Câu hỏi lý thuyết – Internal control & audit procedures past paper môn Kiểm toán | Học viện Ngân hàng

The control environment includes the governance and management functions and the attitudes, awareness and actions of those charged with governance and management concerning the entity’s system of internal control and its importance in the entity. Tài liệu được sưu tầm gồm 12 trang, giúp các bạn ôn luyện và phục vụ cho việc học tập, đạt kết quả tốt. Mời các bạn đón xem!

Môn: Kiểm Toán (HVNH) 57 tài liệu

Trường: Học viện Ngân hàng 2.3 K tài liệu

Tác giả:

Preview text:

CÂU HỎI LÝ THUYẾT – PAST EXAM SEP/DEC 22

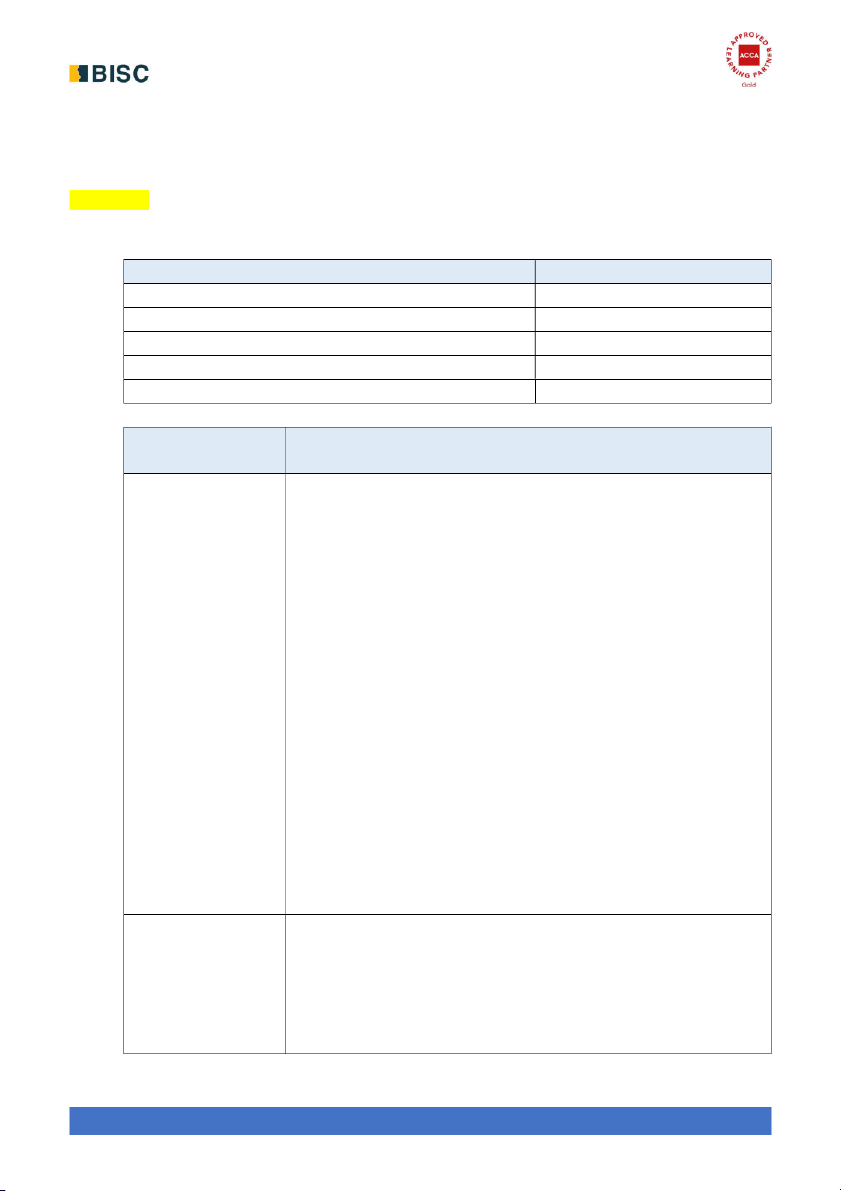

1. Using the table below, describe the five components of an entity's system of internal control. (5 marks) Component of internal control Description Control environment

