Chapter 2 - Summary: Economics & Its Impact on Business Admin | Môn Business Administration - Trường Đại học Quốc tế, Đại học Quốc gia Thành phố Hồ Chí Minh

Chapter 2 - Summary: Economics & Its Impact on Business Admin Môn Business Administration. Tài liệu được sưu tầm gồm 41 trang, giúp bạn ôn tập tốt hơn. Mời các bạn đón xem.

Môn: Business Administration (HCMIU) 10 tài liệu

Trường: Trường Đại học Quốc tế, Đại học Quốc gia Thành phố Hồ Chí Minh 2 K tài liệu

Tác giả:

Preview text:

lOMoAR cPSD| 59078336 Understanding Economics and How it Affects Business McGraw-Hill/Irwin

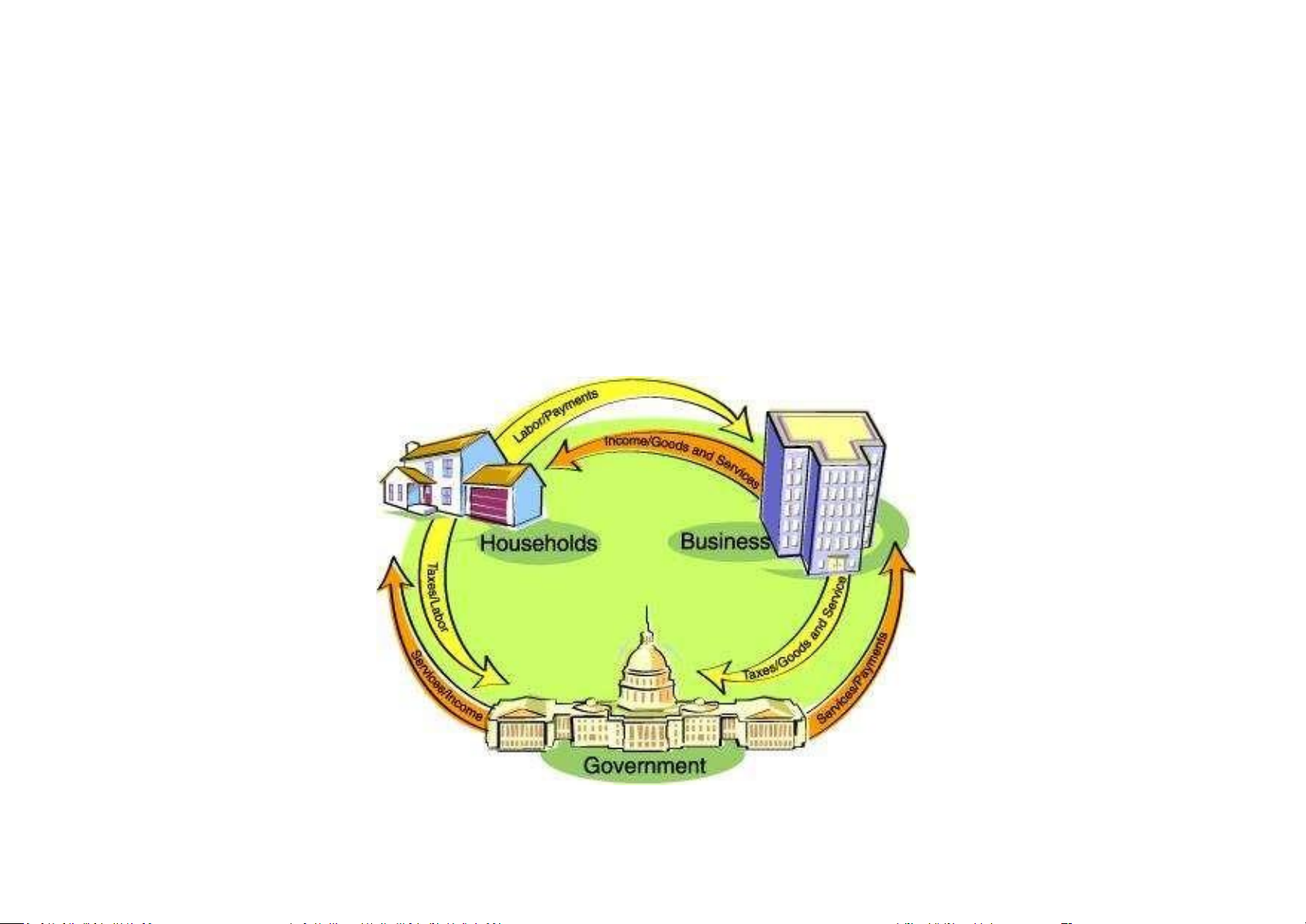

Copyright © 2015 by the McGraw-Hill Companies, Inc. All rights reserved. lOMoAR cPSD| 59078336 What Is Economics?

