Practice Exercise - Budgeting

Preview text:

Budget schedules for a manufacturer. Logo Specialties manufactures, among other things,

woolen blankets for the athletic teams of the two local high schools. The company sews the

blankets from fabric and sews on a logo patch purchased from the licensed logo store site. The teams are as follows:

• Knights, with red blankets and the Knights logo

• Raiders, with black blankets and the Raider logo

Also, the black blankets are slightly larger than the red blankets.

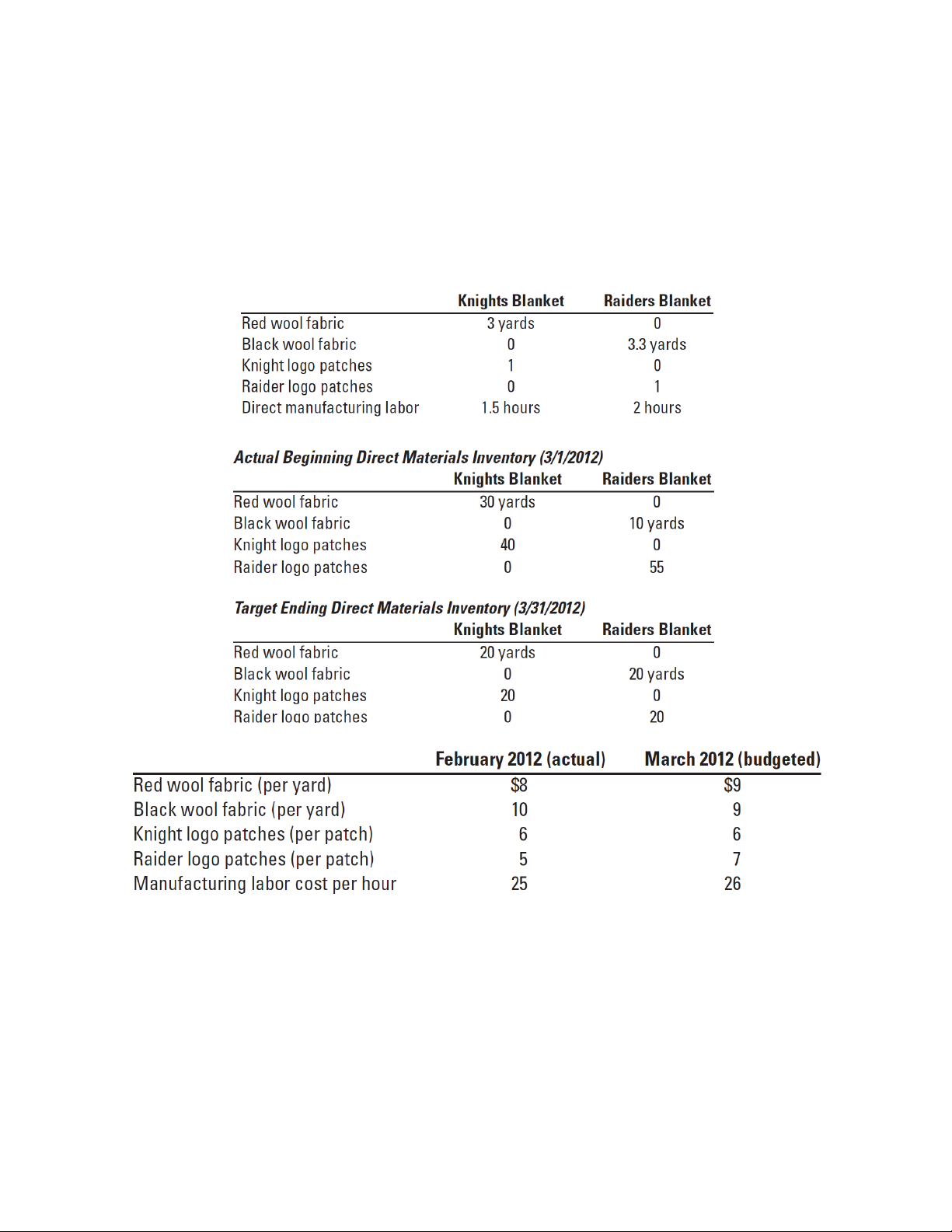

The budgeted direct-cost inputs for each product in 2012 are as follows:

Unit data pertaining to the direct materials for March 2012 are as follows:

Unit cost data for direct-cost inputs pertaining to February 2012 and March 2012 are as follows:

Manufacturing overhead (both variable and fixed) is allocated to each blanket on the basis of

budgeted direct manufacturing labor-hours per blanket. The budgeted variable manufacturing

overhead rate for March 2012 is $15 per direct manufacturing labor-hour. The budgeted fixed

manufacturing overhead for March 2012 is $9,200. Both variable and fixed manufacturing

overhead costs are allocated to each unit of finished goods.