Entity's risk assessment process

Entity's process to monitor the system of internal control

Information system and communication Control activities Component of Description internal control

Control environment - The control environment includes the governance and management

functions and the attitudes, awareness and actions of those charged

with governance and management

concerning the entity’s system of internal control and its importance

in the entity. The control environment sets the tone of an

organisation, influencing the control consciousness of its people and

provides the overall foundation for the operation of other components

- The control environment encompasses many elements, such as how

management’s responsibilities are carried out (such as creating and

maintaining the entity’s culture and demonstrating management’s

commitment to integrity and ethical values); how those charged with

governance demonstrate independence from management and

exercise oversight of the entity’s system of internal control; how the

entity assigns authority and responsibility in pursuit of its objectives;

how the entity attracts, develops and retains competent individuals

in alignment with its objectives; and how the entity holds individuals

accountable for their responsibilities in pursuit of the entity’s system of internal control. Entity's risk

The entity’s risk assessment process is an iterative process for assessment process

identifying and analysing risks to achieve the entity’s objectives and

forms the basis for determining the risks to be

managed. For financial reporting purposes, the entity’s risk

assessment process includes how management identifies business

risks relevant to the preparation of financial statements

BẢN QUYỀN THUỘC BISC TRAINING CENTER GIANG HÀ ACCA

in accordance with the entity’s applicable financial reporting

framework. It estimates their significance, assesses the likelihood of

their occurrence, and decides upon actions to respond to and

manage them and the results thereof Entity's process to

Monitoring of controls is a continual process to assess the monitor the system

effectiveness of internal control performance over time. It involves of internal control

assessing the effectiveness of controls and taking necessary remedial

actions on a timely basis. Management accomplishes the monitoring

of controls through ongoing activities, separate evaluations, or a combination of the two.

Ongoing monitoring activities are often built into the normal

recurring activities of an entity and include regular management and supervisory activities Information system

The information system relevant to the preparation of the financial and communication

statements consists of the activities, policies and records designed

and established to initiate, record, process, and report entity

transactions (as well as events and conditions) and to maintain

accountability for the related assets, liabilities, and equity

Communication which involves providing an understanding of

individual roles and responsibilities may be through policy and

accounting and financial reporting manuals. It may be made

electronically, orally or through management actions Control activities

Control activities include controls which are designed to ensure

proper application of policies in all the components of the entity’s

system of internal control and include both direct and indirect

controls. Control activities include information processing controls

and general IT controls and may be manual or automated in nature.

They have various objectives and are applied at various organisational and functional levels.

They may include authorisation and approvals, reconciliations,

verifications, physical or logical controls and/or segregation of duties

2. Describe substantive procedures the auditor should perform to obtain sufficient and

appropriate audit evidence in relation to Daley Co's bank balances. (4 marks)

Substantive procedures over the bank balances

- Obtain a bank confirmation letter from Daley Co’s bank for all of its bank accounts.

- Agree all accounts listed on the bank confirmation letter to Daley Co’s bank reconciliations

- Obtain the year-end bank reconciliations and cast to ensure mathematical accuracy.

- Agree the balance per cash book on the year-end bank reconciliation statements to the cash

book/trial balance/financial statements.

BẢN QUYỀN THUỘC BISC TRAINING CENTER GIANG HÀ ACCA

- Agree the balance per the bank reconciliations to the year-end bank confirmation letter and bank statements.

- Trace all outstanding lodgements/deposits to the pre year-end cash book, post year-end bank statement and also to the

- Paying in book pre year end.

- Trace all unpresented cheques through to the pre year-end cash book and post year-end bank

statements. For any unusual amounts or delays, obtain explanations from management.

- Examine any old unpresented cheques to assess if they need to be written back to the payables

ledger as they are no longer valid.

- Examine the bank confirmation letter for details of any security provided by the company or any

legal right of set-off as this may require disclosure.

