Exercise and solution chapter 19

Tài liệu học tập môn Statistics for Business (BAO8OIU) tại Trường Đại học Quốc tế, Đại học Quốc gia Thành phố Hồ Chí Minh. Tài liệu gồm 8 trang giúp bạn ôn tập hiệu quả và đạt điểm cao! Mời bạn đọc đón xem!

Môn: Statistics for Business (BAO8OIU) 43 tài liệu

Trường: Trường Đại học Quốc tế, Đại học Quốc gia Thành phố Hồ Chí Minh 2 K tài liệu

Tác giả:

Preview text:

lOMoARcPSD|359 747 69 Chap 19

1.Dividends and Taxes Lee Ann, Inc., has declared a $9.50 per-share dividend.

Suppose capital gains are not taxed, but dividends are taxed at 15 percent. New IRS

regulations require that taxes be withheld when the dividend is paid. Lee Ann sells

for $115 per share, and the stock is about to go ex-dividend. What do you think the

ex-dividend price will be?

After tax dividend = $9.50(1 – .15) = $8.08

The stock price should drop by the aftertax dividend amount, or Ex-

dividend price = $106.93

3. Stock Splits For the company in Problem 2, show how the equity accounts will change if: a.

Hexagon declares a four-for-one stock split. How many shares are

outstanding now? What is the new par value per share? b.

Hexagon declares a one-for-five reverse stock split. How many shares are

out-standing now? What is the new par value per share? a.

To find the new shares outstanding, we multiply the current

shares outstanding times theratio of new shares to old shares, so:

New shares outstanding = 30,000(4/1) = 120,000

The equity accounts are unchanged except that the par value of the stock is changed by the

ratio of new shares to old shares, so the new par value is:

New par value = $1(1/4) = $0.25 per share. b.

New shares outstanding = 30,000(1/5) = 6,000.New par value =

$1(5/1) = $5.00 per share.

4. Stock Splits and Stock Dividends Roll Corporation (RC) currently has 330,000

shares of stock outstanding that sell for $64 per share. Assuming no market

imperfections or tax effects exist, what will the share price be after: a. RC has a five-for-three stock split?

b. RC has a 15 percent stock dividend?

c. RC has a 42.5 percent stock dividend?

d. RC has a four-for-seven reverse stock split?

Determine the new number of shares outstanding in parts (a) through (d). The new stock price:

a. $38.40 b. $55.65 c. $44.91 d. $112

The new shares outstanding:

a. 550,000 b. 379,500 c. 470,250 d. 188,571 5.

Regular Dividends The balance sheet for Levy Corp. is shown here in market

valueterms. There are 12,000 shares of stock outstanding. Market Value Balance Sheet Cash $ 55,000 Equity $465,000 Fixed assets 410,000 Total $465,000 Total $465,000 lOMoARcPSD|359 747 69

The company has declared a dividend of $1.90 per share. The stock goes ex

dividend tomorrow. Ignoring any tax effects, what is the stock selling for today?

What will it sell for tomorrow? What will the balance sheet look like after the dividends are paid? The stock price today:

P0 = $465,000 equity/12,000 shares = $38.75 per share

Ignoring tax effects, the stock price will drop by the amount of the dividend, so:

PX = $38.75 – 1.90 = $36.85

The total dividends paid will be: $22,800

The equity and cash accounts will both decline by $22,800. 6.

Share Repurchase In the previous problem, suppose Levy has announced it isgoing

to repurchase $22,800 worth of stock. What effect will this transaction have on the

equity of the firm? How many shares will be outstanding? What will the price per

share be after the repurchase? Ignoring tax effects, show how the share repurchase

is effectively the same as a cash dividend.

Repurchasing the shares wil reduce shareholders’ equity by $22,800.

The shares repurchased will be the total purchase amount divided by the stock price, so:

Shares bought = $22,800/$38.75 = 588 shares And

the new shares outstanding will be: 11,412 shares

After the repurchase, the new stock price is:

Share price = $442,200/11,412 shares = $38.75

The repurchase is effectively the same as the cash dividend because you either hold a

share worth $38.75 or a share worth $36.85 and $1.90 in cash. Therefore, you participate in

the repurchase according to the dividend payout percentage; you are unaffected.