Economics is the study of how society

chooses to employ resources to produce goods

and services and distribute them among

competing groups and individuals. lOMoAR cPSD| 59078336 BRANCHES OF ECONOMICS

Macroeconomics: Concentrates on the operation of a nation’s economy as a whole. Microeconomics: Concentrates on the behavior of people and organizations in markets for particular products or services. RESOURCE DEVELOPMENT lOMoAR cPSD| 59078336

Resource Development -- The study of how to

increase resources and create conditions that will

make better use of them. We accomplish this by: • New Technology • New Methods • New Processes • Better Resources EXAMPLES of RESOURCE DEVELOPMENT lOMoAR cPSD| 59078336

• Making resources last longer - Recycling

• New energy sources - Hydrogen fuel • New ways of growing foods - Hydroponics

• New ways of creating goods and services – Aquaculture – Nanotechnology

Resource Development is often referred to as the New Economy. lOMoAR cPSD| 59078336 Economic Systems

CAPITALISM is an economic system in which all or most of the

factors of production and distribution are privately owned and operated for profit.

SOCIALISM is an economic system based on the premise that some,

if not most, basic businesses should be owned by the government

so that profits can be distributed among the people.

COMMUNISM is an economic and political system in which the

state (the government) makes almost all economic decisions and

owns almost all the major factors of production.

Note: These are nothing but economic philosophies of how

society (country) chooses to employ its resources. TWO MAJOR ECONOMIC SYSTEMS lOMoAR cPSD| 59078336

• Free-Market Economies -- The market largely

determines what goods and services are produced,

who gets them, and how the economy grows. (Capitalism)

• Command Economies -- The government

largely determines what goods and services are

produced, who gets them, and how the economy will grow. (Socialism, Communism} 2-7 MIXED ECONOMIES

• Note: Neither free-market nor command economies

have created sound economic conditions so countries

use a mix of the two economic systems. lOMoAR cPSD| 59078336

• Mixed Economies -- Some allocation of resources is

made by the market and some by the government.

• Although the U. S. subscribes to the Capitalism

philosophy, the U.S. does employ some

Socialism and Communism philosophies making it a mixed economy. 2-8

Limits of Free-Markets (Capitalism)

• Inequality of Wealth Causes National & World Tension • Greed Compromises Ethics

• Limitations Push Country towards Socialism, which Leads to More Government lOMoAR cPSD| 59078336 Regulation Trends in World Economies

• Communist governments are disappearing. • Socialist governments are cutting back on social programs, lowering taxes and moving toward capitalism. • Capitalist countries are

increasing social programs and moving more toward socialism. FOUR DEGREES

of COMPETITION or FORMS of CAPITALISM lOMoAR cPSD| 59078336 1. Perfect or Pure Competition 2. Monopolistic Competition 3. Oligopoly 4. Monopoly EXAMPLES

Perfect (Pure) Competition: Many sellers, similar

products. Example Agricultural Products Kansas Nebraska VS. Wheat Wheat lOMoAR cPSD| 59078336

