Chapter 14: Basic Elements Of Control And Management Strategies môn Principles of Management | Trường Đại học Quốc tế, Đại học Quốc gia Thành phố Hồ Chí Minh

The regulation of organizational activities to ensure that goals are achieved effectively. Helps keep performance within acceptable limits. Tài liệu giúp bạn tham khảo, ôn tập và đạt kết quả cao. Mời đọc đón xem!

Môn: Principles of Management 314 tài liệu

Trường: Trường Đại học Quốc tế, Đại học Quốc gia Thành phố Hồ Chí Minh 2 K tài liệu

Tác giả:

Preview text:

CHAPTER 14: BASIC ELEMENTS OF CONTROL

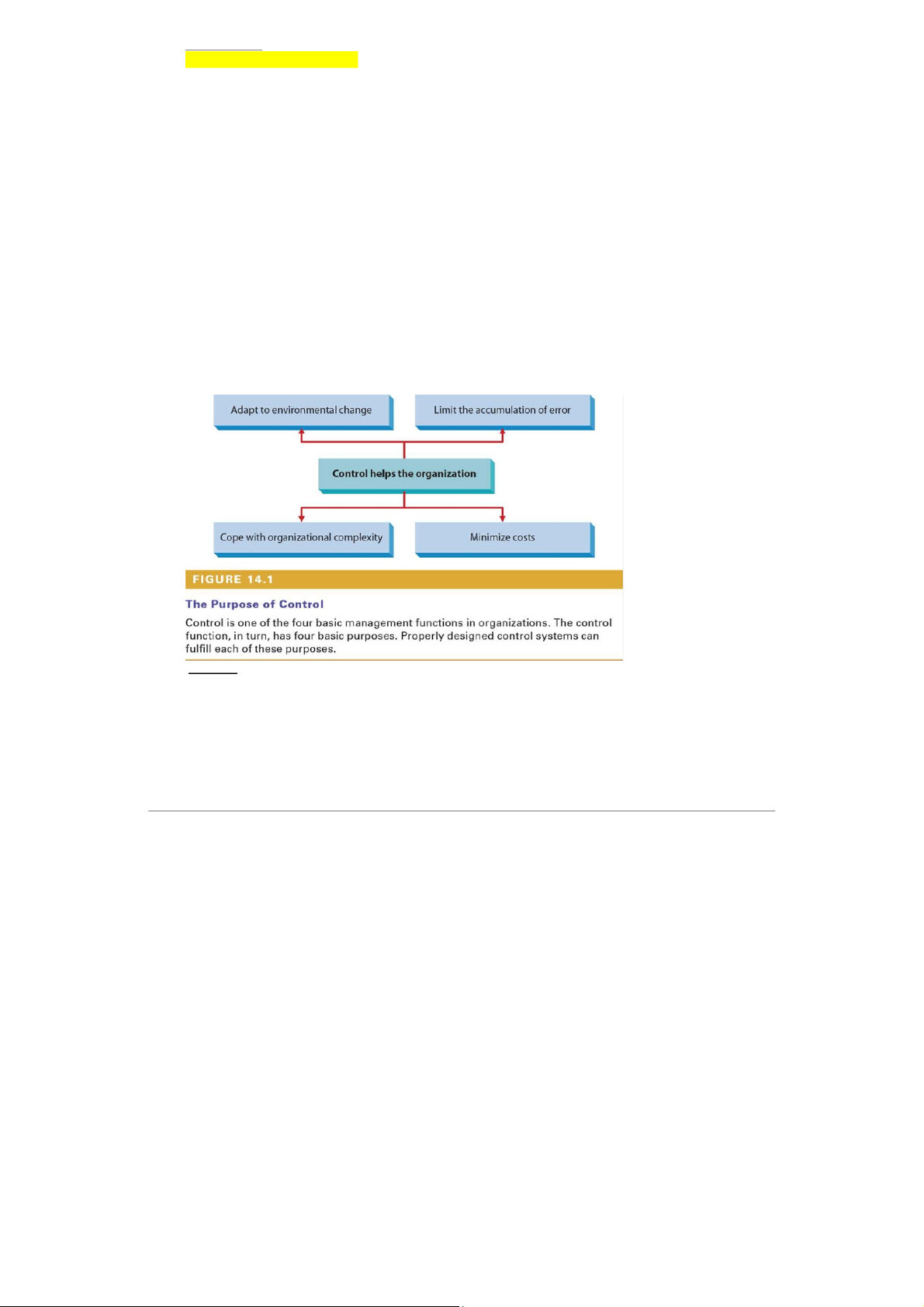

14-1a The Purpose of Control 1. Concept Control:

The regulation of organizational activities to ensure that goals are achieved effectively.

Helps keep performance within acceptable limits.

2. Purposes of Control

1. Provide indications of performance:

Helps the organization understand how well it is achieving its goals.

Example: Company tracks monthly sales to see if targets are met.

2. Provide a mechanism for adjustment:

When performance is below target, control allows plans, processes, or actions to be adjusted course.

Example: If sales drop, company may increase marketing, improve products, or train sales sta

3. Real-life Example

Apple Inc.: Monitors iPhone product development progress, cost, and deadlines. If issues arise,

adjust schedule, personnel, and processes to ensure on-time, high-quality product launch.

4. Benefits / Drawbacks Benefits:

oEnsures the organization stays on course and achieves goals.

oDetects problems early, reducing failure risk.

oImproves resource and workforce efficiency.

Drawbacks / Risks:

oExcessive control → reduces creativity and employee motivation.

oControl costs can be high if too complex or repetitive.

Example: Control helps organizations operate effectively in a constantly changing environment. Th

McDonald’s clearly illustrates this role.

As customer preferences shift toward healthier food options, McDonald’s uses control systems to

data and customer feedback. This allows the company to adjust its menu in a timely manner, environmental change.

At the same time, McDonald’s enforces strict quality control procedures in food preparation and

errors are detected early at the store level, which helps limit the accumulation of errors that could global brand.

With tens of thousands of restaurants worldwide, operations would become chaotic without effectiv

Through standardized procedures and centralized reporting, McDonald’s is able to cope with organiza complexity.

Finally, by controlling inventory, raw material usage, and labor costs, McDonald’s reduces waste

minimizes operating costs, improving overall efficiency.

👉 Therefore, control enables McDonald’s to respond to change, maintain quality, manage complexity,

and control costs.

14-1b Types of Control

1. General Concept

Types of Control:

Control is applied based on the types of resources an organization uses and the levels within the organizational system.

Goal: ensure resources are used efficiently and organizational strategies stay on track.

2. Control by Resource Type

1. Physical resources:

Examples: inventory management, quality control, equipment control.

Real-life: VinFast manages inventory of components to ensure assembly lines run smoothly.

2. Human resources:

Examples: selection, training, performance appraisal, compensation.

Real-life: Google conducts 360-degree evaluations to improve employee performance and reward appropriately.

3. Information resources:

Examples: sales forecasts, environmental analysis, PR, production scheduling, economic forecasting

Real-life: Amazon uses sales data analysis to forecast inventory and plan shipping.

4. Financial resources:

Examples: managing capital, cash flow, collections and payments.

Real-life: Vietcombank monitors cash flow and capital to maintain banking stability.

