Đề cương ôn tập môn học - Kinh tế vi mô | Trường Đại học Hà Nội

1. Absolute advantage: the ability to produce a good using fewer inputs than another producer Or: the ability to produce more goods with the same input than other producer. 2. Opportunity cost: whatever must be given up to obtain some items. Tài liệu được sưu tầm giúp bạn tham khảo, ôn tập và đạt kết quả cao trong kì thi sắp tới. Mời bạn đọc đón xem !

Môn: Kinh tế vi mô (HANU) 17 tài liệu

Trường: Trường Đại học Hà Nội 1.1 K tài liệu

Tác giả:

Preview text:

lOMoARcPSD|46958826 lOMoARcPSD|46958826

INTERDEPENDENCE & GAINS FROM TRADE

1. Absolute advantage: the ability to produce a good using fewer inputs than another producer

Or: the ability to produce more goods with the same input than other producer.

2. Opportunity cost: whatever must be given up to obtain some items.

3. Comparative advantage: the ability to produce a good at a lower opportunity cost than another producer.

NOTE: 1 person can have an absolute advantage in both goods, but it is impossible for

1 person to have a comparative advantage in both goods.

4. The gains from specialization and trade are based not on absolute advantage but on

comparative advantage

5. Price of the Trade: For both parties to gain from trade, the price at which they

trade must lie between the two opportunity costs.

THE MARKET OF DEMAND AND SUPPLY 1. Demand

- Quantity demanded: of any goods is the amount of the good that buyers are

willing and able to purchase.

- Law of demand: other things equal when price of a good rises -> quantity demanded of this good decreases. Shift in demand curve:

If something happens to alter the quantity demanded at any given price, the demand curve shifts.

Shift to the right - > raises quantity demanded

Shift to the left -> lowers quantity demanded lOMoARcPSD|46958826

+ Income: lower income -> spend less

o if the demand for a good falls when income falls -> the good is

called normal good. Ex: milk tea, novels…..