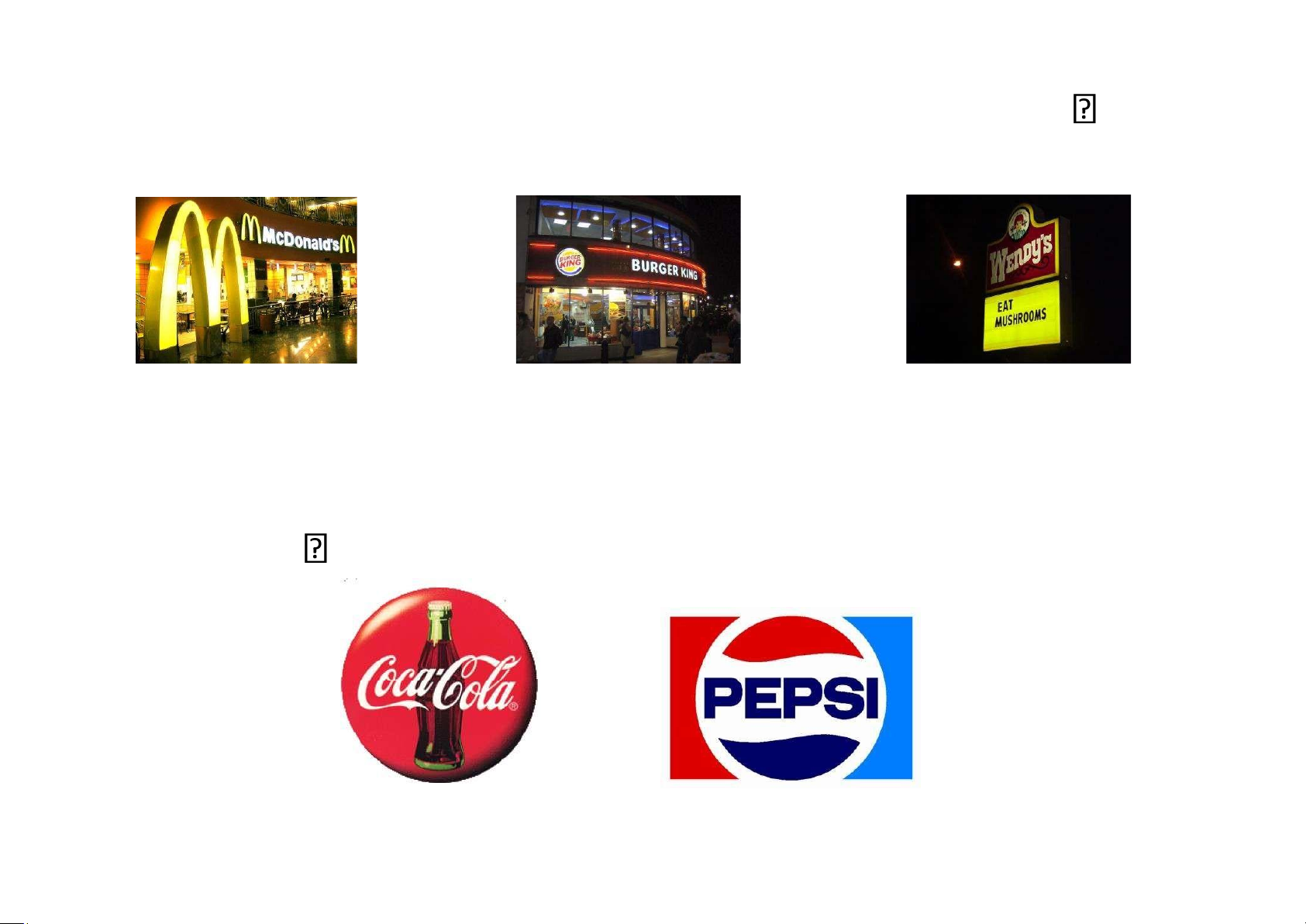

Monopolistic Competition: Large number of sellers,

products differ but are close substitutes. Example Fast Food EXAMPLES

Oligopoly: Few sellers that dominate market. Example Soft Drinks lOMoAR cPSD| 59078336

Pure Monopoly: Single seller has all the sales. Example Public Utilities PRICING lOMoAR cPSD| 59078336

