CFA Level I Formula Sheet & Key Concepts - 2023 Exam Preparation

CFA Level I Formula Sheet & Key Concepts - 2023 Exam Preparation. Tài liệu sưu tầm.Mời các bạn tham khảo

Môn: Tài liệu Tổng hợp 3.6 K tài liệu

Trường: Tài liệu khác 3.9 K tài liệu

Tác giả:

Preview text:

CFA cheat sheet - CFA

CFA Program Curriculum (CFA Université Et Sports) QUANTITATIVE METHODS

Mean Absolute Deviation Sample Covariance MAD = 1 ∑n |X − XE| n i=1 i

∑n 1(Xi − Xb)(𝑌𝑖 − 𝑌b)

THE TIME VALUE OF MONEY n − 1

Variance and Standard Deviation

Required Rate of Return n

Sample Correlation Coefficient 1

interest rate = real risk-free rate Sample variance, s2 = F(Xi − XE)2 r + inflation premium n − 1 i=1 + default risk premium

Standard deviation is square root of variance PROBABILITY CONCEPTS + liquidity premium

Target Downside Deviation + maturity premium Odds

Sample target semideviation, s = X∑Xi≤B(Xi–B)2 P(E)

Future Value (FV) and Present Value (PV) Target n–1 Odds of E = 1 − P(E) FV = PV(1 + r)N

Coefficient of Variation Probabilities Effective Annual Rates

CV = s⁄EX; measures dispersion relative to mean r m

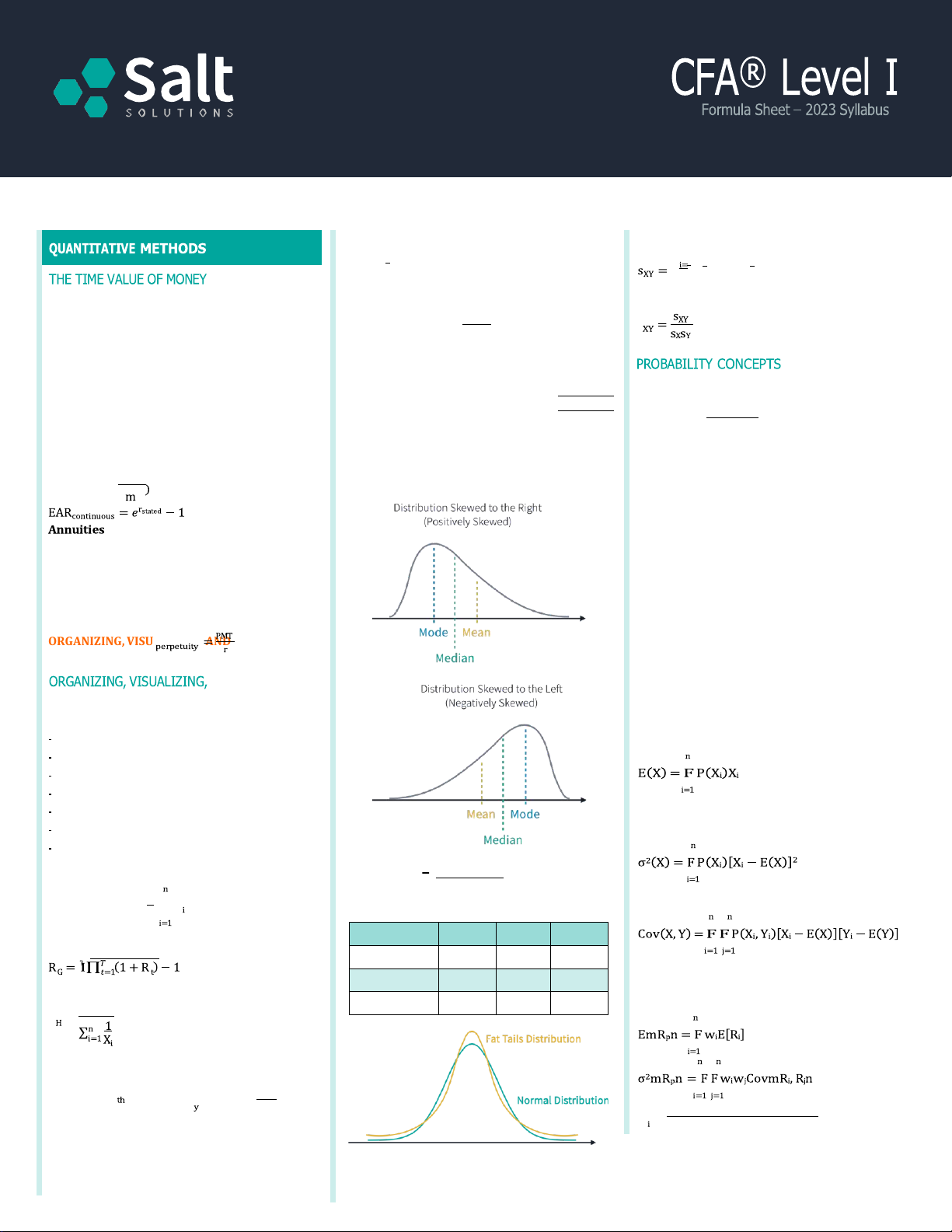

Unconditional: P(A), probability of A EAR = >1 + stated − 1 Skewness

Conditional: P(A|B), probability of A given B

Joint: P(AB), probability of A and B Probability Rules

Annuity: Finite set of level sequential cash flows,

Conditional: P(A|B) = P(AB)/P(B)

valued using calculator’s TVM function

Multiplication: P(AB) = P(A|B) × P(B)

Ordinary Annuity: 1st cash flow received in one year

Addition: P(A or B) = P(A) + P(B) − P(AB)

Annuity Due: 1st cash flow received immediately

Perpetuity: Ordinary annuity with payments that

Total: P(A) = P(A|S1)P(S1) + ⋯ + P(A|Sn)P(Sn) where S O c RG ont A i N nuIZ e I f N orG e , v V e I r S , UA PV LIZING, AND D ESCRIBING

1, S2,… Sn is an exhaustive set of mutually DATA exclusive probabilities Independence AND DESCRIBING DATA

If A and B are independent events, Data Visualization P(AB) = P(A) × P(B)

Histogram and frequency polygon Expected Value Bar chart (and Pareto chart) Tree-map Word cloud/tag cloud

Line chart (and bubble line chart)

E(X) = E(X|S1)P(S1) + ⋯ + E(X|Sn)P(Sn)

Scatter plot (and scatter plot matrix) Variance Heat map 1 ∑n (X − EX)3 Arithmetic Mean Return Skewness ≈ \ ] i=1 i n s3 1

Sample mean, EX = F X ; n = sample size Covariance n

Kurtosis (Excess Kurtosis = Kurtosis – 3) Distribution 𝑇𝑎𝑖𝑙𝑠 Peaked Kurtosis Geometric Mean Return Leptokurtic Fatter More >3

An asset’s covariance with itself is its variance Mesokurtic Normal Normal 3

Harmonic Mean Return (Cost Averaging) Platykurtic Thinner Less <3 n

Expected Value & Variance of Portfolio Return E X =

, where X > 0 for i = 1, 2, … , n If returns are volatile, XE

Arith. > XEGeo. > EXHar. Quantiles y Location of y percentile, L = (n + 1) 100 Market value of investment i w = If L

y is not an integer, use linear interpolation. Market value of portfolio

Distributions may be divided into quarters

(Quartiles), fifths (Quintiles), or tenths (Deciles)

E.g., 50th percentile = 2nd quartile = 5th decile www.saltsolutions.com 1 1 ∑n (X − EX)4

Excess kurtosis, KE ≈ \ ] i=1 i − 3 n s4 www.saltsolutions.com 2

DownloaCdoepydribghyt v© n2g02(1nSgatlttgSio2l0u 8ti o0n4s@

. Agl mRigahilt.scRoemse)rved. Personal copies permited. Resale or distribution is prohibited.

For portfolio with 2 investments: Lognormal Distribution SAMPLING AND E STIMATION EmRpn = wARA + wBRB

- eX where X is normally distributed Sampling - Used to model asset prices

Simple random sampling: Subset of population is

Cov(RA, RB) = σ(RA)σ(RB)ρ(RA, RB) - Positively skewed chosen at random σ2mR

Continuously compounded return from t to t + 1: pn = w2σ2(R ) + w2σ2(R )

Systematic sampling: Every kth observation is St+1 + 2w = ln \ ] = lnm1 + R

chosen until desired sample size is achieved AwBCov(RA, RB) rt,t+1 S t,t+1n t

Stratified sampling: Simple random samples are Correlation

where Rt,t+1 is the effective annual rate

drawn from each subpopulation (strata) ρ

Cluster sampling: Sample set is divided into mini- = CorrmR , R n = ; min −1, max 1

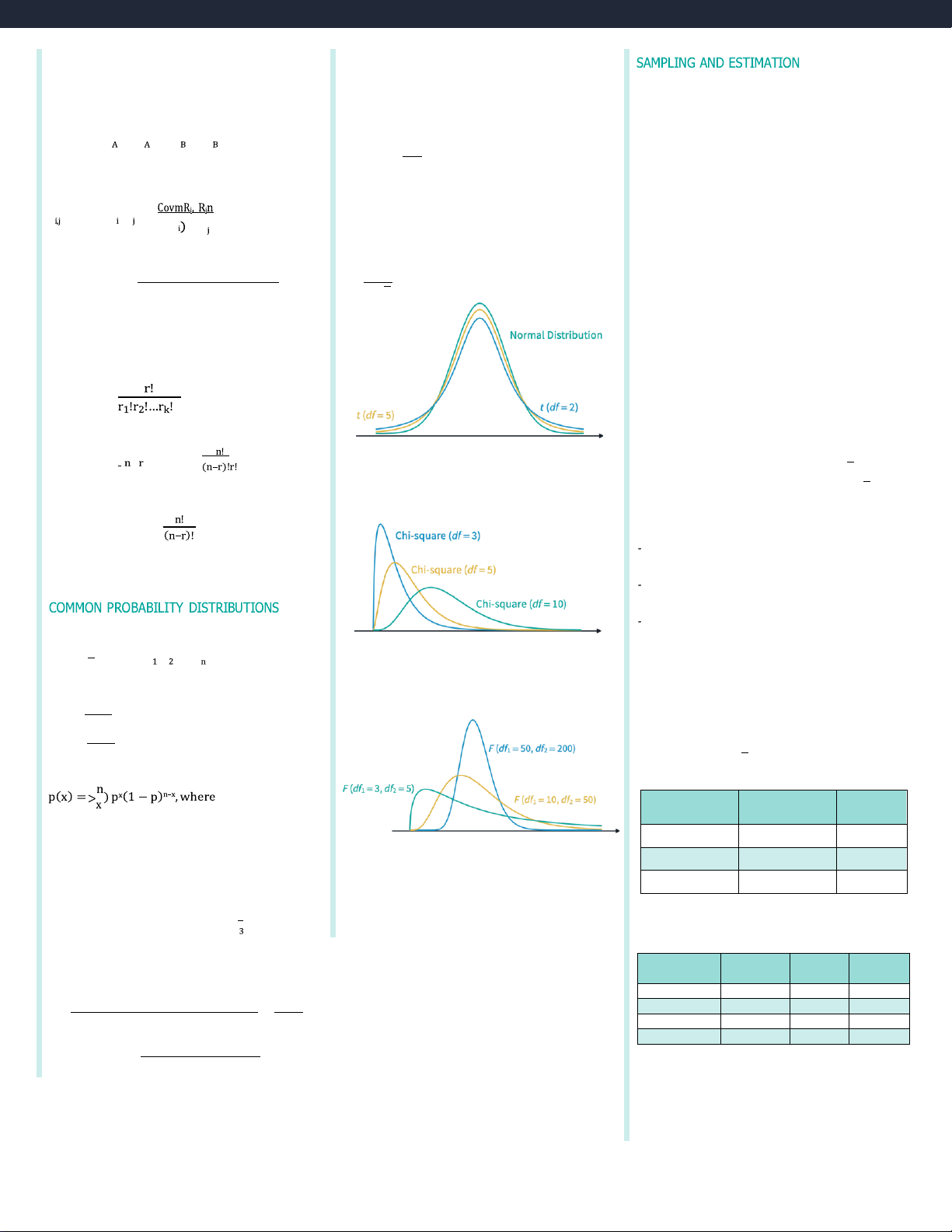

Student’s t-Distribution σ(R σ mR n

representations of the population (cluster)

Parameters: degrees of freedom (df) Bayes’ Formula

Convenience sampling: Samples are selected based

The ratio below is t-distributed with df = n − 1: P(Info|Event) × P(Event) on accessibility XE − µ P(Event|Info) = t = P(Info)

Judgmental sampling: Samples are selected based s/√n

Updates prior probabilities to give posterior

on researchers’ knowledge and expertise

probabilities based on new information

Sampling error = Sample mean – Population mean Counting Rules

Central Limit Theorem (CLT)

Factorial: n! = n(n − 1)(n − 2) … 1

For a sample of size n ≥ 30 from a population with

mean µ and variance σ2, the sample mean XE Multinomial:

approximately follows a normal distribution with

Counts ways to label n items with k labels mean µ and variance σ2⁄n n

Standard Error of Sample Mean Combination: C = (r) =

Chi-Square Distribution

Population variance is known: σx̅ = σ⁄√n

Definition: Sum of squares of independent normal

Counts ways to choose r items from n if order does

Population variance is not known: sx̅ = s⁄√n

random variables. It cannot be negative. NOT matter

Properties of Estimators Permutation: nPr = A point estimator is:

Counts ways to choose r items from n if

Unbiased if its value matches the value of the order does matter parameter it estimates

Efficient if it has the lowest variance of all unbiased estimators COMMON P ROBABILITY D ISTRIBUTIONS

Consistent if its value approaches the parameter

Discrete Uniform Distribution as the sample size increases 1 p(x) = , x = x , x , F-Distribution … , x n Confidence Interval

Definition: A ratio of two chi-square random

Continuous Uniform Distribution

Point estimate ± Reliability factor × Std error

variables (two df’s). It cannot be negative. 1

Point estimate: Estimate of population parameter f(x) = ; a ≤ x ≤ b b − a

Reliability factor: Value from distribution of point x − a F(x) = ; a ≤ x ≤ b

estimate, such as normal or t-distribution b − a

E.g., XE ± z𝝰⁄2 × σ⁄√n Binomial Distribution

Reliability factors for normal distributions Significance Confidence 𝑧𝛼⁄2

n = number of Bernoulli trials level interval p = probability of success 10% 90% 1.645 E(X) = np Simulation Techniques 5% 95% 1.960 σ

Monte Carlo simulation: Generate many random 2(X) = np(1 − p)

samples to produce a distribution of outcomes 1% 99% 2.575

Normal Distribution (µ = mean, σ = SD)

Historical simulation: Sample from a historical

If the population is not normally distributed

~50% of observations are within ± 2 𝜎 of µ

record of returns to simulate a process

and/or variance is unknown, the t- or z-

~68% of observations are within ±𝜎 of µ

distributions may be used to get reliability factors.

