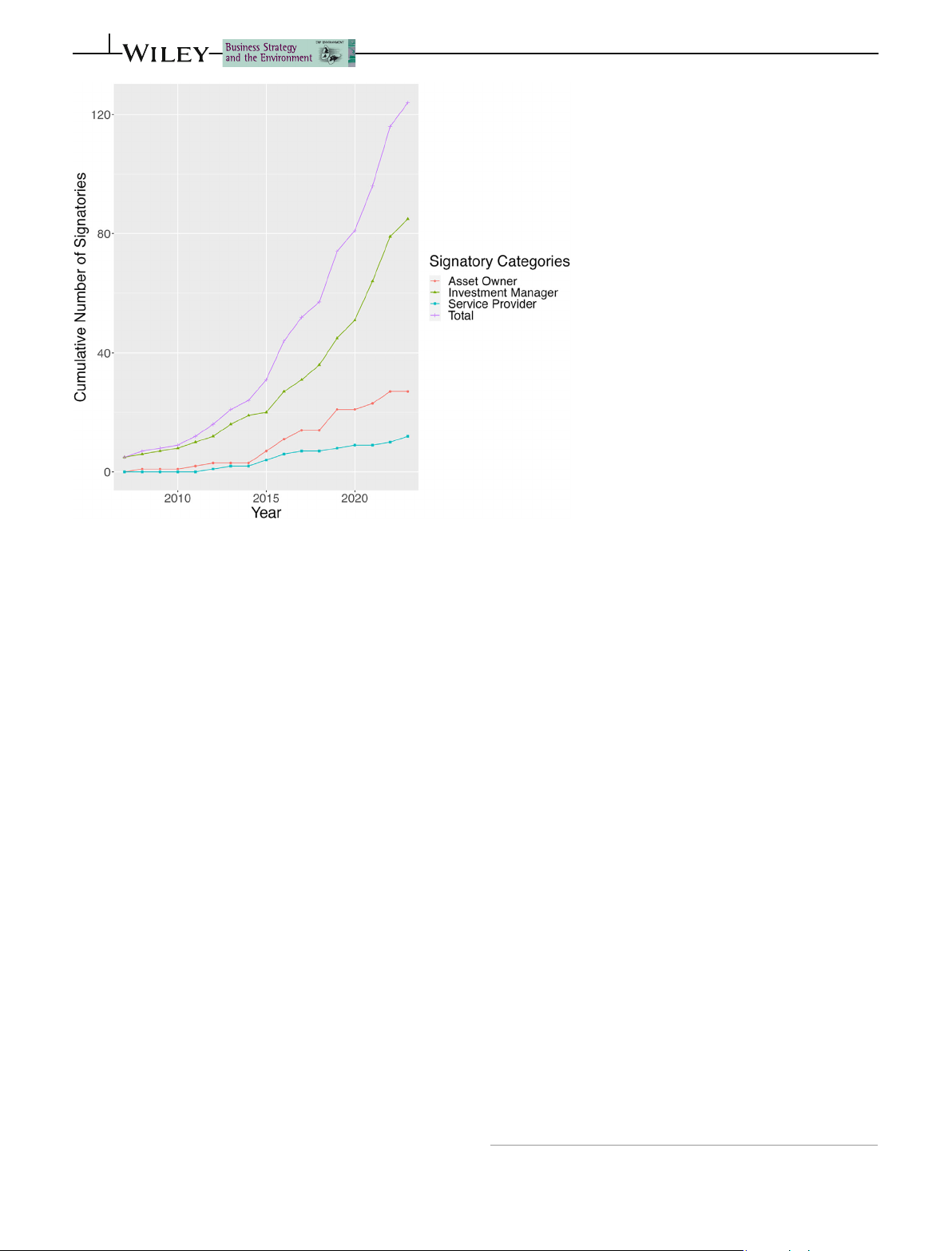

10990836, 2024, 4, Downloaded from https://onlinelibrary.wiley.com/doi/10.1002/bse.3649 by Readcube (Labtiva Inc.), Wiley Online Library on [07/03/2026]. See the Terms and Conditions (https://onlinelibrary.wiley.com/terms-and-conditions) on Wiley Online Library for rules of use; OA articles are governed by the applicable Creative Commons License 3674 AZUMA and HIGASHIDA F I G U R E 1 Cumulative number of PRI

signatories headquartered in Japan. Source: http://

www.unpri.org, accessed on September 1, 2023

Hypothesis 2. The presence of PRI signatories posi-

Simultaneously, the FSA unveiled the “Corporate Governance Code

tively influences the relationship between the institu-

(2014)” and the “Guidelines for Investor and Company Engagement

tional investor ratio and climate change disclosure. (2018).”

In tandem with these changes, Japanese institutional investors

have shown an increasing alignment with ESG requirements. Japan 2.3 | Urgency

has observed a rise in the number of institutional investors endorsing

the PRI, mirroring global trends. Figure 1 highlights this uptrend, with

The theory highlights urgency as its third component. Mitchell et al.

a noticeable surge post-2015. Delving into the specifics, this growth

(1997) described urgency as the extent to which stakeholders' claims

is primarily attributed to the ascendance of investment managers, demand swift response.

typically the direct shareholders of corporations. Notably, in 2015,

Historically, in Japan, the urgency of institutional investors' claims

the GPIF (Government Pension Investment Fund, Japan)—one of

was a recent phenomenon for corporations. Following the collapse of

the world's leading pension funds—became a signatory of the PRI.

the “bubble economy” in the early 1990s, traditional oversight mecha-

This move amplified the ESG demands on investment managers. Rein-

nisms such as cross-holding and “main banks” saw a decline in their

forcing this shift, a 2019 survey by the Investment Trust Association

influence. This shift led institutional investors to actively enhance the

identified ESG concerns, inclusive of climate change disclosure, as

corporate governance of the firms they invested in (Mizuno, 2010).