7. Stock Dividends The market value balance sheet for Outbox Manufacturing is

shown here. Outbox has declared a stock dividend of 25 percent. The stock

goes ex-dividend tomorrow (the chronology for a stock dividend is similar to

that for a cash dividend). There are 20,000 shares of stock outstanding. What

will the ex-dividend price be? Cash $295,000 Debt $180,000 Fixed assets 540,000 Equity 655,000 Total $835,000 Total $835,000

The stock price is the total market value of equity divided by the shares outstanding, so: P0 = $32.75 per share

The shares outstanding will increase by 25 percent, so:

New shares outstanding = 25,000 shares

The new stock price is the market value of equity divided by the new shares outstanding, so: PX = $26.20 Chap 20

1.Rights Offerings Again, Inc., is proposing a rights offering. Presently, there are

550,000 shares outstanding at $87 each. There will be 85,000 new shares offered at $81 each.

a. What is the new market value of the company?

b. How many rights are associated with one of the new shares?

c. What is the ex-rights price?

d. What is the value of a right? lOMoARcPSD|359 747 69

e. Why might a company have a rights offering rather than a general cash offer? a. The new

market value =$54,735,000

b. Number of rights needed = 550,000 shares outstanding/85,000 new shares =6.47 rights per new share c. The new price of the stock (ex-rights price) will be:

PX = $54,735,000/(550,000+ 85,000) = $86.22

d. The value of a right = $87.00 – 86.22 = $0.78

e. A rights offering usually costs less, it protects the proportionate interests of

existingshareholders and also protects against underpricing

2. Rights Offering The Clifford Corporation has announced a rights offer to raise $28

million for a new journal, the Journal of Financial Excess. This journal will review

potential articles after the author pays a nonrefundable reviewing fee of $5,000 per

page. The stock currently sells for $27 per share, and there are 2.9 million shares outstanding.

a. What is the maximum possible subscription price? What is the minimum?

b. If the subscription price is set at $25 per share, how many shares must be sold?

How many rights will it take to buy one share?

c. What is the ex-rights price? What is the value of a right?

d. Show how a shareholder with 1,000 shares before the offering and no desire

(ormoney) to buy additional shares is not harmed by the rights offer.

a. The maximum subscription price is the current stock price, or $27.

The minimum price is anything greater than $0.

b. The number of new shares will bethe amount raised divided by the subscription price,so:

Number of new shares = 1,120,000 shares

Number of rights needed = 2,900,000 shares outstanding/1,120,000 new shares = 2.59 rights per new share

c. The ex-rights price is: PX = (2,900,000x$27 + $28,000,000) / (2,900,000 + 1,120,000)=$26.44

Value of a right =$27 – 26.44 =$0.56

d. Before the rights offer, a shareholder will have the shares owned at the

currentmarketprice, or:

Portfolio value = 1,000 shares x $27 = $27,000

After the rights offer, the share price will fall, but the shareholder will also hold 1,000

rights,so: Portfolio value = (1,000 shares x $26.44) + (1,000 rights x $0.56) = $27,000 3.

Rights Stone Shoe Co. has concluded that additional equity financing will be

needed to expand operations and that the needed funds will be best obtained

through a rights offering. It has correctly determined that as a result of the rights

offering, the share price will fall from $65 to $63.18 ($65 is the “rights-on” price;

$63.18 is the ex-rights price, also known as the when-issued price). The company

is seeking $15 million in additional funds with a per-share subscription price equal

to $50. How many shares are there currently, before the offering? (Assume that the

increment to the market value of the equity equals the gross proceeds from the offering.)