o If the demand for a good rises when income falls -> the food is

called inferior good. Ex: instant noodles

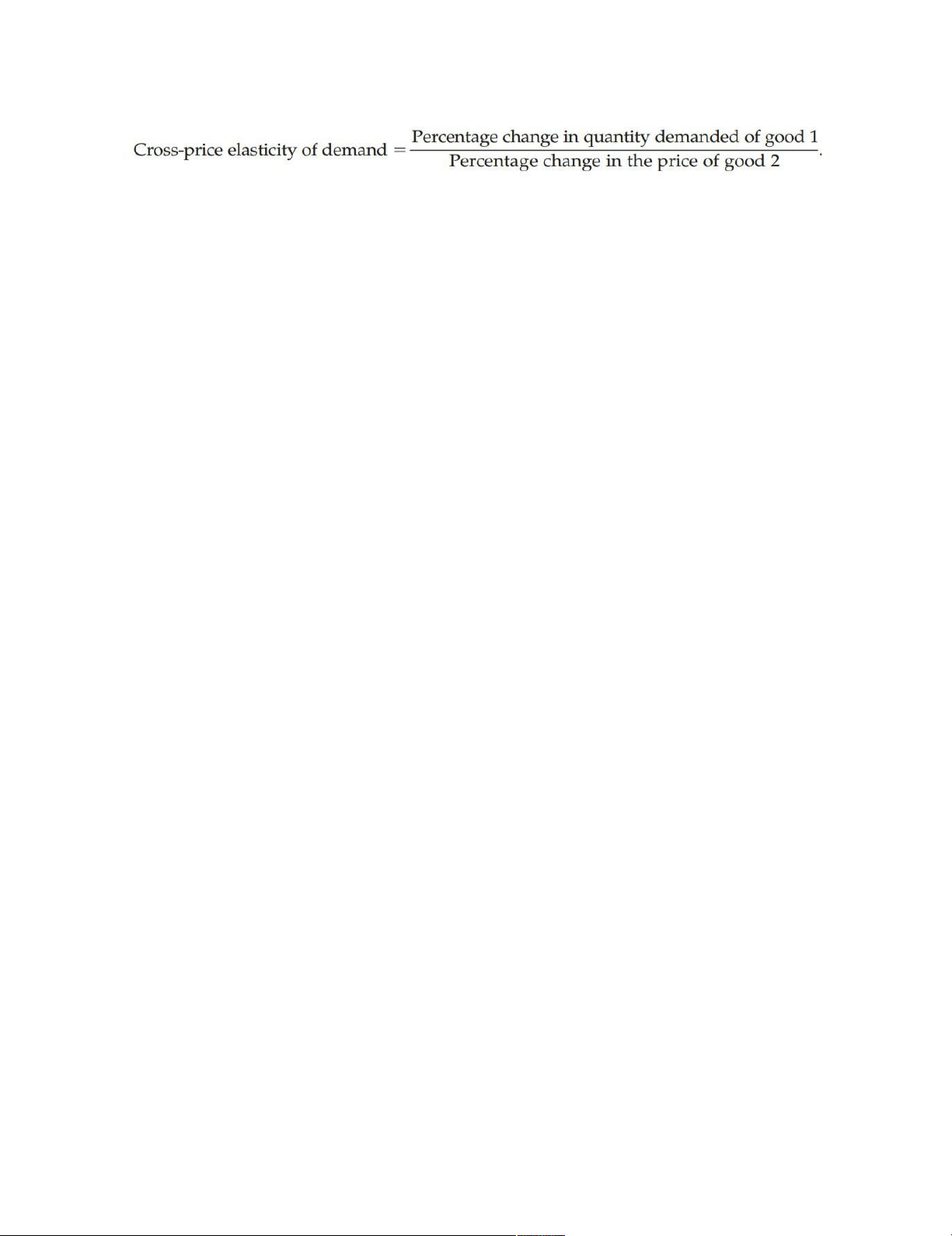

+ Price of related goods:

o When a fall in the price of 1 good reduces the demand for another good ->

2 goods are called substitutes => pairs of goods that are used in place of each other.

Ex: Mc Donald’s or Burger King, Coca cola or Pepsi

o When a fall in the price of 1 good increases the demand for another food ->

2 goods are called complements => pairs of goods that are used together

Ex: Bread and butter, movies ticket and popcorn ….

+ Tastes: ex: Jeans…..

+ Expectations: your expectations about the future may affect your demand for a good/ service today.

Ex: If you (customers) expect the price of I- phone 14 will decrease in the

next month, your demand for I- phone 14 today will be lower.

+ Number of buyers: more people => more quantity demanded 2. Supply

- Quantity supplied: of any good is the amount of the good that sellers are

willing and able to sell.

- Law of supply: other things equal, price rise -> quantity supplied increases Shift in supply curve:

Shift to the right: if the change raises the quantity that sellers want to produce

Shift to the left: if the change lowers the quantity that sellers wish to produce

+ Input prices: when the price of one or more of these inputs rises, firms supply less

+ Technology: the advance in technology raises the supply.

+ Expectations: if firm (producer) expect the price of 1 good to rise in the future,

it will store this goods and supply less in the market today

+ Number of sellers: more sellers -> more quantity supplied. lOMoARcPSD|46958826

3.Supply & Demand together.

- Equilibrium point: QD = QS (the intersect between demand curve and supply curve)

- Surplus a situation in which quantity supplied is greater than quantity demanded

- Shortage a situation in which quantity demanded is greater than quantity supplied ELASTICITY AND ITS

APPLICATION 1. The elasticity of Demand.

Elasticity a measure of the responsiveness of quantity demanded or quantity supplied

to a change in one of its determinants

Demand for a good is said to be elastic if the quantity demanded responds substantially

to changes in the price.

Demand is said to be inelastic if the quantity demanded responds only slightly

to changes in the price.