focal points in shareholder engagement.9

However, the influence of these institutional investors was not imme-

Recent developments in Japan have accentuated the urgency of

diate in its medium- and long-term impacts. A factor attributing to this

institutional investors' claims, especially on ESG matters, including cli-

delay was the inherent short-term focus of Japanese institutional

mate change. Consequently, we anticipate that the relationships out-

investors, driven by the need for frequent self-promotion and portfo-

lined in Hypotheses 1 and 2 have become increasingly pronounced

lio performance improvement (Suto & Toshino, 2005).

with these institutional shifts in Japan. Our third hypothesis is out-

Over the last decade, Japan has witnessed a surge in the urgency lined below.

of institutional investors' demands due to regulatory changes. The

Financial Services Agencies (FSA) in Japan introduced the “Principles

Hypothesis 3. The positive influence of institutional

for Responsible Institutional Investors, Japan's Stewardship Code

investors' holding ratio and the presence of the PRI sig-

(2014),” aiming to foster proactive engagement from investors and

natories has increased over the passage of time.

meaningful conversations with companies they invest in (Ueda, 2015).

Responding to the rising importance of ESG, the Stewardship Code

9https://www.toushin.or.jp/files/statistics/11/2019_plan_servey.pdf (last accessed on

underwent revisions in 2020 to include ESG considerations. August 16, 2022).

10990836, 2024, 4, Downloaded from https://onlinelibrary.wiley.com/doi/10.1002/bse.3649 by Readcube (Labtiva Inc.), Wiley Online Library on [07/03/2026]. See the Terms and Conditions (https://onlinelibrary.wiley.com/terms-and-conditions) on Wiley Online Library for rules of use; OA articles are governed by the applicable Creative Commons License AZUMA and HIGASHIDA 3675 3 | R E S E A R C H D E S I G N

take this alternative approach because we were not able to find evi-

dence on whether the effect of the PRI signing was shared among 3.1 | Data collection

institutions within the financial groups. For example, Mizuho Finan-

cial Group has numerous subordinated institutions with “Mizuho”

This study is predicated on archival quantitative methods, utilizing

included in their names, such as “Mizuho Trust,” “Mizuho Bank,” and

statistical analyses of secondary data. The main data analyzed in this

“Mizuho Securities.” An alternative approach would have been using

study is retrieved from Japanese Annual Securities Reports (ASR,

the string “Mizuho” to match all the subordinated institutions as

Yukashoken Hokokusho) in XBRL (eXtensible Business Reporting

signed. Instead, we used the string “Mizuho Trust” so that only the

Language)10 format. The following procedure was undertaken to col-

institution that has actually signed the PRI would be identified as lect the data: signed.

First, through the API (Application Programming Interface) pro-

The list of shareholders in security reports included names of

vided by the FSA (Financial Service Agency, Japan), a list of security

Japanese institutions as standing proxies (“Jonin-Dairinin”) where

reports published for accounting years ending between January

non-Japanese institutions hold shares of the firm. Thus, non-Japanese

1, 2017, and December 31, 2022, was downloaded in JSON

shareholders were considered as PRI-signed, corresponding to their

(JavaScript Object Notation) format (the so-called metadata). We then

standing proxies. The signing dates were also considered in this

scraped annual security reports from the API using a self-developed

approach. The shareholders would not be identified as signed until

program relying on the RCurl package in R. In total, 25,033 firm-year

the latest closing date after the signing.

security reports were downloaded in XBRL format. Each report con-

Summing up the holding ratios of PRI-signed shareholders in the

tained a list of the ten largest shareholders with their respective

report, the total holding ratios by PRI-signed investors were calculated

names and holding ratios. Using commands in stringr package, we

for each firm-year security report.

extracted a list of 261,620 shareholders with the data points from the XBRL files.11

The dataset scraped from the API was merged with the NIKKEI 3.3 | Climate change disclosure

CGES (Corporate Governance Evaluation System) dataset, a com-

monly used database in empirical analyses of Japanese firms. In total,

This study uses computer-assisted text analysis to measure climate

CGES had 22,794 observations during the timeframe of our analysis

change disclosure. Computer-assisted text analysis is broadly divided

(2017–2022). The common observations between the two databases

into two types: dictionary-based text analysis and unsupervised

(XBRL documents and CGES) were 18,702, and after eliminating those

machine learning algorithms (Li, 2010; Matthies & Coners, 2015).

with missing data, we were left with a sample of 17,604 firm-year

While the former relies on predetermined lists of words and catego- observations.

ries, the latter attempts to learn the “hidden structure” in unlabeled

texts. This study is based on the former approach; we predetermine

a list of strings related to climate change and count the appearances 3.2 |

Identifying shareholders who had signed

of the strings in the text as explained by the concrete procedure the PRI below.

We argue that using dictionary-based text analysis with computer

PRI-signed shareholders were identified based on public data. A list of

assistance is relevant, particularly for this study's task. First, the task

signatories was downloaded from the PRI website as of July 28, 2023.

addressed in this study, the measurement of climate change disclo-

This list captures the names of all institutions that have signed the PRI

sure, is topic-specific and comparable to previous studies using the

since its launch, accompanied by their signing dates. This facilitates

dictionary-based approach such as Hummel et al. (2022) and

accurate identification of PRI signatories based on the timing of publi-

Mittelbach-Hörmanseder et al. (2021). This is distinct from the

cation dates of the reports. For the sake of feasibility, the list was

goals pursued in previous environmental disclosure literature, such

limited to institutions headquartered in Japan, resulting in a total of

as a more comprehensive understanding (Clarkson et al., 2008; 87 institutions.