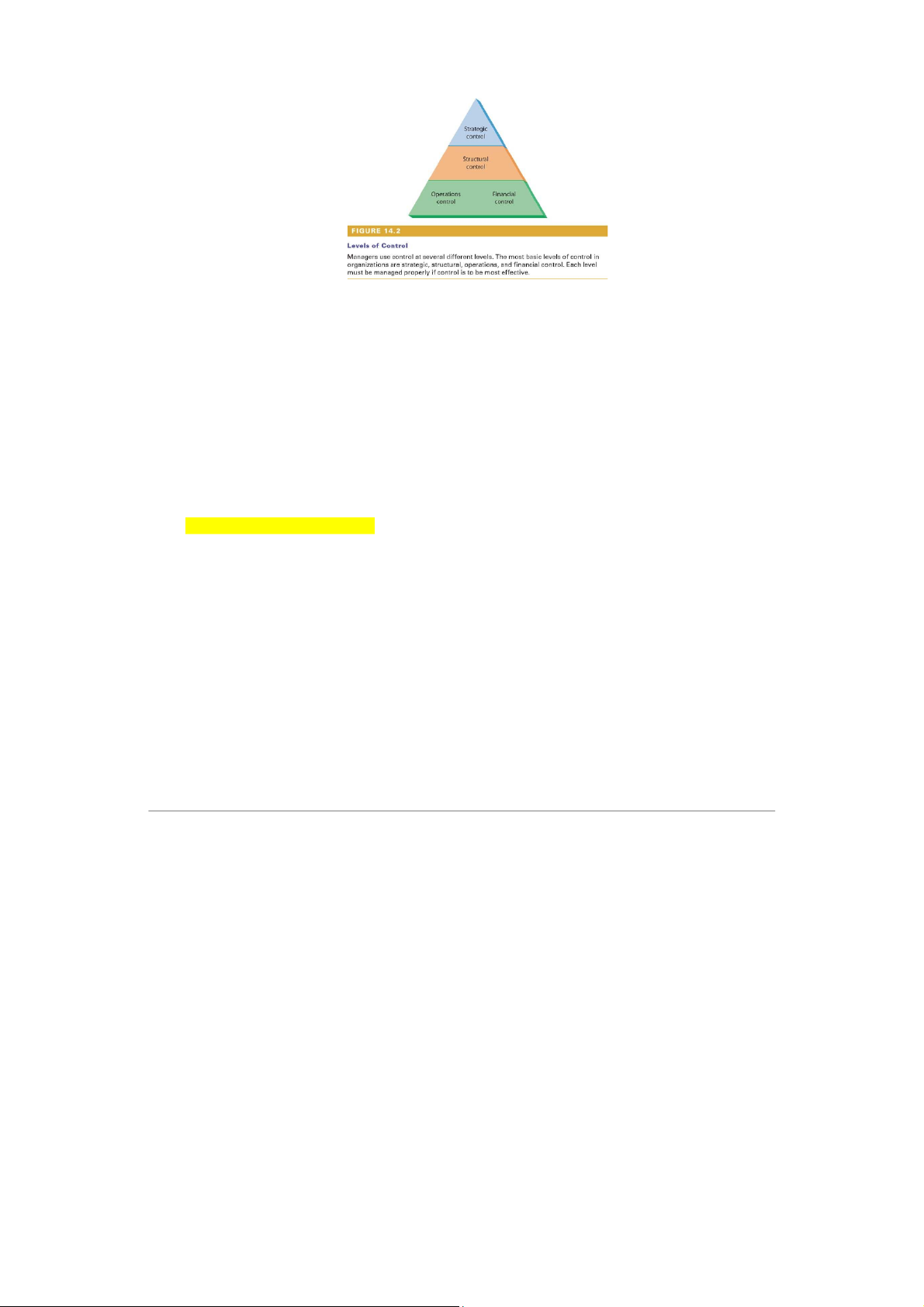

3. Control by Organizational Level

1. Operations control: Focuses on processes that transform resources into products/services.

2. Financial control: Concerned with financial resources.

3. Structural control: Ensures organization units and structure serve intended purposes.

4. Strategic control: Monitors effectiveness of strategies in achieving organizational goals.

Real-life: PepsiCo evaluates its Asian market expansion strategy to adjust business plans.

4. Benefits / Drawbacks Benefits:

oEnsures efficient resource use and smooth operations.

oDetects problems early and allows strategic adjustments.

oIncreases likelihood of achieving organizational goals. Drawbacks:

oExcessive control → reduces creativity, increases cost, slows decision-making.

oImproper control → wastes resources or confuses employees.

Which type of control helps the organization transform resources such as raw materials into products or

services that are then sold in the market? A. Operations B. Financial C. Structural D. Strategic

Operations control

Operations control focuses on the processes that the organization uses to transform resources into products or

services. This includes quality control, production, and other aspects of converting raw materials into goods and services.

Example of levels of control at Starbucks: Strategic control:

Starbucks’ top management regularly evaluates its international expansion strategy to ensure

with long-term vision, sustainable growth, and competitive advantage. Key performance indica

as market share, brand recognition, and customer satisfaction are used to assess strategic e Structural control:

Starbucks adopts a regional and functional organizational structure (e.g., North America, Euro

marketing, operations, finance). Structural control ensures clear authority and responsibility, im

coordination and decision-making across the organization. Operations control:

At the store level, managers closely monitor daily operations, including beverage preparation

procedures, service standards, and food safety. Standard operating procedures (SOPs) are imp

to maintain consistent quality across all stores. Financial control:

Starbucks tracks revenues, operating costs, and profits of each store and compares them w

approved budget. Financial control helps identify cost overruns and ensures efficient use of

14.1b Responsibilities of Control

1. General Concept

Responsibilities of Control:

Control is not just a system; it is the responsibility of people in the organization, especially man

and relevant employees.

Goal: ensure resources and organizational activities are effective and goal-oriented.

2. Specific Roles 1. Managers:

Accountable for control activities within their authority.

Involved in monitoring, evaluating, and adjusting performance.

Example: Production manager at Samsung monitors phone production progress to meet targets quality standards. 2. Controller:

A position that assists line managers in control activities.

Focuses on finance, reporting, and data analysis.

Example: Chief accountant at Vinamilk tracks production costs and alerts if spending exceeds 3. Operating employees:

Help maintain effective control at the operational level.

Resolve quality issues and monitor production processes.

Example: Toyota assembly line employees detect product defects promptly and report them for correction.

3. Benefits / Drawbacks Benefits:

oEnsures coordination across organizational levels in control.

oHelps detect problems early and improve efficiency.

oEnsures organizational goals are . achieved

Drawbacks / Risks:

oIf managers or employees neglect responsibility → control fails, wasting resources.

oOver-reliance on one position (e.g., Controller) → operational issues may be overlooked