- Review the cash book and bank statements for any unusual items or large transfers around the

year end as this may be evidence of window dressing

3. Explain the PURPOSE of an audit engagement letter and list FOUR items which should be

included in an audit engagement letter.(4 marks)

Engagement letter purpose and matters to be included

The audit engagement letter outlines the nature of the contract between the audit firm and the audit

client. Its purpose is to minimise the risk of any misunderstanding of the terms of the engagement

between the auditor and the client and it confirms acceptance of the engagement. The purpose of

the engagement letter is to also set out the terms and conditions of the engagement and the

responsibilities of the auditor and management.

Matters which should be included in the engagement letter include:

- The objective and scope of the audit;

- The auditor's responsibilities;

- Management's responsibilities;

- Identification of the applicable financial reporting framework for the preparation of the financial statements;

- Expected form and content of any reports to be issued by the auditor and a statement that there

may be circumstances in which a report may differ from its expected form and content;

- Elaboration of the scope of the audit with reference to legislation;

- The form of any other communication of results of the audit engagement;

- The requirement for the auditor to communicate key audit matters in accordance with ISA 701

Communicating Key Audit Matters in the Independent Auditor's Report;

- The fact that some material misstatements may not be detected;

- Arrangements regarding the planning and performance of the audit, including the composition of the audit team;

- The expectation that management will provide written representations;

- The expectation that management will provide access to all information relevant to or affecting the financial statements;

- The basis on which fees are computed and any billing arrangements;

BẢN QUYỀN THUỘC BISC TRAINING CENTER GIANG HÀ ACCA

- A request for management to acknowledge receipt of the audit engagement letter and to agree to the terms of the engagement

- Arrangements concerning the involvement of internal auditors and other staff of the entity;

- Any obligations to provide audit working papers to other parties;

- Any restriction on the auditor’s liability; and

- Arrangements to make available draft financial statements and any other information

4. Describe substantive procedures the auditor should perform to obtain sufficient and

appropriate audit evidence in relation to the COMPLETENESS of Pacific Co’s trade payables and accruals. (5 marks)

- Calculate the payables payment period for Pacific Co, compare to prior years and investigate any

significant differences, in particular any decrease this year due to the inclusion of the payment run on 1 June.

- Compare the total trade payables, or significant supplier balances, and good received not

invoiced (GRNI) accrual against the prior year and investigate any significant differences.

- Compare the list of accruals this year to the prior year to identify any missing items or unusual

fluctuations and discuss with management.

- Discuss with management the process they have undertaken to quantify the misstatement of

trade payables due to the payment run and consider the materiality of the error in isolation as

well as with other misstatements found.

- Review the journal entry processed to correct the misstatement of trade payables due to the

payment run to ensure all errors have been included.

- Select a sample of purchase invoices received around the year end. Ascertain, through reviewing

goods received notes (GRNs), if the goods were received pre or post year end. If post year end,

then confirm that they have been excluded from the ledger.

- Review after-date payments; if they relate to the current year, then follow through to the

payables ledger or GRNI accrual to ensure they are recorded in the correct period.

- Reperform a sample of supplier statement reconciliations and agree these to the payables

ledger balances. Investigate any reconciling items.

- Select a sample of trade payables balances and perform a trade payables’ circularisation. Follow

up any non-responses and any reconciling items between the balance confirmed and the trade payables’ balance.

- Select a sample of GRNs before the year end and after the year end and follow through to

inclusion of the liability in the correct period’s payables balance to ensure correct cut-off

5. Describe substantive procedures the auditor should perform to obtain sufficient and

appropriate audit evidence in relation to Pacific Co’s provision for the legal claims. (6 marks)

- Enquire with the directors or inspect relevant supporting documentation to confirm if a present

obligation exists at the year end.

- Discuss with directors how the mislabelling of ingredients is alleged to have occurred and

whether it is likely that any other customers have been affected.

BẢN QUYỀN THUỘC BISC TRAINING CENTER GIANG HÀ ACCA

- Discuss the claim with management and review the internal investigation report in order to gain

an insight into the circumstances which led to the mislabelling.

- Inspect board minutes to ascertain whether payment is probable.

- Inspect post year-end bank statements to identify whether any payments have been made in respect of the claim.

- Review correspondence with Pacific Co’s lawyers or with the client’s permission, contact the

lawyers and obtain confirmation regarding the claim to assess whether a provision should be

recognised and whether the amount of the provision is material.