Patten, 2002) or investigation of verbal tones (Cho et al., 2010). Tech-

We manually developed a list of strings for the 87 institutions

nically, climate change has specific terms used only in the context of

after translating each name to Japanese to match the shareholder

the issue; for example, the term “greenhouse gas” typically appears

names extracted from the security reports in XBRL format. In devel-

only under the topic of climate change. This is especially true when

oping this set of strings, we aimed to match them only with institu-

the text analyzed is extracted from a specific context, namely certain

tions that had actually signed the PRI. An alternative approach

sections of the Japanese security reports. In general, a computer-

would have been to match all the institutions within the financial

assisted content analysis must be conditioned on the words for spe-

group to which the signing institution belongs. However, we did not

cific meanings in specialized contexts (Krippendorff, 2019), and the

task in this study meets this condition well.

10https://www.xbrl.org (last accessed on August 16, 2022). 11

Second, applying computer-assisted content analysis to XBRL

The number of shareholders does not match the exact tenfold of security reports

downloaded because some firms list more than ten shareholders.

documents dramatically increases the analysis's efficiency. The most

10990836, 2024, 4, Downloaded from https://onlinelibrary.wiley.com/doi/10.1002/bse.3649 by Readcube (Labtiva Inc.), Wiley Online Library on [07/03/2026]. See the Terms and Conditions (https://onlinelibrary.wiley.com/terms-and-conditions) on Wiley Online Library for rules of use; OA articles are governed by the applicable Creative Commons License 3676 AZUMA and HIGASHIDA

crucial advantage of computer-aided techniques is the higher speed

specifically opted to count nouns. Subsequently, stopwords were

of processing a large volume of data in a programmed manner (Riffe omitted.14

et al., 2014). Along with the growing availability of “big data,” the pop-

• Raw disclosure volume: Due to the unique characteristics of the

ularity of automated content analysis methods is increasing in social

Japanese language, which does not have clear word separations

science studies; these studies have the advantage of analyzing large

like English, our first measure could introduce biases. To counter-

datasets, such as SNS (Jung et al., 2018) and patent documents (Tseng

act this, we employed specialized algorithms, such as MeCab, for

et al., 2007). Similarly, we apply computer-assisted content analysis to

precise word counting. However, to further ensure the robustness

a large dataset of XBRL disclosure documents.

of our results and provide a more nuanced understanding, we also

To delineate our approach, we used a predetermined list of

incorporated the absolute frequency of the predetermined words.

strings to detect and measure climate change disclosure in security

reports. Relying on Cannon et al. (2020) and Landrum and Ohsowski

For the independent variables, our primary focus is on the

(2017), which used external documents on the topics in selecting following:

strings, both authors read the best practice examples of climate

change disclosure chosen by the local authority,12 then made a list of

• Institutional investors holding ratio: This variable represents the

strings, selecting from the strings that appeared in the document.

holding ratio by institutional investors, as sourced from the Nikkei

Strings included in the list had to be directly related to the issue of cli- CGES.

mate change; strings potentially used in different contexts, such as

• PRI signatories: A binary variable, it assigns a value of 1 when over

“carbon” and “environment,” were not included in the list following

1% of the firm's shareholders have signed the PRI and 0 otherwise. Cannon et al. (2020).

This categorization is conducted following the procedure of

Using a self-developed program in R, we searched for the follow-

identifying PRI-signed investors outlined previously. Given our

ing strings in the sections and counted their appearance frequencies.

assumption that the influence of PRI-signed investors does not

Concrete strings used were “global warming” (“Ondanka”), “green-

linearly correlate with their holding ratio, this variable takes on a

house effect” (“Onshitsukoka”), “climate change” (“Kikohendo”), “car-

binary form. Our choice of a 1% threshold aligns with Johnson

bon dioxide” (“Nisankatanso”), CO2 (“CO2”), and “decarbonization”

and Greening (1999), which deemed holdings below 1% as negligi-

(“Datsutanso”). Because of the nature of the Japanese language and

ble. This leads us to postulate that the sway of institutional

the strings chosen, stemming and lemmatization13 are not issues that

investors shifts noticeably once this 1% threshold is crossed. Fur-

need to be addressed. The sections searched in the security reports

thermore, only the interaction effect of PRI signatories with Insti-

are “Management Policy, Management Environment, Issues to

tutional investors holding ratio was considered, excluding PRI

Address” (“Keieihoshin, Keieikankyo oyobi Taishosubeki Kadai to”)

signatories as an individual term to avoid collinearity issues. It is

and “Business Risks (“Jigyo to no Risuku”). Based on the electronic

worth noting that non-institutional investors are less likely to

search, two different variables (plus one for robustness checks) on cli- become PRI signatories.

mate change disclosure were developed (explained in detail in the var- iable description section).

The control variables incorporated in the models are detailed below: 3.4 | Variable descriptions

• Corporate Size: Various studies have empirically confirmed the

impact of corporate size on social and environmental disclosure

The dependent variables of the analysis are related to climate change

(Gray et al., 1995b; Patten, 2002), as well as on climate change

disclosure and are captured using two distinct measures:

disclosure (Cotter & Najah, 2012; Prado-Lorenzo et al., 2009). To

account for this, we include the natural logarithm of total assets as

• Relative disclosure volume: This measure is constructed in line with a control for corporate size.