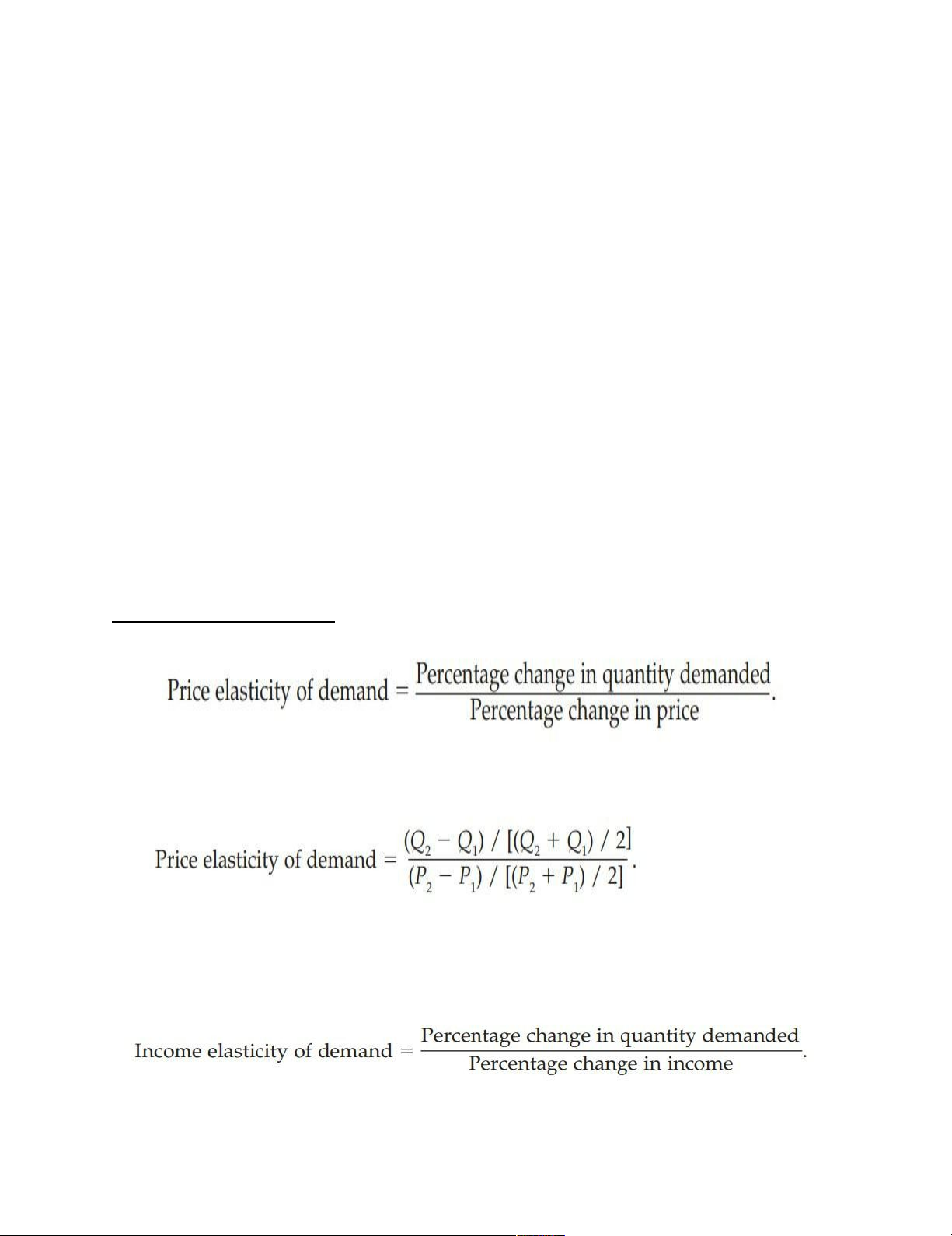

Price elasticity of demand:

- Demand is considered elastic when the elasticity is greater than 1.

- Demand is considered inelastic when the elasticity is less than 1.

- If the elasticity is exactly 1 and demand is said to have unit elasticity. lOMoARcPSD|46958826

2. What influences the Price Elasticity of Demand?

Availability of Close Substitutes Goods with close substitutes tend to have more elastic demand.

Necessities versus Luxuries Necessities tend to have inelastic demands, whereas luxuries have elastic demands

Definition of the Market . Narrowly defined markets tend to have more elastic

demand than broadly defined markets because it is easier to find close substitutes for narrowly defined goods

Time Horizon Goods tend to have more elastic demand over longer time horizons.

SUPPLY, DEMAND AND GOVERNMENT POLICIES 1. Controls on Prices

- Price ceiling: a legal maximum on the price at which a good can be sold.

- Price floor: a legal minimum on the price at which a good can be sold.

1.1. How price ceilings affect market outcomes?

If the government imposes a price ceiling higher than equilibrium price =>

the price ceiling is not binding

If the government imposes a price ceiling lower than equilibrium price =>

the price ceiling is binding => shortage

1.2. How price floors affect market outcomes?

If equilibrium price is above the price floor => the price floor is not binding If

equilibrium price is below the price floor => the price floor is binding => surplus 2. Taxes

2.1. How tax on sellers affect market outcome?

=> tax ships the supply curve -> to the left

Price received by sellers = selling price – size tax lOMoARcPSD|46958826

2.2. How tax on buyers affect market outcome?

=> tax ships the demand curve -> to the left

Total cost buyers have to pay = price to buyers + tax

2.3. Elasticity and tax incidence.

- Elastic supply, inelastic demand => the incidence of tax falls more heavily

on consumers than on producers.