~95% of observations are within ±2𝜎 of µ Normally Variance Small Large

~99% of observations are within ±3𝜎 of µ Distributed? known? Sample Sample Yes Yes z z

Observed value − Population mean X − µ Yes No t t or z Z = = Standard deviation σ No Yes n/a z No No n/a t or z EmRpn − shortfall level Shortfall Ratio = σ Resampling P

Bootstrap: Replace each drawn sample with an

identical element for the next draw

Jackknife: Draw each sample by leaving out one

observation at a time without replacement www.saltsolutions.com 3 Biases

Tests Concerning Differences between Means

Assumptions of Simple Linear Regression

Data snooping bias: “Drilling” data to find any

Normal populations with unknown variances that Model

statistically significant relationship are assumed equal:

- Linear relationship between X and Y

Sample selection bias: Excluding unavailable data (XE

- Homoscedasticity (i.e., constant variance of t-statistic = 1 − EX2) − (µ1 − µ2)

Survivorship bias: Excluding the impact of failed s2 s2 1⁄2 residuals)

funds or companies that no longer exist

- Independence between X and Y

Look-ahead bias: Information needed is not known (n - Normality of the residuals 1 − 1)s2 + (n − 1)s2

on the date the observation was recorded Analysis of Variance

Time-period bias: Using data from an era that df = n1 + n2 − 2

Sum of squares error (SSE): Unexplained variation

makes the results time-period specific in Y

Tests Concerning Mean Differences SSE = ∑n mY − YÖ n2 HYPOTHESIS T ES TE TIN STIG NG

Normal populations with unknown variances: i=1 i i db − µ

Sum of squares regression (SSR): Explained

Steps in Hypothesis Testing t-statistic = dO , df = n − 1 variation in Y

State hypotheses (null and alternative) Identify test statistic

Tests Concerning a Single Variance SSR = ∑n mÖY − EYn2 i=1 i Specify significance level

Normal population (df = n – 1):

Sum of squares total (SST): Total variation in Y State decision rule SST = SSE + SSR = ∑n (Y (n − 1)s i − EY)2 2 1 i=1

Collect data; calculate test statistic , σ2 O

Coefficient of determination:

Make decision regarding hypothesis SSR

Tests Concerning Two Variances R2 =

Test Statistic (General) SST Normal populations:

= r2 (if there is only one independent variable)

Sample statistic − Hypothesized value F-statistic:

Standard error of sample statistic s2 1 s2 = − xb n2 for j = 1, 2 MSR s2 SSR/k F = =

Hypothesis Test Results MSE SSE/(n − [k + 1])

Reject H0 if test

Standard error of regression: Type Hypotheses statistic is Nonparametric Tests ∑n mY − YÖ n2 One-tailed H0: µ ≤ µ0

Test that is not concerned with parameter and is s = √MSE = Ü i=1 i i e > critical value n − 2 (upper) Ha: µ > µ0

implemented in situations such as: One-tailed H0: µ ≥ µ0

Data do not meet distributional assumptions

Hypothesis Testing of Linear Regression < critical value (lower) Ha: µ < µ0 Data are subject to outliers Coefficients Data are given in ranks

To test a hypothesis about the slope: < lower critical Two- H0: µ = µ0

Hypothesis does not concern a parameter bÑ value or > upper t = 1 − b1 tailed Ha: µ ≠ µ0 s critical value

Tests Concerning Correlation b^1 s s e ^ = 𝑟√n − 2

Hypothesis Testing Decision Errors t-statistic = b1 , df = n − 2 I∑ n i=1 (Xi − XE)2 √1 − r2 Decision 𝐻O is True 𝐻O is False

To test a hypothesis about the intercept:

To use the Spearman rank correlation coefficient, Do not reject H bÑ O Correct Type II ()

substitute the following value into the t-statistic t = O − bO s Reject HO Type I () Correct calculation: b^0 1 (XE)2 s = ÜMSE á + )

Power of a test = 1 − P(Type II error) = 1 – b^ n(n2 − 1) 0 n n ∑ ( i=1 Xi − EX)2

p-value: smallest value of at which 𝐻O is rejected

INTRODUCTION TO LINEAR REGRESSION

Tests Concerning a Single Mean

Estimated variance of the prediction error for Y: 1 (

Population is normal with known variance:

Simple Linear Regression X − EX)2 s2 = s2 â1 + + ä XE − µ

Y: Dependent variable/explained variable f e n (n − 1)s2x z-statistic = O σ⁄√n

X: Independent variable/explanatory variable

Large sample from any population with unknown Y = bO + b1X + ϵ, variance (2 choices):

where bO is the intercept, b1 is the slope coefficient, XE − µ t-statistic = O , df = n − 1 and ϵ is the error term s⁄√n XE − µ

The parameters can be estimated by: z-statistic = O σ⁄√n Cov[Y, X] ∑n (Y − EY)(X − EX) =

Small sample from normal population with Var[X]

unknown population variance: bÑ E O = EY − bÑ1 X XE − µ t-statistic = O , df = n − 1 s⁄ √n www.saltsolutions.com 3 ECONOMICS Breakeven Analysis

Monopolistic Competition

Economic breakeven occurs if a firm’s accounting - Firms: Many TOPICS IN DEMAND A ND SUPPLY A NALYSIS

profit is enough to cover its implicit opportunity

- Products: Differentiated (via advertising)

costs (i.e., normal profit). In the long run, firms

Own-Price Elasticity of Demand - Barriers to entry: Low

cannot earn positive economic profits.

- Pricing power of firms: Some

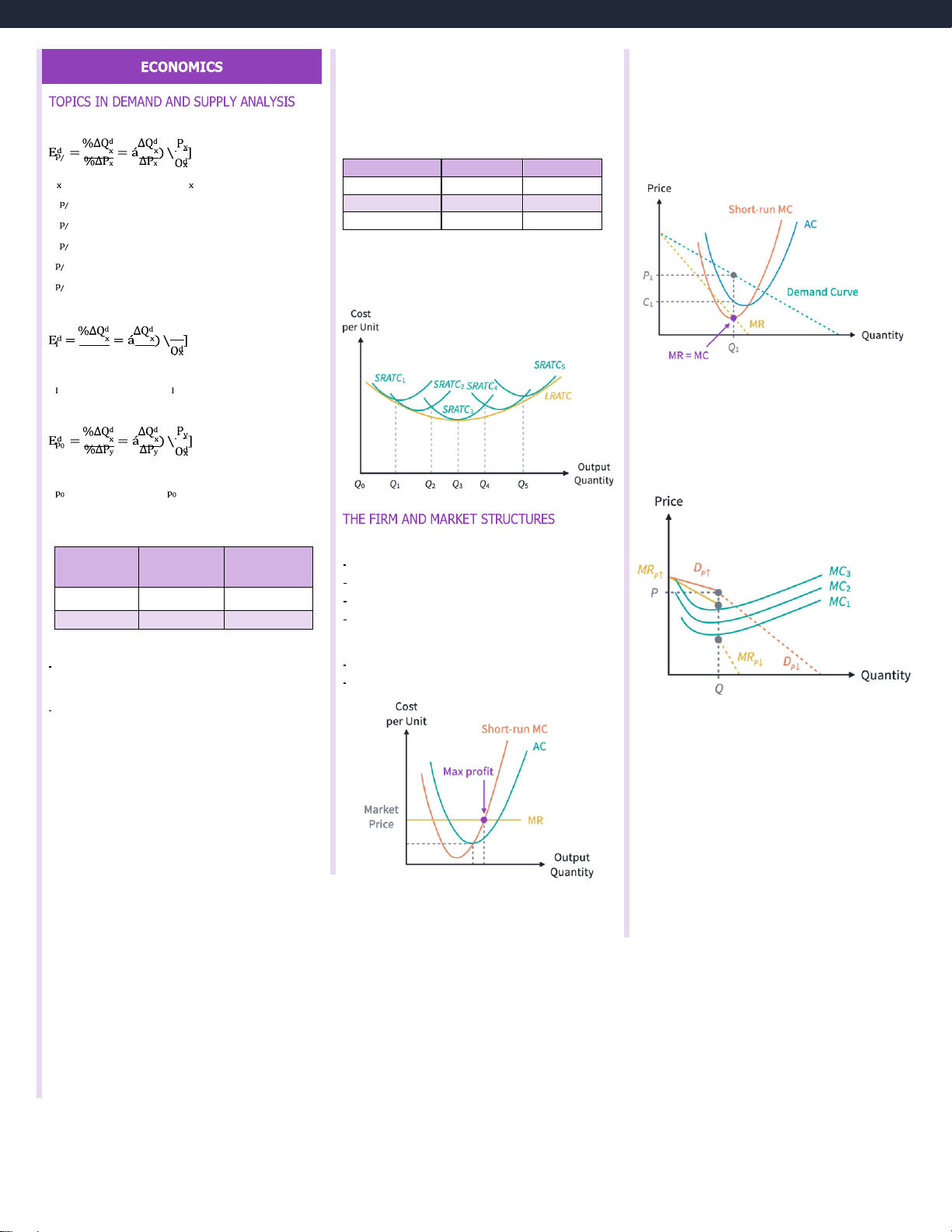

Shutdown Decision (Short-term vs. Long-term)

Profit maximization: MR = MC Short-Term Long-Term

Qd = quantity demanded, P = price per unit TR ≥ TC Stay in Stay in éEd é > 1: elastic TVC < TR < TC Stay in Exit market éEd é < 1: inelastic TR < TVC Shut down Exit market

éEd é = ∞: perfectly elastic Economies of Scale Ed = 0: perfectly inelastic

Each stage of expansion has its own short-run ATC Ed = −1: unit elastic

curve. Minimum efficient scale is the low point on

the long-run average total cost curve.

Income Elasticity of Demand I %ΔI ΔI where I = consumers’ income

Ed > 0: normal good; Ed < 0: inferior good Oligopoly - Firms: Few

Cross-Price Elasticity of Demand

- Products: Similar (close substitutes) - Barriers to entry: High

- Pricing power: Some or considerable

where Py is the price per unit of another good Y

Profit maximization: MR = MC

Ed > 0: substitutes; Ed < 0: complements

Income and Substitution Effects THE FIRM A ND MAR

KET STRUCTURES

Impacts of a reduction in a good’s price: Perfect Competition Substitution Type of good Income effect Firms: Many effect Products: Identical Normal Buy more Buy more Barriers to entry: Very low Inferior Buy less Buy more Pricing power of firms: None

Goods with positively sloped demand curves: Profit maximization:

Giffen goods: Negative income effect is greater P = MR = MC

than positive substitution effect if good’s price

P > ATC economic profit, P < ATC economic loss falls

Veblen goods: Demand for a status symbol good

Kinked demand curve: A price increase will impact falls if its price is reduced

sales more than an equivalent price decrease Revenue Terms

Cournot assumption: Competitors will maintain

current output levels if one firm changes its price

Total revenue (TR): Price times quantity; P × Q

Game theory: If one firm changes its prices,

Average revenue (AR): TR⁄Q

competitors will adjust to maximize their profits,

Marginal revenue (MR): ΔTR⁄ΔQ

resulting in a Nash equilibrium Cost Terms

Price collusion is more likely to happen if:

- Few firms or one dominant firm

Total fixed cost (TFC): Sum of fixed costs

- Products are relatively similar

Total variable cost (TVC): Sum of variable costs

- Firms have similar cost structures

Total costs (TC): TFC + TVC

- Orders are frequent and relatively small

Average fixed cost (AFC): TFC⁄Q

- Credible threat of retaliation for breaking pact

Average variable cost (AVC): TVC⁄Q

- The threat of external competition is high

Average total cost (ATC): AFC + AFV or TC⁄Q

Marginal cost (MC): ΔTC⁄ΔQ Profit Measures

Accounting profit = Revenue − Accounting costs

Economic costs = Accounting costs + Implicit costs

Economic profit = Revenue – Economic costs

= Accounting profit−Implicit costs

Normal profit = Zero economic profit

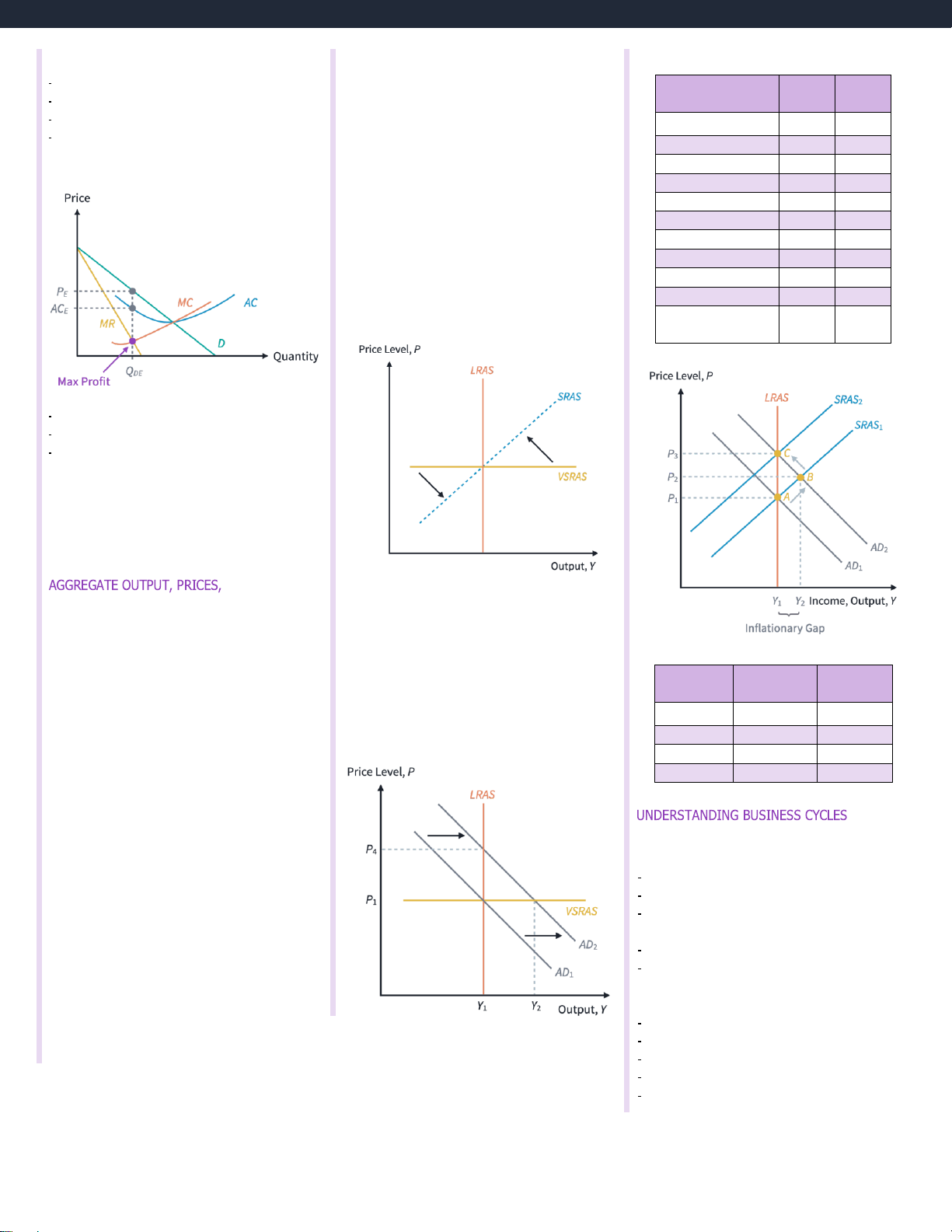

Profits maximized if MR = MC and MC isn’t falling Monopoly

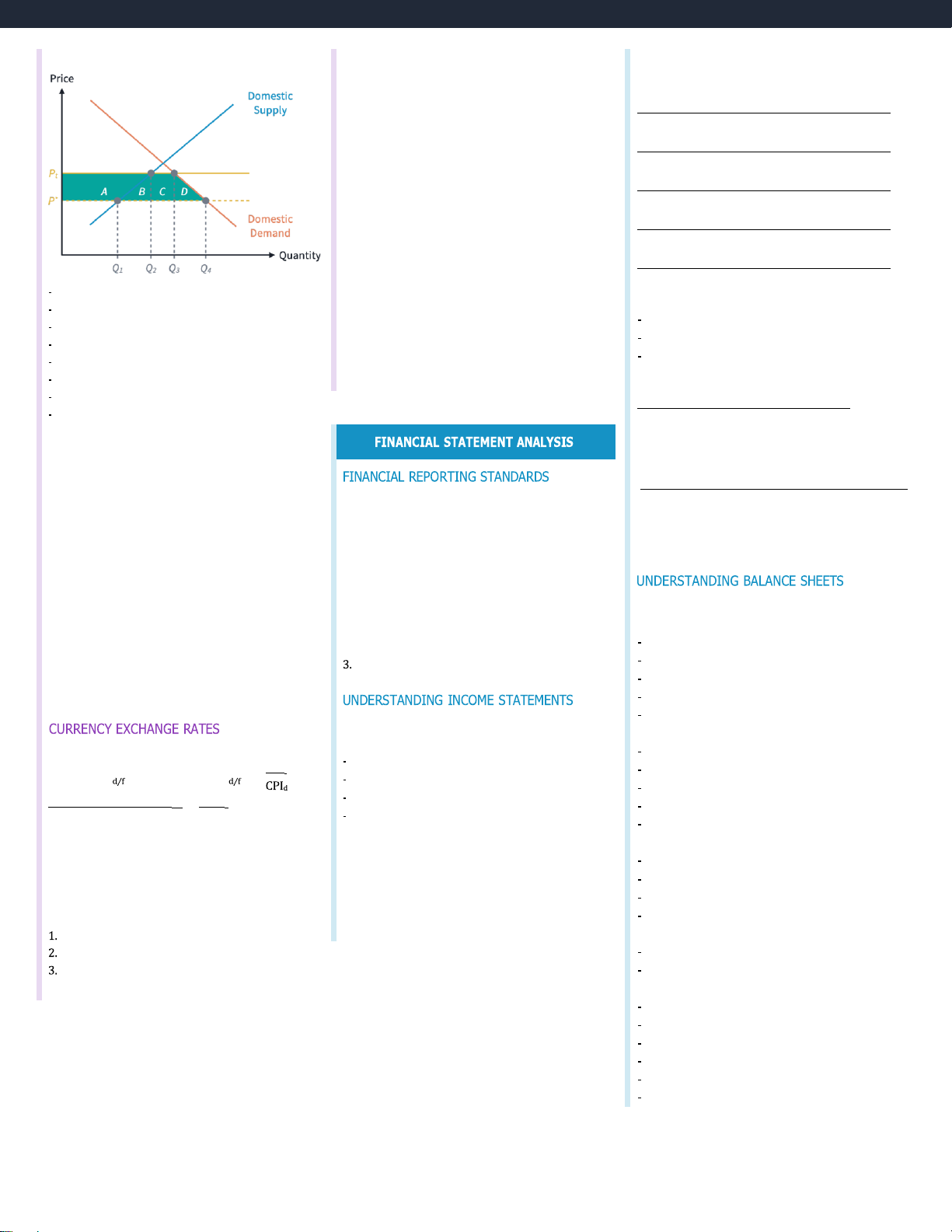

Relationship among Saving, Investment, the

Shifts in Aggregate Supply (SRAS and LRAS) Firm: One

Fiscal Balance, and the Trade Balance SRAS LRAS Increase in

Products: Unique (no close substitutes)

(G − T) = (S − I) − (X − M) Shift Shift Barriers to entry: Very high G − T = fiscal balance Labor supply Right Right

Pricing power of firm: Considerable (price

S − I = savings minus domestic investment Natural resources Right Right discrimination possible) X − M = trade balance Human capital Right Right

Profit maximization: MR = MC Aggregate Demand (AD) Physical capital Right Right

The downward slope of the AD curve results from: Productivity/Tech Right Right

- Wealth effect: Price level ↑, real wealth ↓, quantity Nominal wages Left None demanded ↓ Input prices Left None

- Interest rate effect: Price level ↑, interest rate ↑, Price expectations Right None

investment and consumption expenditures ↓ Business taxes Left None

- Real exchange rate effect: Price level ↑, real Business subsidies Right None

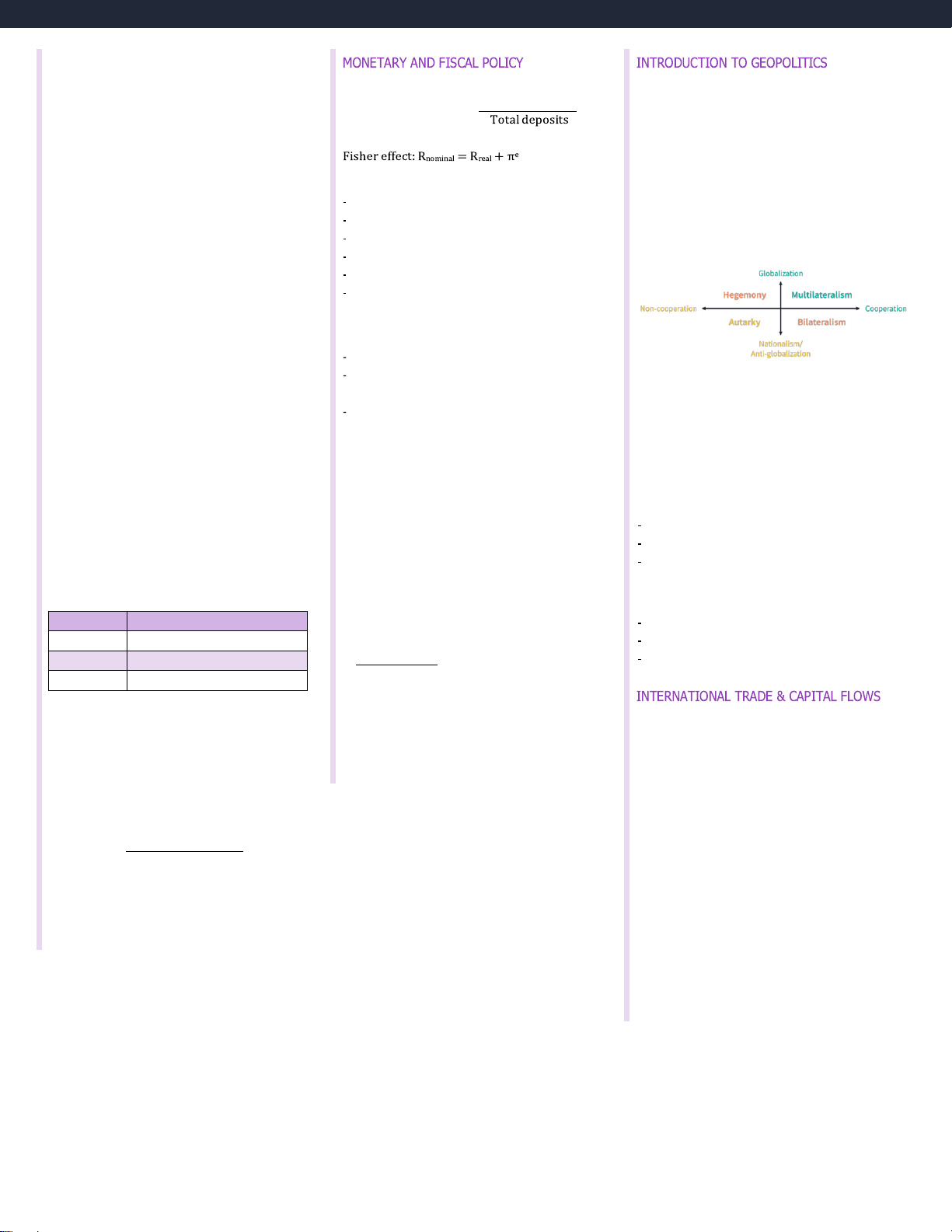

exchange rate ↑, exports ↓ and imports ↑ Foreign currency Right None Aggregate Supply (AS) values Inflationary Gap

Price discrimination by monopolists:

1st degree: Different price for each customer

2nd degree: Quantity-based menu options

3rd degree: Pricing for demographic groups Market Power Measures

N-firm concentration ratio: Sum of market share

of the N largest firms in the industry

Herfindahl-Hirschman Index (HHI): Sum of squared

market share of the N largest firms

AGGREGATE OUTPUT, PRICES, AND ECONOMIC

Full employment level of output: Long-run GR A OW ND T E H C ONOMIC GROWTH equilibrium level of output

Gross Domestic Product (GDP)

Factors Increasing Aggregate Demand (AD)

Nominal GDP: GDP in terms of current prices - Higher household wealth

Effect of Combined Changes in AS and AD

Real GDP: GDP in terms of base-year prices

- Higher business and consumer confidence

GDP deflator: (Nominal GDP⁄Real GDP) × 100 Changes in Real GDP Prices - Higher capacity utilization GDP = C + I + G + (X − M) AS and AD

- Expansionary monetary and fiscal policies C = consumption AS ↑, AD ↑ Increase Unclear

- Depreciating domestic currency value I = investment AS ↓, AD ↓ Decrease Unclear

- Faster global economic growth G = government spending AS ↑, AD ↓ Unclear Decrease X = exports; M = imports AS ↓, AD ↑ Unclear Increase GDI = Net domestic income UNDERSTANDING B

USINESS C YCLES

+ Consumption of fixed capital Business Cycle Phases + Statistical discrepancy Recovery

Economy: Going through a trough GDI

Activity level: Below potential but start to increase = Compensation of employees

Employment: Layoffs slow, but firms prefer

+ Gross operating surplus + Gross mixed income

extending overtime to rehiring full-time

+ Taxes (net of subsidies) on production Inflation: Moderate

+ Taxes (net of subsidies) on products and imports

Capital spending: Low but increasing, with a focus Personal household income

on efficiency rather than capacity = Compensation of employees Expansion + Net mixed income from

Economy: Enjoying an upswing unincorporated businesses

Activity level: Above-average growth rates +Net property income

Employment: Full-time rehiring, more overtime

Inflation: Moderate, but increasing

Capital spending: Focused on capacity expansion www.saltsolutions.com 5 Slowdown

MONETARY AND FISCAL P OLICY INTRODUCTION TO G EOPOLITICS

- Economy: Going through a peak Monetary Policy

National Governments and Political

- Activity level: Decelerating Required reserves Cooperation Required reserve ratio =

- Employment: Hiring slows

State actors possesses the authority to deploy a

- Inflation: Accelerating

Money multiplier = 1⁄Reserve requirement

country’s national security resources

- Capital spending: Strong capital spending, but

Non-State Actors and the Forces of

inventory starts building up as sales growth Globalization Central Bank Roles slows