Li et al. (2013) and Cannon et al. (2020), utilizing the frequency of

• Leverage: The stakeholder theory literature underscores the pres-

predetermined word appearances normalized by the total word

sure exerted by capital lenders (Liesen et al., 2015; Roberts, 1992).

count in the sections. The values are multiplied by 1000 to simplify

We control for this influence by incorporating the firm's leverage

coefficient presentations, following Cannon et al. (2020). Given the ratio.

structural nuances of the Japanese language, which lacks “white

• Carbon Intensive: Previous research highlights the relationship

spaces” between words, we utilized the MeCab algorithm with the

between environmental performance and social and environmental

mecab-ipadic-NEologd dictionary (Kudo et al., 2004) to tokenize disclosures (Cho & Patten, 2007; Clarkson et al., 2008;

the text. Based on the taxonomy of MeCab, our research

Patten, 2002). In the realm of climate change, this extends to GHG

(greenhouse gas) performance (Cong et al., 2020; Freedman &

12https://www.fsa.go.jp/news/r3/singi/20220325/01-2.pdf (last accessed on August 16, 2022).

14Stopwords were removed using the list of words https://svn.sourceforge.jp/svnroot/

13https://nlp.stanford.edu/IR-book/html/htmledition/stemming-and-lemmatization-1.html

slothlib/CSharp/Version1/SlothLib/NLP/Filter/StopWord/word/Japanese.txt (accessed on

(last accessed on August 16, 2022). December 21, 2021).

10990836, 2024, 4, Downloaded from https://onlinelibrary.wiley.com/doi/10.1002/bse.3649 by Readcube (Labtiva Inc.), Wiley Online Library on [07/03/2026]. See the Terms and Conditions (https://onlinelibrary.wiley.com/terms-and-conditions) on Wiley Online Library for rules of use; OA articles are governed by the applicable Creative Commons License AZUMA and HIGASHIDA 3677

Jaggi, 2005; Luo & Tang, 2014). To account for this effect, we

over the years, we repeatedly run Equation (1) as a cross-sectional

employ an industry-based approach (Stanny & Ely, 2008) and for-

analysis from 2017 to 2022 and then conduct a panel analysis.

mulate a binary variable as per Liesen et al. (2015). The variable

In Hypothesis 3, we posited that the institutional investors'

Carbon intensive is binary, assigned a value of 1 if the firm operates

positive influence increases over the passage of time. To be precise,

within carbon-intensive industries, as classified by the Nikkei

we predict that the marginal effect of institutional investors' holding

Industry Classification System (Nikkei-Chubunrui). This includes

ratio and the presence of the PRI signatories, which we expect to be

industries of sea transportation, air transportation, petroleum,

positive for Hypotheses 1 and 2, respectively, increased over the

iron & steel, electric & electronic equipment, utilities (electric and

years. To test Hypothesis 3, we develop the following Equation (2):

gas), chemicals, motor vehicles & auto parts, trucking, railroad

transportation, pulp & paper, and precision equipment. Disclosurei,t ¼ γ þ γ 0

1 Inst:hold:ratioi,t Timetrendi,t

• Manufacturing: Besides carbon intensity, certain studies address þγ ð

2 Inst:hold:ratioi,t PRIsig:i,t Timetrendi,t 2Þ þγ

the industry sector's influence, such as potential regulatory threats

3 Timetrendi,t þ θ2 Xi,t þ υi,t

(Reid & Toffel, 2009). Aligning with this perspective, we introduce

this variable, a binary variable. It assumes a value of 1 if the firm is

In Equation (2), we introduce an interaction between the Time

part of the manufacturing sector, based on the Nikkei Industry

trend and Institutional investors' holding ratio, as well as its interaction

Classification System (Nikkei-Daibunrui), and 0 otherwise.

with PRI signatories. Contrary to conventional models, we do not

• Time Trend: We opted for a continuous variable rather than year-

include the main effects of Institutional investors' holding ratio or its

fixed effects in panel regressions to encapsulate the time trend.

interaction with PRI signatories in this equation. Our primary interest

This decision stems from an intention to sidestep the potential bias

lies in understanding how the influence of Institutional investors'

that fixed effects estimators might introduce in nonlinear models

holding ratio and its interaction with PRI signatories evolves over time.

(Greene et al., 2002). As outlined by Wooldridge (2008), Time trend

This is distinct from their individual effects, which are explored in

sequentially takes values from 1 to 6, mapping onto the study

Equation (1). We argue that, for the purposes of Equation (2), it is not years from 2017 to 2022.

imperative to account for these variables outside of their relationship

with Time trend. Furthermore, we control for the linear progression of

time by incorporating Time trend as an independent term. 3.5 | Econometric models

The marginal effect of Institutional investors' holding ratio on

Disclosure after holding all other variables fixed in Equation (2) is

This study employs two econometric models, and the first one is pre- expressed as follows:

sented as the following equation (1): ΔDisclosure ¼ γ

ΔInstitutionalinvestors0holdingratio

1 Timetrendi,t þ γ2 PRIsig:i,t Timetrendi,t Disclosurei ¼ β þ β 0

1 Inst:hold:ratioi þ β2Inst:hold:ratioi PRIsig:i þ θ ¼ ðγ þ γ Þ 1 2 PRIsig:i,t Timetrendi,t 1Xi þ εi ð1Þ ð3Þ

Equation (1) includes alternately one of Relative disclosure volume

or Raw disclosure volume as a dependent variable. X is a vector of

Equation (3) shows that the marginal effect of Institutional inves-

control variables and θ is a vector of their coefficient estimates. Of

tors' holding ratio is a linear function of Time trend, and our prediction

interest to our hypotheses are β1 and β2, which are coefficients of

of the marginal effect's growth along with the time passage requires

Institutional investors' holding ratio and its interaction with PRI signa- ðγ þγ 1

2 PRIsig:i,tÞ to be positive (Time trend increases with the progres-

tories, respectively. We interacted PRI signatories with Institutional

sion of time). When PRI signatories are absent (PRIsig:i,t ¼ 0),

investors holding ratio and, supposing only this interaction effect, did

Equation (3) becomes γ1 Timetrendi,t. Then, γ1 needs to be positive to

not include PRI signatories by itself in the model. Non-institutional

assume the growth of Institutional investors' holding ratio's marginal

investors are unlikely to become PRI signatories, and the exclusion of

effect along with time progression. In the case of the PRI signatories'

PRI signatories for the main effect was necessary because of collinear-

presence (PRIsig:i,t ¼ 1), Equation (3) becomes ðγ þ γ Þ 1 2 Timetrendi,t. In ity concerns.

alignment with Hypothesis 3, the sum ðγ þ γ Þ 1 2 must be positive.