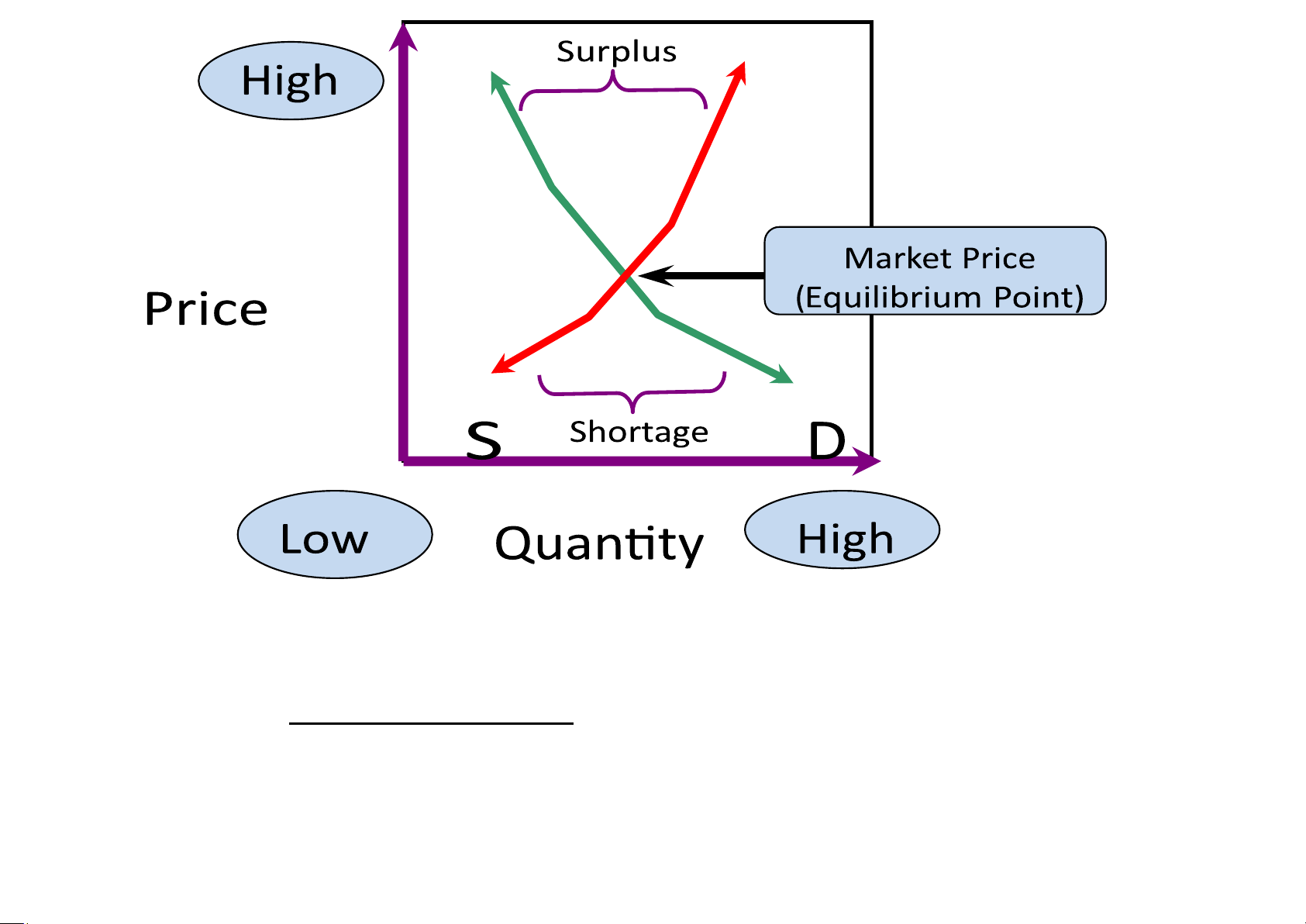

• A seller may want to sell shirts for $50, but only a few

people may buy them at that price. This creates a surplus of goods.

• A seller lowers the price to $30,

more people than normal buy the

shirts. This creates a shortage of goods.

