Bài giảng đại học tôn đức thắng ôn giữa kỳ 1

Bài giảng đại học tôn đức thắng ôn giữa kỳ

Môn: Quản trị tài chính doanh nghiệp 297 tài liệu

Trường: Trường Đại học Kinh Tế Quốc Dân 8.7 K tài liệu

Tác giả:

Preview text:

TON DUC THANG UNIVERSITY FACULTY OF ACCOUNTING Chapter 5:

Audit completion and audit report Course code: 201106 1/29/2024

201106- Audit completion and audit report 1 Learning objectives

Understand the auditor’s tasks and responsibilities in audit completion

Understand the nature and significance of the auditor’s reporting obligations

Identify the different types of audit reports and realize the

circumstances under which an auditor would issue each type of report 1/29/2024

201106- Audit completion and audit report 2 Contents 5.1 Audit completion 5.2 Audit report 1/29/2024

201106- Audit completion and audit report 3 STARTUP

Life of A Big 4 Auditor

Asking The Client About Fraud 4 1/29/2024

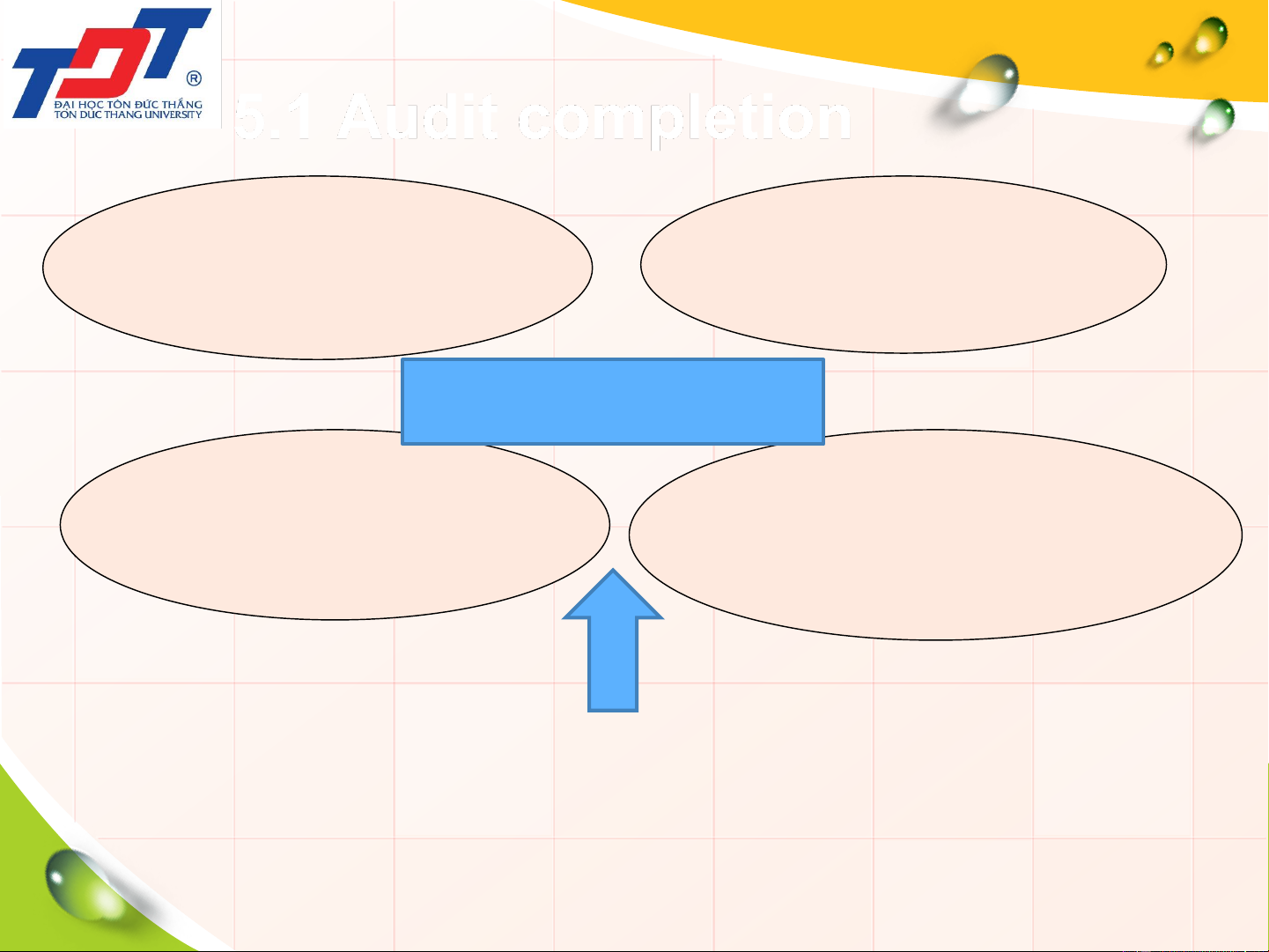

201106- Audit completion and audit report 5.1 Audit completion Subsequent events Representation letters (VSA 560) (VSA 580) Audit Completion Review of audit working Appropriateness of the papers and FS going concern basis (VSA 570)

The date of the auditor’s report 5 1/29/2024

201106- Audit completion and audit report 5.1 Audit completion

Audit Completion Stage includes the following issues:

• The date of the auditor’s report • Subsequent events • Representation letters

• Review of audit working papers and financial report

• Appropriateness of the going concern basis 1/29/2024

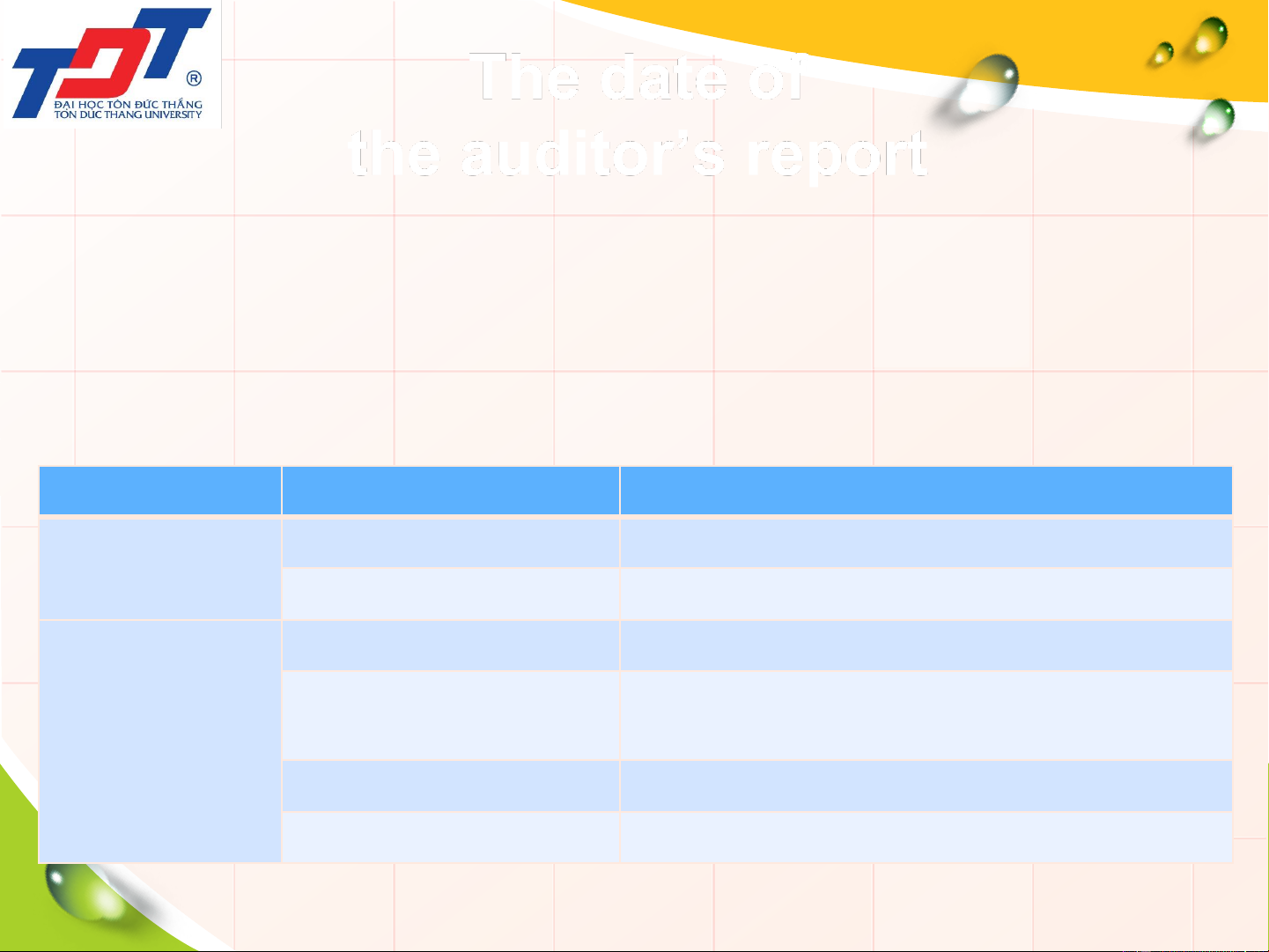

201106- Audit completion and audit report 6 The date of the auditor’s report

• The date of the auditor’s report is important.

• It establishes the date of the auditor’s responsibility for

knowledge of important events that should be reflected in the financial report.

• The auditor can not provide an auditor’s opinion based

on events that occur after the auditor’s report has been signed.

• The auditor’s report must be dated with the actual date

on which it is physically signed. 1/29/2024

201106- Audit completion and audit report 7 The date of the auditor’s report

• The date of the auditor’s report is determined by the date

of the directors’ declaration

• The date of the auditor’s report should be no earlier than

the date on the directors’ declaration. Period Date Events Financial 01 January 20X1 to Beginning of financial year report period 31 December 20X1 Balance date Subsequent 31 December 20X1 to Balance date events period 15 March 20X1

Signing of directors’ declaration and

report and signing of auditor’s report 31 March 20X1 Distribution of annual report 30 April 20X1 Annual general meeting 1/29/2024

201106- Audit completion and audit report 8 Subsequent events

• Some specific audit procedures are necessary to provide

reasonable assurance that the auditor is aware of significant subsequent events.

• VSA 560 extends “subsequent events” to include:

events occurring between the balance date and the date of the auditor’s report

facts that become known to the auditor after the date of the auditor’s report. 1/29/2024