Number of new shares issued = $15,000,000 / $50 = 300,000 shares lOMoARcPSD|359 747 69

Let C be the number of current shares outstanding before the rights offering, we have the

equation of the ex-rights price: PX = (Cx$65 + $15,000,000) / (C +300,000) = $63.18 Solve

for C = 2,172,527 shares

8. Price Dilution Raggio, Inc., has 135,000 shares of stock outstanding. Each share is

worth $75, so the company’s market value of equity is $10,125,000. Suppose the firm

issues 30,000 new shares at the following prices: $75, $70, and $65. What will the

effect be of each of these alternative offering prices on the existing price per share? Chap 21

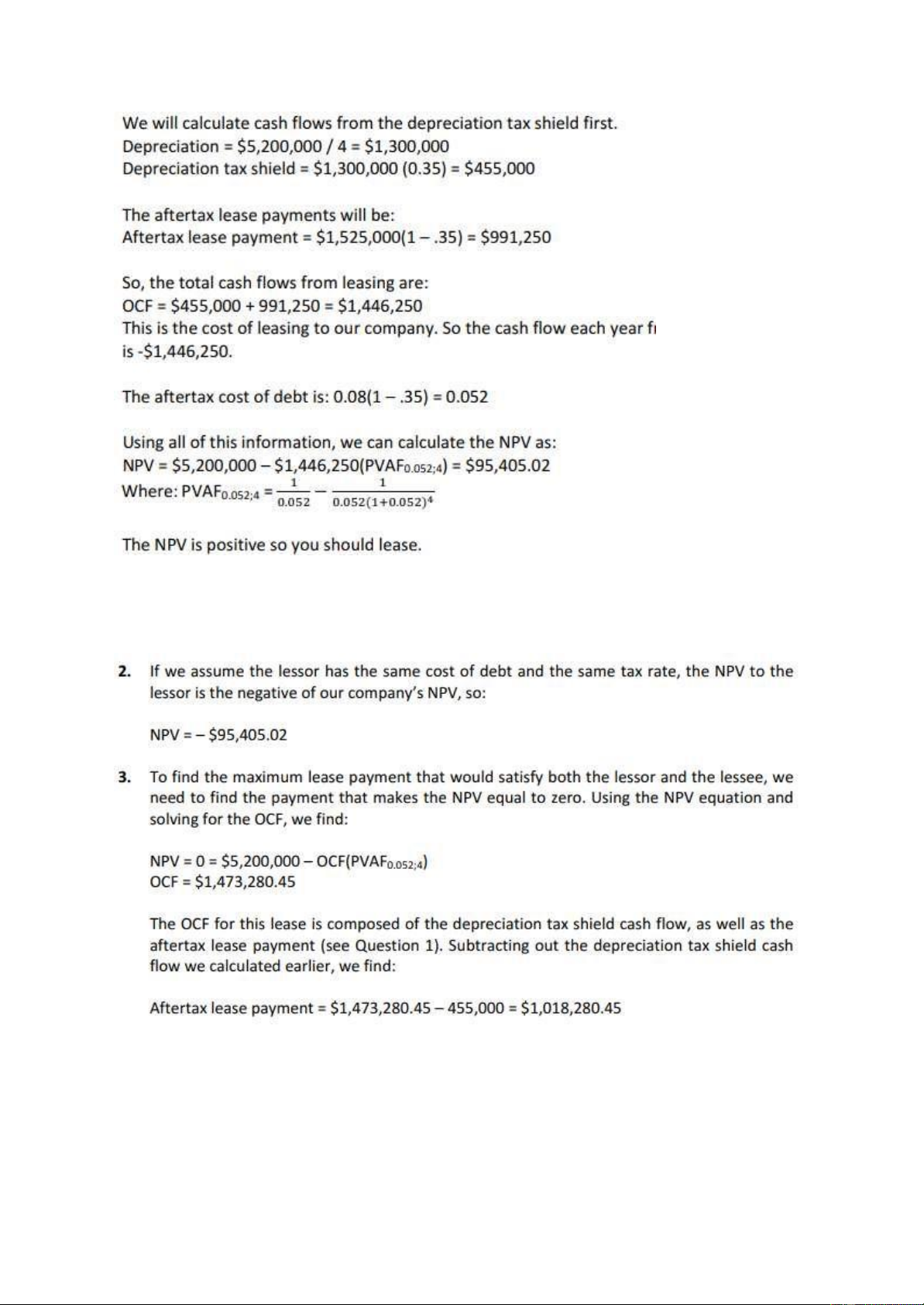

You work for a nuclear research

laboratory that is contemplating leasing a diagnostic scanner (leasing is a common

practice with expensive, high-tech equipment). The scanner costs $5,200,000, and it

would be depreciated straight-line to zero over four years. Because of radiation

contamination, it will actually be completely valueless in four years. You can lease it

for $1,525,000 per year for four years. 1.