• The seller establishes a price of $40 based on what consumers are

willing to pay and what the seller is willing to provide. SUPPLY CURVES

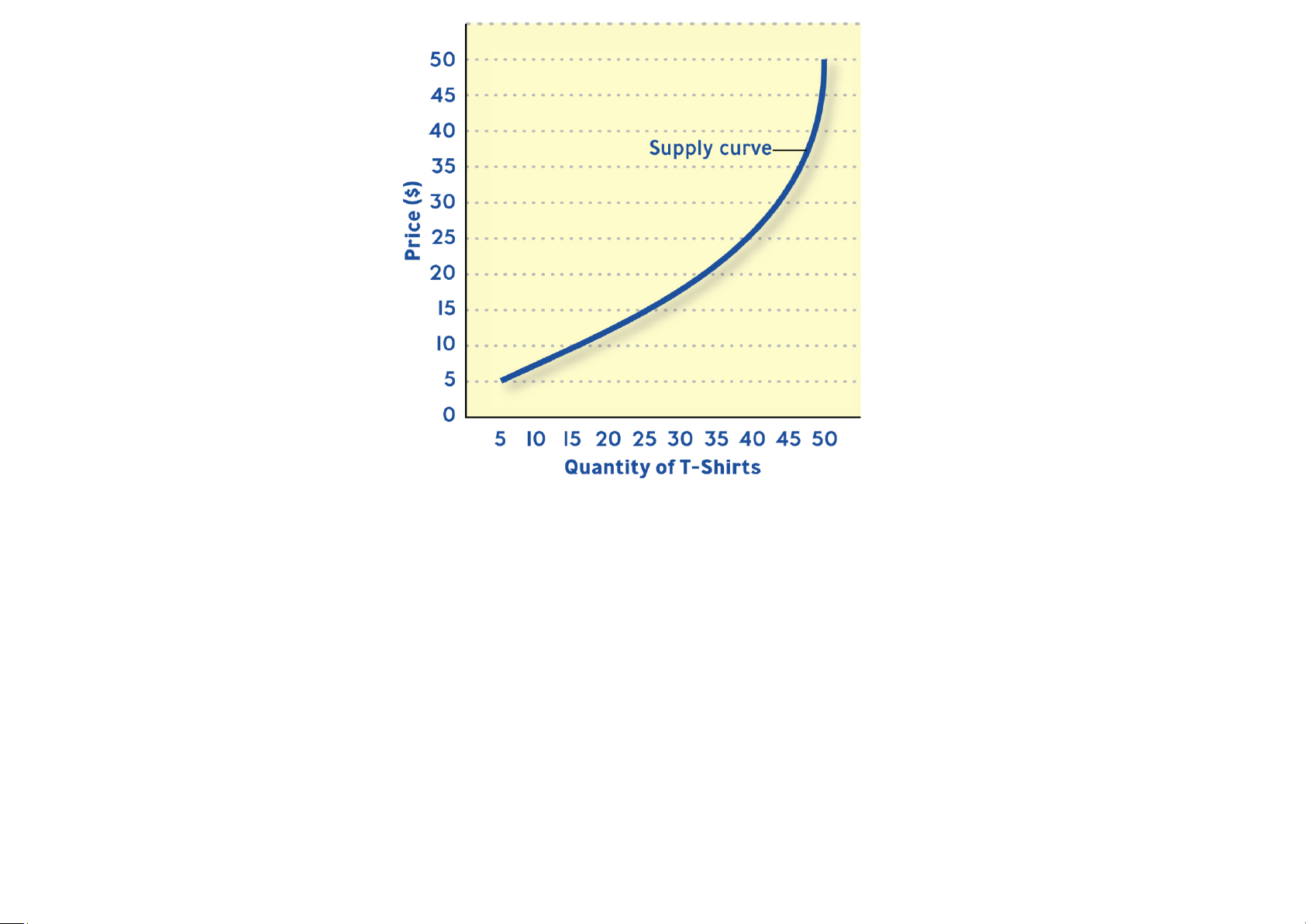

• Supply -- The quantities of products businesses are