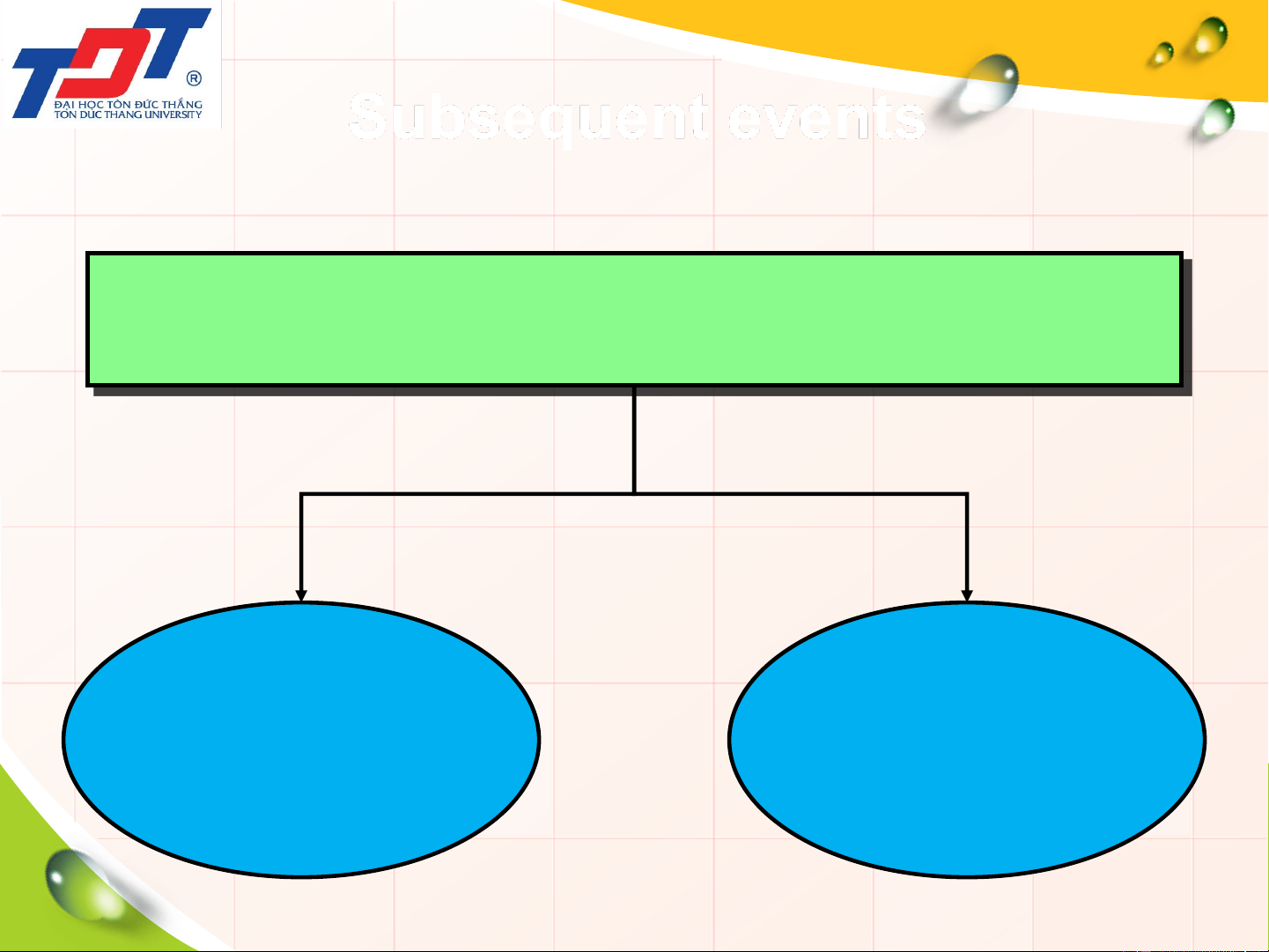

201106- Audit completion and audit report 9 Subsequent events

Events occurring between the balance date and

the date of the auditor’s report Adjusting events Non-adjusting events 10 1/29/2024

201106- Audit completion and audit report Subsequent events • Adjusting events are those events, both

favorable and unfavorable, providing evidence

of, or further elucidate, conditions that existed at balance date. • Examples:

Sale of inventories at a price below recorded cost Debtors’ bankruptcy 1/29/2024

201106- Audit completion and audit report 11 Subsequent events

• Non-adjusting events are those events, both favorable and unfavorable, creating new

conditions, as distinct from any that may have existed at balance date. • Examples:

Fire or flood loss after balance date not fully covered by insurance

Major currency realignment subsequent to balance date 1/29/2024

201106- Audit completion and audit report 12 Subsequent events

Events between balance date and the date of auditor’s

report – The auditor must:

• Complete audit procedures in relation to subsequent

events up to the date of auditor’s report

• Consider the impact of any necessary adjustments on the auditor’s report 1/29/2024

201106- Audit completion and audit report 13 Subsequent events

Events subsequent to the date of auditor’s report

• The auditor has no responsibility to carry out audit

procedures after the auditor’s report has been signed.

• Aware of a material adjustment after the auditor’ report

has been signed but before the financial report has been issued, the auditor should:

discuss the matter with management

consider to issue a new report based on whether adjustments made by management 1/29/2024

201106- Audit completion and audit report 14 Subsequent events

Events subsequent to the issue of the financial report

• Aware of a material adjustment after the financial report

has been issued, the auditor should:

discuss with management the possible recall and

reissue of the financial report

take action to prevent reliance on the auditor’s report

if impossible to discuss with management 1/29/2024

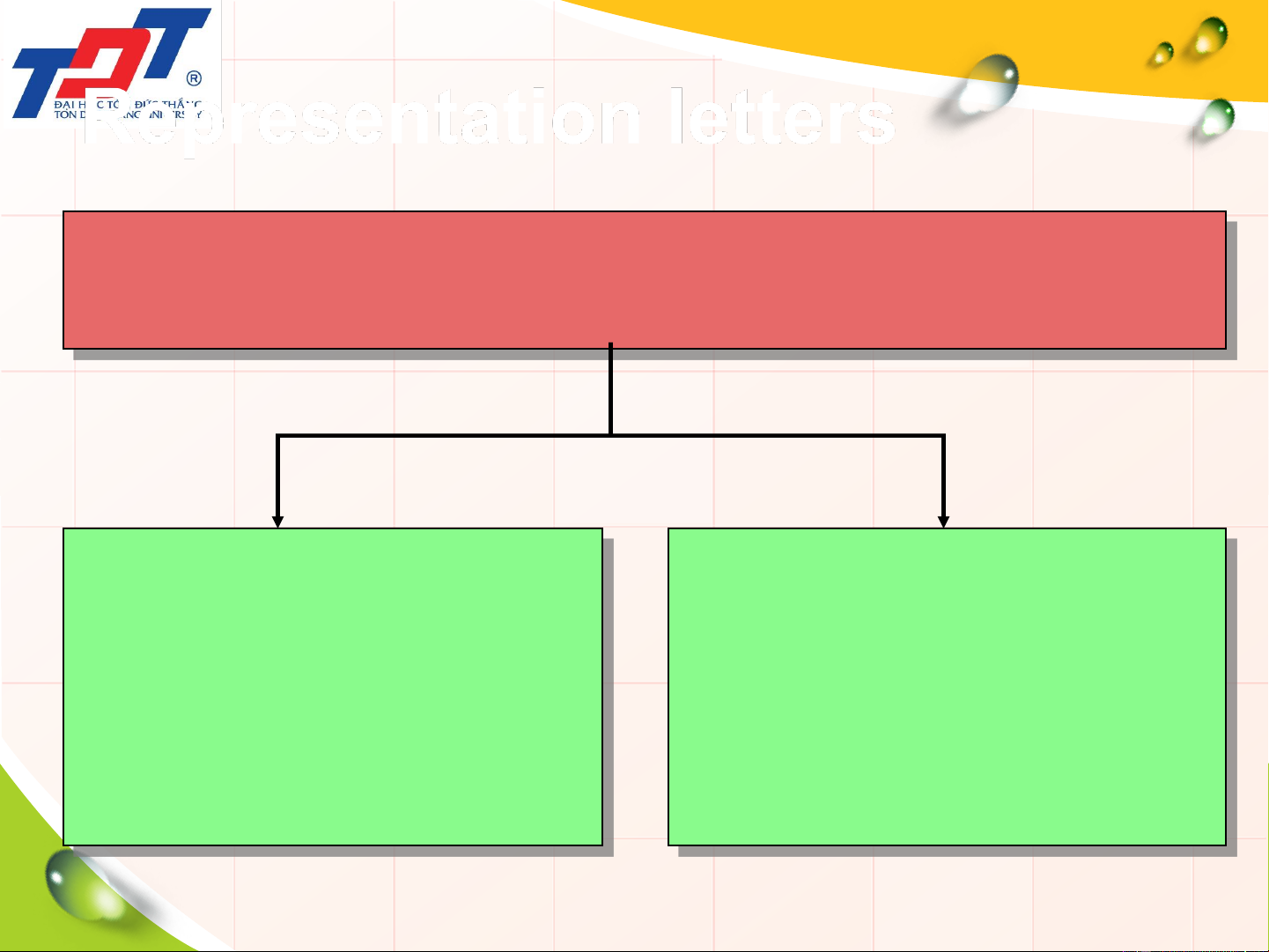

201106- Audit completion and audit report 15 Representation letters

As part of the subsequent events review, the auditor

normally obtains formal representation letters Solicitors’ letter Management (obtain evidence of representation letter possible legal (evidence to support contingencies)

management’s intentions) 16 1/29/2024

201106- Audit completion and audit report Representation letters

• Solicitors’ letter is sent to a solicitor as a means

of obtaining corroborating information about

management’s assertion concerning:

the status of litigation, claims

unrecorded or contingent liabilities

• Management representation letter signed by management that contains representations

made by management to an auditor during the course of an audit. 1/29/2024

201106- Audit completion and audit report 17

Review of audit working papers

and financial statements

• The cause of any errors need to be considered to

determine whether they affect any earlier decisions concerning risk assessment.

• The auditor needs to summarize errors to determine

whether individually or in aggregate they are material and require adjustment.

• The audit working papers are reviewed to ensure:

the audit is complete and properly documented

the audit working papers contain sufficient appropriate audit evidence 1/29/2024

201106- Audit completion and audit report 18

Review of audit working papers

and financial statements

Review of audit working papers and financial report includes the following issues:

• Final assessment of materiality and audit risk

• Review of the financial report and other information contained in the annual report

• Examining related-party transactions

• Administrative completion of audit working papers • Activities after the audit 1/29/2024

201106- Audit completion and audit report 19

Review of audit working papers and financial report

Activities after the audit includes the following issues:

• Preparing a management letter covering internal control

weakness discovered during the audit

• Having meetings with management and the audit

committee or board of directors

• Maintaining the quality of the audit practice 1/29/2024

201106- Audit completion and audit report 20