Lease or Buy Assume that the tax rate is 35 percent. You can borrow at 8

percentbefore taxes. Should you lease or buy? lOMoARcPSD|359 747 69 2.

Leasing Cash Flows What are the cash flows from the lease from the

lessor’sviewpoint? Assume a 35 percent tax bracket. 3.

Finding the Break-Even Payment What would the lease payment have to be

forboth the lessor and the lessee to be indifferent about the lease? lOMoARcPSD|359 747 69

7. Lease or Buy Super Sonics Entertainment is considering buying a machine that

costs $540,000. The machine will be depreciated over five years by the straight-

line method and will be worthless at that time. The company can lease the machine

with year-end payments of $145,000. The company can issue bonds at a 9 percent

interest rate. If the corporate tax rate is 35 percent, should the company buy or lease? Chap 29

1. Calculating Synergy Evan, Inc., has offered $340 million cash for all of the

common stock in Tanner Corporation. Based on recent market information, Tanner

is worth $317 million as an independent operation. If the merger makes economic

sense for Evan, what is the minimum estimated value of the synergistic benefits from the merger?

7. Cash versus Stock Payment Penn Corp. is analyzing the possible acquisition of

Teller Company. Both firms have no debt. Penn believes the acquisition will increase

its total aftertax annual cash flow by $1.1 million indefinitely. The current market

value of Teller is $45 million, and that of Penn is $62 million. The appropriate

discount rate for the incremental cash flows is 12 percent. Penn is trying to decide

whether it should offer 40 percent of its stock or $48 million in cash to Teller’s shareholders.

a. What is the cost of each alternative?

b. What is the NPV of each alternative?

c. Which alternative should Penn choose?

a. The cash purchase price is the amount of cash offered, $48 million.

Cost/Premium = $48 million - $45 million = $3 million

To calculate the purchase price of the stock offer, we first need to calculate the value of the

target to the acquirer. The value of the target firm to the acquiring firm will be the

market value of the target plus the PV of the incremental cash flows generated by the

target firm. The cash flows are a perpetuity, so

V* = $45,000,000 + $1,100,000/.12 = $54,166,667

The purchase price of the stock offer is the percentage of the acquiring firm given up times

the sum of the market value of the acquiring firm and the value of the target firm to the

acquiring firm. So, the purchase price will be: lOMoARcPSD|359 747 69

Purchase price of stock offer = .40($62,000,000 + 54,166,667) = $46,466,667

Cost/Premium = $46,466,667 - $45 million = $1,466,667 b.

The NPV of each offer is the value of the target firm to the acquiring firm minus

thepurchase price of acquisition, so:

NPV cash = $54,166,667 – 48,000,000 = $6,166,667

NPV stock = $54,166,667 – 46,466,667 = $7,700,000 c.

Since the NPV is greater with the stock offer, the acquisition should be done with