- Review correspondence or discuss with lawyers the likelihood and amount of other potential future claims.

- If evidence indicates that it is only possible that the claim will be successful, inspect the financial

statement for contingent liability disclosures to ensure compliance with IAS 37 Provisions,

Contingent Liabilities and Contingent Assets

- Obtain a written representation from management confirming their view that they have an

obligation at the year end in respect of the claim and that it is appropriate to include a provision MAR/ JUN 22

1. Describe the PRECONDITIONS for an audit that Bannock & Co should have established prior to

accepting the audit of Esk Co. Preconditions for an audit

In order to establish whether the preconditions for an audit are present, Bannock & Co must:

- Determine whether the financial reporting framework (tor example IFRS) to be applied by Esk

Co in the preparation of its financial statements is acceptable. In considering this, the auditor

should have assessed the nature of the entity, the nature and purpose of the financial

statements and whether law or regulation prescribes the applicable reporting framework; and

- Obtain the agreement of the management of Esk Co that they acknowledge and understand their responsibility:

+ for the preparation of the financial statements in accordance with the applicable financial

reporting framework, including where relevant their fair presentation;

+ for the design and implementation of internal controls which management considers

necessary to enable Esk Co to prepare financial statements which are free from material

misstatement, whether due to fraud or error; and

+ to provide Bannock & Co with access to all information which is relevant to the preparation of

the financial stay-vents such as records, documentation and other matters. Access to

information includes any additional information Which Bannock & Co may request from

management for the purpose of the audit and an agreement to provide unrestricted access to

ESk co's staff in order that Bannock & co can obtain relevant evidence.

2. Describe FOUR matters the auditor may consider in determining whether a deficiency in

internal control is significant.

BẢN QUYỀN THUỘC BISC TRAINING CENTER GIANG HÀ ACCA

ISA 265 Communicating Deficiencies in Internal Control to Those Charged With Governance and

Management details matters the external auditor should consider when determining whether a

deficiency in internal control is significant, including:

- The likelihood of the deficiency (or deficiencies) resulting in material misstatements in the

financial statements in the future.

- The susceptibility to loss or fraud of the related asset or liability.

- The subjectivity and complexity of determining estimated amounts.

- The amounts exposed to the deficiencies.

- The volume of activity which has occurred or could occur in the account balance or class of

transaction exposed to the deficiency or deficiencies.

- The importance of the identified deficient controls to the financial reporting process.

- The cause and frequency of the exceptions identified as a result of the deficiencies in the controls.

- The interaction of the deficiency with other deficiencies in internal control.

3. Describe substantive procedures the auditor should perform to obtain sufficient and

appropriate audit evidence in relation to Spinach Co’s revenue.

Substantive procedures for revenue

- Cast a breakdown of revenue and agree to the general ledger, trial balance and draft financial statements.

- Compare the overall level of revenue against prior year/budget and investigate any significant fluctuations.

- Obtain a breakdown of sales analysed by month and compare this to the prior year/month.

Investigate any significant fluctuations.

- Obtain a schedule of sales for the year disaggregated into the main product categories/by type of

customer by month and compare this to the prior year breakdown. Discuss any unusual movements with management.

- Perform a proof in total calculation for revenue by taking the prior year revenue and increasing it

for the three new product lines launched in February 20X5 and the price rise in line With inflation

from September 20X4 and other known factors. This expectation should be compared to actual

revenue and any significant fluctuations should be investigated.

- Calculate the gross profit margin for Spinach Co for the year, compare this to the prior year and

investigate any significant fluctuations.

- Select a sample of sales invoices for wholesale customers and agree the sales prices back to the

price list or customer master data information, noting whether the price was pre or post the price

increase, to confirm the accuracy of invoices.

- For a sample of invoices, recalculate invoice totals including any discounts and sales tax.

- Select a sample of credit notes raised, trace through to the original invoice and ensure the invoice

has been correctly removed from sales.

- Select a sample of dispatch notes and agree these to sales invoices through to inclusion in the

sales day book and revenue accounts in the general ledger to confirm completeness of revenue.

