CFA Level 1: Comprehensive Formulas for Financial Concepts

CFA Level 1: Comprehensive Formulas for Financial Concepts. Tài liệu sưu tầm. Mời bạn tham khảo

Môn: Tài liệu Tổng hợp 3.6 K tài liệu

Trường: Tài liệu khác 3.9 K tài liệu

Tác giả:

Preview text:

CFA Level 1 All Formulas

Post Graduate Diploma in management (Rajagiri Business School)

Downloaded by v ng (ngttgi20804@gmail.com)

Downloaded by v ng (ngttgi20804@gmail.com)

Copyright © 2017 by John Wiley & Sons, Inc. All rights reserved.

Published by John Wiley & Sons, Inc., Hoboken, New Jersey.

Published simultaneously in Canada.

No part of this publication may be reproduced, stored in a retrieval system, or transmitted in any

form or by any means, electronic, mechanical, photocopying, recording, scanning, or otherwise,

except as permitted under Section 107 or 108 of the 1976 United States Copyright Act, without

either the prior written permission of the Publisher, or authorization through payment of the

appropriate per-copy fee to the Copyright Clearance Center, Inc., 222 Rosewood Drive, Danvers,

MA 01923, (978) 750-8400, fax (978) 646-8600, or on the Web at www.copyright.com. Requests

to the Publisher for permission should be addressed to the Permissions Department, John Wiley &

Sons, Inc., 111 River Street, Hoboken, NJ 07030, (201) 748-6011, fax (201) 748-6008, or online

at http://www.wiley.com/go/permissions.

Limit of Liability/Disclaimer of Warranty: While the publisher and author have used their best

efforts in preparing this book, they make no representations or warranties with respect to the

accuracy or completeness of the contents of this book and specifically disclaim any implied

warranties of merchantability or fitness for a particular purpose. No warranty may be created or

extended by sales representatives or written sales materials. The advice and strategies contained

herein may not be suitable for your situation. You should consult with a professional where

appropriate. Neither the publisher nor author shall be liable for any loss of profit or any other

commercial damages, including but not limited to special, incidental, consequential, or other damages.

For general information on our other products and services or for technical support, please contact

our Customer Care Department within the United States at (800) 762-2974, outside the United

States at (317) 572-3993 or fax (317) 572-4002.

Wiley publishes in a variety of print and electronic formats and by print-on-demand. Some

material included with standard print versions of this book may not be included in e-books or in

print-on-demand. If this book refers to media such as a CD or DVD that is not included in the

version you purchased, you may download this material at http://booksupport.wiley.com. For