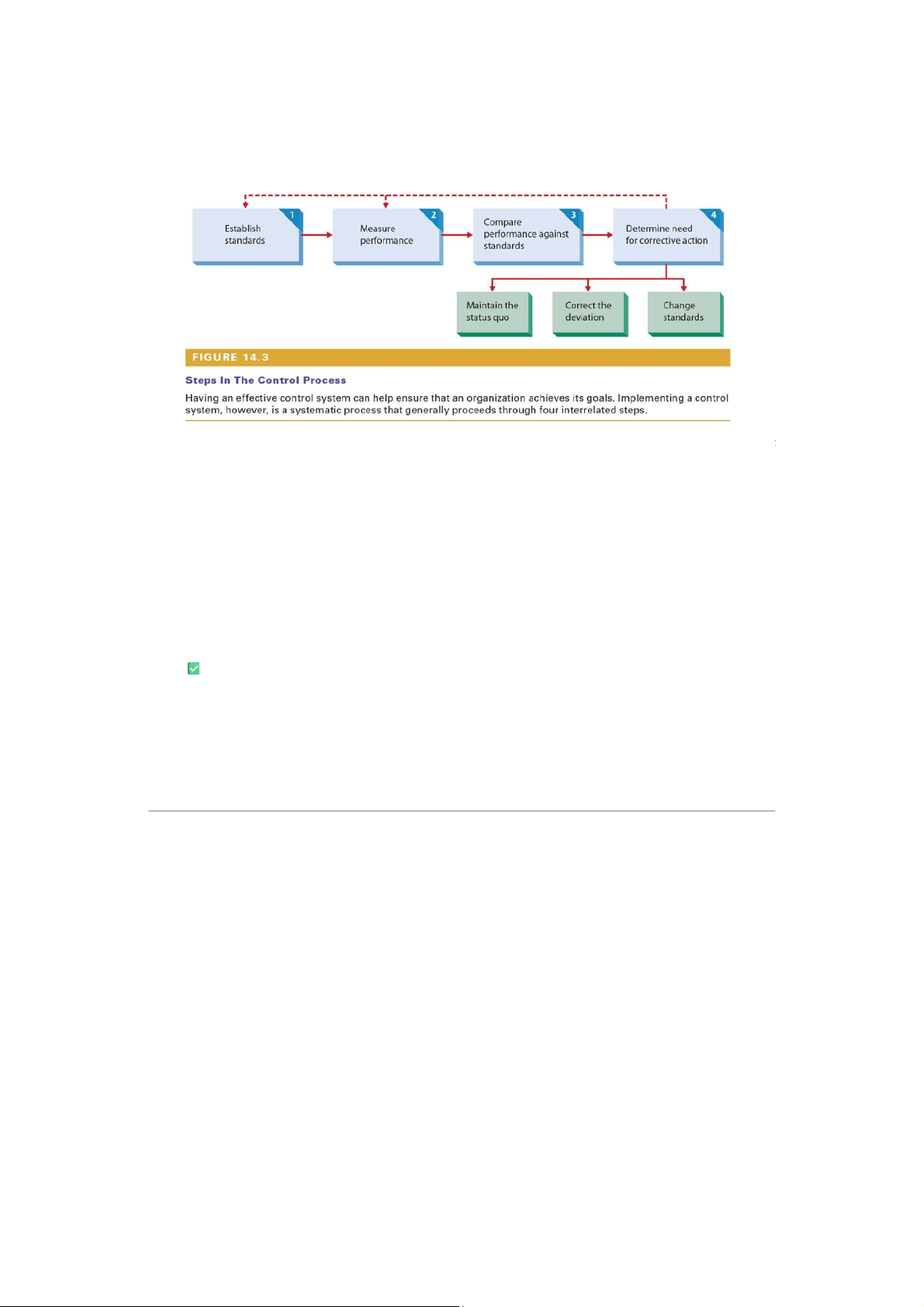

Figure 14.3 illustrates four main steps in the control process, which help organizations ensure that their

are achieved. This process can be illustrated using ABC Manufacturing Company.

Step 1: Establish standards

First, the organization sets standards that serve as benchmarks for performance evaluation.

Example: ABC Manufacturing sets a standard of producing 10,000 units per month with a de below 2%.

Step 2: Measure performance

Next, the company measures actual performance.

Example: ABC records the actual number of units produced and the defect rate each mon

Step 3: Compare performance against standards

Actual performance is compared with the established standards to identify deviations.

Example: ABC finds that production is only 9,000 units with a defect rate of 3%.

Step 4: Determine the need for corrective action

Based on the comparison, managers may maintain the status quo, correct deviations, or ch standards.

Example: ABC decides to retrain workers and improve the production process to correct th

✅ Concluding sentence

In conclusion, the control process enables organizations to monitor performance, identify deviations,

corrective actions to ensure organizational objectives are met.

Example of the control process at Toyota Motor Corporation: 1. Establish standards:

Toyota establishes standards for product quality, safety, production cost, and productivity base

Toyota Production System (TPS). 2. Measure performance:

Actual performance is measured using indicators such as defect rates, production cycle time unit, and process compliance.

3. Compare performance against standards:

Actual results are compared with established standards to identify deviations in quality, cost

4. Determine need for corrective action:

When deviations occur, Toyota implements continuous improvement (Kaizen), adjusts production

processes, or revises standards to enhance long-term performance. Conclusion:

This control process enables Toyota to maintain high quality, minimize waste, and achieve sustain competitive advantage.

14-1c Steps in the Control Process

1. General Concept Control Process:

A process of monitoring and adjusting organizational activities to ensure goals are achieved effectively.

Includes 4 basic steps: establishing standards, measuring performance, comparing against standards,

and considering corrective action.

2. Steps in the Control Process

Step 1: Establishing standards Control standard:

oA target for comparing subsequent performance.

oMust be measurable, consistent with organizational goals, and have identifiable performance indicators.

Example: VinMart sets a sales target of 100,000 products/month.

Step 2: Measuring performance

Must be an ongoing process.

Performance measures must be valid indicators of performance.

Example: Toyota records daily defective products to evaluate quality.

Step 3: Comparing performance against standards

Define permissible deviation from the standard.

Use an appropriate timetable for measurement.

Example: If defective products exceed 5% → alert is triggered.

Step 4: Considering corrective action Options:

1. Do nothing if deviation is minor.

2. Correct the deviation to meet standards.

3. Change the standard if initially set too high or low.

Example: Apple adjusts iPhone assembly process if defects exceed acceptable level; or change

standard if new technology allows better production.

3. Benefits / Drawbacks Benefits:

oEnables continuous performance monitoring.

oDetects problems early for timely adjustments.

oEnsures activities and organizational goals stay on track. Drawbacks:

oUnrealistic or rigid standards → reduces creativity, increases employee stress.

oExcessive measurement/control → costly and time-consuming.

Why is the control of financial resources considered to be the most important area of control? How might a

controller support this function at various levels of the organization?

1. Why is financial control the most important?

Financial resources are the backbone of all organizational activities:

oPoor financial management → other resources (physical, human, information) cannot operate effectively.

oExample: VinFast without cash flow cannot buy components, pay salaries, operate assem lines → operations halt.

Finance directly affects decision-making:

oEvery strategy, plan, and investment depends on budget and cash flow control.

Prevents legal risks and bankruptcy:

oGood financial control ensures tax compliance, debt repayment on time, avoiding legal issues.

2. Role of the Controller

Controller supports managers in all financial control activities, at all levels. 1. Strategic level:

Analyze long-term cash flow, profitability, and investment ,

costs providing data for leadership decisions.

Example: Vinamilk controller analyzes new factory project profitability for CEO decision. 2. Operational level:

Monitor daily expenses, income, department budget, ensuring operations stay within limits.

Example: Samsung factory controller tracks production and material costs, reporting to plant m

3. Tactical / Management level:

Assist departments in budgeting, forecasting, and cost analysis, aligning department goals with organizational objectives.

Example: Controller helps marketing department plan an advertising budget within limits.

3. Benefits / Drawbacks Benefits:

oEnsures efficient organizational operations, avoids waste.

oEnables timely and accurate decision-making.

oPrevents bankruptcy, bad debt, and legal issues.