Non-state actors participate in global political, Sole currency supplier Contraction

economic, or financial affairs but do not control a Lender of last resort

- Economy: Weakens and may go into a recession

country's national security resources

Bank for commercial banks and government

- Activity levels: Below potential

Regulate and supervise payments system

Assessing Geopolitical Actors and Risk

- Employment: Hiring freezes, then layoffs

Gold and foreign exchange reserves holder

- Inflation: Decelerating, but with a lag Oversee monetary policy

- Capital spending: New orders halted and existing Monetary Policy Tools

orders canceled, scale back on maintenance

Expansionary monetary policy measures:

Business Cycle Theories

Policy rate: Set policy rate below neutral level

- Neoclassical: “Invisible hand” lets markets reach a

Reserve requirement: Reduce reserves for

The Tools of Geopolitics

natural equilibrium; government should not commercial banks

National security tool: Military force, espionage intervene

Open market operations: Buy bonds from

Economic tools: Currency union, nationalization

- Austrian: Like Neoclassical, focus on loose commercial banks

Financial tools: Currency markets, sanctions,

monetary policy causing credit-fueled booms capital controls

Fiscal Policy: Spending Tools

- Keynesian: Countercyclical fiscal policy should be

Transfer payments: Redistribution of wealth (e.g.,

Incorporating Geopolitical Risk into the

used to support aggregate demand Investment Process unemployment benefits)

- Monetarist: Oppose Keynesian fiscal focus, call for Types of geopolitical risk:

Current spending: Spending on goods and services steady growth of money Event risk

Capital spending: Spending on infrastructure Unemployment Exogenous risk

- Unemployed: Jobless people who are seeking jobs

Fiscal Policy: Revenue Tools Thematic risk -

Direct taxes: Tax on income (e.g., income taxes,

Labor force: People with a job or unemployed

Assessing Geopolitical Threats

- Unemployment rate: Unemployed⁄Labor force

corporate taxes, capital gains taxes)

To assess geopolitical risk, consider:

Indirect taxes: Tax on goods and services Type Result of The likelihood of occurrence Frictional Temporary transitions Fiscal Multiplier

The velocity (speed) of impact Structural Long-run changes in economy 1 The size and nature of impact = , where MPC = marginal Cyclical Changes in economic activity 1 − MPC(1 − t)

propensity to consume; t = tax rate

INTERNATIONAL TRADE AND CAPITAL FLOW S Inflation

Difficulties Executing Fiscal Policy

Basics of International Trade

Deflation: Negative inflation rate

Recognition lag: Government must see need

Terms of trade: Price of exports/Price of imports

Disinflation: Declining inflation rate

Action lag: Time needed to choose policy

Autarky: No trade with other countries

Hyperinflation: Extremely high inflation rate

Impact lag: Policies do not have immediate impact

Absolute advantage: Lower total cost of production

Cost-push: From decrease in aggregate supply

Comparative advantage: Lower opportunity cost

Demand-pull: From increase in aggregate demand

Laspeyres index: Use base consumption basket International Trade Models

Ricardian: Labor is the only factor of production,

Paasche index: Use current consumption basket

comparative advantage due to labor productivity

Fisher index: ILaspeyres × Paasche

Hecksher-Ohlin: Both labor and capital are factors, Economic Indicators

income redistribution is possible through trade

Leading: Stock indexes, building permits Trade Restrictions

Coincident: Real income, industrial production

Tariffs: Taxes on imported goods

Lagging: Unemployment rate, prime lending rate

Quotas: Limits on quantity of imported goods

Export subsidies: Payments to exporters

Minimum domestic content requirements

Voluntary export restraints: Self-imposed

limitations by foreign producers

Impact of Trade Restrictions Exchange Rate Regimes

Income Statement Line Items

Dollarization: Adopt another country’s currency Revenue

Monetary union: Adopt a common currency − Cost of goods sold (COGS)

Currency board: Commitment to exchange Gross Profit

domestic currency at fixed exchange rate

− Selling, General & Admin. (SG&A)

Fixed peg: Currency is pegged to foreign currency EBITDA

(or basket of currencies) within ±1% margin

Target zone: Fixed peg with wider margin

− Depreciation and Amortization

Crawling peg: Peg rate is periodically adjusted EBIT (Operating profit)

Crawling bands: Margin increases over time, − Interest

usually to transition from fixed peg to floating EBT (Earnings before taxes)

Managed floating: Monetary authority intervenes, − Taxes

but no official target exchange rate Net Income (NI)

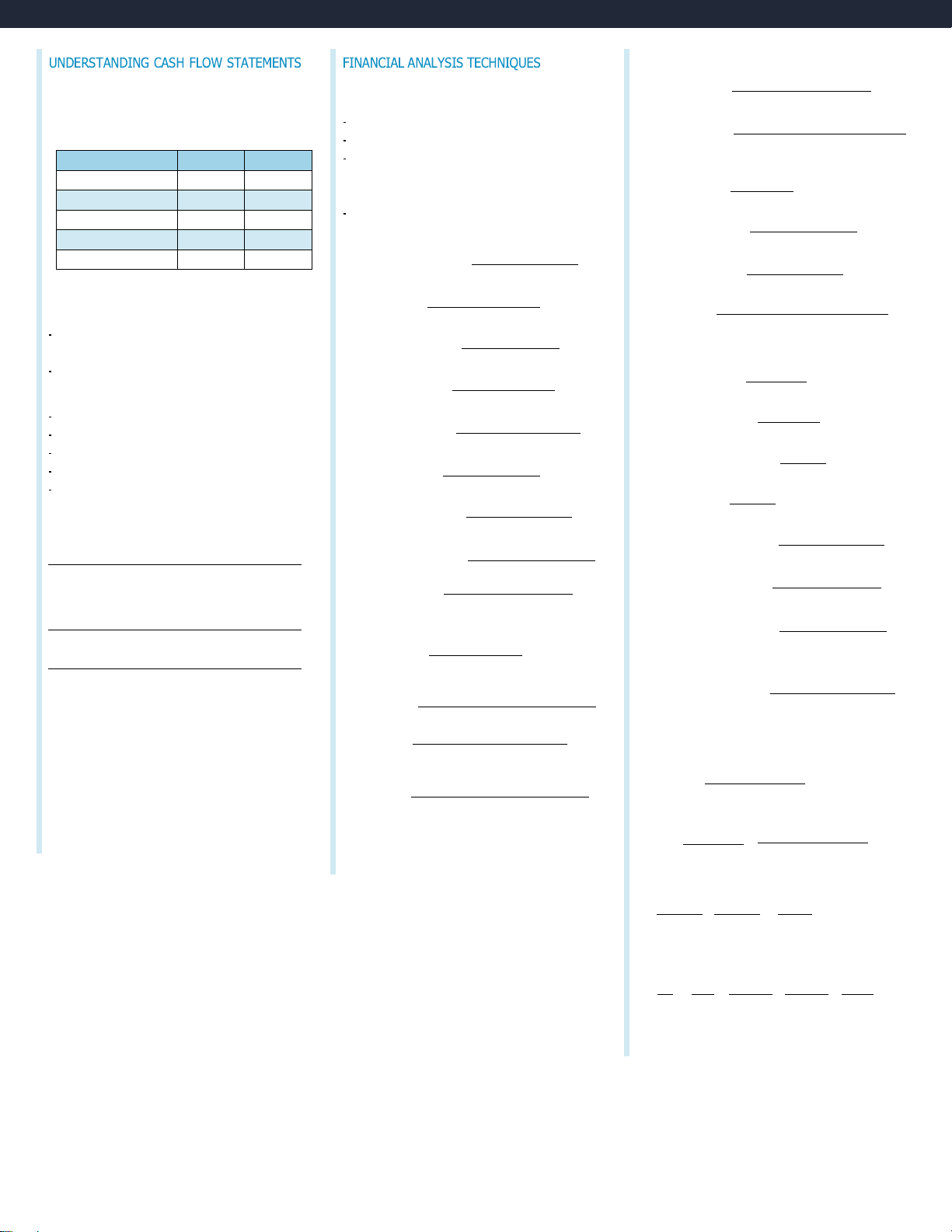

Price increases from P∗ to Pt

Independently floating: Market sets exchange rate

Separately Reported Items

Domestic production increases from Q1 to Q2

Marshall-Lerner Condition Discontinued operations

Domestic consumption falls from Q4 to Q3

Currency devaluation can improve a country’s

Unusual or infrequent items (US GAAP only)

Imports fall from (Q4 − Q1)to (Q3 − Q2)

trade balance if demand elasticities cause export Non-operating items

Loss of consumer surplus = (A + B + C + D)

receipts to increase more than import

National welfare loss = (B + D) expenditures

Basic Earnings per Share

Increase in producer surplus = A

Net income − Preferred dividends Tariff revenue/Quota rent = C

Weighted average of shares outstanding Regional Trading Blocs

FINANCIAL STATE MENT ANALY SIS

Diluted Earnings per Share

Free trade area (FTA): Free trade among members Convertible Convertible

Net − Preferred + preferred + debt (1 − 𝑡)

Customs union (CU): FTA + common trade policy FINANCIAL R EPORTING S TANDARDS income dividends dividends interest

Common market (CM): CU + free movement of FASB, IASB, and IOSCO

Weighted Shares from Shares from Shares issuable

factors of production within bloc

average + preferred + convertible + from stock

FASB: Sets forth US GAAP shares shares debt options

Economic union (EU): CM + common economic IASB: Establishes IFRS

institutions and coordination of economic policies

Must be equal to or less than basic EPS

IOSCO: International body of regulatory authorities

Monetary union (MU): EU + common currency

SEC: US capital markets regulator UNDERSTANDING B

ALANCE S HEETS

Balance of Payments Components

Fundamental Qualities of Financial Reports

Current account: Merchandise and services, income

1. Relevance 2. Faithful Representation

Classified Balance Sheet

receipts, unilateral transfers

Enhancing Characteristics

Current Assets: To be used within one year

Capital account: Capital transfers, non-financial

1. Comparability 2. Verifiability Cash and equivalents assets sales/purchases

Timeliness 4. Understandability Marketable securities

Financial account: Government-owned assets

Accounts receivable, net of bad debt expense

abroad, foreign-owned assets in the country UNDERSTANDING I

NCOME S TATEMENTS Inventories

Other (e.g., prepaid expenses) CURRENCY E XCHANGE R ATES Revenue Recognition Non-Current Assets

Revenue must not be recognized unless:

Exchange Rate Calculations

Property, Plant, and Equipment (PP&E)

Risks of ownership have been transferred CPIf Investment property

Real ex. rate = Nominal ex. rate × \ ]

Amount of revenue can be reliably measured Intangible assets Customer is likely to pay

Forward exchange rated⁄f 1 + id Goodwill =

Transaction is unlikely to be reversed Spot exchange rated⁄f 1 + if Financial assets

Service revenue may be recognized as earned

Cross rate: SA⁄B = SA⁄C × SC⁄B

Current Liabilities: To be settled within one year

Allowance for doubtful accounts: Contra-asset

Forward exchange rates in points: Accounts payable

account, estimated based on historical experience

- Unit of points is last decimal place in the rate Notes payable

quote (e.g., 1.5301 to 1.5302 is a 1-point increase) Expense Recognition Accrued expenses

Matching principle: Expenses must be recognized Ideal Currency Regime

Deferred income (Unearned revenue)

in the same period as associated revenue

Exchange rates are credibly fixed Long-term Liabilities

Fully convertible currencies, free capital flows Long-term debt

Countries pursue independent monetary policies Deferred tax liabilities

Such an ideal currency regime is NOT possible Equity Contributed capital Preferred shares Treasury shares Retained earnings

Accumulated other comprehensive income (OCI)

Non-controlling (minority) interest www.saltsolutions.com 7 UNDERSTANDING C

ASH F LOW S TATEMENTS

FINANCIAL ANALYSIS TECHNIQUES Solvency Ratios Total debt

Cash Flow Statement Classifications Common-Size Analysis Debt-to-equity =

CFO: Cash flows from regular operations Vertical: Total shareholders' equity

CFI: Cash flows for buying/selling long-term assets

State income statement items as % of revenue Total debt

CFF: Financial transactions with capital providers

State balance sheet items as a % of total assets

Debt-to-capital = Total debt + Total shareholders' Item US GAAP IFRS

State each cash flow statement item as a % of equity Dividends paid CFF CFO/CFF total cash inflows/outflows Total debt

Horizontal (Trend) Analysis: Interest paid CFO CFO/CFF Debt-to-assets = Total assets

State each item relative to its base-year value Dividends received CFO CFO/CFI Average total assets Financial leverage = Interest received CFO CFO/CFI Activity Ratios Average total equity Tax expenses CFO CFO* Annual sales

Receivables turnover = Average receivables EBIT

*I FRS treat tax expenses for investing or financing

Interest coverage = Interest payments transactions as CFI or CFF Fixed Days of sales = 365 EBIT + Lease payments CFO Direct Method outstanding Receivables turnover

charge = Interest payments + Lease pmts

Convert each accrual-based item in the income coverage Cost of goods sold Inventory turnover =

statement to cash inflow/outflow Average inventory Profitability Ratios

CFO is net of cash inflows and outflows Net income Days of inventory 365 Net profit margin = = Revenue CFO Indirect Method on hand Inventory turnover Gross profit Start with net income Gross profit margin = Purchases

Add noncash expenses (e.g., Depreciation) Payables turnover = Revenue Average trade payables Subtract gains/add losses EBIT Operating profit margin =

Add increases in current liabilities Number of days 365 = Revenue of payables Payables turnover

Subtract increases in (non-cash) current assets EBT Revenue Pretax margin = Beginning accounts receivable Total asset turnover = Revenue Average total assets + Revenue Net income Return on assets (ROA) = Revenue

− Ending accounts receivable Average total assets Fixed asset turnover = Average net fixed assets

Cash collected from customers EBIT Working capital = Revenue Return on total capital = Cost of goods sold turnover Average working capital Average total capital + Increase in inventory Net income Liquidity Ratios Return on equity (ROE) = Purchases from suppliers Average total equity Current assets Current ratio =

− Increase in accounts payable Current liabilities Valuation Ratios Cash paid to suppliers Dividends declared