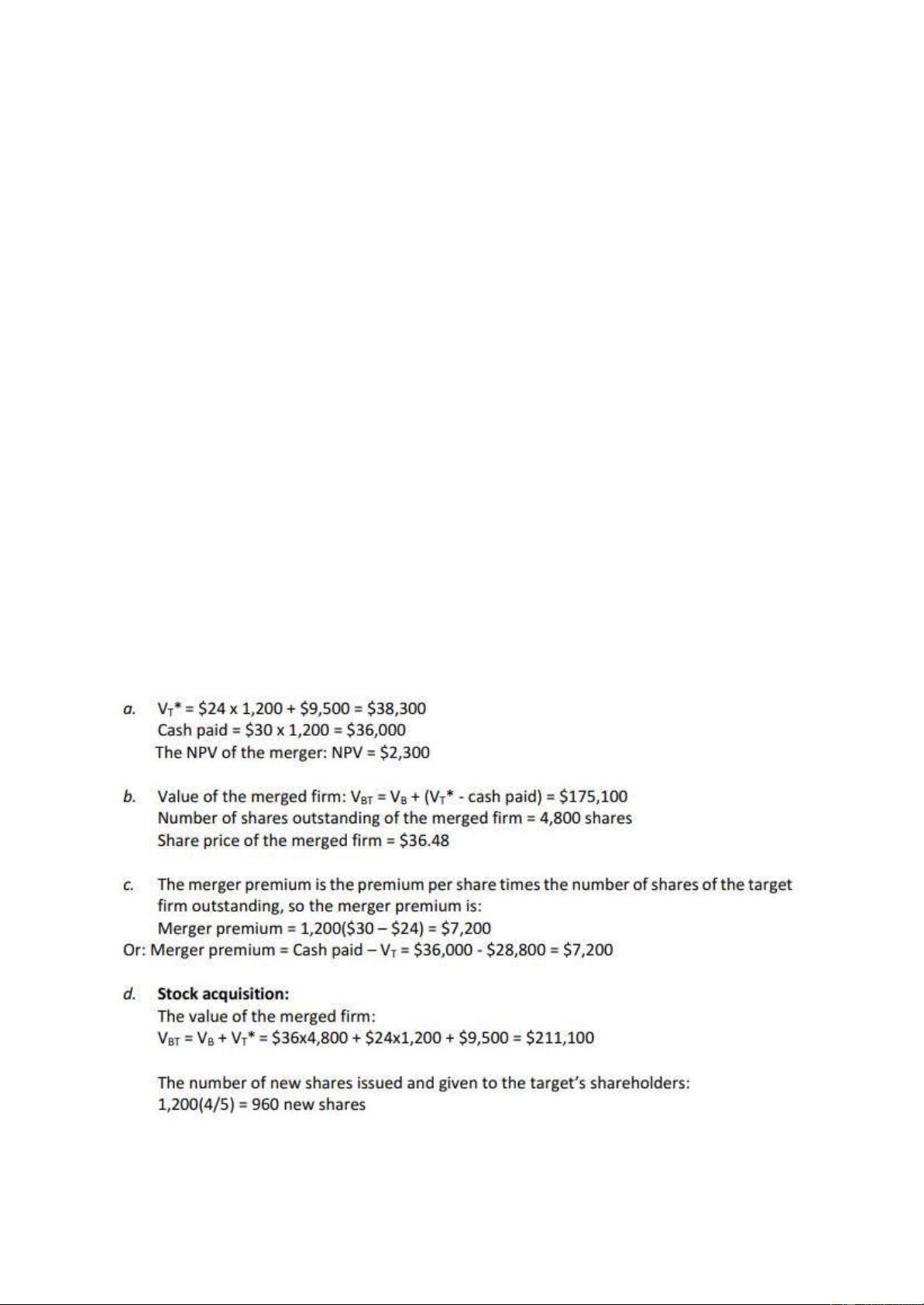

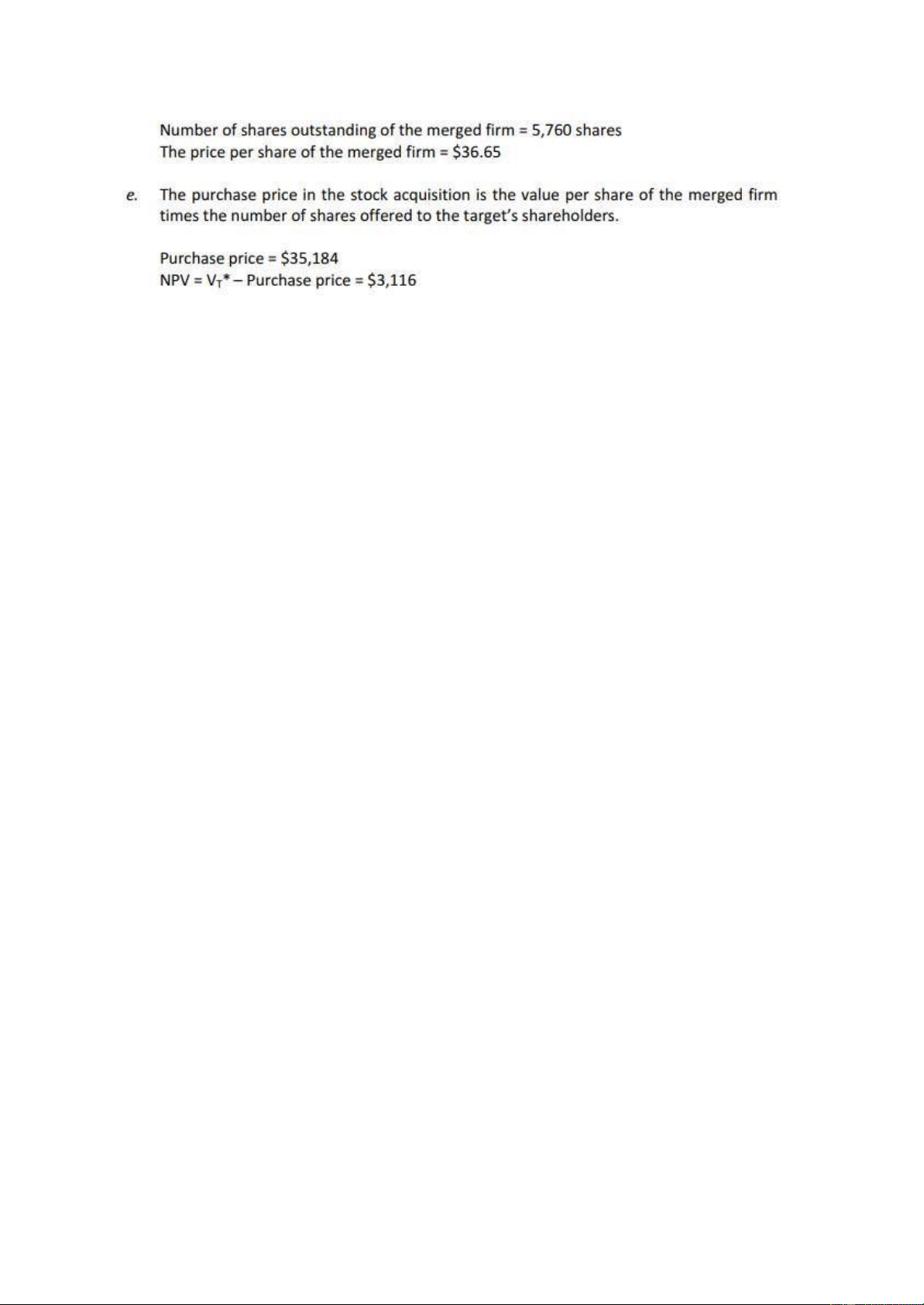

stock.10. Cash versus Stock as Payment Consider the following premerger

information about a bidding firm (Firm B ) and a target firm (Firm T ). Assume that

both firms have no debt outstanding. Firm B Firm T Shares

outstanding 4,800 1,200 Price per share $36 $24

Firm B has estimated that the value of the synergistic benefits from acquiring Firm T is $9,500.

a. If Firm T is willing to be acquired for $30 per share in cash, what is the NPV ofthe merger?

b. What will the price per share of the merged firm be assuming the conditions in (a)?

c. In part (a), what is the merger premium?

d. Suppose Firm T is agreeable to a merger by an exchange of stock. If B offersfour

of its shares for every five of T ’s shares, what will the price per share of the merged firm be?

e. What is the NPV of the merger assuming the conditions in (d)? lOMoARcPSD|359 747 69

Tài liệu liên quan:

-

Đề thi giữa kỳ học phần Statistics for Business năm 2015 | Trường Đại học Quốc tế, Đại học Quốc gia Thành phố Hồ Chí Minh

341 171 -

Đề thi giữa kỳ học phần Statistics for Business có đáp án | Trường Đại học Quốc tế, Đại học Quốc gia Thành phố Hồ Chí Minh

410 205 -

Đề thi giữa kỳ học phần Statistics for Business năm 2019 | Trường Đại học Quốc tế, Đại học Quốc gia Thành phố Hồ Chí Minh

292 146 -

Đề thi giữa kỳ học phần Statistics for Business | Trường Đại học Quốc tế, Đại học Quốc gia Thành phố Hồ Chí Minh

304 152 -

Bài tập tiểu luận nhóm học phần Statistics for Business | Trường Đại học Quốc tế, Đại học Quốc gia Thành phố Hồ Chí Minh

307 154