willing to sell at different prices. lOMoAR cPSD| 59078336 DEMAND CURVES

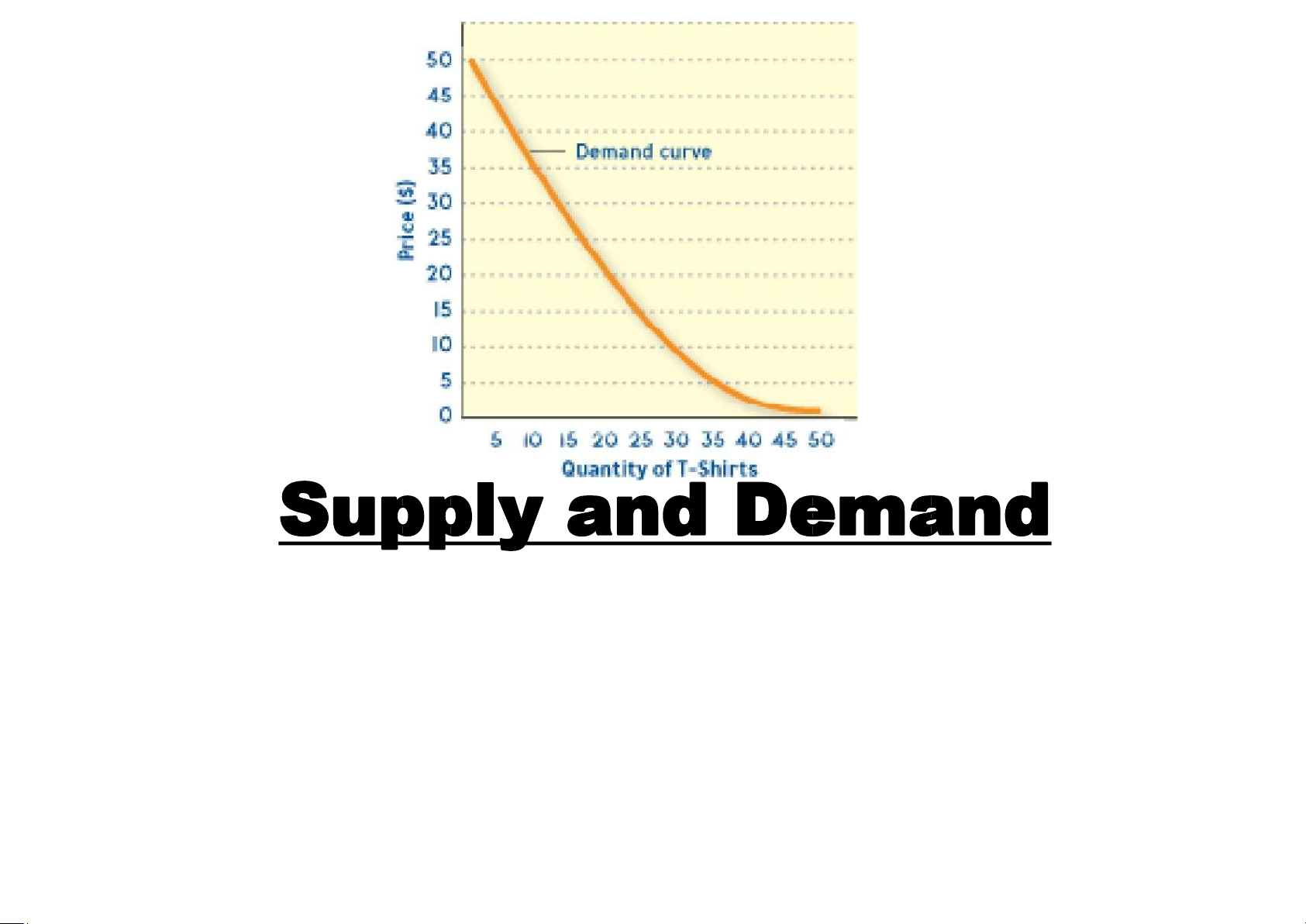

• Demand -- The quantities of products consumers are

willing to buy at different prices. lOMoAR cPSD| 59078336 lOMoAR cPSD| 59078336 Price Elasticity