Cash + Marketable + Receivables Dividend payout ratio = Free Cash Flow (FCF) Quick ratio = securities NI available to common Current liabilities

Free cash flow to the firm (FCFF): Cash available to

Retention rate (RR) = 1 − Dividend payout ratio Cash + Marketable securities

equity owners and debt holders. ( ) Cash ratio = Current liabilities

Sustainable growth rate g = RR × ROE

FCFF = NI + NCC + I × (1 − t) − FCI − WCI

= CFO + I × (1 − t) − FCI Price per share

Cash + Marketable + Receivables P/E Ratio = Defensive securities = Earnings per share

Free cash flow to equity (FCFE): Cash flow available interval Average daily expenditures to common shareholders DuPont Analysis Cash Days of Days of Number ] \ Assets

FCFE = CFO − FCI + Net Borrowing ROE = \ Net income Assets conversion = sales + inventory − of days ] Book Value of Equity cycle outstanding on hand payables = (ROA) >Leverage) ratio NI Revenue Assets ] \ ] \ ] = \ Revenue Assets Equity

= \Net profit] > Asset ) >Leverage) margin turnover ratio NI EBT EBIT Revenue Assets = / 5 / 5 / 5 / 5 / 5 EBT EBIT Revenue Assets Equity = ( Tax ) (I nterest ) ( EBIT ) ( burden margin ) ( Asset Financial leverage ) burden turnover IN I VE NV N E TO NT R O IE R S I ES Depreciation Methods INCOME TAX TA ES XE S

Inventory Valuation Requirements

Straight-line: = Cost–Salvage value

Temporary Taxable Differences Depreciable life

IFRS: Lower of cost or net realizable value

Deferred tax assets (DTA): Created when taxes

US GAAP: Lower of cost or market value

Double-declining balance (DDB):

payable exceeds income tax expense

Reversals of inventory write-downs are allowed Book valuet Depreciation = \ ] × 2

Deferred tax liabilities (DTL): Created when taxes t

under IFRS, but not under US GAAP Depreciable life

payable is less than income tax expense Units-of-production:

Tax base of assets: Amount that will be deducted on

Inventory Valuation Methods and Systems Cost − Salvage Depreciation = × Output units

the tax return as asset’s benefits are realized US GAAP IFRS t Total output t

Tax base of liabilities: Carrying value of liability FIFO Allowed Allowed Intangible Assets

minus amount that will be deductible LIFO Allowed N/A

Purchased: Record at fair value (purchase price) Weighted Allowed Allowed

Asset carrying amount > Tax base DTL Developed internally: average

Asset carrying amount < Tax base DTA IFRS Specific Allowed Allowed

Liability carrying amount > Tax base DTA

- Research expenditures are expensed Identification

Liability carrying amount < Tax base DTL

- Development expenditures are capitalized

Impact of Inventory Valuation Method US GAAP

Impact of tax rate changes If prices are rising FIFO LIFO

- Generally, both R&D costs are expensed

If tax rate increases, DTA and DTL will increase Ending Inventory Higher Lower

Acquired in business combination:

If tax rate decreases, DTA and DTL will decrease COGS Lower Higher

Purchase price is allocated to each asset on fair

Income tax exp. = Taxes payable + ΔDTL − ΔDTA Net income Higher Lower

value basis; excess recorded as goodwill Valuation Allowance Income Tax Expense Higher Lower

Capitalizing vs. Expensing

Contra account used if it is unlikely that future Operating cash flow Lower Higher

- Capitalizing increases assets on the balance sheet

profits will be sufficient to use DTAs and credits and investing cash outflows

Deferred Tax Charges Directly to Equity

Perpetual vs. periodic inventory system:

- Expensing reduces net income by the after-tax

Periodic system matches total units sold for the

Revaluation of PP&E (IFRS only)

expenditure amount in the period it is incurred

Impact of changes in accounting policies

period with total purchases for the same period

Perpetual system updates after each transaction

Impairment of PP&E and Intangible Assets

Impact of exchange rate fluctuations

Under FIFO, ending inventory and COGS are the US GAAP

Changes in fair value of certain investments

same for periodic or perpetual

- Asset tested for impairment only when firm may

Weighted average and LIFO will show differences

NON-CURRENT (LONG-TERM) LIABILITIES

not recover carrying value through future use

- Asset is impaired when carrying value exceeds Long-Term Liabilities LIFO Reserve

asset’s future undiscounted cash flows

Premium bond: Coupon rate > yield at issuance

Used to adjust LIFO COGS and ending inventory

- Impaired asset’s value is written down to fair

Discount bond: Coupon rate < yield at issuance

(EI) to FIFO-equivalent values

value and a loss is recognized and cannot be Issuance costs: subsequently reversed

US GAAP – capitalized as an asset IFRS

IFRS – reduces initial bond liability

- Assets are tested annually for impairment

Derecognition of debt: If an issuer redeems a bond LIFO Liquidations

- Impaired if carrying value > recoverable amount

before maturity, a gain/loss (book value minus

Happen when units sold exceed units purchased

- Impaired asset’s value is written down to

redemption price) is recognized

May result in higher gross profit than otherwise

recoverable amount and a loss is recognized

Debt covenants: Affirmative – borrower promises

- Loss can be reversed if asset value recovers, but

to do certain things; negative – borrower promises LONG-LIVED A SSETS

only up to pre-impairment carrying value

to refrain from certain things Long-Term Assets Lessee Accounting

Property, plant, and equipment (PP&E): US GAAP IFRS Finance lease:

Both cost model and revaluation model allowed

Lessee purchases the asset, financed by the lessor

Recoverable amount is greater of:

Lessee's periodic lease payments have separate

fair value less selling costs, and

value in use (PV of asset’s future cash flows)

depreciation and interest components - Loss recoveries are allowed

Operating lease (like a rental agreement):

Single lease expense, not separated into different US GAAP

components for depreciation and interest Only cost model is allowed

The value of an operating lease payment is Loss recoveries not allowed

calculated as a straight-line allocation of total

payments over the term of the lease www.saltsolutions.com 9

Conditions requiring a lease to be a finance lease: Limited Partnership

Principal-Agent and Other Relationships

- Ownership of the leased asset is transferred to Set by partnership agreement

Shareholder vs. manager/director the lessee Operated by GP

- Entrenchment: Managers avoid justifiable risks to

- Lessee has the option to purchase the asset and

Business liability is limited by LPs and unlimited avoid losing their positions will likely do so for GP

- Empire building: Making unjustified acquisitions

- Lease term covers most of asset's useful life

Business profits are shared by partners and taxed

to increase company size and compensation

- The present value of lease payments at inception as personal income

- Excessive risk taking: Taking unjustifiable risks to

is close to the asset’s fair value

Partners are the main source of income

maximize returns on stock-based compensation

- The leased asset is so specialized that only the

Partners’ resources, risk appetite, and GP’s

- Agency costs reduce the potential for exploitation

lessee can use it without modification

competence/integrity limit business growth in an agency relationship

IFRS require all leases to be treated in the manner

Corporations (Limited Companies)

Controlling shareholder vs. minority shareholder

that is prescribed by US GAAP for finance leases.

Legal identity is separated from owners

- Dispersed ownership: Controlled by many

Operated by management team voted by Lessor Accounting minority shareholders shareholders -

- Concentrated ownership: Controlled by a single

For operating leases (under both IFRS and US

Limited business liability for shareholders shareholder

GAAP), the lessor retains the leased asset on its Financed by equity and debt

- Multiple-class share structures: Disproportionate

balance sheet and incurs the associated

Profits are taxed directly; double taxation occurs

voting power to certain shareholder classes

depreciation expense. Lease income from the

when shareholders are taxed on their dividend

lessor is recorded as revenue. Shareholder vs. creditor income

- For finance leases (under both IFRS and US

- Equity owners prefer growth and have a higher

GAAP), the lessor removes the leased asset from

Public and Private Corporations risk tolerance

its balance sheet and creates an asset with a

Market capitalization: Product of the current share

- Creditors prefer stability and limited downside

value equal to the lease receivable and any

price and the number of outstanding shares risk residual value.

Enterprise value = MVShares + MVDebt – Cash

Corporate governance can be described as:

- Lease payments are recognized as an operating

Private placement memorandum (PPM) is used by

- A system of internal controls and procedures for

inflow on the lessor’s cash flow statement (for

private companies to raise capital in primary

managing organizational business

both operating leases and finance leases) market

- A framework for defining the rights and

Private companies can go public by: Pensions

responsibilities of individuals and groups within Initial public offering (IPO)

Defined benefit (DB): Firm makes periodic the organization Direct listing (DL)

payments to employee after retirement.

- An arrangement of checks, balances, and Acquisition

Overfunded (underfunded) plan is recognized as

incentives to minimize and manage conflicts an asset (liability).

Public companies can go private by:

between the interests of insiders and external Leveraged buyout (LBO) stakeholders Management buyout (MBO) Stakeholder Mechanisms CORPORATE ISSUERS Lenders and Owners Shareholder:

Risk vs return characteristics of equity and debt: - CORPORATE S

TRUCTURES A ND O WNERSHIP

Corporate reporting and transparency Equity Debt

- Shareholder meetings (cumulative voting, proxy Sole Proprietorship Upside Limited to voting) Extension of owner Unlimited potential payments - Shareholder activism Operated by owner Maximum Cannot be more than the - Derivative lawsuits

Business liability is retained by owner loss investment value

- Corporate takeovers (proxy contests, tender

Business profits are owned by owner and taxed offers, hostile takeovers) as personal income Investment Higher Lower

Owner is the main source of capital risk Creditor:

Owner’s capital and risk appetite limit business Investment Maximize Timely

- Bond indentures, collateral, and trustees growth interest company repayment - Corporate reporting value - Creditor committees General Partnership Set by partnership agreement

INTRODUCTION TO CORPORATE GOVERNANCE

Board of director and management: Operated by partner A AND ND O T O HE TH R E E R SEG C SG O N C S O IDE

NSI RDAETRIO A NS TI ONS - Audit committee

Business liability is retained and shared by - Governance committee Stakeholder Groups partners

- Remuneration/Compensation committee

Business profits are shared by partners and taxed - Nomination committee as personal income - Risk committee

Partners are the main source of capital - Investment committee

Partners’ resources and risk appetite limit business growth Employee: BUSINESS MO DELS & R ISKS

Business Models: Financial Implications - Labor laws Value Proposition External factors:

- Code of ethics and compliance department Target customers Economic conditions - Whistleblower protections Product/service offering Demographics - Employee contracts Channel strategy Sector demand Pricing strategy Customer and supplier: Industry cost characteristics - Commercial contracts Channel strategy: Social and political trends

- Public reputation and social media Traditional channel Firm-specific factors: Direct sales Government: Firm maturity Drop shipping - Laws and regulations Competitive position Omnichannel strategy - Corporate governance codes Business model

- Common law and civil law systems Pricing model: Business Models: Risks Cost-based Macro risk:

Risks and Benefits of Corporate Governance Value-based Exchange rates

and Stakeholder Management Interest rates

Operational risks of poor stakeholder governance: Price discrimination: Political instability

- Weak control systems that do not treat all Tiered pricing Legal and regulatory changes stakeholders fairly Dynamic pricing Country-level risks

- Ineffective decision-making process

Auction/reverse auction models - Inadequate board scrutiny Business risk:

Pricing for multiple products:

- Diminished operating performance Industry risks Bundling Company-specific risks

Financial risks of poor stakeholder governance: Razors-and-blades pricing

- Higher default and bankruptcy risks Optional product pricing Financial risk: - Higher borrowing costs

Total leverage = Operating leverage Pricing for rapid growth: - Poor equity returns × Financial leverage Penetration pricing Contribution margin EBIT

Factors Relevant to Corporate Governance and Freemium pricing = × EBIT EBT

Stakeholder Management Analysis Hidden revenue business model Contribution margin

- Economic ownership and voting control = EBT Alternatives to ownership:

- Board of directors representation Subscription pricing

- Remuneration and company performance CAPITAL INVE NV S E TM ST E M N E TS NT S Fractionalization - Investors in the company

Types of Capital Investments Leasing

- Strength of shareholders’ rights Business maintenance: Licensing

- Management of long-term risks Going concern projects Franchising

Regulatory/compliance projects

ESG Considerations for Investors and Analysts Value Chain ESG investment approaches: Business growth:

Value chain: Systems and functions within the firm - Responsible investing Expansion projects

that create value for its customers - Sustainable investing

Pet projects/high-risk investments

Supply chain: Series of steps and processes needed

- Socially responsible investing (SRI)

to prepare a product to be sold to the consumer

Principles of Capital Budgeting

- Value-based and values-based approaches

Key assumptions of capital allocation:

Profitability and Unit Economics ESG investment styles:

Decisions are based on cash flows instead of

Unit economics: The quantitative analysis of a - Negative screening accounting concepts

company's revenues and costs on a per unit basis - Positive screening

Cash flows are not equivalent to accounting Fixed costs - ESG integration Breakeven point = income or economic income Contribution margin - Thematic investing

Cash flows must account for opportunity costs Fixed costs - Engagement/active ownership =

Analysis is done on an after-tax basis

Unit price − Variable cost per unit - Impact investing

Timing of cash flows is important Business Model Types Financing costs are ignored

Green finance: Use financial instruments to Private label manufacturers

support economic growth while minimizing

Other important considerations: Licensing arrangements environmental impact Sunk costs are ignored Value added resellers

Opportunity cost is the value of a resource’s next- Franchises best use Network effects

Incremental cash flows reflect the cash flows Crowdsourcing realized from a decision Hybrid business models

Externalities (e.g., cannibalization) may have E-commerce business models:

unexpected negative impact the company Affiliate marketing

Conventional cash flow pattern only has Marketplace businesses one sign change Aggregators www.saltsolutions.com 11

Net Present Value (NPV)

