Chapter 21: Process Costing System Overview and Flow | Môn Managerial Accounting - Trường Đại học Quốc tế, Đại học Quốc gia Thành phố Hồ Chí Minh

Chapter 21: Process Costing System Overview and Flow Môn Managerial Accounting. Tài liệu được sưu tầm gồm 8 trang, giúp bạn ôn tập tốt hơn. Mời các bạn đón xem.

Môn: Managerial Accounting 11 tài liệu

Trường: Trường Đại học Quốc tế, Đại học Quốc gia Thành phố Hồ Chí Minh 1.9 K tài liệu

Tác giả:

Preview text:

lOMoAR cPSD| 58605085 Chapter 21: Process Costing

1. Process Costing System

● Mục đích: Phân bố chi phí cho từng sản phẩm bằng cách chia tổng chi phí cho tổng số lượng những sản phẩm giống nhau được sản xuất

● Đặc điểm: áp dụng cho những sản phẩm giống nhau, sản xuất hàng loạt với số lượng lớn (homogeneous, mass- produced)

● Example: beverages factory, fertilizer factory, oil refinery

2. Process Costing Flow (kèm transactions)

Bước 0: (tương tự Job Order Costing)

● Mua nguyên vật liệu bằng tiền hoặc ghi nợ mua thiếu: Dr. Raw Materials Inventory

Cr. Accounts Payable / Cr. Cash

● Tính lương phải trả cho công nhân: Dr. Factory Labor Cr. Factory Wages Payable

Cr. Employer Payroll Taxes Payable

● Charge những chi phí sản xuất chung: Dr. Manufacturing Overhead Cr. Accounts Payable

Cr. Accumulated Depreciation- Equipment lOMoAR cPSD| 58605085 Cr. Utilities Payable Cr. Prepaid Insurance

Bước 1: Manufacturing Costs ⇒ Work in Process Inventory

Raw Materials, Direct Labor và Manufacturing Overhead mua ở trên không charge cho duy nhất 1 quy trình WIP mà có thể nhiều

quy trình cùng lúc, ví dụ cục bột sau khi mua về dùng cho cả qui trình cắt Cutting và cán tấm Rolling:: Dr. Work in Process - Cutting 10 Dr. Work in Process - Rolling 15 25 Cr. Raw Materials Inventory

Tương tự với Direct Labor và OH: Dr. Work in Process - Cutting 12 Dr. Work in Process - Rolling 11 Cr. Factory Labor 23 Dr. Work in Process - Cutting 10 Dr. Work in Process - Rolling 10 Cr. Manufacturing Overhead 20 lOMoAR cPSD| 58605085

Bước 2: Chuyển giao tới Department tiếp theo

Stage này hoàn thành nhiệm vụ rồi thì hàng hóa chuyển tới stage khác để tiếp tục dây chuyền sản xuất, ví dụ cục bột sau khi

hấp Steaming sẽ qua bước sấy khô Drying: Dr. Work in Process - Drying 10

Cr. Work in Process - Steaming 10

Bước 3: Work in Process Inventory ⇒ Finished Goods Inventory (tương tự Job Order Costing) Dr. Finished Goods Inventory Cr. Work in Process - Drying

Bước 4: Sau khi thành phẩm đã ra lò, bán hàng và ghi nhận doanh thu (tương tự Job Order Costing)

Dr. Cash/ Dr. Accounts Receivable Cr. Sales Revenue Dr. Cost of Goods Sold Cr. Finished Goods Inventory

3. Production Cost Report (quan trọng)

Bao gồm 4 steps, chép format có sẵn ở slide 42 ppt Chapter 21 và fill in những thông tin đề bài cho và tính toán đơn giản như sau: Mixing Department Production Cost Report

For the Month Ended July 31, 2024 lOMoAR cPSD| 58605085 Equivalent Units Physical Units Materials Conversion Costs Quantities [STEP 1] Uníts to be accounted for Work in process, July 1 Started into production Total units Units accounted for [STEP 2] Transferred out Work in process, July 31 100% 40% Total units Materials Conversion Costs Total costs Costs [STEP 3] Unit costs Total cost (a) Equivalent units (b) lOMoAR cPSD| 58605085 Unit costs (a/b) Cost to be accounted for Work in process, July 1 Started into production Total costs

Cost Reconciliation Schedule [STEP 4] Costs accounted for Transferred out Work in process, July 31 Materials Conversion costs Total costs