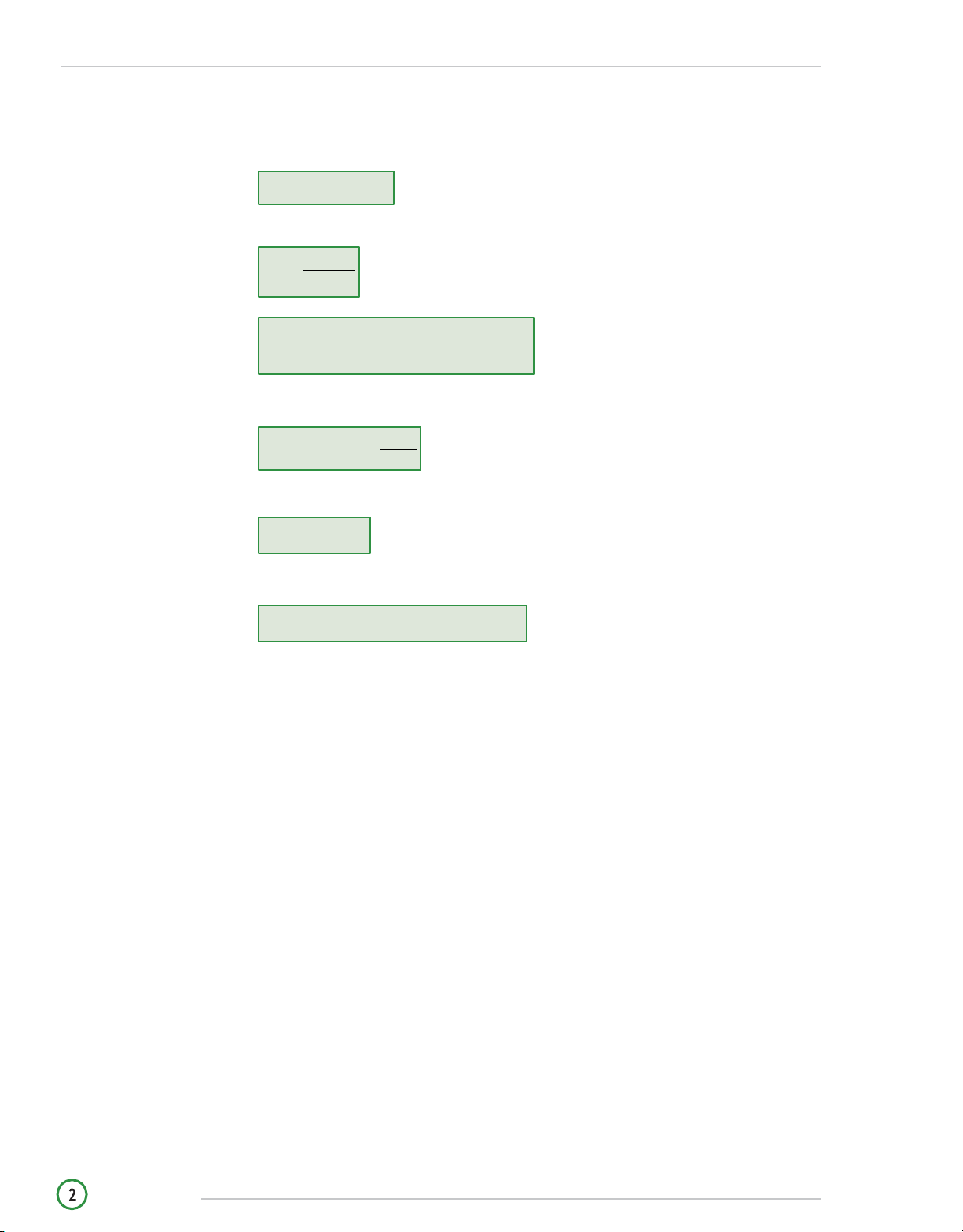

more information about Wiley products, visit www.wiley.com. QUANTITATIVe MeTHODs THE TIME VALUE OF MONEY

THe TIme VAlUe of MoneY

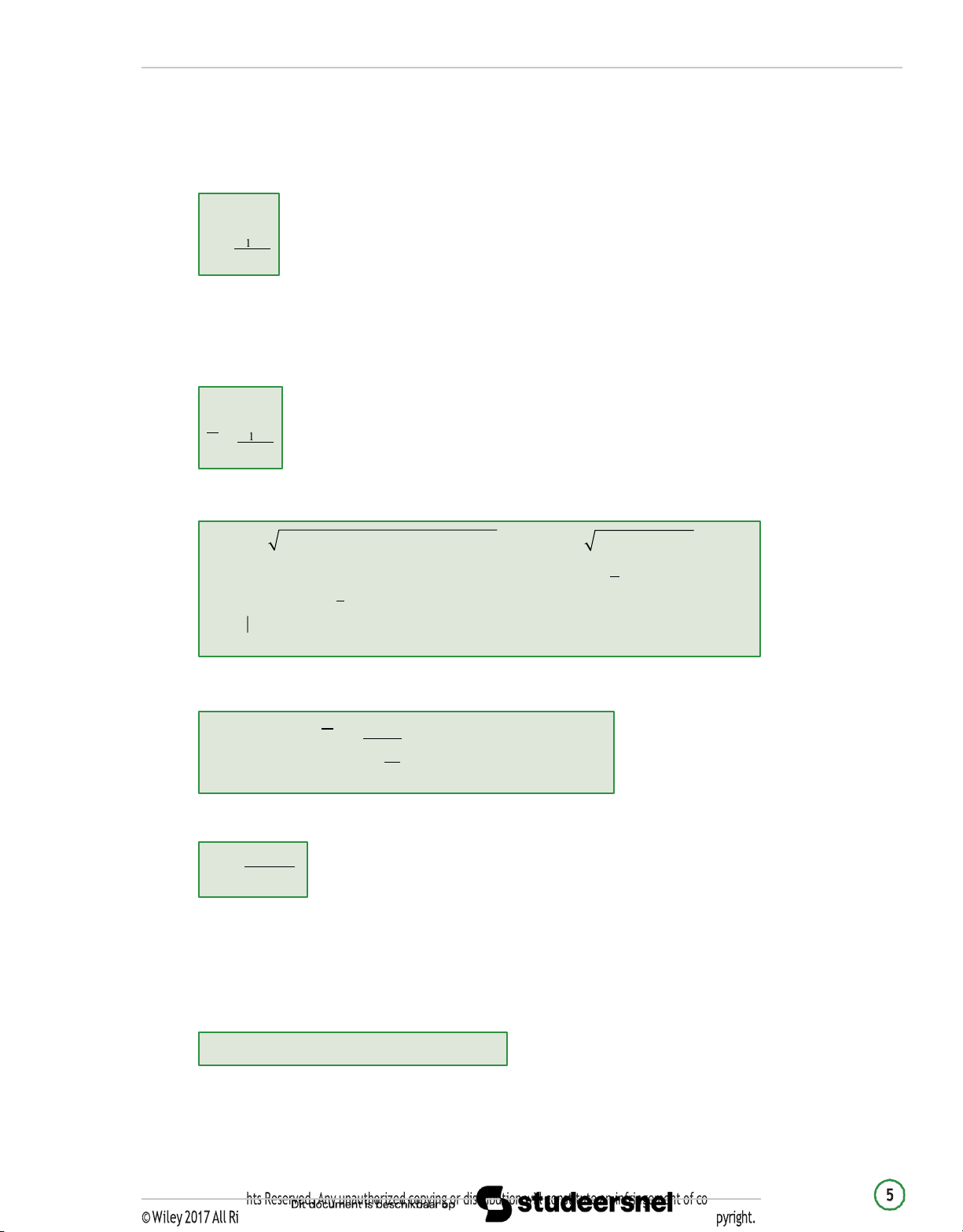

The Future Value of a Single Cash Flow FVN = PV (1 + r)N

The Present Value of a Single Cash Flow FV PV = (1 + r)N

PVAnnuity Due = PVOrdinary Annuity (1 + r)