In accordance with Hypothesis 1, that Institutional investors' hold-

Notably, when γ2 is positive, it indicates an enhanced marginal effect

ing ratio positively influences climate change disclosure, we predict β1

due to the presence of PRI signatories. Our prediction in Hypothesis 2

to take a positive value. In Hypothesis 2, we predicted that the pres-

expects a positive effect with the presence of PRI signatories. If the

ence of PRI-signed institutional investors positively influences the

time progression positively moderates this effect as suggested by

relationship between institutional investors and climate change disclo-

Hypothesis 3, γ2 would manifest a positive value.

sure. Econometrically, this means that the marginal effect of Institu-

In summary, for Hypotheses 1 and 2, we refer to Equation (1) and

tional investors' holding ratio is greater when PRI-signed institutional

anticipate β1 and β2 to be positive, respectively. In the context of

investors are present (β þ β 1

2 > β1 if PRI signatories = 1). Thus, we pre-

Hypothesis 3, we draw upon Equation (2) and its derivative,

dict β2 to be positive. To illustrate the effects of institutional investors

Equation (3), expecting both γ1 and γ2 to exhibit positive values.

10990836, 2024, 4, Downloaded from https://onlinelibrary.wiley.com/doi/10.1002/bse.3649 by Readcube (Labtiva Inc.), Wiley Online Library on [07/03/2026]. See the Terms and Conditions (https://onlinelibrary.wiley.com/terms-and-conditions) on Wiley Online Library for rules of use; OA articles are governed by the applicable Creative Commons License 3678 AZUMA and HIGASHIDA

As for the statistical approach, we employed the Tobit model

In contrast to the variables above, the time trend is not observed in

given that our dependent variables, Relative disclosure volume and

any of the control variables of Corporate size, Carbon intensive, Lever-

Raw disclosure volume, represent censored variables (with a left-

age, and Manufacturing as expected.

skewed distribution and a peak at 0). When conducting panel regres-

Table 3 exhibits the mean value comparisons of climate change

sions, we opted against using fixed effects to sidestep the inherent

disclosure to the presence of PRI-signed institutional investors along

bias of the fixed effects estimator within nonlinear frameworks

with the years. The group of firms with (without) PRI-signed institu-

(Greene et al., 2002). Consequently, we adopted the random effects

tional investors (ownership ratio over (under) 1%) are displayed under

model (Tobit RE) (Berndt et al., 1974; Henningsen, 2022) and

the columns of Present (Absent), and the mean values of the two cli-

accounted for the time trend effect by incorporating a continuous

mate change disclosure measures are compared between the groups

time trend variable (Flammer, 2013; Wooldridge, 2008).

for each year. With both Relative disclosure volume and Raw disclosure

volume, the mean values are greater for the Present group throughout

the timeframe of the analysis, and the absolute value of t generally 4 | R E S U L T S

increases along with the year's passage. This indicates that the influ-

ence of PRI-signed institutional investors on climate change disclosure 4.1 | Main results

becomes more distinct with time. Overall, the results suggest a posi-

tive influence of PRI signing by institutional investors on climate

Table 2 presents the descriptive statistics of the variables. These

change disclosure, and the influence is growing with time.

statistics are organized annually, with the final column amalgamating

Tables 4 and 5 present the results of the multivariate analysis.

data across all years. Means of Relative disclosure volume and Raw

Table 4 exhibits the results of the Tobit regression analyses with Rela-

disclosure volume are constantly increasing over the years. Notably,

tive disclosure volume as a dependent variable. Cross-sectional ana-

the medians for these variables consistently stand at zero in every

lyses are repeated for each year from 2017 to 2022, and then a panel

sub-sample (data not shown), pointing to a leftward skew in their

regression analysis with random effect Tobit is executed. distributions.

Concerning the annual executions of cross-sectional analyses, the

The means of Institutional investors holding ratio over the years

estimated coefficient for Institutional investors holding ratio is positive

reflect an increasing presence of institutional investors in Japan,

throughout the analysis period except for 2017. Statistical significance

although not strictly persistent. The means of PRI signatories repre-

was first detected in 2020, but only with p < 0:1. In 2021 and 2022,

sent percentage ratios of firms with PRI-signed institutional investors

statistical significance becomes more evident (p < 0:01 and p < 0:01,

over 1% holding ratio within the firm. The values reflect a gradual pro-

respectively), which is consistent with Hypothesis 1. Analogous results

liferation of PRI-signed institutional investors among Japanese firms.