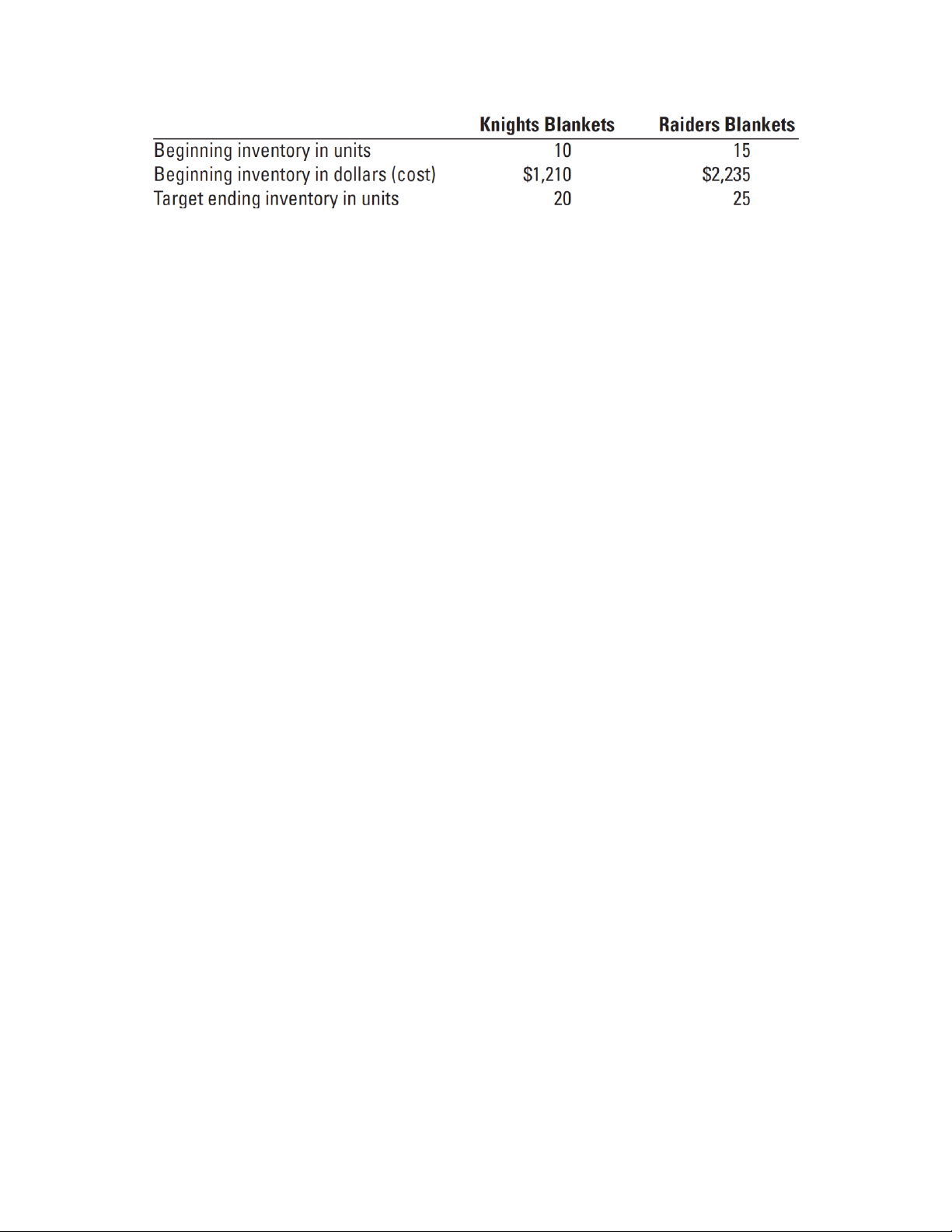

Data relating to finished goods inventory for March 2012 are as follows:

Budgeted sales for March 2012 are 120 units of the Knights blankets and 180 units of the

Raiders blankets. The budgeted selling prices per unit in March 2012 are $150 for the Knights

blankets and $175 for the Raiders blankets. Assume the following in your answer:

• Work-in-process inventories are negligible and ignored.

• Direct materials inventory and finished goods inventory are costed using the FIFO method.

• Unit costs of direct materials purchased and finished goods are constant in March 2012. Requirements:

Prepare the following budgets for March 2012: 1. Revenues budget 2. Production budget in units

3. Direct material usage budget and direct material purchases budget

4. Direct manufacturing labor budget

5. Manufacturing overhead budget

6. Ending inventories budget (direct materials and finished goods)