FVAnnuity Due = FVOrdinary Annuity (1 + r)

Present Value of a Perpetuity PMT PV(perpetuity) = I/Y

Continuous Compounding and Future Values FV N N = PVers Effective Annual Rates

EAR = (1 + Periodic interest rate)N − 1

© Wiley 2017 Al Rights Reserved. Any unauthorized copying or distribution wil constitute an infringement of copyright.

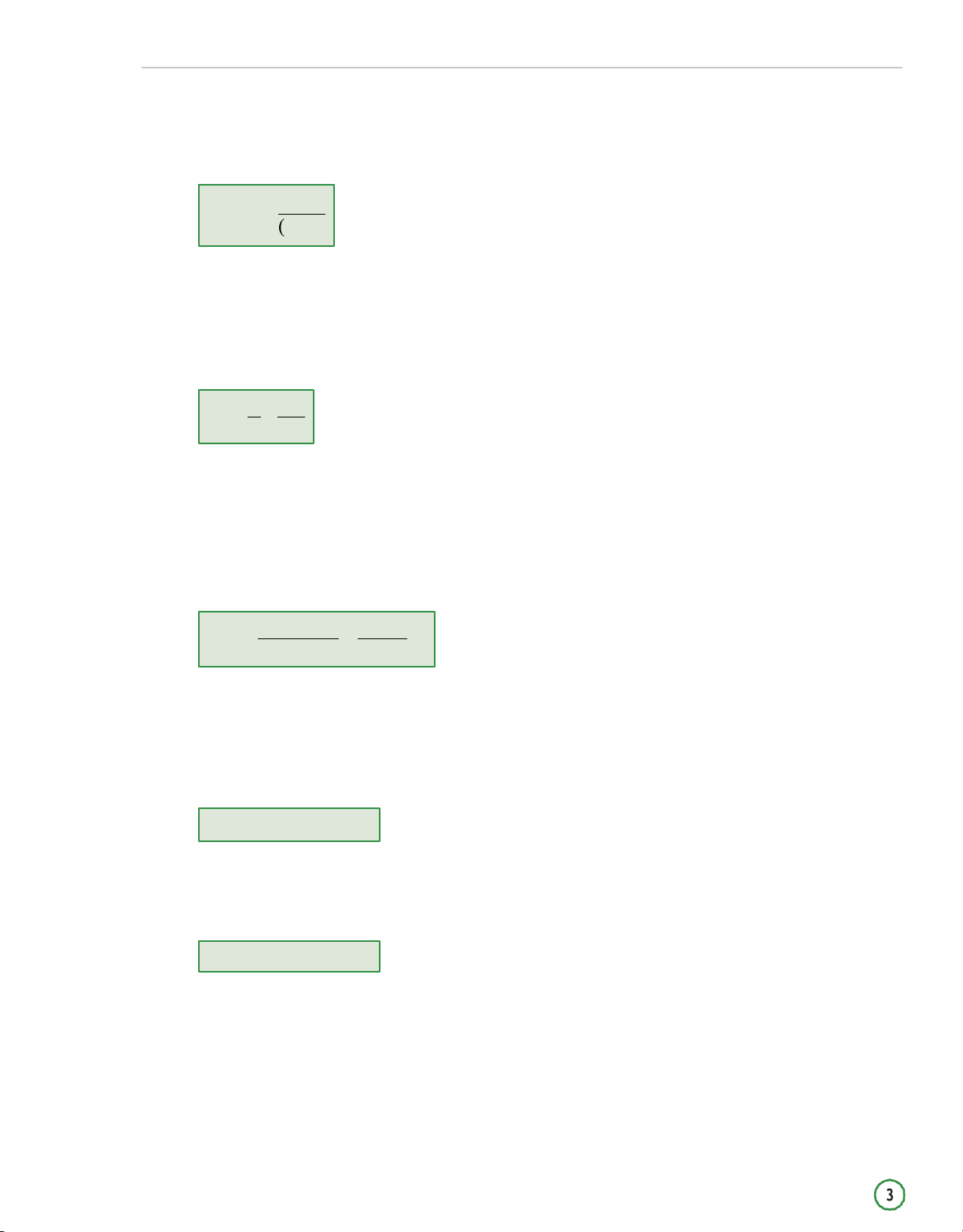

DISCOUNTED CASH FLOW APPLICATIONS

DIscoUNTed CAsH Flow APPlICATIONs Net Present Value N NPV = CFt t=0 1 + r) t where:

CFt = the expected net cash flow at time t

N = the investment’s projected life

r = the discount rate or appropriate cost of capital Bank Discount Yield r = D 360 BD F t where:

rBD = the annualized yield on a bank discount basis

D = the dollar discount (face value – purchase price)

F = the face value of the bill

t = number of days remaining until maturity Holding Period Yield P P

HPY = 1 − P0 + D1 = 1 + D1 − 1 P0 P0 where:

P0 = initial price of the investment.