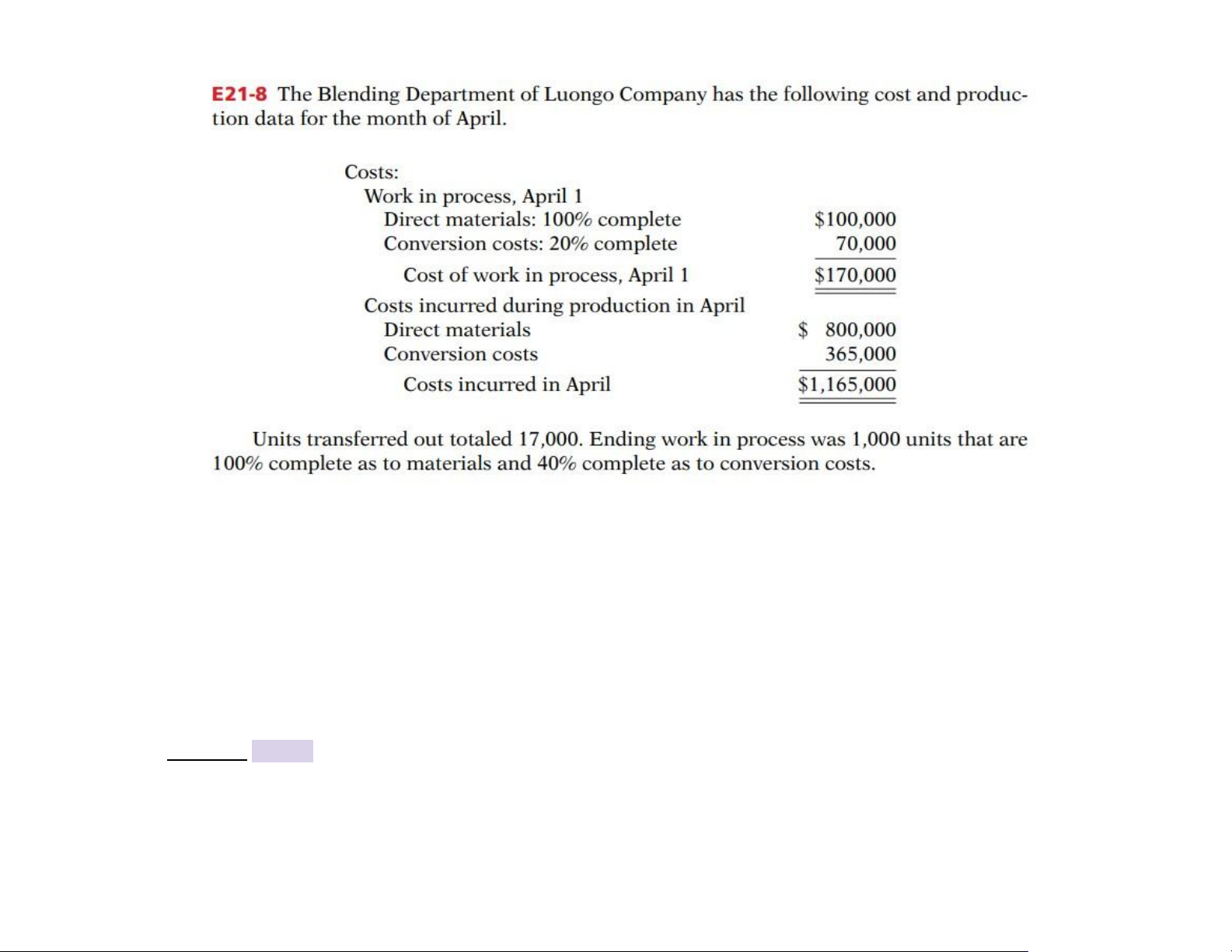

Để dễ hình dùng step by step, chúng ta có bài tập áp dụng sau, thi mid cũng sẽ tương tự vậy nha! E21-8 lOMoAR cPSD| 58605085 Blending Department Production Cost Report

For the Month Ended April 30, 2020 Equivalent Units Physical Units Materials Conversion Costs Quantities [STEP 1] Uníts to be accounted for lOMoAR cPSD| 58605085 Work in process, April 1 Started into production Total units 18,000 Units accounted for [STEP 2] Transferred out 17,000 17,000 17,000

Work in process, April 30 1,000 1,000 x 100% 1,000 1,000 x 40% 400 Total units 18,000 18,000 17,400 Materials Conversion Costs Total costs Costs [STEP 3] Unit costs Total cost (a) $900,000 $435,000 $1,335,000 Equivalent units (b) 18,000 17,400 Unit costs (a/b) $50 $25 $75 Cost to be accounted for Work in process, April 1 $170,000 lOMoAR cPSD| 58605085 Started into production 1,165,000 Total costs $1,335,000

Cost Reconciliation Schedule [STEP 4] Costs accounted for $1,275,000

Transferred out (17,000 x $75) Work in process, April 30 Materials (1,000 x $50) $50,000 Conversion costs (400 x $25) 10,000 60,000 Total costs $1,335,000

Tài liệu liên quan:

-

Chapter 1 Introduction to management accounting - Slide bài giảng môn Managerial Accounting | Trường Đại học Quốc tế, Đại học Quốc gia Thành phố Hồ Chí Minh

39 20 -

Practice Notes and Key Concepts | Môn Managerial Accounting - Trường Đại học Quốc tế, Đại học Quốc gia Thành phố Hồ Chí Minh

84 42 -

Budgetary Control and Responsibility | Môn Managerial Accounting - Trường Đại học Quốc tế, Đại học Quốc gia Thành phố Hồ Chí Minh

88 44 -

Tài liệu Môn Managerial Accounting | Trường Đại học Quốc tế, Đại học Quốc gia Thành phố Hồ Chí Minh

92 46