External Financing: Capital Markets

COST OF CAPITAL – FOUNDATIONAL TOPIC

Sum of present values of expected future cash - Short-term commercial paper

Weighted Average Cost of Capital (WACC)

inflows, net of initial cash outlay - Long-term debt

WACC = wdrd(1 − t) + wprp + were - Common equity w

d = percentage of debt in capital structure (1 + r)t

wp = percentage of preferred stock

Conservative Working Capital Management

Accept a project if NPV > 0 Advantages:

we = percentage of common stock - Low rollover risk t = tax rate

Internal Rate of Return (IRR) - Greater cash flow certainty rd = cost of debt IRR is r such that NPV = 0

- Low risk of inventory shortages

rp = cost of preferred stock = Dp⁄P

Accept a project if its IRR > required return

- Flexibility to adapt to adverse market conditions re = cost of common stock

BA II Plus NPV Worksheet Function Disadvantages:

Cash inflows are positive; outflows are negative (CAPM) - High borrowing costs

F01, F02, etc. refer to cash flow frequencies = rd + Risk Premium

- High cost of equity and shareholder dilution

CPT + NPV to compute NPV; CPT + IRR for IRR

(Bond Yield plus Risk Premium)

- Less flexibility to borrow on an as-needed basis

Common Capital Budgeting Pitfalls - Longer lead times

Costs of the Various Sources of Capital Inertia - More covenants Cost of debt: Source of capital bias

- High risk of obsolete inventory - Yield-to-maturity approach

Failing to consider alternatives

Aggressive Working Capital Management P = â∑ + Pet projects Advantages:

Basing decisions on earnings metrics

Debt rating approach (e.g., matrix pricing)

- Low financing costs under an upward-sloping Internal forecasting errors yield curve Cost of preferred stock:

Corporate Usage of Capital Allocation Methods

- Great flexibility to borrow only as needed

Return on invested capital (ROIC):

- Short-term borrowing involves less rigorous After-Tax Net Profit Cost of common stock: credit analysis

ROIC = Average BV of Invested Capital Yield-to-maturity approach Disadvantages: Real Options

- Risk of having to refinance at higher Multifactor model

Timing option: Option to delay the investment short-term rates

Sizing option: Option to expand, grow, or abandon

- Potential difficulty rolling over short-term debt + ⋯ + βjmFactorjn

Flexibility option: Option to alter operations, with market turmoil

Bond yield plus risk premium approach

such as changing prices or substituting inputs

- Possible need to rely on expensive trade credit re = rd + Risk Premium

Fundamental option: Option to alter decisions - Tight customer credit terms

based on future events (e.g., drill based on price Estimating Beta

Liquidity and Short-Term Funding Needs

of oil, continue R&D depending on initial results)

Blume’s beta adjustment formula:

Primary sources of liquidity: 2 1

Analyzing Projects with Real Options

Adjusted β = \ ] (Unadjusted β) + \ ] (1.0) - Free cash flows 3 3

Use the discounted cash flow (DCF) analysis

- Ready cash balances (bank accounts)

Asset beta/unlevered beta for comparable

without considering real options

- Short-term funds (lines of credit) company:

Adjust the stand-alone DCF analysis by including

- Cash flow management (centralized collection)

the present value of the expected costs and

Secondary sources of liquidity: 1 β = β û benefits options - Negotiating debt contracts (1 − t) D + 1 E Use option pricing models - Liquidating assets

Levered project beta for subject firm: Use decision trees - Filing for bankruptcy

Drag on liquidity: Delayed cash inflows, such as = β †(1 − t) + 1°

WORKING CAPITAL & LIQUIDITY

uncollected receivables and obsolete inventory Internal Financing Flotation Costs

Pull on liquidity: Accelerated cash outflows, such as

Increasing after-tax operating cash flows r settling payables earlier

e adjusted for flotation costs (amount):

Improving working capital efficiency D

Net operating cycle (a.k.a. cash conversion cycle) = r = + g

Converting liquid assets to cash P0 − F

# days of inventory + # days of receivable – # days

re adjusted for flotation costs (percentage): of payable

External Financing: Financial Intermediaries D r = + g Uncommitted lines of credit

Evaluating Short-Term Financing Choices P0[1 − f] Committed lines of credit

Factors influencing a company’s short-term Revolving credit agreements borrowing strategy: Secured (asset-based) loans - Size and creditworthiness Factoring

- Legal and regulatory considerations Others (web-based lenders and - Sufficient access non-bank lenders)

- Flexibility of borrowing options CAPITAL S TRU STR C U T C U T R U E R E Breakeven

Internal Factors Affecting Capital Structure F + C

Breakeven: QBE = P − V

Business model characteristics: F

Revenue, earnings, and cash flow sensitivity

Operating breakeven: Q OBE = P − V Asset type

Q = quantity; P = price; V = variable cost/unit Asset ownership

F = fixed operating cost; C = fixed financial cost Existing leverage: Liquidity Profitability EQUITY Interest coverage Leverage

To estimate a company’s target capital structure:

MARKET ORGANIZATION AND STRUCTURE

Corporate tax rate: The higher the tax rate, the

Assume the company will main its current capital

Functions of the Financial System more benefit of using debt structure Saving

Capital structure policies/guidelines: Firm-specific

Infer target weights the company is moving Borrowing policies and debt covenants toward Raising Equity Capital Company life stage: Use the industrial average

Pecking order theory: Since managers have an Managing Risks

asymmetric information advantage, they prefer Exchanging Assets

capital sources that reveal the least amount of Information-Motivated Trading information: Securities Markets

Internally generated earnings (best option)

Spot vs. Forward Markets: Spot market trades are New debt settled within 3 days.

New equity (least attractive for managers)

Primary vs. Secondary Markets: Primary market Stakeholder Interests

transactions are done directly with the issuer,

Agency costs arise from conflicts between

while secondary market trades take place on

managers and owners. The interests of managers, organized exchanges.

External Factors Affecting Capital Structure

shareholders, and bondholders are not always

Capital vs. Money Markets: Money markets are

Market conditions/business cycles aligned.

used for securities with maturities of less than Regulatory constraints

one year, while longer-dated securities are traded Industry/peer firm leverage MEASURES OF L EVERAGE in capital markets.

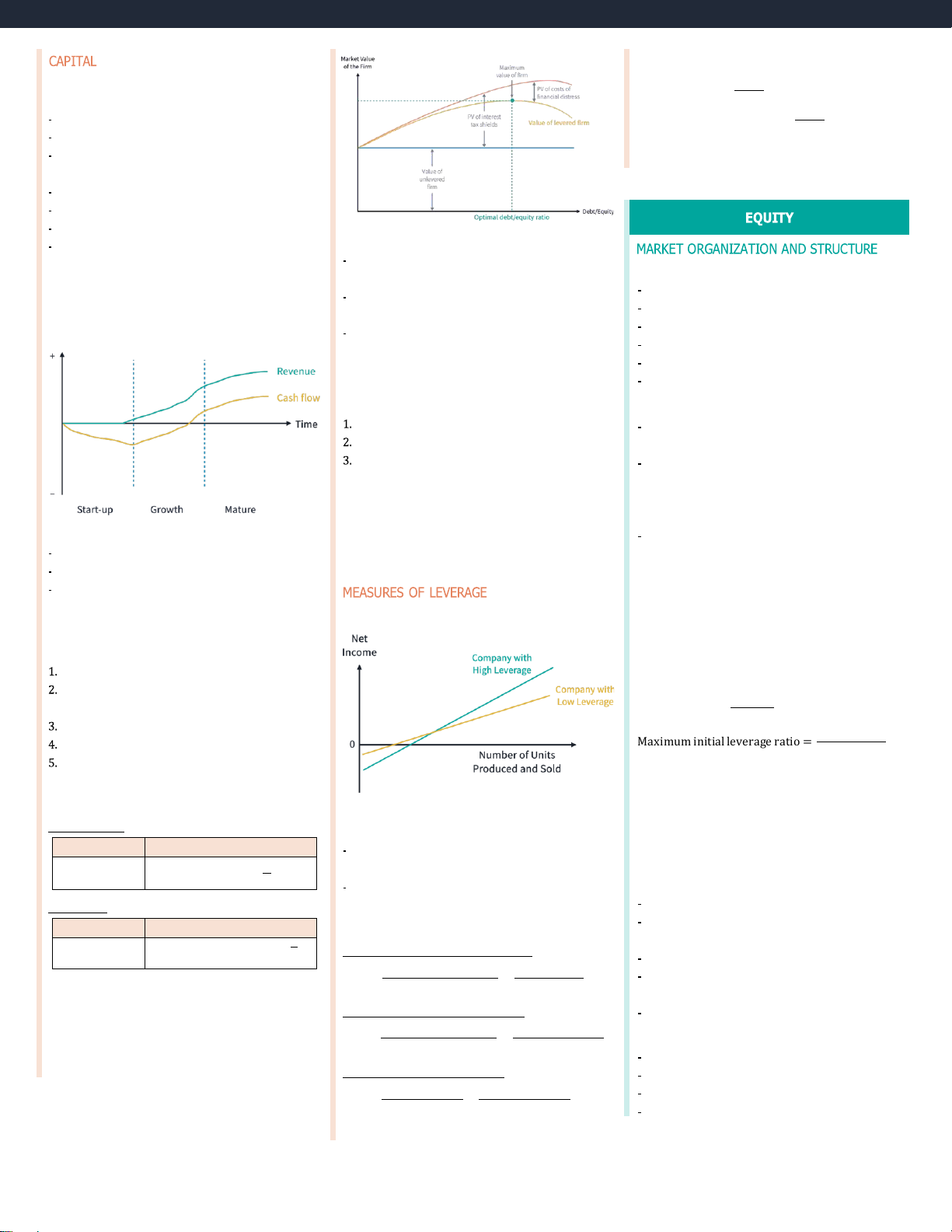

Modigliani and Miller Propositions Leverage Positions

MM Proposition I: A firm's capital structure would

Long positions: Benefit from price appreciation

have no effect on its value, assuming:

Short positions: Benefit from price depreciation

Investors have homogeneous expectations Leveraged Positions

No market frictions (e.g., transaction costs, taxes, Position

or costs of financial distress) Leverage ratio = Equity No agency costs 1

Investors can borrow and lend at risk-free rate

Maximum initial leverage ratio = Intial margin

Investing/financing decisions are independent

Maintenance margin: minimum amount of equity

MM Proposition II: Cost of equity increases with the required debt-to-equity ratio.

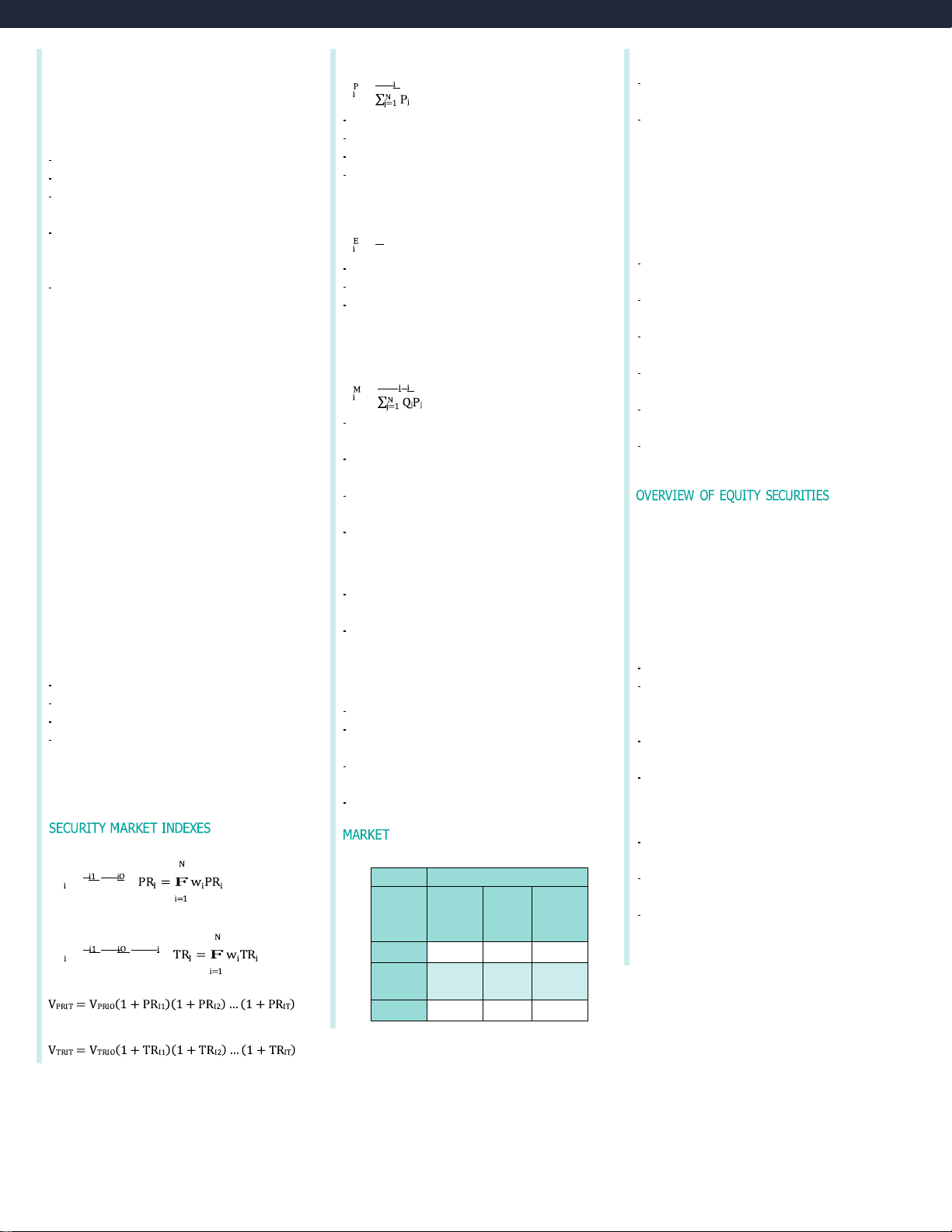

Margin call is triggered if the equity falls below the Business Risk Without Taxes

maintenance margin. Additional equity will be

Two components of business risk are:

requested to bring the account balance back to the Firm value VL = VU

Sales risk: determined by the elasticity of demand D initial margin. ] for products and services Cost of Equity r = r + (r − r ) e 0 0 d \E