P1 = price received from the instrument at maturity/sale.

D1 = interest or dividend received from the investment. Effective Annual Yield EAY = (1 + HPY)365/t − 1 where: HPY = holding period yield

t = numbers of days remaining till maturity HPY = (1 + EAY)t/365 − 1

ghts Reserved. Any unauthorized copying or distribution wil constitute an infringement of co

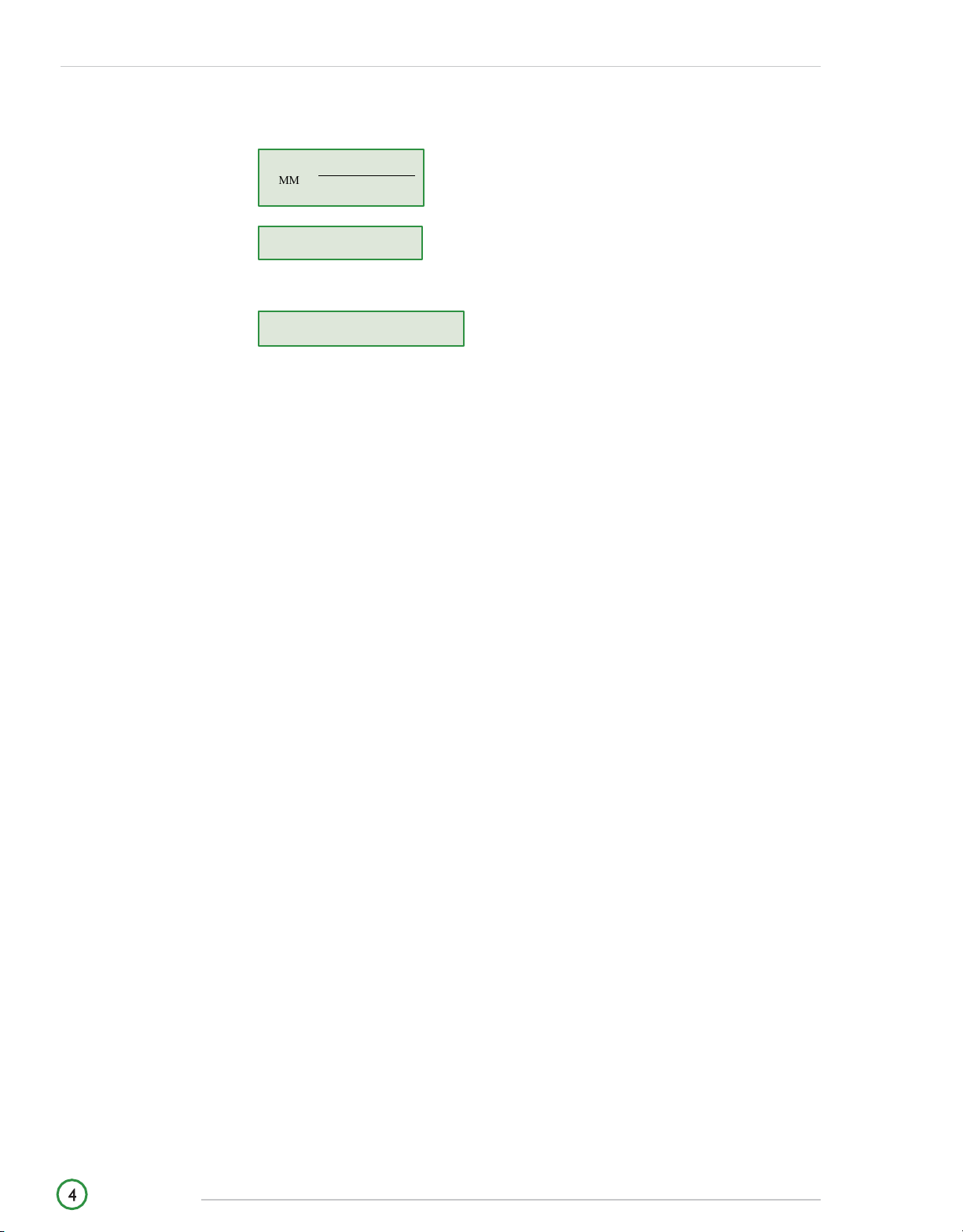

DISCOUNTED CASH FLOW APPLICATIONS Money Market Yield 360 rBD RMM = 360 − (t rBD ) RMM = HPY (360/t) Bond Equivalent Yield