- Inelastic supply, elastic demand => the incidence of tax falls more heavily on producers than on consumers. COST OF PRODUCTION

- Amount a firm received for sale of its output called total revenue

- Amount a firms paid to buy inputs called total cost

Profit = total revenue – total cost

- Input cost that require the firms to pay out money => explicit costs

- Input cost that do not require a cash outlay by the firm => implicit costs

Total cost = explicit costs + implicit costs

- Fixed cost (FC): costs that do not vary with the quantity of output produced.

- Variable cost (VC): costs that vary with the quantity of output produced.

Total cost = Fixed costs + Variable costs.

- Marginal cost (MC): the increase in total cost that arises from an extra unit

of production. = change in total cost / change in quantity

- Average total cost (ATC) = TC / Q = AFC + AVC

- Average fixed cost (AFC) = FC / Q

- Average variable cost (AVC) = VC / Q

Whenever marginal cost is less than average total cost, average total cost is falling.

Whenever marginal cost is greater than average total cost, average total cost is rising

The marginal-cost curve crosses the average-total-cost curve at the minimum of average total cost lOMoARcPSD|46958826

When quantity is low, ATC declines as quantity rises;

When quantity is high, ATC rises as quantity rises EXTERNALITY

An externality arises when a person engages in an activity that influences the well-

being of a bystander but neither pays nor receives any compensation for that effect.

- If the impact on the bystander is adverse, it is called a negative externality.

- If it is beneficial, it is called a positive externality.

Negative externalities lead markets to produce a larger quantity than is socially desirable.

Positive externalities lead markets to produce a smaller quantity than is socially desirable.

=> To remedy the problem, government can internalize the externality by taxing goods

that have negative externalities and subsidizing goods that have positive externalities.

PUBLIC POLICIES TOWARD EXTERNALITIES

Government can respond to externalities in one of two ways:

- Command-and-control policies: Regulation regulate behavior directly.

- Market-based policies provide incentives so that private decision makers

will choose to solve the problem on their own.

+ Corrective taxes and Subsidies + Tradable Pollution Permits lOMoARcPSD|46958826

CONSUMERS, PRODUCERS AND THE EFFICIENCY OF MARKETS Willingness

to pay the maximum amount that a buyer will pay for a good Consumer

Consumer surplus = the amount a buyer is willing to pay for a Surplus

good - the amount the buyer actually pays for it

The area below the demand curve and above the price

Cost the value of everything a seller must give up to produce a good Producer

Producer surplus = the amount a seller is paid for a good -

the seller’s cost of providing it Surplus

The area below the price and above the supply curve.

Total surplus = Value to buyers - Cost to sellers.

If an allocation of resources maximizes total surplus =>

allocation exhibits efficiency o

Free markets allocate the supply of goods to the buyers who value them most highly o

Free markets allocate the demand for goods to the sellers

who can produce them at the lowest cost. Market efficiency o

Free markets produce the quantity of goods that

maximizes the sum of consumer and producer surplus

o At quantities < the equilibrium quantity, the value to buyers

> the cost to sellers

o At quantities > the equilibrium quantity, the cost to sellers >

the value to buyers. lOMoARcPSD|46958826 Competitive market Monopoly market Oligopoly market • There are many buyers The sole seller of A few sellers and many sellers in the this product Offer similar or identical market. Not have close products • The goods offered by substitutes High barrier to entry the various sellers are High barrier to largely the same. entry • Firms can freely enter or exit the market. Price taker Price maker P=MR=AR P>MR=MC Oligopoly price < Monopoly price > Competitive price P=MC MR=MC When firms in an oligopoly => profit maximizing => profit maximizing individually choose production

to maximize profit, they produce

a quantity of output greater than the level produced by monopoly

and less than the level produced by competition. Short run decision: Price discrimination

Nash equilibrium: a situation in - Shut down: P < AVC the business practice of which economic actors Long run decision:

selling the same good at interacting with one another, - Exit: P < ATC different prices to

each choose their best strategy - Enter: P > ATC different customers.

given the strategies that all the other actors have chosen

Dominant strategy a strategy

that is best for a player in a game regardless of the strategies chosen by the other players

Tài liệu liên quan:

-

Chapter 14 Firms in Competitive Markets - Kinh tế vi mô | Trường Đại học Hà Nội

411 206 -

Chapter 14 Firms in Competitive Markets - Kinh tế vi mô | Trường Đại học Hà Nội

302 151 -

Profits and Perfect Competition - Kinh tế vi mô | Trường Đại học Hà Nội

318 159 -

Chapter 6 Supply, Demand, and Government Policies - Kinh tế vi mô | Trường Đại học Hà Nội

312 156 -

10 Principles of economics and thinking like an economist - Kinh tế vi mô | Trường Đại học Hà Nội

332 166