are observed for the interactive variable Inst. holding ratio*PRI sig. The T A B L E 2 Descriptive statistics. Year 2017 Year 2018 Year 2019 Year 2020 Year 2021 Year 2022 Pooled n = 2809 n = 2903 n = 2995 n = 3092 n = 2707 n = 3098 n = 17,604 mean sd mean sd mean sd mean sd mean sd mean sd mean sd Relat. dis. volume 0.18 0.88 0.22 1.00 0.33 1.42 0.71 2.04 1.59 3.40 2.97 4.92 0.98 2.84 Raw dis. volume 0.13 0.63 0.17 0.92 0.28 1.37 0.75 2.44 1.65 4.42 3.43 7.53 1.04 3.88 Inst. holding ratio 7.37 7.18 8.36 7.62 9.56 8.31 8.91 8.19 8.97 8.16 10.00 8.90 8.86 8.12 PRI signatories 0.33 0.47 0.32 0.47 0.38 0.49 0.42 0.49 0.40 0.49 0.40 0.49 0.37 0.48 Corporate size 7.02 1.64 6.99 1.65 7.02 1.66 6.99 1.66 6.98 1.67 7.02 1.65 7.00 1.65 Leverage 2.44 35.39 3.08 8.86 2.92 4.69 2.81 9.74 3.16 7.42 3.14 5.89 2.93 15.76 Carbon intensive 0.25 0.43 0.24 0.43 0.23 0.42 0.23 0.42 0.23 0.42 0.23 0.42 0.23 0.42 Manufacturing 0.56 0.50 0.57 0.49 0.58 0.49 0.59 0.49 0.59 0.49 0.59 0.49 0.58 0.49 Time trend 1.00 0.00 2.00 0.00 3.00 0.00 4.00 0.00 5.00 0.00 6.00 0.00 3.50 1.68

Note: Variable descriptions as follows: Relat. dis. volume = continuous variable taking word frequency values of climate words that appeared in the relevant

sections of security reports deflated by the total number of nouns in the text; Raw dis. volume = continuous variable taking word frequency values of

climate words that appeared in the relevant sections of security reports; Inst. holding ratio = institutional ownership holding ratio; PRI signatories = binary

variable taking a value of 1 when the holding ratio of PRI signed institutional investors exceeds 1% or 0 otherwise; Corporate size = natural log of total

assets; Leverage = leverage ratio of the firm; Carbon intensive = binary variable taking a value of 1 when firm belongs to carbon-sensitive industries or 0

otherwise; Manufacturing = binary variable taking a value of 1 when the firm belongs to manufacturing industry or 0 otherwise; and Time trend =

continuous variable taking values from 1 to 6 corresponding to 2017 to 2022.

10990836, 2024, 4, Downloaded from https://onlinelibrary.wiley.com/doi/10.1002/bse.3649 by Readcube (Labtiva Inc.), Wiley Online Library on [07/03/2026]. See the Terms and Conditions (https://onlinelibrary.wiley.com/terms-and-conditions) on Wiley Online Library for rules of use; OA articles are governed by the applicable Creative Commons License AZUMA and HIGASHIDA 3679 T A B L E 3

Mean value comparisons between climate change disclosure and the presence of PRI signatories. Relative disclosure volume Raw disclosure volume N PRI signatories Absent Present Absent Present Absent Present mean mean t mean mean t 2017 0.13 0.27 3.55*** 0.09 0.20 3.86*** 1883 926 2018 0.17 0.32 3.65*** 0.12 0.27 3.73*** 1969 934 2019 0.23 0.50 4.85*** 0.19 0.41 4.22*** 1862 1133 2020 0.41 1.13 9.00*** 0.44 1.17 7.72*** 1805 1287 2021 1.00 2.50 11.34*** 0.99 2.65 9.25*** 1871 1227 2022 1.90 4.55 13.20*** 2.08 5.41 10.44*** 1613 1094 *p < 0:1: **p < 0:05: ***p < 0:01: T A B L E 4

Regression analysis: Relative disclosure volume as dependent variable. Relative disclosure volume 2017 2018 2019 2020 2021 2022 2017–2022 2017–2022 Inst. holding ratio 0.02 0.00 0.01 0.04* 0.09*** 0.20*** 0.09*** (0.03) (0.03) (0.03) (0.02) (0.02) (0.03) (0.01)

Inst. holding ratio* Time trend 0.03*** (0.00) Inst. hol. ratio*PRI sig. 0.05 0.03 0.03 0.07*** 0.08*** 0.09*** 0.06*** (0.03) (0.03) (0.03) (0.02) (0.02) (0.02) (0.01)

Inst. hol. ratio*PRI sig.* Time trend 0.01*** (0.00) Corporate size 1.05*** 1.14*** 1.42*** 1.34*** 1.59*** 1.55*** 1.66*** 1.57*** (0.14) (0.14) (0.14) (0.10) (0.11) (0.13) (0.07) (0.07) Leverage 0.00 0.05 0.05 0.00 0.03 0.04* 0.00 0.00 (0.01) (0.04) (0.03) (0.01) (0.03) (0.03) (0.02) (0.02) Carbon intensive 2.19*** 1.74*** 1.80*** 0.89** 0.93** 0.93** 1.07*** 1.13*** (0.45) (0.43) (0.46) (0.35) (0.37) (0.42) (0.25) (0.25) Manufacturing 0.10 0.07 0.63 1.26*** 1.85*** 1.53*** 1.70*** 1.67*** (0.42) (0.41) (0.44) (0.32) (0.33) (0.37) (0.24) (0.23) Time trend 2.62*** 2.16*** (0.03) (0.04) (Intercept) 15.96*** 16.20*** 18.71*** 14.71*** 14.64*** 13.70*** 29.07*** 26.55*** (1.33) (1.24) (1.26) (0.83) (0.81) (0.88) (0.57) (0.57) Model Tobit Tobit Tobit Tobit Tobit Tobit Tobit RE Tobit RE N 2809 2903 2995 3092 3098 2707 17,604 17,604 Left-censored 2601 2655 2669 2457 2063 1435 13,880 13,880 Uncensored 208 248 326 635 1035 1272 3724 3724 Log Likelihood 1042.42 1227.45 1586.62 2734.59 4269.61 5060.03 14,717.49 14,659.23 PseudoR2 0.08 0.07 0.08 0.09 0.08 0.08 0.21 0.21 *p < 0:1. **p < 0:05. ***p < 0:01.