BEY = [(1 + EAY)0.5 − 1] 2

© Wiley 2017 Al Rights Reserved. Any unauthorized copying or distribution wil constitute an infringement of copyright. STATISTICAL CONCEPTS STATIsTICAl ConcePTs Population Mean N xi = i= 1 N where:

xi = is the ith observation. Sample Mean n xi X = i= 1 n Geometric Mean

1 + RG = T (1 + R1) (1 + R2 ) (1 + RT ) OR G = n X1X2 X3 Xn

with Xi 0 fori = 1, 2,, n. 1 T T RG = (1 + Rt ) − 1 t=1 Harmonic Mean N Harmonic mean: XH =

with X 0 for i = 1,2,,N. N i 1 x i=1 i Percentiles (n + 1)y L = y 100 where:

y = percentage point at which we are dividing the distribution

Ly = location (L) of the percentile (Py) in the data set sorted in ascending order Range

Range = Maximum value − Minimum value

ghts Reserved. Any unauthorized copying or distribution wil constitute an infringement of co STATISTICAL CONCEPTS

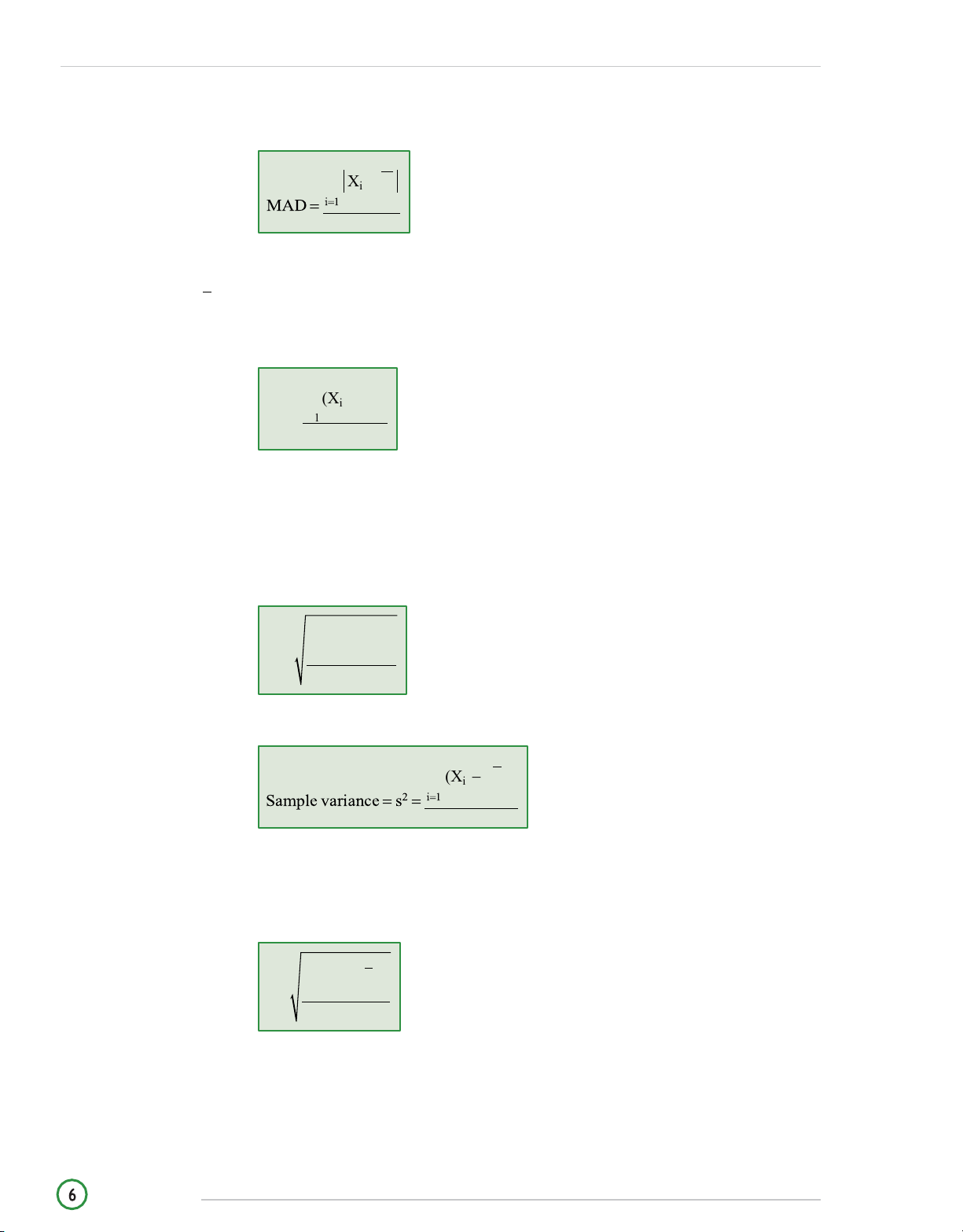

Mean Absolute Deviation n Xi − X n where:

n = number of items in the data set

X = the arithmetic mean of the sample Population Variance N (Xi − )2 2 = i= 1 N where: Xi = observation i μ = population mean N = size of the population

Population Standard Deviation N (Xi − )2 = i=1 N Sample Variance n (Xi − X)2 n − 1 where: n = sample size.