Drawbacks / Risks:

oExcessive financial control → employees feel micromanaged, creativity reduced.

oOver-reliance on controller → wrong or incomplete information can lead to poor financial decisions.

14-2 Operations Control

1. General Concept Operations Control:

Focuses on the processes an organization uses to transform resources into products or services.

Goal: ensure the transformation process is efficient, produces quality outputs, and meets deadlines.

2. Types of Operations Control

a) Preliminary control

Monitors financial, physical, human, and information resources before they become part of the system.

Example: VinFast checks components before assembly to avoid production errors.

Benefits: Prevents errors early, saves cost.

Drawbacks: Too strict → costly, slows progress.

b) Screening control

Relies on feedback during the transformation process.

Encourages employee participation and early problem detection.

Example: Toyota uses the Andon system: employees signal defects immediately during assembly.

Benefits: Early error detection, increases employee responsibility, improves quality.

Drawbacks: Slow or no feedback → reduced effectiveness.

c) Postaction control

Monitors outputs or results after the transformation process is complete.

Example: Vinamilk checks milk quality before packaging and distribution.

Benefits: Ensures final product meets standards, enhances organizational reputation.

Drawbacks: Late detection → high correction costs, customer impact.

Example of forms of operations control at Toyota Motor Corporation:

Toyota applies operations control throughout the entire production system based on the Input –

Transformation – Output model, supported by continuous feedback. Preliminary control:

Toyota tightly controls inputs such as raw materials, equipment, and workforce skills. Suppl

meet strict quality standards, and employees receive extensive training before entering the p

process. The goal is to prevent problems before they occur. Screening control:

During the transformation process, Toyota monitors how inputs are converted into outputs th

Toyota Production System (TPS). Tools such as Just-in-Time and Kaizen enable real-time d correction of deviations. Postaction control:

After production, finished vehicles are inspected for quality, safety, and reliability before be

delivered to the market. Customer feedback is then used to improve future products and standards. Conclusion:

By integrating all three forms of operations control, Toyota ensures consistent quality, operational

and long-term competitive advantage.

Which type of operations control focuses on the quality and quantity of resources such as financial,

material, human, and information? A. Preliminary B. Screening C. Postactional a. Preliminary

Preliminary control concentrates on the resources—financial, material, human, and information—the

organization brings in from the environment. Preliminary control attempts to monitor the quality or quantity of

these resources before they enter the organization.

14-3 Financial Control Financial Control:

Focuses on the organization’s financial resources, including revenues, shareholder investments, wo

capital, retained earnings, and expenses.

Goal: ensure proper cash flow, prevent waste, comply with laws, and support strategic decisio

2. Financial Flows Controlled 1. Inflows:

Includes sales revenue, shareholder investment, loans, and other funding.

Example: VinFast receives shareholder investment to expand electric car production.

2. Held within the organization:

Includes working capital and retained earnings used for operations and growth.

Example: Vinamilk retains profits to reinvest in new factories or product research. 3. Outflows:

Includes operating expenses, salaries, raw materials, debt payments.

Example: Samsung pays monthly for materials and employee salaries.

3. Role of the Controller

Supports managers at all levels to monitor cash flows, analyze costs, forecast finances, and e compliance.

Example: Vinamilk controller tracks production costs and reports to management to increase productivity within budget.

4. Benefits / Drawbacks Benefits:

oEnsures proper cash flow, avoids waste, and supports accurate decision-making.

oPrevents bankruptcy, bad debt, and legal violations.

oSupports efficiency and sustainable growth.

Drawbacks / Risks:

oExcessive focus on finance → employees feel micromanaged, creativity reduced.

oErrors by controller → poor financial decisions, affecting the whole organization.

14-3a Budgetary Control 1. Concept Budgets:

A plan expressed in numerical terms.

Can be established at any organizational level.

Typically for one year or less, but can be shorter.

Can be expressed in financial terms, units of output, or other quantifiable factors.

2. Purposes of Budgets

1. Coordinate resources and projects:

Helps departments allocate human, material, and financial resources efficiently.

Example: VinFast creates a budget for a new electric car project, allocating costs for materi and marketing.

2. Define control standards:

Budget provides benchmarks to evaluate performance.

Example: Production costs exceeding budget by 5% → need for adjustment or investigation.

3. Provide guidance on resources and expectations:

Helps departments know limits for quantity, quality, and costs.

Example: Vinamilk Marketing Department knows the advertising budget for each campaign.

4. Evaluate managerial and unit performance:

Compare actual results with budgeted plans to assess management capability.

Example: Samsung controller compares actual vs. budgeted factory expenses to evaluate product manager.

3. Benefits / Drawbacks Benefits:

oFacilitates planning and effective control, increases transparency.

oSupports strategic decision-making and efficient resource allocation.

oMakes it easy to assess departmental and managerial performance.

Drawbacks / Risks:

oToo rigid → employees feel over-controlled, reduces creativity.

oIncorrect budget forecast → poor decisions, resource waste. Question:

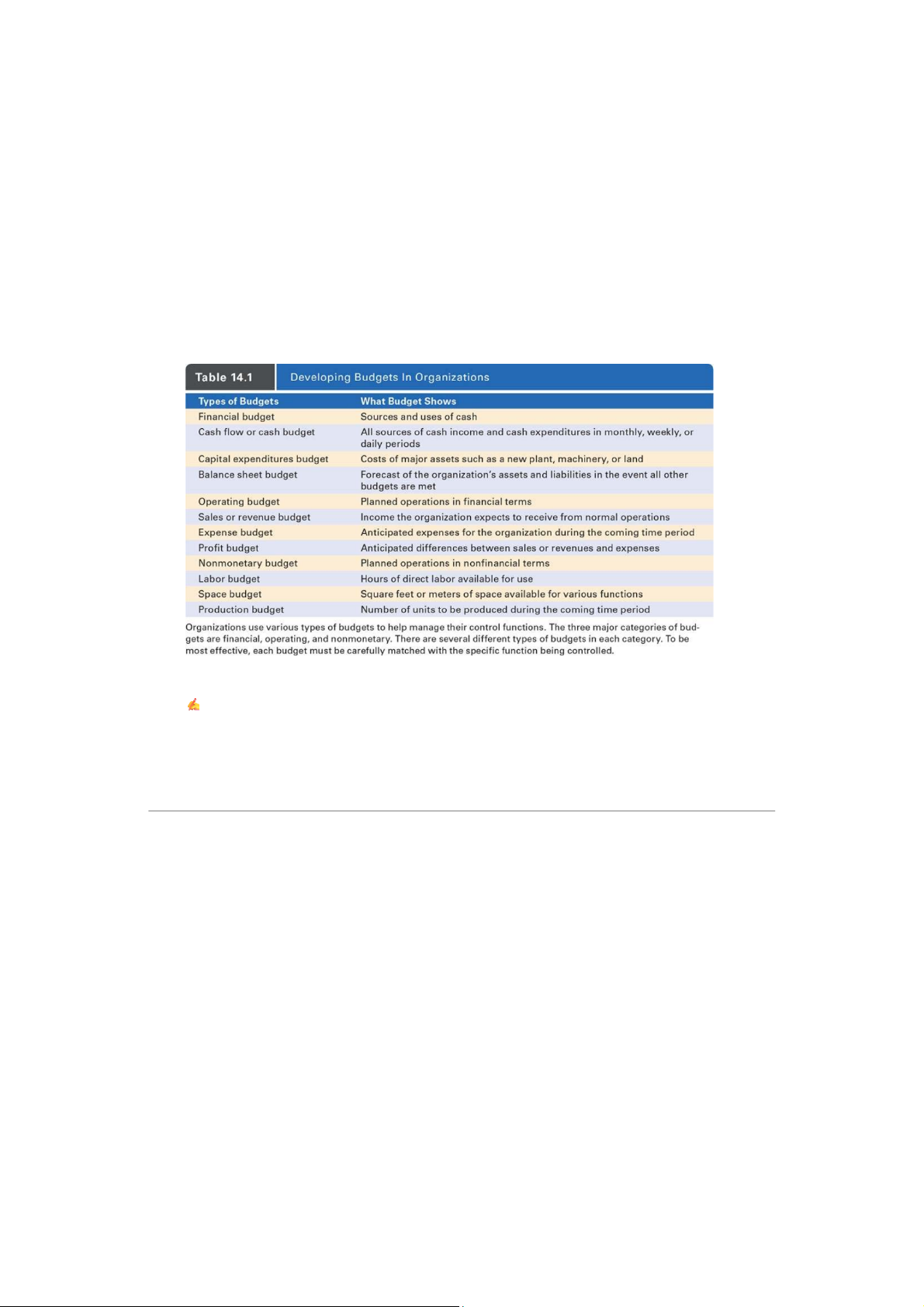

Based on the table “Developing Budgets in Organizations”, explain the different types of budgets used

organization. Use ABC Manufacturing Company as an example to clearly illustrate each type of bu

✍ SAMPLE ANSWER (EXAM-READY)

ABC Manufacturing is a company that specializes in producing and selling household appliances.

manage its operations effectively, the company uses various types of budgets, including financial, and nonmonetary budgets.

1. Financial Budget

A financial budget shows the sources and uses of cash in the organization.

→ For example, ABC Manufacturing prepares a financial budget to plan cash inflows from sale

loans, as well as cash outflows for production and operating costs.

2. Cash Flow (Cash) Budget

This budget shows all sources of cash income and cash expenditures over a specific period such as m or yearly.

→ For instance, ABC Manufacturing expects to receive $5 million from sales each month and

on raw materials, salaries, and utilities.

3. Capital Expenditures Budget

A capital expenditures budget focuses on the costs of major assets such as machinery, land, or ne

→ For example, ABC Manufacturing plans to invest $10 million in new production equipment.

4. Balance Sheet Budget

This budget provides a forecast of the company’s assets and liabilities if all other budgets are achieve

→ For example, ABC Manufacturing estimates total assets of $50 million and total liabilities of the end of the year.

5. Operating Budget

An operating budget presents planned operations in financial terms.

→ For example, ABC Manufacturing prepares an operating budget that includes production, marke administrative expenses.

6. Sales (Revenue) Budget

The sales or revenue budget shows the income the organization expects to earn from normal operations.

→ For instance, ABC Manufacturing expects to sell 100,000 units and earn $60 million in rev

7. Expense Budget

An expense budget estimates the anticipated expenses during the coming period.

→ For example, ABC Manufacturing forecasts expenses of $40 million for materials, labor, and 8. Profit Budget

A profit budget shows the expected difference between revenues and expenses.

→ For example, ABC Manufacturing anticipates a profit of $20 million based on expected reven

million and expenses of $40 million.

9. Nonmonetary Budget

A nonmonetary budget outlines planned operations in nonfinancial terms.

→ For example, ABC Manufacturing sets goals to improve product quality and customer satisfact 10. Labor Budget

A labor budget shows the number of direct labor hours available for use.

→ For example, ABC Manufacturing estimates that 50,000 direct labor hours will be required in 11. Space Budget

A space budget identifies the amount of space available for various functions.

→ For example, ABC Manufacturing allocates 3,000 square meters for production and 500 square office use.

12. Production Budget

A production budget shows the number of units to be produced during a specific period.

→ For example, ABC Manufacturing plans to produce 120,000 units to meet customer demand.

✅ CONCLUSION (OPTIONAL IN EXAM)

In conclusion, using different types of budgets helps ABC Manufacturing effectively control financ

resources, operations, and organizational planning, leading to better overall performance.

14-3a Types of Budgets

a) Financial budget

Indicates where the organization will get cash and how it will be used.

Example: VinFast financial budget for expanding production includes shareholder capital, bank l

raw material costs, salaries, and marketing expenses.

Benefits: Controls cash flow, prevents shortages, ensures smooth operations.

Drawbacks: Incorrect cash flow forecast → shortage or waste.

b) Operating budget

Outlines the quantities of products or services the organization intends to create and the reso needed.

Example: Vinamilk operating budget for milk production: planned milk quantity, raw materials, labor, and machine hours.

Benefits: Enables efficient production planning and resource allocation.

Drawbacks: Inaccurate forecast → underproduction or overproduction.

c) Nonmonetary budget

Includes units of output, direct labor hours, machine hours.

Most commonly used at lower organizational levels for daily operational control.

Example: VinFast production department nonmonetary budget: 1000 direct labor hours, 500 mac hours for next month.

Benefits: Enables detailed management and performance tracking.

Drawbacks: Does not include money, difficult to evaluate total costs without financial budget.