10990836, 2024, 4, Downloaded from https://onlinelibrary.wiley.com/doi/10.1002/bse.3649 by Readcube (Labtiva Inc.), Wiley Online Library on [07/03/2026]. See the Terms and Conditions (https://onlinelibrary.wiley.com/terms-and-conditions) on Wiley Online Library for rules of use; OA articles are governed by the applicable Creative Commons License 3680 AZUMA and HIGASHIDA T A B L E 5

Regression analysis: Raw disclosure volume as dependent variable. Raw disclosure volume 2017 2018 2019 2020 2021 2022 2017–2022 2017–2022 Inst. holding ratio 0.01 0.00 0.02 0.06** 0.11*** 0.27*** 0.13*** (0.02) (0.02) (0.03) (0.03) (0.03) (0.04) (0.02)

Inst. holding ratio* Time trend 0.04*** (0.00) Inst. hol. ratio*PRI sig. 0.03 0.02 0.02 0.06** 0.08*** 0.13*** 0.06*** (0.02) (0.02) (0.02) (0.02) (0.03) (0.03) (0.01)

Inst. hol. ratio*PRI sig.* Time trend 0.01*** (0.00) Corporate size 0.79*** 1.06*** 1.38*** 1.74*** 2.29*** 2.75*** 2.19*** 1.91*** (0.10) (0.11) (0.13) (0.11) (0.14) (0.19) (0.08) (0.07) Leverage 0.00 0.05 0.04 0.00 0.01 0.09** 0.01 0.01 (0.01) (0.04) (0.03) (0.01) (0.03) (0.04) (0.02) (0.02) Carbon intensive 1.43*** 1.29*** 1.35*** 0.88** 0.72 0.57 0.73** 0.84*** (0.31) (0.36) (0.41) (0.38) (0.45) (0.62) (0.33) (0.32) Manufacturing 0.04 0.08 0.59 1.14*** 1.94*** 1.55*** 1.90*** 1.77*** (0.29) (0.34) (0.39) (0.35) (0.41) (0.55) (0.29) (0.28) Time trend 3.18*** 2.49*** (0.04) (0.05) (Intercept) 11.46*** 14.26*** 17.58*** 18.38*** 21.02*** 24.83*** 37.10*** 32.30*** (0.91) (1.02) (1.12) (0.91) (1.00) (1.31) (0.61) (0.62) Model Tobit Tobit Tobit Tobit Tobit Tobit Tobit RE Tobit RE N 2809 2903 2995 3092 3098 2707 17,604 17,604 Left-censored 2601 2655 2669 2457 2063 1435 13,880 13,880 Uncensored 208 248 326 635 1035 1272 3724 3724 Log Likelihood 960.57 1168.95 1533.49 2763.93 4411.36 5475.34 15,559.81 15,500.31 PseudoR2 0.09 0.09 0.09 0.10 0.09 0.08 0.20 0.20 *p < 0:1. **p < 0:05. ***p < 0:01.

coefficient is estimated to be positive throughout the analysis period,

Table 5 exhibits the results of regression analyses with Raw

consistent with Hypothesis 2. Statistical significance is detected for

disclosure volume as the dependent variable. Models are repeated

the first time in 2020 (p < 0:01) and stays until 2022 (p < 0:01). Gradual

identically to the analyses in Table 4. Concerning the repeated cross-

increase of the statistical significance of the coefficients for Institu-

sectional analyses along with the years, the signs of the coefficients

tional investors holding ratio and Inst. holding ratio*PRI sig. conform

are all identical. Statistical significance in 2020 was p < 0:05, but then with Hypothesis 3.

later turns into p < 0:01 for both Institutional investors holding ratio

The random effects Tobit regressions in the final two columns

and Inst. holding ratio*PRI sig. The panel regression analyses display

report consistent results. In the first model (the second from the right-

similar results. In the first model, the coefficients for Institutional

est), the coefficients for Institutional investors holding ratio and Inst.

investors holding ratio and Inst. holding ratio*PRI sig. are both positive

holding ratio*PRI sig. are both positive and statistically significant and statistically significant (p < 0:01). These results support

(p < 0:01) supporting Hypotheses 1 and 2, respectively. In the second

Hypotheses 1 and 2, respectively. In the second model (the final col-

model (the final column) using Time trend as an interactive variable,

umn) using Time trend as an interaction term, the coefficients for Inst.

the estimated coefficients for the variables of Inst. holding ratio*Time

holding ratio*Time trend, Inst. holding ratio*PRI sig.*Time trend, and

trend, Inst. holding ratio*PRI sig.*Time trend, and Time trend are all

Time trend are all positive and statistically significant (p < 0:01). Conse-

positive and statistically significant (p < 0:01). Thus, the result is in

quently, the findings corroborate Hypothesis 3. support of Hypothesis 3.

Overall, our empirical results support our Hypotheses 1,2, and 3.