Sample Standard Deviation n (Xi − X)2 s = i=1 n − 1

© Wiley 2017 Al Rights Reserved. Any unauthorized copying or distribution wil constitute an infringement of copyright. STATISTICAL CONCEPTS

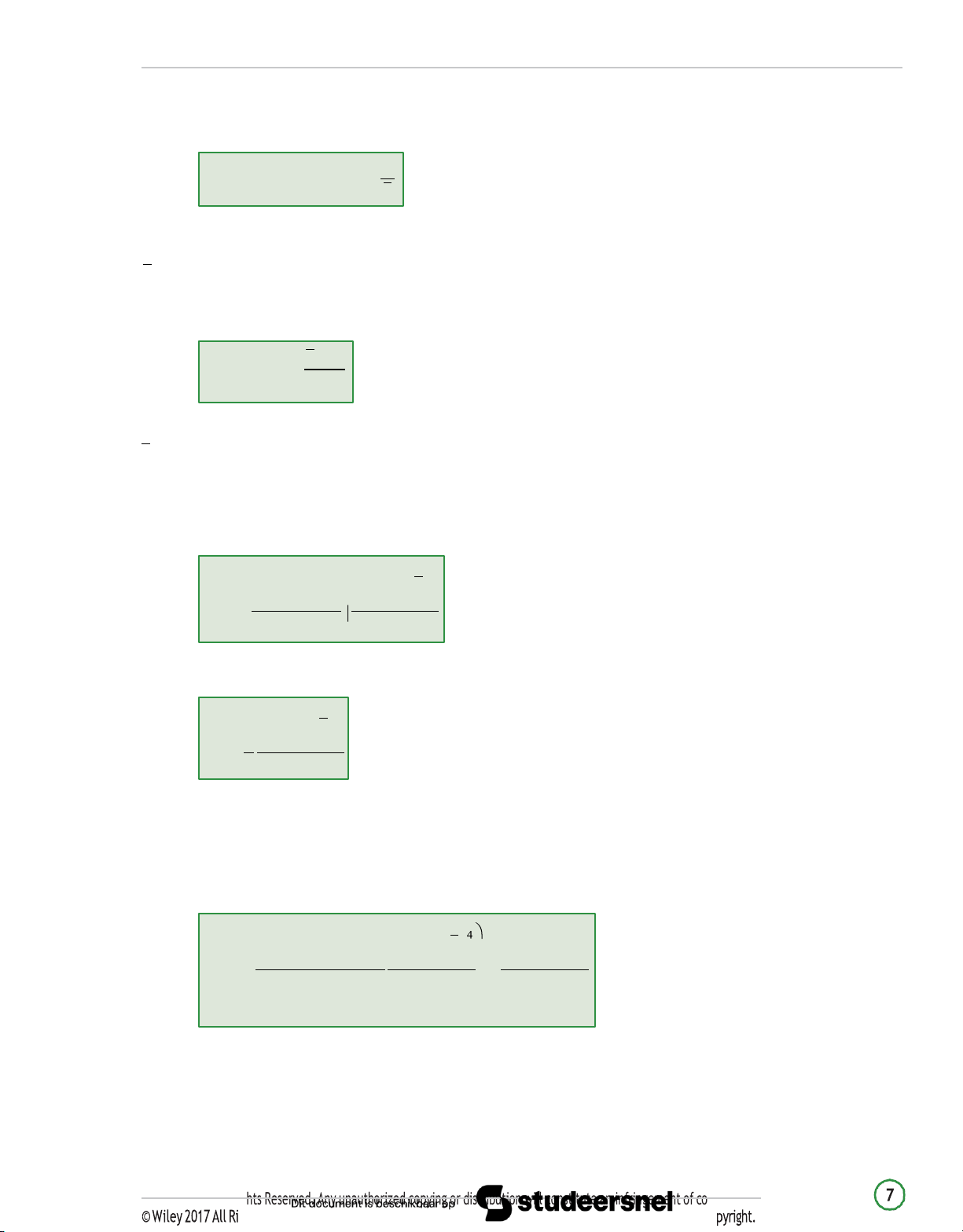

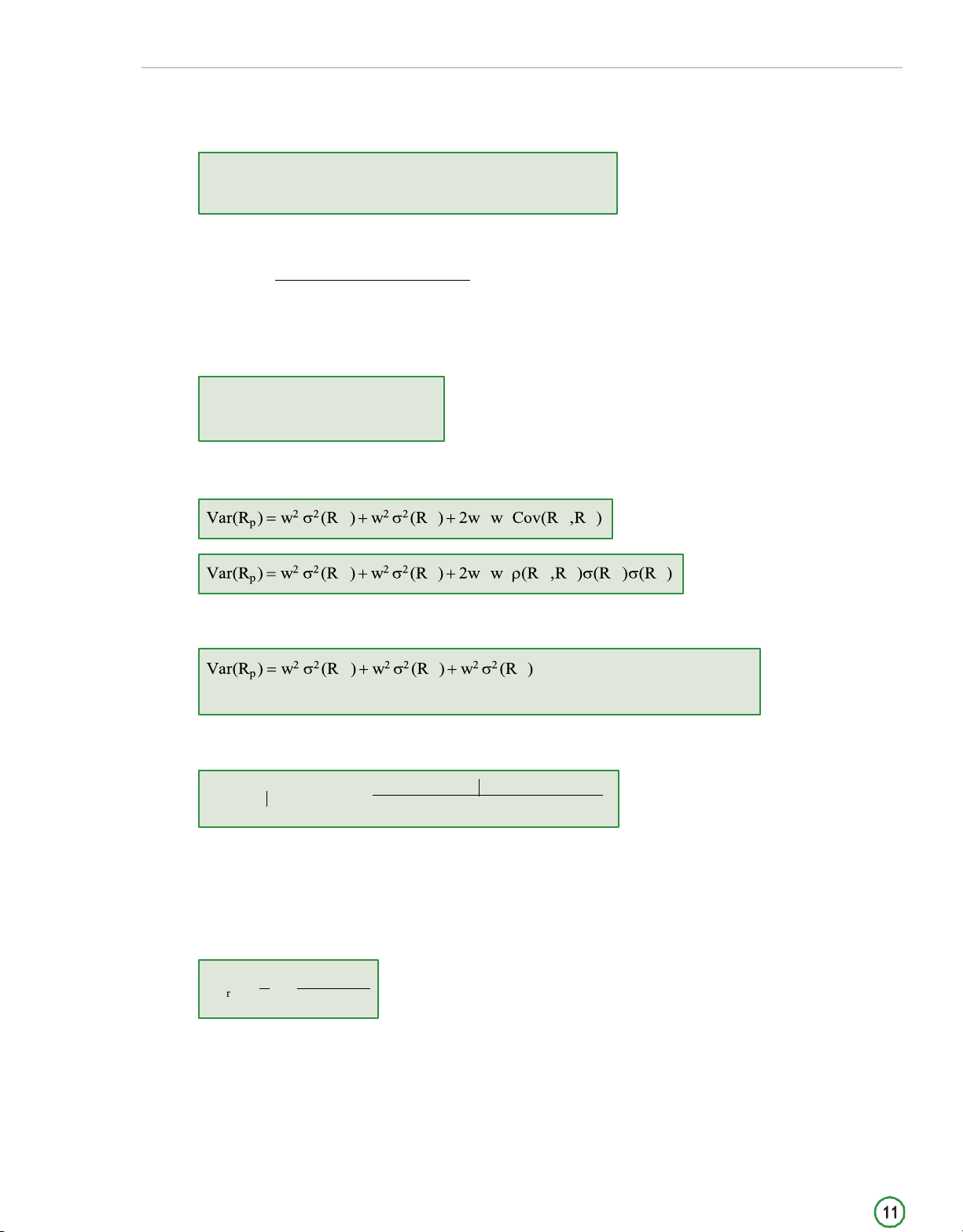

Coefficient of Variation s Coefficient of variation = X where: s = sample standard deviation X = the sample mean. Sharpe Ratio r Sharpe ratio = p − rf sp where: rp = mean portfolio return rf = risk‐free return

sp = standard deviation of portfolio returns

Sample skewness, also known as sample relative skewness, is calculated as: n (X n i − X)3 S = i=1 K

( n − 1)(n − 2) s3

As n becomes large, the expression reduces to the mean cubed deviation. n (Xi − X)3 1 S i=1 K n s3 where: s = sample standard deviation

Sample Kurtosis uses standard deviations to the fourth power. Sample excess kurtosis is calculated as: n (Xi − X) n(n + 1) 3(n − 1)2 i=1 K − E = 4

(n − 1)(n − 2)(n − 3) s (n − 2)(n − 3)

ghts Reserved. Any unauthorized copying or distribution wil constitute an infringement of co STATISTICAL CONCEPTS

As n becomes large the equation simplifies to: n (X 1 i − X)4 K i=1 E − 3 n s4 where: s = sample standard deviation

For a sample size greater than 100, a sample excess kurtosis of greater than 1.0 would be

considered unusually high. Most equity return series have been found to be leptokurtic.