14-3a Developing Budgets

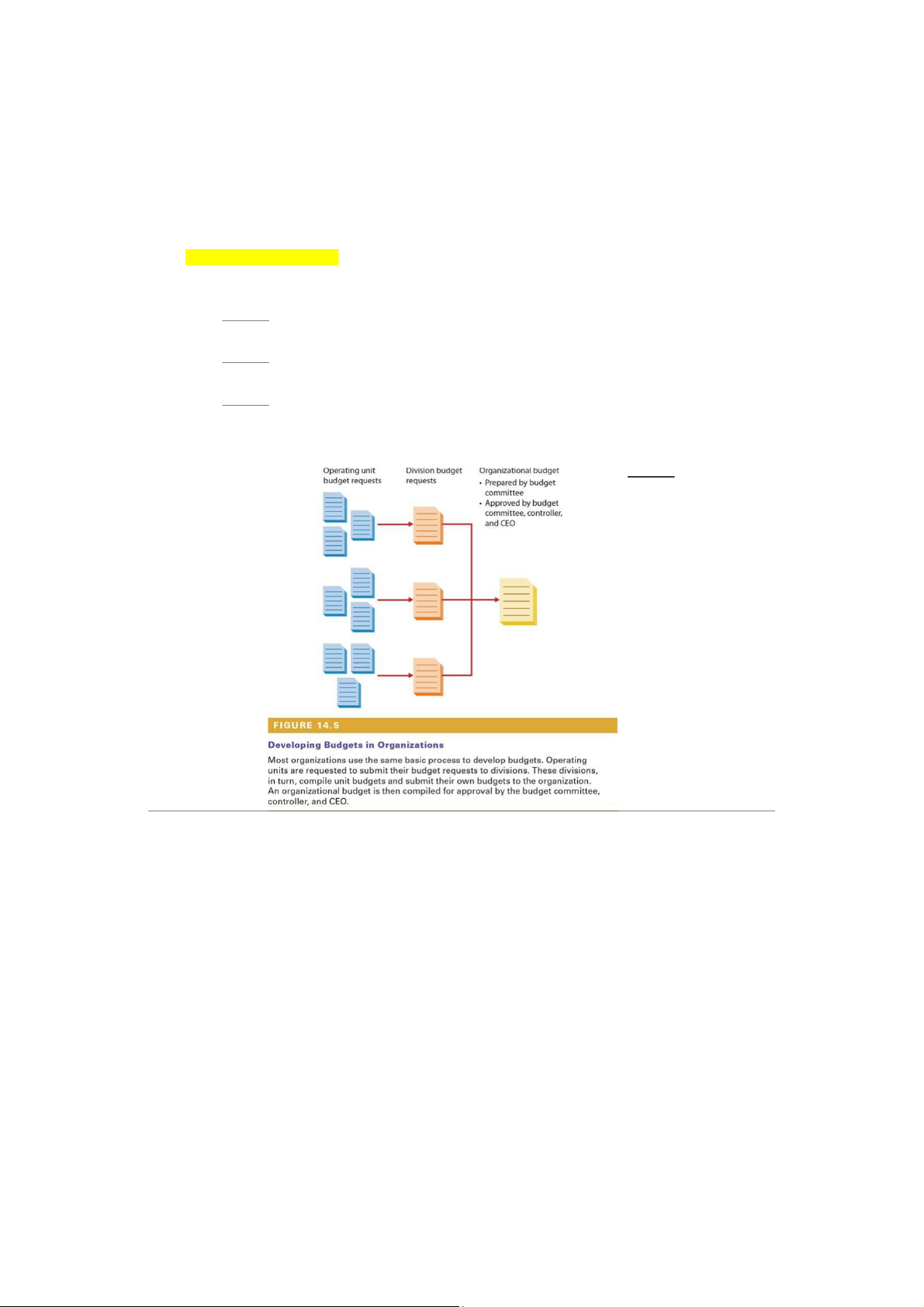

1. Budgeting Process

1. Top management issues a call for budget requests

All departments are asked to prepare budget plans for the coming year. Example:

VinFast requests all departments to submit budgets for production, marketing, and R

2. Operating units submit requests to division head

Each department outlines costs, manpower needs, and materials. Example:

Vinamilk Marketing submits advertising and event costs to department head.

3. Division head integrates and consolidates into overall division budget

Ensures no duplication or omission between departments. Example:

VinFast production division head consolidates budgets from all assembly plants.

4. Forward to budget committee (usually top managers) Roles:

oCorrect duplications and inconsistencies.

oReview and agree on overall budget. Example: VinFast CEO, controller, and division directors approve the consolidated budget. 2. Benefits / Drawbacks Benefits: oBu allocation. oIn oH udget.

Drawbacks / Risks: oLo oPo dget. Question:

Based on Figure 14.5 “Developing Budgets in Organizations”, explain the budget development process

organization. Illustrate your answer using a specific company example.

✍SAMPLE ANSWER (EXAM-READY)

Figure 14.5 illustrates the basic process used by organizations to develop budgets. This process

operating units, divisions, and top management.

First, operating units prepare and submit their operating unit budget requests. These requests include

estimates of expenses, labor needs, and operational requirements.

→ For example, in ABC Manufacturing, the production department submits a budget request cover

materials, labor hours, and equipment maintenance costs.

Second, these requests are sent to the division level, where managers review and combine them

budget requests. At this stage, unnecessary costs may be reduced and priorities are aligned with goals.

→ For instance, the manufacturing division at ABC Manufacturing consolidates budget requests fro

production, quality control, and logistics departments.

Next, the division budgets are forwarded to top management to form the organizational . budget T

represents the overall financial plan of the company.

→ In ABC Manufacturing, the organizational budget is compiled by the budget committee.

Finally, the organizational budget must be approved by the budget committee, the controller, and the CEO

before it is implemented. This ensures that the budget supports the company’s strategic objectives constraints.

✅ CONCLUSION (OPTIONAL IN EXAM)

In conclusion, the budget development process is a bottom-up approach that begins with operating

ends with top management approval. This process helps organizations coordinate activities, control achieve organizational goals.

14-3a Strengths and Weaknesses of Budgeting

Strengths of Budgets

1. Facilitate effective operational control

Budgets provide benchmarks to compare actual performance with plans, helping departments

control costs, manpower, and materials.

Example: VinFast compares actual production costs with the planned budget to avoid overspen

2. Facilitate coordination and communication between departments

Budgeting requires departments to discuss needs and plans, improving coordination.

Example: Vinamilk Marketing and Production coordinate the advertising budget based on produc capacity.

3. Establish records of organizational performance, aiding planning

Budgets create historical data on costs and outputs, supporting next year’s planning.

Example: Samsung uses last year’s budget to forecast labor and material costs for the next

Weaknesses of Budgets

1. Can hamper operations if applied too rigidly

Employees must follow the budget strictly, limiting flexibility in changing situations.

Example: VinFast faces rising material costs but cannot adjust production because the budget

2. Time-consuming to develop

Collecting data, consolidating, and approving budgets takes time.

Example: Vinamilk takes several months to prepare the budget from departments to CEO app

3. Can limit innovation and change

Highly detailed budgets may discourage employees from experimenting or adjusting processes.

Example: Samsung delays production line improvements because the initial budget did not acc innovation.

14-3b Other Tools for Financial Control

1. General Concept Financial statement:

A profile of some aspect of an organization’s financial circumstances.

Helps managers, investors, banks, and stakeholders assess the organization’s financial status.

2. Types of Financial Statements a) Balance sheet

Lists an organization’s assets and liabilities at a specific point in time. Example:

VinFast on 31/12/2025: total assets 50,000 billion VND, liabilities 20,000 billion VN equity 30,000 billion VND.

Benefits: Shows financial position at that moment, helps manage cash and assets.

Drawbacks: Only reflects a specific point in time, not trends.

b) Income statement

Summarizes financial performance over a period of time, usually one year.

Includes revenues, expenses, and profit.

Example: Vinamilk 2025: revenue 60,000 billion VND, expenses 45,000 billion VND → profit billion VND.

Benefits: Shows whether the company is performing efficiently, supports strategic decisions.

Drawbacks: Does not show assets and liabilities at a moment, so must be used with the b

Where could a manager find information about financial performance for the past six months? A. Balance sheet

B. Income statement

C. Ration analysis

D. Audit records

B. Income statement

Whereas the balance sheet reflects a snapshot profile of an organization’s financial position at a single point in

time, the income statement summarizes financial performance over a period of time, usually one year. The

income statement summarizes the firm’s revenues less its expenses to report net income (profit or loss)

for the period. Information from the balance sheet and income statement is used in computing important financial ratios.

14-3b Ratio Analysis 1. Concept Ratio analysis:

The calculation of one or more financial ratios to assess some aspect of the organization’s health.

Helps management, investors, and stakeholders evaluate efficiency, liquidity, and financial risk. 2. Common Ratios

a) Liquidity ratios

Show how readily the firm’s assets can be converted to cash. Example:

oCurrent ratio = Current assets ÷ Current liabilities.

oVinamilk: Current assets 10,000B VND, current liabilities 5,000B VND → Current ratio good short-term liquidity.

Benefits: Assess ability to meet short-term obligations.

Drawbacks: Does not reflect profitability or long-term risk. b) Debt ratios

Reflect the firm’s ability to meet long-term financial obligations. Example:

oDebt-to-equity ratio = Total debt ÷ Equity.

oVinFast: Total debt 20,000B VND, equity 30,000B VND → Debt-to-equity ratio = 0.67 healthy leverage.