10990836, 2024, 4, Downloaded from https://onlinelibrary.wiley.com/doi/10.1002/bse.3649 by Readcube (Labtiva Inc.), Wiley Online Library on [07/03/2026]. See the Terms and Conditions (https://onlinelibrary.wiley.com/terms-and-conditions) on Wiley Online Library for rules of use; OA articles are governed by the applicable Creative Commons License AZUMA and HIGASHIDA 3681 4.2 | Robustness tests

changes (results not tabulated). We also created a binary version of

the variable that takes the value of 1 if any of the keywords were

We conducted a series of additional tests to check the robustness of

detected and 0 otherwise. Once more, after replicating our primary

our results. First, we experimented with various alternative versions

analysis with the Probit regression model using this binary metric, we

of the disclosure measures. Although our measures of Relative disclo-

observed no significant variations (results not shown).

sure volume and Raw disclosure volume are derived from the previous

Second, we examined if lagging explanatory variables by one year

studies (Cannon et al., 2020; Li et al., 2013), the computer-assisted

would result in any notable changes. We developed our models posit-

text analysis is a comparatively novel method, and as such, the appro-

ing that the institutional investors' holding ratio during the year has

priateness of the disclosure measure chosen still requires verification.

affected firms' disclosure at the end of the year. In line with certain

To mitigate any potential effects from the long tail distributions of the

studies that consider values from one year prior (e.g., Flammer et al.,

measures, we replaced the measures with natural logs of Relative dis-

2021; Liesen et al., 2015), we adjusted all explanatory variables with a

closure volume + 1 and Raw disclosure volume + 1, respectively; add-

one-year lag and replicated the main analysis (results not shown). We

ing 1 before computing the natural logarithm is customary to

verified that lagging the variables by one year does not produce any

accommodate variables with 0 values (Wooldridge, 2008). We repli-

essential changes to our results.

cated our main analyses presented in Tables 4 and 5 with the alterna-

Third, we ascertained that employing a fixed effects model does

tive logged forms, and the results did not produce any notable

not yield alternative conclusions. As mentioned before, because our T A B L E 6 Robustness check with Relative disclosure volume Raw disclosure volume instrumental variables. 2017–2022 2017–2022 2017–2022 2017–2022 Inst. holding ratio 0.29*** 0.30*** (0.07) (0.02)

Inst. holding ratio* Time trend 0.09*** 0.15*** (0.02) (0.02) Inst. hol. ratio*PRI sig. 0.25** 0.61*** (0.12) (0.02)

Inst. hol. ratio*PRI sig.* Time trend 0.06* 0.03* (0.03) (0.02) Corporate size 0.51*** 0.48*** 0.45*** 0.78*** (0.13) (0.15) (0.10) (0.10) Leverage 0.00 0.00 0.01 0.01 (0.01) (0.01) (0.01) (0.01) Carbon intensive 1.68*** 1.68*** 1.76*** 1.64*** (0.21) (0.21) (0.25) (0.25) Manufacturing 1.44*** 1.45*** 1.53*** 1.33*** (0.16) (0.16) (0.23) (0.23) Time trend 2.47*** 2.47*** 3.15*** 2.86*** (0.07) (0.07) (0.13) (0.13) (Intercept) 22.38*** 22.31*** 28.48*** 29.76*** (0.93) (1.06) (1.45) (1.45) Model Tobit Tobit Tobit Tobit Method Pooling Pooling Pooling Pooling SE estimate Bootstrap Bootstrap Bootstrap Bootstrap N 17,521 17,521 17,521 17,521 Left-censored 13,823 13,823 13,823 13,823 Uncensored 3698 3698 3698 3698 Log Likelihood 15,981.70 15,981.93 16,604.33 16,548.57 *p < 0:1: **p < 0:05: ***p < 0:01:

10990836, 2024, 4, Downloaded from https://onlinelibrary.wiley.com/doi/10.1002/bse.3649 by Readcube (Labtiva Inc.), Wiley Online Library on [07/03/2026]. See the Terms and Conditions (https://onlinelibrary.wiley.com/terms-and-conditions) on Wiley Online Library for rules of use; OA articles are governed by the applicable Creative Commons License 3682 AZUMA and HIGASHIDA

main analyses are based on the non-linear Tobit model, we did not

both disclosure measures (p < 0:01). Conversely, the coefficients of

use a fixed effects model in our panel regressions to avoid potential

Inst. holding ratio PRI sig. Time trend register only borderline

bias in our estimators (Greene et al., 2002). Replacing it with linear

significance with the disclosure metrics (p < 0:10). Hence, when

OLS panel regression, we introduced firm fixed effects to account for

accounting for endogeneity, Hypothesis 3 is supported only to a lim-

unobserved, time-invariant individual characteristics. We reproduced ited extent.

the analysis of the final two columns in Tables 4 and 5, and the results

did not generate notable changes to our conclusions (results not shown). 5 | C O N C L U S I O N

Last, we employed an instrumental variable strategy to tackle

potential endogeneity concerns. Overall, we present consistent results 5.1 | Summary and discussion

with our hypotheses after controlling for endogeneity; however, it is

worth noting that our ability to demonstrate robustness in this con-

This study investigated the influence of institutional investors on cli-

text is relatively constrained (results shown in Table 6). This study

mate change disclosure from the perspective of stakeholder salience

potentially suffers from reverse causality; institutional investors might

theory (Mitchell et al., 1997) with a particular focus on institutional

prefer companies with specific attributes that do not influence their

investors signing the PRI. The theoretical framework was developed

disclosure practices after acquiring shares in these firms.

in relation to institutional investors' power, legitimacy, and urgency.

We employed an instrumental variable approach to alleviate this

Empirical data was collected in Japan, where institutional investors'

concern. In our primary models, we incorporate the Institutional inves-

influence is exerted mainly through shareholder engagement. The

tors' holding ratio and its interaction. To address potential endogeneity

determinants—holding ratio (power), PRI signing (legitimacy), and time

concerns, it is imperative to identify a minimum of two instrumental

passage (urgency)—were tested in relation to climate change disclosure

variables. These instruments should be anticipated to affect the hold-

captured by two alternative measurements. As a result, all three

ing ratios of institutional investors yet remain orthogonal to disclosure hypotheses were supported.

practices. We use the following three variables as instruments. As

Regarding Hypothesis 1, institutional investors' holding ratio posi-

inclusion in a local market index may positively affect (especially local)

tively influenced climate change disclosure. With Hypothesis 2, the

institutional investors' investment behaviors (Gao et al., 2019), we use