BẢN QUYỀN THUỘC BISC TRAINING CENTER GIANG HÀ ACCA

- Select a sample of dispatch notes both pre and post year end and follow these through to sales

invoices in the correct accounting period to ensure that cut-off has been correctly applied.

- Select a sample of website sales made in the final week prior to the year end and where goods

were dispatched post year end, confirm that the sale proceeds received are recorded as deferred

income (contract liability) rather tun as revenue.

4. Describe the audit procedures the auditor should perform as part of the audit of Spinach Co

BEFORE and DURING the inventory count. Inventory count procedures Before the count

- Review the prior year audit files to identify whether there were any particular warehouses where

significant inventory issues arose last year.

- Discuss with management whether any of the warehouses this year are new, whether any

significant changes have occurred this year with regards to inventory items or if any warehouses have

experienced significant control issues.

- Decide WhiCh of the six warehouses the audit team members Will attend, basing this on

materiality and risk of each site.

- Obtain a copy of the proposed inventory count instructions, review them to identify any control

deficiencies and, if any are noted, discuss them with management prior to the counts.

- Discuss With management whether third-party inventory is stored in any Of the other warehouses and What the procedures are

- for ensuring that third-party inventory is omitted from the counts. During the count

- Observe the counting teams of Spinach Co to confirm whether the inventory count instructions are being followed correctly.

- Select samples of inventory and perform test counts from inventory sheets to physical inventory

and from physical inventory to inventory sheets.

- Observe the counts in order to confirm that the procedures for identifying and segregating

damaged goods are operating correctly and inspect inventory for evidence of any damaged or slow- moving items.

- Observe the procedures for movements of inventory during the counts, in order to confirm that all movements have ceased.

- Discuss with the internal audit supervisors how any raw materials quantities have been estimated.

Where possible, reperform the procedures adopted by the supervisors.

- Obtain a copy of the completed sequentially numbered inventory sheets for follow up testing at the final audit.

- Obtain copies of the last goods received notes (GRNs) and goods dispatched notes (GDNs) for 31

July and request copies of GRNs and GDNs raised on 1 August in order to perform cut-off procedures as at the year end.

BẢN QUYỀN THUỘC BISC TRAINING CENTER GIANG HÀ ACCA

- Observe the procedures carried out by Spinach Co's staff in identifying third-party inventories are

operating correctly and review the completed inventory count sheets to confirm no third-party inventory is included.

- Select samples of inventory and perform test counts from inventory sheets to physical inventory

and from physical inventory to inventory sheets.

5. Describe substantive procedures the auditor should perform to obtain sufficient and

appropriate audit evidence in relation to Spinach Co’s issue of share capital.

Substantive procedures for issue of share capital

- Review board minutes to confirm the number of additional shares issued in May 20X5 and the issue price.

- Agree the issue of shares is permitted from a review of any statutory constitution agreements in place.

- Review legal documentation, correspondence or share issue prospectus to confirm the details of the share issue.

- Agree the issue of new shares to the share register.

- Inspect the cash book and bank statements for evidence of the amount of cash received from the share issue.

- Where the sum received is less than $4.3m, confirm the difference is treated as share capital

called up but not paid in the financial statements.

- Recalculate the split of proceeds between the nominal value of shares and premium on issue

and agree correctly recorded within share capital and share premium account (other components of equity).

- Review the disclosure of the share issue in the draft financial statements and ensure it is in line

with relevant accounting standards and local legislation.

6. (i) Describe the factors which the audit engagement partner would have considered in

determining that this issue is a KAM; and

(ii) Describe the content of the KAM section of the auditor’s report for Spinach Co. Auditor's report (i) Factors to consider

As Spinach Co is listed, a key audit matters (KAM) section will be required in the auditor's report.