Operating risk: determined by the share of fixed

Execution Instructions (How to fill) With Taxes

costs as a share of total operating costs

Market: Fill immediately at market price

Limit: Buy below maximum price or sell above Firm value VL = VU + tD Measures of Leverage D

minimum price specified in order Cost of Equity

Degree of operating leverage (DOL):

re = r0 + (r0 − rd)(1 − t) / 5 E

All-or-nothing: Cancel order if not fully filled %Δ Operating income Q(P − V) DOL = =

Hidden: Visible to brokers and exchanges, but

r0 = cost of capital for a firm financed only by equity %Δ Units sold Q(P − V) − F invisible to other traders

Optimal and Target Capital Structure

Degree of financial leverage (DFL):

Iceberg: Only a fraction of order amount is visible

Static trade-off theory balances costs of financial %Δ Net income Q(P − V) − F DFL = =

Validity Instructions (When to fill)

distress with tax shield benefits from using debt: %Δ Operating income Q(P − V) − F − C

Day orders: Cancelled if unfilled at end of day

VL = VU + tD − PV(costs of financial distress)

Degree of total leverage (DTL):

Good-till-cancelled: No set expiry date %Δ Net income Q(P − V) DTL = =

Good-on-close: Filled at end of day %Δ Units sold Q(P − V) − F − C

Stop-loss: Sell if prices fall below specified level DTL = DOL × DFL www.saltsolutions.com 13 Clearing Instructions Price-Weighted Indexes Implications of EMH

Settlement/clearing typically done by brokers for P

If weak form holds, investors will not earn w =

retail trades; brokers or custodians for

abnormal profits from technical analysis institutional trades

Like buying one share of each stock

If markets are semi-strong efficient, investors Advantage is simplicity

must have a comparative advantage to earn

Primary Market Transactions

Disadvantage is arbitrary weights

abnormal profits from fundamental analysis

Initial Public Offerings (IPOs)

A stock’s weight is halved due to a stock split, Private placements Market Anomalies

requiring an adjustment to the divisor

Shelf registrations: Part of issue is held back to be

Changes in a security’s price that are not

sold directly to secondary market investors later

Equally Weighted Indexes

attributable to known information

Dividend reinvestment plans (DRIPs): Investors 1 w =

can roll over dividend payments to purchase new

Selected Behavioral Biases N

shares, possibly at a discount

Like investing the same amount in each stock

Loss aversion: Disliking losses more than liking

Rights offerings: Current shareholders gain right Advantage is simplicity equivalent gains

to purchase additional shares at below-market

Disadvantages are that the impact of large

Information Cascades: Those who act first will

price; dilutes value of existing shares

companies is underrepresented and frequent

convey information that influences others rebalancing is required

Representativeness: Rely too much on current Market Structure

state when assessing probabilities

Quote-driven: Investors trade with dealers

Capitalization-Weighted Indexes

Mental accounting: Keep track of gains and losses

Order-driven: Exchanges use order matching rules Q P w =

separately for different investments/goals

Brokered: Trades arranged by brokers

Conservatism: Failing to incorporate new

Call markets: Conduct periodic single price

Like holding all stocks in proportion to their

information in a timely manner

auctions, otherwise completely illiquid market values

Narrow framing: Focusing on certain issues in

Continuous Trading markets: Allow trades

Float adjustment may be used to reflect the isolation

whenever market is open, may use call market

number of shares that may be actively traded

auction at beginning and/or end of each day

Advantage is that the asset classes’ performance

OVERVIEW OF EQUITY SECURITIES is well-represented

Common Share Voting Methods Trade Pricing Rules

Disadvantage is that returns are heavily driven by

Uniform pricing rules: Used by call markets, all

Statutory: One vote per share

large-cap (possibly overvalued) firms

trades executed at the price that maximizes total

Cumulative: Votes can be bundled quantity traded

Fundamentally Weighted Indexes Example: 10 board positions

Discriminatory pricing rules: Used by continuous

Built like price-weighted indexes, but using a

Statutory: 1 share votes for 10 different candidates

markets, fills most aggressively priced orders first

fundamental measure such as sales or cash flows

Cumulative: 10 votes may go to 1 candidate

Derivative pricing rules: Used by crossing networks

Contrarian effect of rebalancing by selling off top

Cumulative method advantages small shareholder

to trade at midpoint of quotes from other markets

performers and buying underperforming stocks Preference Shares produces a value tilt Complete Markets

Cumulative: Accrue dividends if payments missed Facilitate savings/investment

Types of Equity Market Indexes

Non-cumulative: Missed dividends do not accrue,

Facilitate lending to creditworthy borrowers

Broad market indexes: Covers one equity market

but no common dividends allowed if preferred

Allow risk exposures to be hedged

Multi-market indexes: Covers equity markets in

shareholders do not receive their dividend

Facilitate exchange of currencies/commodities multiple countries

Participating: May receive additional dividend if

An ideal financial system is complete (see above),

Sector indexes: Important for assessing a

firm is profitable or in the event of liquidation

operationally efficient (low transaction costs), and

manager’s performance (selection vs. allocation)

Non-participating: No compensation beyond

informationally efficient (prices reflect all info.)

Style indexes: Large/small cap; Value/growth

dividends and face value in a liquidation

Private Equity Securities SECURITY MAR KET I NDEXES MARKET E EFFFI F C I I CEIN E C NYC Y

Venture capital (VC): Start-up, early-state, or

Price Return over Single Period

Forms of Efficient Market Hypothesis (EMH)

mezzanine financing with IPO as exit strategy P − P Market Prices Reflect: PR

Leveraged buyouts (LBO): Debt-financed deals to = P iO Past

take undervalued listed companies private Public Private Form market

Private investment in public equity (PIPE):

Total Return over Single Period info info data

Companies can raise new capital quickly, P − P + Inc Weak TR

investors can negotiate discounts = ✔ P iO Semi- ✔ ✔

Price Return Index over Multiple Periods strong Strong ✔ ✔ ✔

Total Return Index over Multiple Periods

Depository Receipts (DRs) Multistage DDM: Credit Enhancements n D P

Sponsored DRs: Issued directly by foreign

Internal: Subordination, over-collateralization, V0 = F t + n

company; Investors receive same voting rights and (1 + r)t (1 + r)n reserve accounts t=1

dividends as other common shareholders D

External: Surety bonds, letters of credit, guarantees P = n+1 n r − g from financial institutions L

Unsponsored DRs: Foreign company not involved; Dn+1 = D0(1 + gS)n(1 + gL)

Depository bank purchases shares, issues DRs, and

Bonds with Contingency Provisions retains voting rights Price Multiples Callable Bonds P

May be recalled by issuer if rates fal 0 D

Global DRs: Issued outside company’s home = 1/E1 E1 r − g

country to avoid limits on capital flows; May be

P⁄B = Price per share⁄Book value per share

denominated in any currency, but USD is common; Putable Bonds

P⁄CF = Price per share⁄Cash flow per share

Cannot be listed on US exchanges, but US investors

May be sold back to issuer if rates rise

P⁄S = Price per share⁄Sales per share

can purchase them via private placements

Asset-Based Valuation Models

American DRs: USD-denominated GDRs that can be

Useful for companies with natural resource or a Convertible Bonds

traded on US exchanges; Underlying securities,

large share of current assets/liabilities; Not useful

Conversion price: Price per share at which bond

American depository shares, trade in issuer’s

if company has a large share of PP&E/intangibles can be converted into shares domestic market Enterprise Value (EV)

Conversion ratio: Number of common shares

= MV(Common equity) + MV(Preferred stock)

each bond can be converted into

Global Registered Shares: Traded on multiple

+ MV(Debt) − (Cash + Short term investments) Conversion value:

exchanges, including issuer’s domestic market;

Current share price × Conversion ratio

Denominated in multiple local currencies; Unlike Conversion premium:

DRs, GRS represent an actual ownership interest FIXED INCOME

Convertible bond’s price − Conversion value

Warrants: Options to buy equity, lowers debt costs

INTRODUCTION TO INDUSTRY & COMPANY

FIXED-INCOME SECURITIES: DEFINING AN C A O L MYPSI A S NY ANALYSIS

Convertible Contingent Bonds (CoCos) EL D E E M FI EN NI TS NG ELEMENTS

Porter’s Five Forces Framework

Automatically convert to equity if a condition is Types of Bonds Threat of substitute products

met (e.g., capitalization ratio falls)

Collateral Trust Bonds: Backed by financial assets Bargaining power of customers

Lender does not control if option is exercised

Equipment Trust Bonds: Backed by physical assets Bargaining power of suppliers

Primarily issued by financial institutions

Covered Bonds: Backed by a segregated pool of Threat of new entrants

loans that are replaced if they stop performing Intensity of rivalry

FIXED-INCOME MARKETS: ISSUANCE, TRADING, AN TRD A F D U I NDI NG, N AG

Principal Repayment Structures ND FUNDING

Industry Life Cycle Stages

Bullet Bonds: Full principal repaid at maturity Bond Markets

Embryonic: Slow growth, high prices, high failure

Fully Amortizing: Equal annuity-like payments

Primary bond markets: Markets in which issuers

risk, significant investment required

contain a mix of interest and principal

initially sell bonds to investors to raise capital

Growth: Rapidly increasing demand, improving

Partially Amortizing: Some principal is amortized,

Secondary bond markets: Markets in which bonds

profitability, falling prices, low competition

remainder repaid as a lump sum at maturity

are subsequently traded among investors; Most

Shakeout: Slowing growth, intense competition,

Sinking Funds: Certain percentage of principal

trading is OTC rather than on organized declining profitability retired each year exchanges

Mature: Little or no growth, industry

Grey market: Informal forward market to gauge

consolidation, high entry barriers Coupon Structures

interest in upcoming bond issues and set prices

Decline: Negative growth, excess capacity,

Fixed-rate bonds: Set percentage of principal for the primary market high competition

Floating-rate (FRNs): Reference rate + spread

Step-up: Coupon rate increases on schedule Sovereign Debt

Key Competitive Strategies

Credit-Linked: Coupon rate is increased if issuer is

Issued by national governments, zero default risk

Low-cost leadership: To hold/gain market share

downgraded, reduced if upgraded

Bills mature < 1 year; Bonds mature > 1 year

Product differentiation: To charge premium prices

Payment-in-kind: Coupons may be paid with more

On-the-run: Most recent issues of a given bonds rather than cash

maturity; more liquid than off-the-run issues

EQUITY VALUATION: CONCEPTS AND BASIC

Deferred (Split) Coupon: No coupons in early TO B O A L SIS C TOOLS Non-Sovereign Debt

years, high coupons in later years

Dividend Discount Model (DDM)

Municipal bonds (sub-national issuers)

Inflation-Indexed Bonds

Quasi-government bonds (gov’t-backed agencies) D D P ( +

Zero-coupon: Principal amount is adjusted

Supranational bonds (i.e., IMF, World Bank) 1 + r)t (1 + r)t (1 + r)n

Interest-indexed: Coupons are adjusted

Perpetual preferred stock; constant dividend: Corporate Debt

Capital-indexed: Fixed rate, adjusted principal D

Commercial paper (CP) used for < 1 year, but V =

Indexed-annuity: Amortizing bonds with annuity r carries rollover risk

payments adjusted for inflation

Gordon constant growth model (GGM): Long-term bonds ~12+ years

Bilateral/syndicated bank loans are also used D (1 + g)t D 0(1 + g) D1 ( = 1 + r)t r − g r − g

g = (Retention rate) × ROE = (1 − D⁄E) × ROE www.saltsolutions.com 15

Medium-Term Notes (MTNs) Yield Measures Securitization Example

- Used to bridge gap between CP and L/T bonds Annual cash coupon payment Current yield =

- Firm sells equipment on credit

- Offered to investors through an agent in a range Flat price

- Firm creates bankruptcy-remote SPV of maturities Annual cash + Amortized

- SPV issues debt to purchase loans from firm - coupon payment gain/loss

Lower registration/underwriting costs than Simple yield = - Flat price

SPV creates securities backed by loans

bonds, but relatively illiquid

Yield-to-call (YTC) = IRR assuming bond is called

- Investors purchase securities from SPV -

USCP vs. Eurocommercial Paper

Yield-to-worse = min[YTC, YTM]

SPV collects loan payments from firm’s customers

- SPV distributes cash flows to investors USCP ECP

Yield Measures for FRNs

Residential Mortgage Loans Currency US dollar Any currency

Quoted margin (QM): Spread paid by FRN

- Interest: fixed, adjustable, convertible Maturity Overnight Overnight to

Discount margin (DM): Spread required by market

- Amortization: full, partial, interest-only to 270 days 364 days

If QM > DM, FRN will trade above par

- Prepayment: penalty, no penalty Interest Discount Interest- FRN pricing formula:

- Foreclosure: non-recourse, recourse calculation basis bearing or (Ref + QM)(FV) (Ref + QM)(FV) + FV discount = m

Residential Mortgage-Backed Securities 1 … + m basis \1 + (Ref + DM) N

- Agency RMBS: Issued by government agencies; m ] \1 + (Ref + DM) m ] Settlement T + 0 T + 2 must have conforming loans Negotiable Can be sold Can be sold

Yield Measures for Money Market Instrument

- Non-agency RMBS: Issued by private companies

and may have non-conforming loans

Structured Financial Instruments

Discount Rate (DR) Basis Days

- Guarantee certificate: Zero-coupon bond with a PV = FV × \1 − × DR]

- Pass-through rate: MBS coupon rate

call option on the issuer’s equity Year

- Prepayment risk: Contraction (faster-than-

- Credit-linked note: Seller earns a premium for

Add-on Rate (AOR) Basis

expected); extension (slower-than-expected)

providing credit protection on underlying bond Days

- Prepayment rates are relative to PSA benchmark PV = FV£\1 + × AOR]