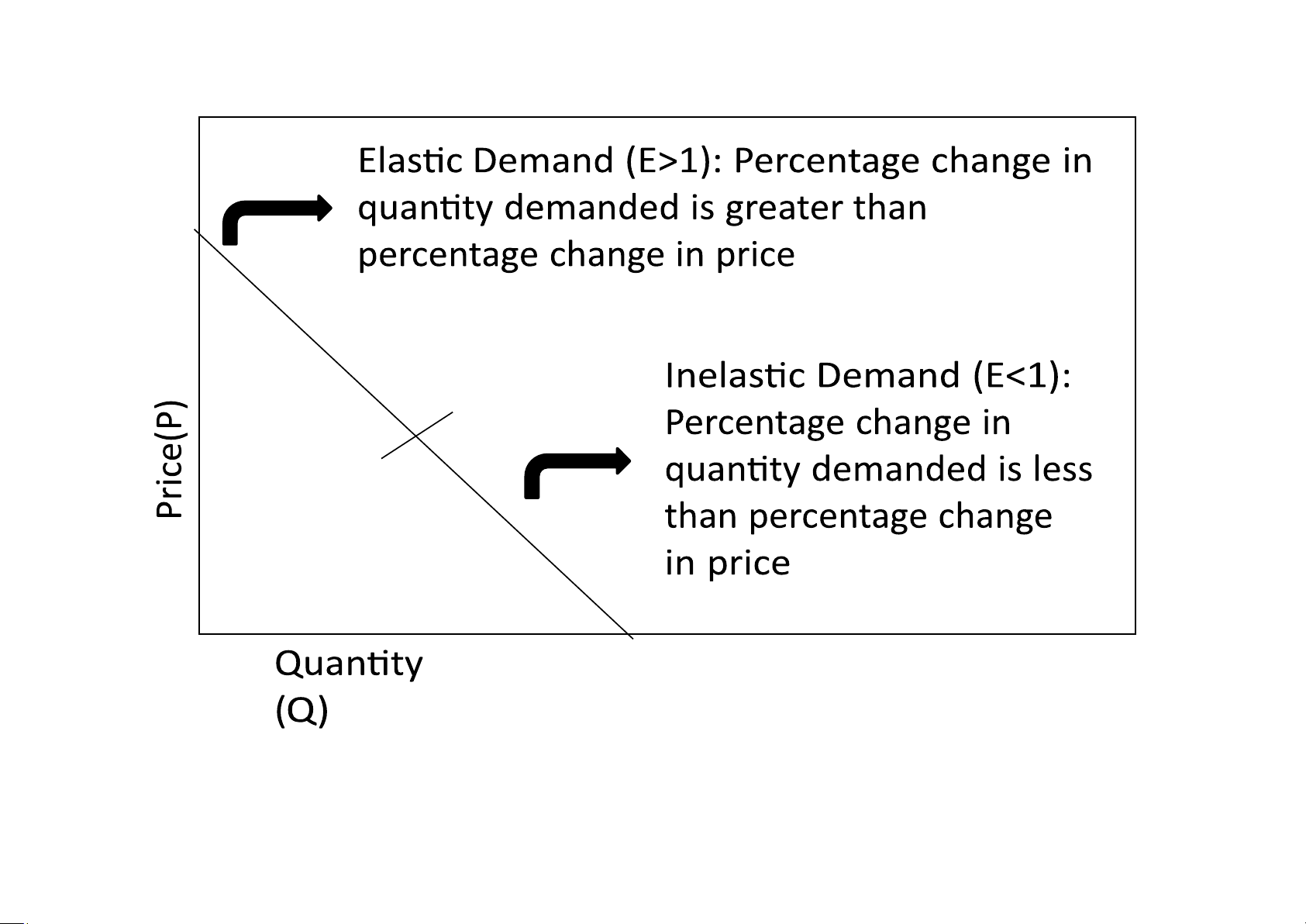

When Elastic Demand exists, a slight decrease in the

price of a product results in a relatively large

increase in demand or items sold. On the other lOMoAR cPSD| 59078336

hand, a slight increase in price results in a relatively

large decrease in demand or items sold. In other

words, people are price sensitive. When Inelastic

Demand exist, a slight increase or decrease in price

will not significantly change the demand or items

sold. However, lowering price will increase the

quantity sold but revenues will decrease. In other

words, people are not as price sensitive. lOMoAR cPSD| 59078336 Price Elasticity lOMoAR cPSD| 59078336 Elasticity Example Elastic Demand Price Demand Revenue $7.00 50 $350.00 $9.00 20 $180.00 Inelastic Demand Price Demand Revenue $7.00 50 $350.00 $9.00 47 $423.00 lOMoAR cPSD| 59078336

SOME DETERMINANTS OF ELASTICITY

Price elasticity can vary with products and services.

A product could have elastic demand in one part of

the country and inelastic demand in another part of

the country. Also price elasticity for a product or

service is influenced by several factors.

Availability of Substitutes: If a product or service

has close substitutes, demand would be elastic.

However if a product or service has few substitutes,

demand would be inelastic. For example, a new

shirt or blouse has many possible substitutes, but

gasoline has almost no substitutes.

Tài liệu liên quan:

-

Chapter 1-3: Taking Risks & Making Profits in Business | Môn Business Administration - Trường Đại học Quốc tế, Đại học Quốc gia Thành phố Hồ Chí Minh

107 54 -

Chap 9 & 10 Summaries: Production, Motivation, & Marketing Insights | Môn Business Administration - Trường Đại học Quốc tế, Đại học Quốc gia Thành phố Hồ Chí Minh

124 62 -

Notes Final Revisions | Môn Business Administration - Trường Đại học Quốc tế, Đại học Quốc gia Thành phố Hồ Chí Minh

86 43 -

Midterm Testbank | Môn Business Administration - Trường Đại học Quốc tế, Đại học Quốc gia Thành phố Hồ Chí Minh

168 84