The audit partner would have considered whether the matter was communicated to those charged

with governance as KAM are selected from matters communicated to those charged with

governance. The audit partner would have also considered the level of risk in relation to the

valuation of inventory and, as determining the net realisable value is an accounting estimate, the

level of judgement involved. The audit partner would have also considered whether, in their

professional judgement, the matters regarding the valuation of inventory were of most significance

in the audit of Spinach Co's financial statements for the year ended 31 July 20X5. (ii) Contents of KAM

BẢN QUYỀN THUỘC BISC TRAINING CENTER GIANG HÀ ACCA

The KAM section of the auditor's report should include a reference to the audit risk in relation to the

valuation of inventory and the level Of judgement required in making this assessment. It Should

detail why this issue was considered to be an area of significance in the audit and therefore

determined to be a KAM. It should also explain how the matter was addressed in the audit and the

auditor Should provide a brief overview of the audit procedures adopted as well as detailing that a

review was undertaken of any related disclosures. SEP/ DEC 21

1. Describe Apricot & Co's responsibilities in relation to the prevention and detection of fraud and error. (4 marks)

Auditor’s responsibilities in relation to the prevention and detection of fraud and error

- Apricot & Co must conduct an audit in accordance with ISA 240 The Auditor’s Responsibilities

Relating to Fraud in an Audit of Financial Statements and are responsible for obtaining

reasonable assurance that the financial statements taken as a whole are free from material

misstatement, whether caused by fraud or error.

- Apricot & Co is required to identify and assess the risks of material misstatement of the financial statements due to fraud.

- The auditor needs to obtain sufficient appropriate audit evidence regarding the assessed risks of

material misstatement due to fraud, through designing and implementing appropriate responses.

- Apricot & Co must respond appropriately to fraud or suspected fraud identified during the audit,

for example, the fraud regarding the purchase of assets for personal use identified by Peach Co.

- When obtaining reasonable assurance, Apricot & Co is responsible for maintaining professional

scepticism throughout the audit, considering the potential for management override of controls

and recognising the fact that audit procedures which are effective in detecting error may not be effective in detecting fraud.

- To ensure that the whole engagement team is aware of the risks and responsibilities for fraud

and error, ISAs require that a discussion is held within the team.

- Apricot & Co must report any actual or suspected fraud to appropriate parties.

2. Describe substantive procedures the auditor should perform to obtain sufficient and

appropriate audit evidence in relation to Peach Co's development expenditure (6 marks)

- Obtain a schedule of capitalised costs within intangible assets, cast it and agree the closing

balance to the general ledger, trial balance and financial statements.

- Select a sample of capitalised costs and agree to invoices, payroll records or other source

documentation in order to confirm that the amount is correct and that the cost relates to the project.

- Discuss with the directors the decision to capitalise the costs from 1 November 20X4 onwards

and assess whether this is based on the project meeting all of the conditions for capitalisation in IAS 38.

BẢN QUYỀN THUỘC BISC TRAINING CENTER GIANG HÀ ACCA

- Review a breakdown of the nature of the costs capitalised to identify if any research costs have

been incorrectly included. If so, request that management remove these and include within profit or loss.

- Select a sample of costs recorded as research expenses and development costs and agree to

supporting documentation confirming the date of the expenditure to ensure that costs were allocated correctly.

- Review market research reports to confirm that there is a market for the new process and that

the selling price is high enough to generate a profit.

- Review feasibility reports as at 1 November 20X4 and discuss with directors their view that the

process was technically feasible at that date

3. Describe the LIMITATIONS of internal control. (4 marks)

Note: You do not need to refer to the scenario to answer this requirement.

There are limitations in any system of internal control which affects the extent to which the auditor

can place reliance on it. The limitations are as follows:

Human error in the design of or application of an internal control

An entity may have an adequate internal control process over a particular area of the financial

statements. However, human error in applying that control gives rise to an inherent limitation, for

example a staff member may review a bank reconciliation but not identify an error.

There may also be a flaw in the design of internal control whereby there is an error in the design of,

or change to, an internal control which means it does not operate as intended.

Circumvention of internal control

No system of internal control will be completely effective at preventing and detecting fraud and

error. Employees may manipulate deficiencies in an entity’s internal control for personal gain or to

conceal fraudulent activity. This is more likely to be possible where

there is collusion between employees.

Management override of internal control

Management is in a position of power to override an entity’s internal control regardless of the

strength of the system of internal control. Such management override could be to conceal

information or for personal financial gain.