- Participation Instruments: Coupon payments Year

Collateralized Mortgage Obligations (CMO)

based on underlying rate (e.g., FRNs)

- Unlike pass-through securities, CMOs have

Implied Forward Rate (IFR)

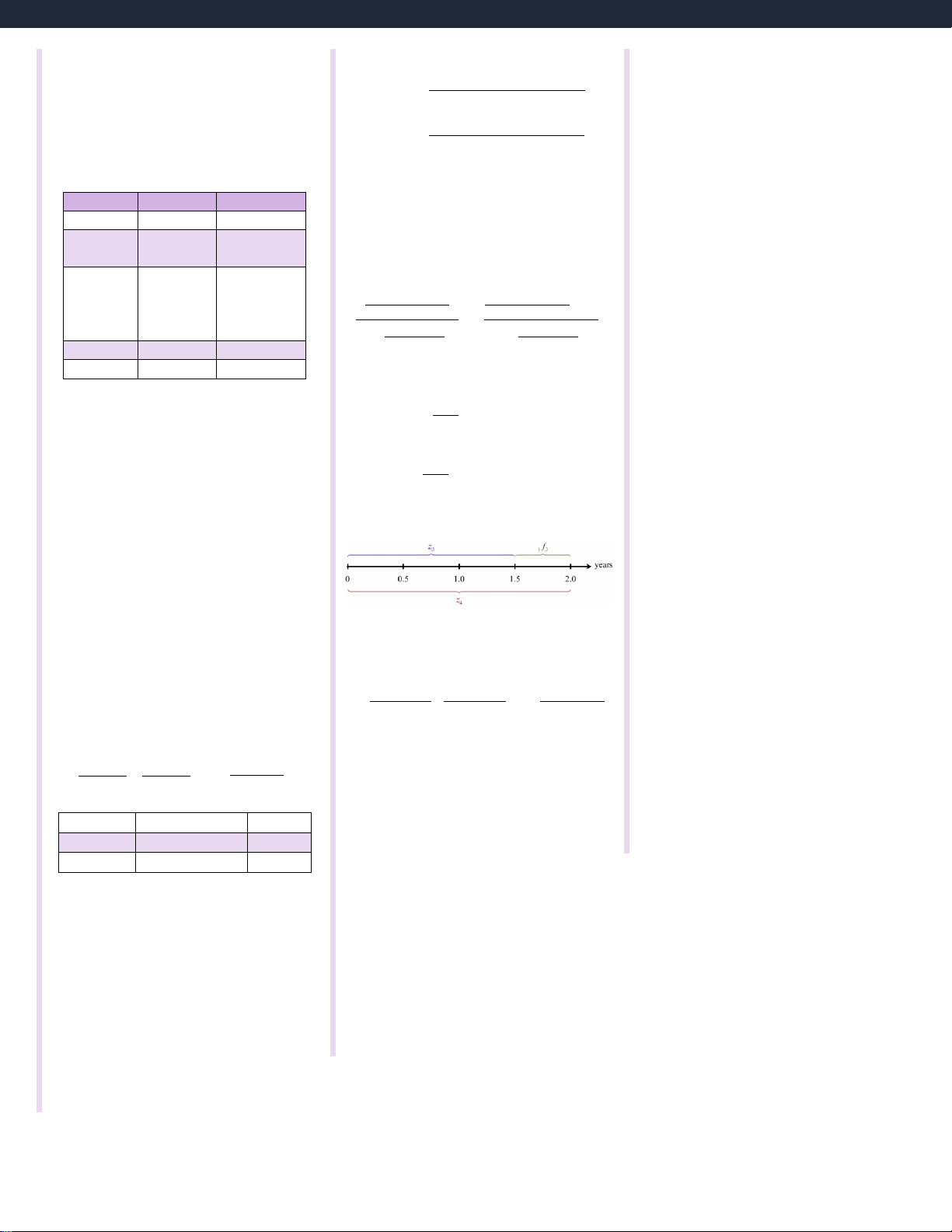

- Leveraged Instruments: Modify returns

tranches to redistribute cash flows and risks (1 + zA )A × m1 + IFR A ,B–A nB–A = (1 + zB )B

Leveraged floater: 2 × (Reference rate)

- Sequential-pay CMOs have principal and

Deleveraged floater: 0.5 × (Reference rate)

prepayments paid to the tranches sequentially

Leveraged inverse floater: Max coupon − 2 × (RR)

- Planned amortization class (PAC) CMOs have

support tranches to absorb prepayment risk

Factors Increasing Repurchase (Repo) Rates - Higher Collateral risk

Yield Spreads over Benchmark Yield Curve Non-Mortgage ABS

- Amortizing: E.g., auto loan ABS - Longer term

G-spread= YTM − Government bond yield

- Non-amortizing: E.g., credit card receivable ABS - Delivery requirement I-spread= YTM − Swap rate - Low quality collateral

Collateralized Debt Obligations (CDO) Z-spread

- Higher rates for alternative sources of funds PMT PMT PMT + FV

Securities backed by pool of debt obligations, such PV = + + ⋯ + (1 + z

as corporate bonds, leveraged bank loans, or credit 1 + Z)1 (1 + z2 + Z)2 (1 + zN + Z)N IN I T N R T O R D O U D CTIO I N O N TO TOFI F X I E X D E - D I-N I COME

NCOM EV A V L A U L A U T A I T O I N O N

(Can only be calculated by trial-and-error) default swap on securities

Bond Pricing with Spot Rates

Option-adjusted spread (OAS) Covered Bonds PMT PMT PMT + FV PV = + + ⋯ +

OAS = Z-spread − Option value (in basis points)

- Dual recourse against the issuing financial (1 + z1)1 (1 + z2)2 (1 + zN)N

institution and the cover pool

CR: Coupon Rate; MDR: Market Discount Rate INTRODUCTION TO

- One bond class per cover pool

INTRODUCTION TO ASSET-BACKED CR = MDR Price = Par Value Par SE A C S U

SERTI-TBIE A S C KED SECURITIES

- Issuer must replace non-performing asset with CR < MDR Price < Par Value Discount performing asset

Parties to a Securitization CR > MDR Price > Par Value Premium

- Seller/Depositor: Originates loans (assets) -

Bond Pricing Relationships

Issuer: Special purpose vehicle (SPV) established

to create asset-backed securities (ABS)

- Inverse effect: Price moves opposite to yield

- Servicer: Collects payments on underlying loans

- Convexity effect: Falling yield has greater price

impact than equivalent increase in yield ABS Tranching

- Coupon effect: Yield changes have greater impact

- Credit tranching: Certain tranches absorb credit on lower coupon bonds losses before others

- Maturity effect: Yield changes have greater impact

- Absolute priority rule: Senior claims outrank

on longer-term bonds (may not apply to low-

subordinated claims in the event of a liquidation

coupon bonds trading at very deep discounts)

- Time tranching: Certain tranches are exposed to prepayment risk

Flat Price, Accrued Interest, and Full Price

PVFull = PVFlat + AI = (PV)(1 + r)t⁄T AI = (t⁄T) × PMT

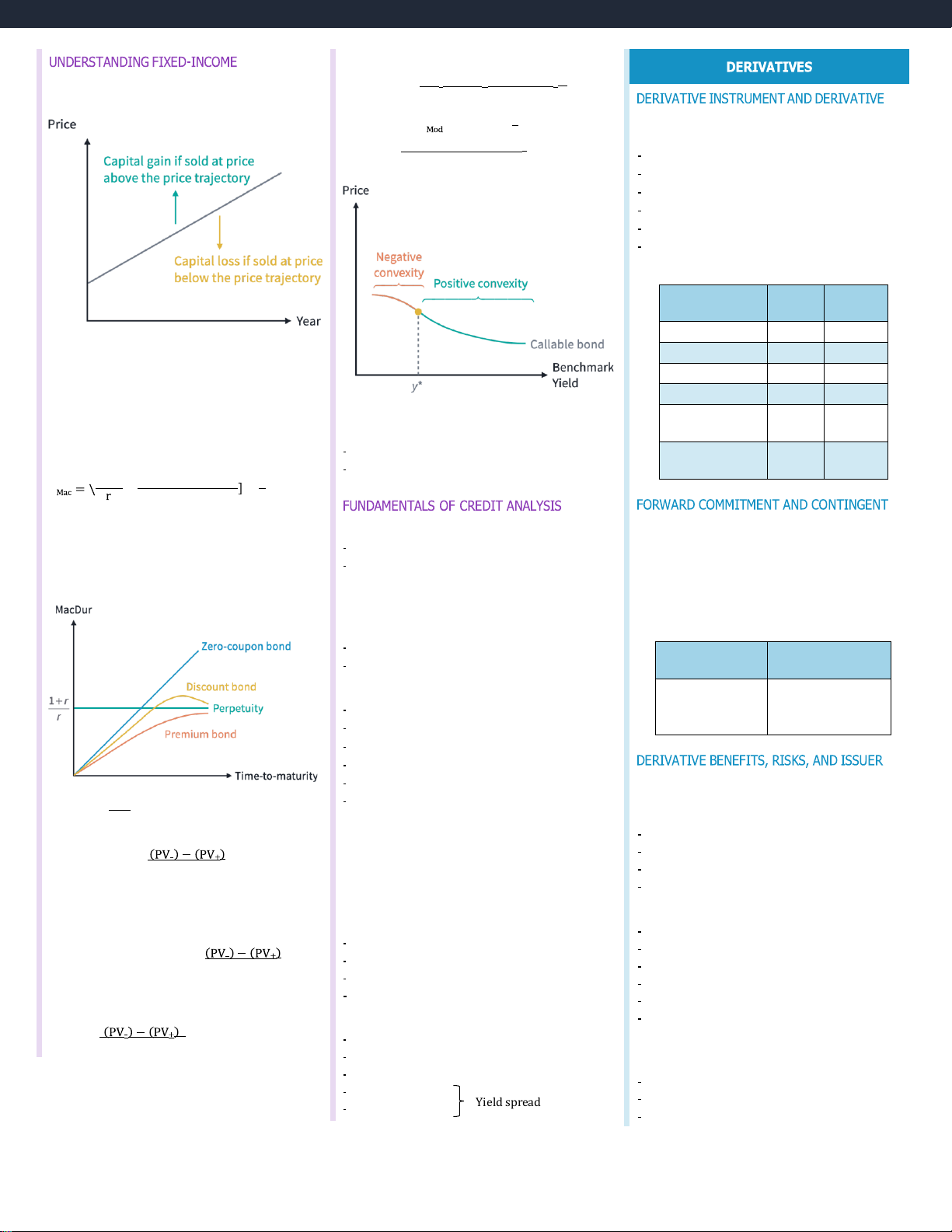

UNDERSTANDING FIXED-INCOME RISK AND Convexity DERIVATIVES RE RITU SKR N A S ND RETURNS (PV ApproxCon = –) + (PV+) − [2 × (PVO)]

Constant Yield Price Trajectory (ΔYield)2(PVO)

DERIVATIVE INSTRUMENT AND DERIVATIVE 1 MAR MA K RKET E T F E F A E T A UR TU E R SE S %ΔPVFull = −D × ΔYTM + (Conv)(ΔYTM)2 2 Derivative Underlyings (PV–) + (PV+) − 2(PVO) EffConv = Equities (ΔCurve)2(PVO)

Fixed-income instruments and interest rates Currencies Commodities Credit

Other (e.g., weather, crypto, longevity risk) Derivatives Markets OTC ETD Market Market Liquidity Lower Higher

Yield Duration vs. Curve Duration Trading costs Higher Lower

Yield duration: Sensitivity to YTM Transparency Less Greater

Measures: Macaulay duration, modified duration,

money duration, price value of basis point (PVBP) Standardization Lower Higher Duration Gap

Curve duration: Sensitivity to benchmark yields Flexibility/ Higher Lower

Duration gap = DMac − Investment horizon

(e.g., effective duration); for bonds with options customization

If positive: Price risk > Reinvestment risk Counterparty Macaulay Duration Higher Lower

If negative: Reinvestment risk > Price risk credit risk 1 + r 1 + r + N(c − r) t D − − c[(1 + r)N − 1] + r T

FUNDAMENTALS OF C REDIT A NALYSIS

FORWARD COMMITMENT AND CONTINGENT r: YTM CL C AI LA M I MF E F A E T A UR TU E R SE A S N AD IN ND S I TRUM NSTR E U N MTES NTS Credit Risk c: Coupon rate Types of Derivatives

Default risk: Probability of default

N: Number of periods to maturity

Forward commitments: Obligation to trade on a

Loss severity: Loss given default

t: Number of days since last coupon payment

specified date at a previously agreed price

E[Loss] = Pr(Default) × Loss severity

T: Number of days in each coupon period

Contingent claims: Trade may or may not occur

Loss severity = 1 − Recovery rate

depending on market conditions Spread Risk

Credit migration risk: Possibility of downgrade Forward

Market liquidity risk: Need to sell at a discount Contingent Claims Commitments Seniority Ranking Forward contract Options

First Lien Loan – Senior Secured Futures contracts Credit derivatives Second Lien Loan – Secured Swaps Senior Unsecured

DERIVATIVE BENEFITS, RISKS, AND ISSUER Senior Subordinated A AND ND I N I VE NV S ETO ST R O U R S E U S SES Subordinated Modified Duration

Derivative Benefits and Risks D Junior Subordinated ModDur = Mac Benefits:

Pari passu: All creditors in the same ranking, 1 + r

Risk allocation, transfer, and management

%ΔPVFull = −AnnModDur × ΔYield

regardless of maturity, have the same priority Information discovery Credit Ratings ApproxModDur = Operational advantages 2(ΔYield)(PVO)

Investment grade: Baa3/BBB- and above Market efficiency

Money Duration and PVBP

Non-investment grade: Ba1/BB+ and below Risks:

MoneyDur = AnnModDur × PVFull

Four C’s of Credit Analysis Potential for speculative use

ΔPVFull ≈ −MoneyDur × ΔYield Capacity Lack of transparency Collateral

Price value of a basis point = Basis risk 2 Covenants Liquidity risk