Benefits: Assess long-term financial risk, supports decisions on borrowing or expansion.

Drawbacks: Only reflects capital structure, not short-term performance.

14-3b Financial Audits 1. Concept Audit:

An independent appraisal of an organization’s accounting, financial, and operational systems.

Helps verify accuracy, transparency, and efficiency of the organization.

2. Types of Audits

a) External audits

Conducted by experts who are not employees of the organization.

Purpose: verify financial statement accuracy and legal compliance.

Example: PwC audits VinFast’s financial statements for 2025. Benefits:

oProvides high credibility to investors, shareholders, and banks.

oHelps detect risks and errors overlooked internally. Drawbacks: oHigh cost and time-consuming.

oDoes not monitor all internal operations in detail.

b) Internal audits

Conducted by employees of the organization.

Purpose: assess operational efficiency, internal control, and policy compliance.

Example: Vinamilk’s internal audit department evaluates marketing budget usage. Benefits:

oDetects errors, fraud, and improves operational efficiency promptly.

oLower cost than external audits. Drawbacks:

oLess objective, may be influenced by internal relationships.

14-4 Structural Control

1. Types of Organizational Control

a) Bureaucratic control Characteristics:

oBased on formal and mechanistic structural arrangements, with clear rules and a rigid hierarchy.

oGoal: ensure employee compliance.

oSets minimum acceptable performance levels. Example:

Vietcombank applies strict approval procedures for every loan → ensures legal com and risk management. Benefits:

oEasy to control, reduces errors and fraud.

oClear responsibilities and authority. Drawbacks:

oReduces creativity and flexibility, employees follow rules rigidly.

oToo rigid → slow response to market changes.

b) Decentralized control Characteristics:

oBased on informal, flexible, and organic structures.

oEmphasizes results over strict compliance. Example:

Google uses decentralized management in creative projects, allowing teams to deci

approach → increases innovation and efficiency. Benefits:

oEnhances flexibility, creativity, and . adaptability

oEmployees feel responsible and motivated. Drawbacks:

oDifficult to monitor in detail, risk of errors or inconsistency across departments.

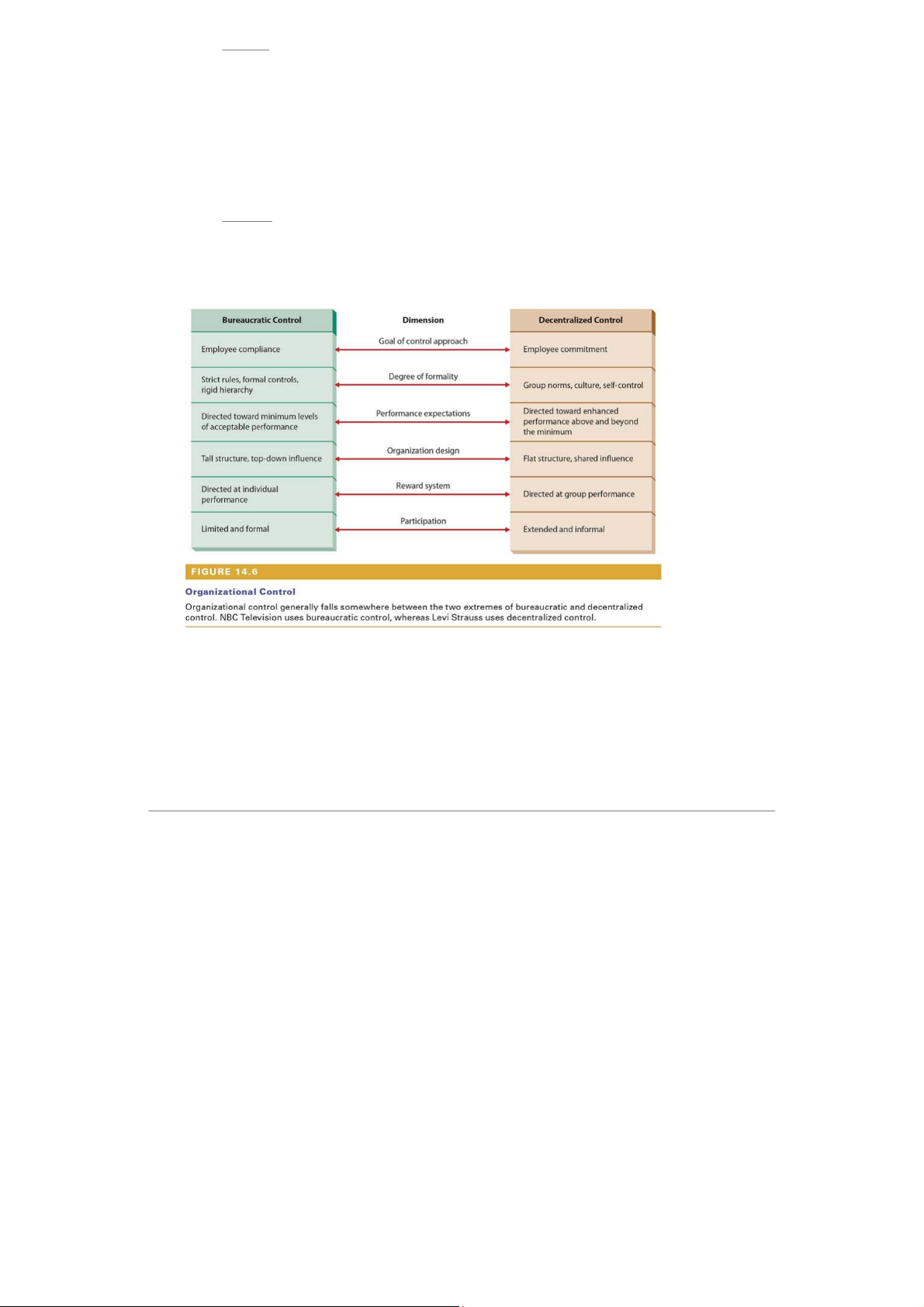

Based on Figure 14.6 “Organizational Control”, compare bureaucratic control and decentralized control.

Figure 14.6 presents two approaches to organizational control: bureaucratic control and decentralized control.

In terms of the goal of control:

Bureaucratic control focuses on employee compliance, whereas decentralized control emphasizes

employee commitment and responsibility.

Regarding the degree of formality:

Bureaucratic control relies on strict rules, formal controls, and a rigid hierarchy, while decentralized

control is based on group norms, organizational culture, and self-control.

With respect to performance expectations:

Bureaucratic control is directed toward achieving the minimum acceptable level of performance,

whereas decentralized control encourages performance above and beyond the minimum.

In terms of organizational design:

Bureaucratic control is associated with a tall organizational structure and top-down influence, w

decentralized control supports a flat structure with shared influence.

Regarding the reward system and participation:

Bureaucratic control emphasizes individual performance and limited, formal participation, whereas

decentralized control focuses on group performance and extended, informal participation.

✅ Concluding sentence

In conclusion, each control approach has its own advantages; bureaucratic control is suitable for o

that require stability and strict procedures, while decentralized control is more effective in dynam

environments that value innovation and employee involvement.

During times of uncertainty and rapid change, which type of organizational control would allow an

organization to manage change better? Why? What characteristics of other types of control might prevent an

organization from successfully managing uncertainty? Why?

During times of uncertainty and rapid change, decentralized control enables an organization to manage

change most effectively.