Use of judgement on the nature and extent of controls

Management is responsible for implementing controls which are designed to prevent, detect and

correct material misstatements and safeguard the company’s assets. Professional judgement will be

needed to determine the type and extent of internal controls needed within the company and

certain controls may be absent or ineffective. In particular, systems may be designed to deal with

routine transactions and may therefore be inadequate in respect of non-routine transactions.

4. Describe substantive procedures the auditor should perform to obtain sufficient and

appropriate audit evidence in relation to Danube Co’s land and buildings. (6 marks)

BẢN QUYỀN THUỘC BISC TRAINING CENTER GIANG HÀ ACCA

- Obtain a schedule of all land and buildings, cast and agree to the trial balance and financial statements.

- Consider the competence and capability of the valuer, by assessing through enquiry their

qualification, membership of a professional body and experience in valuing these types of assets.

- Review the assumptions and method adopted by the valuer in undertaking the revaluation to

confirm the reasonableness and compliance with principles of IAS 16.

- Agree the schedule of revalued land and buildings to the valuation statement provided by the

valuer and to the non-current assets register.

- Agree all land and buildings on the non-current assets register to the valuation report to ensure

completeness of the land and buildings valued to ensure all assets in the same category have

been revalued in line with IAS 16.

- Recalculate the total revaluation adjustment and agree correctly recorded in the revaluation surplus.

- Recalculate the depreciation charge for the year and confirm that for assets revalued at July

20X4, the depreciation was based on cost before the revaluation and based on the valuation after on a pro rata basis.

- For a sample of land and buildings from the non-current assets register, physically verify to confirm existence.

- For a sample of land and buildings trace back to the non-current assets register and general

ledger to confirm completeness.

- Review the financial statements disclosures relating to land and buildings to ensure they comply with IAS 16.

5. Describe substantive procedures the auditor should perform to obtain sufficient and

appropriate audit evidence in relation to the PROVISION and the RECEIVABLE arising from the

sale of defective goods (5 marks)

- Review the correspondence with Kalama Kids Co and establish the details of the claim to assess

whether a present obligation as a result of a past event has occurred.

- Review correspondence with Thames Co, the supplier of the hoverboards, to assess whether

they accept liability for the defect.

- Review correspondence with Danube Co’s legal advisers or, with the client’s permission, contact

the legal advisers to obtain their view as to the probability of either the legal claim from the

customer and the request for reimbursement from the supplier being successful as well as any

likely amounts to be paid or received.

- Discuss with management/enquire of the legal adviser as to whether any other customers of

Danube Co have experienced problems with sales of hoverboards and therefore the likelihood

of any potential future claims.

- Review board minutes to establish whether the directors believe that either claim will be successful or not.

BẢN QUYỀN THUỘC BISC TRAINING CENTER GIANG HÀ ACCA

- Review the post year-end cash book to assess whether any payments have been made to the

customer or cash received from the supplier and compare with the amounts recognised in the financial statements.

- Discuss with management why they have included a receivable for the claim against the supplier

as this is possibly a contingent asset and should only be recognised as an asset if the receipt of

cash is virtually certain. Consider the reasonableness of the proposed treatment.

- Obtain a written representation confirming management’s view that the lawsuit by Kalama Kids

Co is likely to be successful and the claim against Thames Co is virtually certain and hence a

provision and a receivable are required to be included.

- Review the adequacy of the disclosures of the lawsuit and supplier claim in the draft financial

statements to ensure they are in accordance with IAS 37

BẢN QUYỀN THUỘC BISC TRAINING CENTER GIANG HÀ ACCA

Tài liệu liên quan:

-

Nhận Dạng Rủi Ro Tín Dụng - Tài Liệu Học Tập Cơ Bản

8 4 -

Đề cương ôn tập môn Kiểm toán | Học viện Ngân hàng

65 33 -

Câu hỏi trắc nghiệm (có đáp án) môn Kiểm toán | Học viện Ngân hàng

51 26 -

Tổng ôn kiến thức và khái niệm cơ bản môn Kiểm toán | Học viện Ngân hàng

52 26 -

Đáp án đề thi mẫu môn Kiểm toán | Học viện Ngân hàng

55 28