© Wiley 2017 Al Rights Reserved. Any unauthorized copying or distribution wil constitute an infringement of copyright. PROBABILITY CONCEPTS PROBABIlITY ConcePTs Odds for an Event a P(E) = (a + b)

Where the odds for are given as “a to b”, then: Odds for an Event b P(E) = (a + b)

Where the odds against are given as “a to b”, then:

Conditional Probabilities P(AB) P(A B) = given that P(B) 0 P(B)

Multiplication Rule for Probabilities P(AB) = P(A B) P(B)

Addition Rule for Probabilities

P(A or B) = P(A) + P(B) − P(AB) For Independant Events

P(A B) = P(A), or equivalently, P(B A) = P(B)

P(A or B) = P(A) + P(B) − P(AB) P(A and B) = P(A) P(B)

The Total Probability Rule P(A) = P(AS) + P(ASc )

P(A) = P(A S) P(S) + P(A Sc ) P(Sc )

The Total Probability Rule for n Possible Scenarios

P(A) = P(A S1) P(S1) + P(A S2 ) P(S2 ) +⋯+ P(A Sn ) P(Sn )

where the set of events {S1, S2 ,, Sn} is mutually exclusive and exhaustive.

ghts Reserved. Any unauthorized copying or distribution wil constitute an infringement of co PROBABILITY CONCEPTS Expected Value

E(X) = P(X1)X1 + P(X2 )X2 + P(Xn )Xn n E(X) = P(Xi )Xi i=1 where:

Xi = one of n possible outcomes.

Variance and Standard Deviation 2 (X) = E{[X − E(X)]2} n

2 (X) = P(Xi ) [Xi − E(X)]2 i=1

The Total Probability Rule for Expected Value

1. E(X) = E(X | S)P(S) + E(X | Sc)P(Sc)

2. E(X) = E(X | S1) × P(S1) + E(X | S2) × P(S2) + . . . + E(X | Sn) × P(Sn) where:

E(X) = the unconditional expected value of X

E(X | S1) = the expected value of X given Scenario 1

P(S1) = the probability of Scenario 1 occurring

The set of events {S1, S2, . . . , Sn} is mutually exclusive and exhaustive. Covariance

Cov(XY) = E{[X − E(X)][Y − E(Y)]}

Cov(RA ,RB ) = E{[RA − E(RA )][RB − E(RB )]}

Correlation Coefficient Cov(R ,R ) Corr(R A B A ,R B) = (R A ,R B) = (A )(B)

© Wiley 2017 Al Rights Reserved. Any unauthorized copying or distribution wil constitute an infringement of copyright. PROBABILITY CONCEPTS

Expected Return on a Portfolio N

E(Rp ) = wi E(Ri ) = w1E(R1) + w2E(R2 ) +⋯+ wNE(RN ) i=1 where: Market value of investment i Weight of asseti = Market value of portfolio Portfolio Variance N N

Var(Rp ) = wiwjCov(Ri ,R j) i=1 j=1

Variance of a 2 Asset Portfolio A A B B A B A B A A B B A B A B A B

Variance of a 3 Asset Portfolio A A B B C C

+ 2wA wBCov(RA ,RB ) + 2wBwCCov(RB ,RC ) + 2wCwACov(RC ,RA ) Bayes’ Formula

P(Event Information) = P (Information Event) P (Event) P (Information) Counting Rules

The number of different ways that the k tasks can be done equals n1 n2 n3 nk . Combinations C = n = n! n r r (n − r)!(r!)

Remember: The combination formula is used when the order in which the items are

assigned the labels is NOT important. Permutations

ghts Reserved. Any unauthorized copying or distribution wil constitute an infringement of co

COMMON PROBABILITY DISTRIBUTIONS

Common PROBABIlITY DIsTRIBUTIONs

Discrete Uniform Distribution

F(x) = n p(x) for the nth observation. Binomial Distribution

P(X=x) = nCx (p)x (1 − p)n-x where: p = probability of success

1 − p = probability of failure

nCx = number of possible combinations of having x successes in n trials. Stated differently,

it is the number of ways to choose x from n when the order does not matter.

Variance of a Binomial Random Variable

2 x = n p (1 − p) Tracking Error

Tracking error = Gross return on portfolio − Total return on benchmark index

The Continuous Uniform Distribution P(X a), P (X b) = 0

P (x X x ) = x2 − x 1 1 2 b − a Confidence Intervals

For a random variable X that follows the normal distribution:

The 90% confidence interval is x − 1.65s to x + 1.65s

The 95% confidence interval is x − 1.96s to x + 1.96s

The 99% confidence interval is x − 2.58s to x + 2.58s

The following probability statements can be made about normal distributions

• Approximately 50% of all observations lie in the interval μ ± (2/3)σ

• Approximately 68% of all observations lie in the interval μ ± 1σ

• Approximately 95% of all observations lie in the interval μ ± 2σ

• Approximately 99% of all observations lie in the interval μ ± 3σ

Tài liệu liên quan:

-

Ung dung game hoa trong cac chien dich MKT

34 17 -

Bao cao Chi so TMDT Viet Nam 2025

34 17 -

Thông tư quy định về việc phân quyền, phân cấp và phân định thẩm quyền quản lý nhà nước về giáo dục cho chính quyền địa phương

40 20 -

Nghị quyết về phát huy các giá trị di sản văn hóa gắn với phát triên du lịch bền vững tỉnh Khánh Hòa đến năm 2025, định hướng đến năm 2030

40 20 -

Quyết định phê duyệt Chiến lược phát triển du lịch Việt Nam đến năm 2030

25 13