Reason: This type of control is flexible, focuses on results rather than rigid rules, and encourages

creativity and fast decision-making, allowing the organization to adapt quickly to a changing environment.

Example: Google allows teams to decide how to execute projects in a fast-changing tech environment

→ projects are adjusted promptly while still achieving goals.

In contrast, bureaucratic control may hinder an organization from managing uncertainty effectively.

Reason: Bureaucratic control relies on rigid rules, hierarchy, and minimum performance standards,

making employees less flexible and slower in decision-making.

Example: Traditional banks with strict loan approval procedures → slow response to market

fluctuations, missing investment opportunities.

Conclusion: In fast-changing environments, decentralized control allows adaptability, creativity, and rapid

decision-making, while bureaucratic control reduces flexibility and responsiveness.

14-5a Integrating Strategy and Control 1. Concept Strategic control:

Control aimed at ensuring that the organization maintains an effective alignment with its envi

and is moving toward achieving its strategic goals.

Purpose: To assess whether an implemented strategy is effective and if the organization is o reach long-term objectives.

2. Areas of focus

Structure: Check if organizational structure supports the strategy.

Leadership: Evaluate leadership’s ability to guide and execute strategy.

Technology: Ensure technology supports strategic objectives.

Human resources: Assess skills, staffing, and training aligned with strategy.

Informational and operational systems: Ensure data and processes support strategic decision-making. 3. Example

VinFast: Expanding internationally, VinFast applies strategic control by:

oUpdating advanced electric vehicle production technology.

oTraining staff to meet international standards.

oAdjusting organizational structure for fast market response.

→ Strategic control ensures the goal of international expansion is implemented effecti

4. Benefits and drawbacks Benefits Drawbacks

Helps the organization stay on strategic track and Oftenmake

time-consuming and costly, requires extensive timely adjustments data and analysis

Ensures departments, technology, and human resources align with strategy

May respond slowly if strategic data is outdate

Supports strategic decision-making based on real

information Difficult to assess short-term effectiveness of strategy

14-5b International Strategic Control 1. Concept

a) Centralized system Characteristics:

oEach unit reports performance results to . headquarters

oFrequent monitoring, including visits to foreign branches. Benefits:

oTight, consistent control, easy to detect errors and risks. Drawbacks:

oReduces creativity and flexibility at branches.

oDecisions are slower, hard to respond quickly to local markets. Example:

Traditional banks like Vietcombank monitor branches via weekly/monthly reports → control but less flexible.

b) Decentralized system Characteristics:

oReports less often and in less detail.

oTypically submit quarterly summaries and full report once a year.

oEncourages creativity and autonomy. Benefits:

oIncreases flexibility, innovation, and adaptability at branches.

oEmployees feel responsible and motivated. Drawbacks:

oHard to monitor in detail, may lack consistency across units. Example:

Google allows international offices to decide project execution → fosters innovation, quickly to local markets.

14-6a Characteristics of Effective Control

Key Factors for Effective Control Systems

1. Integration with planning

Principle: The more control is linked to organizational planning, the more effective the contro

Reason: Helps compare actual results with planned goals, detect deviations promptly.

Example: VinFast integrates strategic control when planning international expansion → monitors

progress, costs, and product quality to adjust in time. 2. Flexibility

Principle: The control system must be flexible enough to accommodate change.

Reason: Business environment constantly changes; rigid systems hinder quick and creative decis making.

Example: Google’s project control system is flexible → teams adjust schedules and methods market changes. 3. Accuracy

Principle: Control information must be accurate and reliable.

Reason: Inaccurate information leads to poor decisions and inappropriate managerial actions.

Example: Vinamilk receives inaccurate inventory reports → orders wrong material amounts, cau

production disruption and cost waste. 4. Timeliness

Principle: The control system should provide information as often as necessary.

Reason: Timely information allows managers to respond quickly, adjust strategies, and keep op on track.

Example: Supermarket chain Big C needs daily inventory reports → ensures timely ordering a

distribution, avoiding shortages or excess stock. 5. Objectivity

Principle: Control information must be free from bias or distortion.

Reason: Biased or distorted information can lead to poor decisions or inappropriate managerial

Example: If internal audit reports sales data in a biased way → management may make in

production plans, wasting costs.

14-6b Resistance to Control

Common Mistakes in Control Systems 1. Overcontrol

Principle: Trying to control too many details can negatively affect employee behavior if they as unreasonable.

Example: In a manufacturing company, management requires daily reports on every small step

employees feel over-monitored, lose motivation and creativity. 2. Inappropriate focus

Principle: Control system is too narrow or focuses only on quantifiable variables, ignoring qu analysis.

Example: A bank evaluates employees only by the number of customers served, not service

employees rush work, customers dissatisfied.

3. Rewards for inefficiency

Principle: Rewarding operational inefficiency encourages behaviors not in the organization’s best interest.

Example: Production department rewarded by hours worked instead of product quality → emp work slowly, wasting costs.

4. Too much accountability

Principle: Effective controls may be resisted by poorly performing employees.

Example: Sales staff not meeting KPIs may avoid reporting or ignore procedures, reducing co effectiveness.

Why do some people resist control? Are

managers partly to blame for this

resistance? Why or why not? How can

managers help overcome resistance?

1. Reasons why employees resist control

Overcontrol: Employees feel over-monitored and lack autonomy → lose motivation and creativit

Lack of objectivity: Biased or unfair control information → employees distrust and resist.

Too much accountability: Excessive responsibilities without support → stress and resistance.

Rewards for inefficiency: Rewards encourage behaviors harmful to the organization → employees counterproductively.

Example: Sales staff avoiding reporting or falsifying data because they feel over-monitored and un treated.

2. Managers’ role

Managers partly responsible:

oOverly rigid, inflexible, or non-transparent control systems → employees feel oppressed a resist.

oExample: Manufacturing company requires detailed daily reports → employees lose motiv

Not entirely managers’ fault:

oEmployees may naturally resist if unfamiliar with control systems or feel their autonom limited.

3. How managers can overcome resistance

1. Explain the purpose of control: Show that it supports employees and organization, not punishm

2. Design flexible controls: Allow autonomy, creativity, and feedback.

3. Ensure transparency and objectivity: Provide accurate, unbiased information.

4. Reward appropriately: Reward real efficiency and achieved results, avoid rewarding counterprodu behavior.

5. Employee involvement: Let employees participate in designing control systems → increase ac

Example: Google allows teams to design project schedules and reporting → reduces resistance, in creativity and efficiency.

Tài liệu liên quan:

-

CHAP 1: Introduction to Management Concepts and Functions môn Principles of Management | Trường Đại học Quốc tế, Đại học Quốc gia Thành phố Hồ Chí Minh

15 8 -

Guidelines for group’s assignments: Analysing management issues of a FDI company based inVietnam môn Principles of Management | Trường Đại học Quốc tế, Đại học Quốc gia Thành phố Hồ Chí Minh

15 8 -

Financial Planning to Achieve 300m VND Goal in 3 Years môn Principles of Management | Trường Đại học Quốc tế, Đại học Quốc gia Thành phố Hồ Chí Minh

12 6 -

A Case Study in Fast Fashion Success môn Principles of Management | Trường Đại học Quốc tế, Đại học Quốc gia Thành phố Hồ Chí Minh

15 8 -

Chap 16 Hierarchy of Needs Theory and Applications môn Principles of Management | Trường Đại học Quốc tế, Đại học Quốc gia Thành phố Hồ Chí Minh

16 8