Chất Lượng Lợi Nhuận và Phương Pháp Kế Toán Môn Lý thuyết xác xuất và thống kê ứng dụng | Trường Đại học Tài chính - Marketing

A quality of earnings report (báo cáo chất lượng lợi nhuận) is a routine step in the due diligence process for private acquisitions. The report assesses how a company accumulates its revenues – such as cash or non-cash, recurring or nonrecurring. Tài liệu gồm 5 trang, giúp các bạn tham khảo, ôn tập và đạt kết quả cao. Mình bạn đọc đón xem!

Môn: Lý thuyết xác suất và thống kê ứng dụng 11 tài liệu

Trường: Trường Đại học Tài Chính - Marketing 1 K tài liệu

Tác giả:

Preview text:

KẾ TOÁN QUẢN TRỊ 2

1. Quality of earnings:

A quality of earnings report (báo cáo chất lượng lợi nhuận) is a routine step in

the due diligence process for private acquisitions. The report assesses how a company

accumulates its revenues – such as cash or non-cash, recurring or nonrecurring.

The quality of earnings ratio (QoE) helps distinguish a company’s true earnings

by separating net income from non-operating items and accounting adjustments that do

not relate to its core business activities. It filters out irregularities and accounting

adjustments to provide a more accurate assessment of the company’s financial performance.

- sử dụng để thẩm định đối với các thương vụ mua bán tư nhân, đánh giá cách một

công ty tích lũy doanh thu của mình – chẳng hạn như tiền mặt hoặc phi tiền mặt, định kỳ hoặc không định kỳ

Tỷ lệ chất lượng thu nhập (QoE) giúp phân biệt thu nhập thực tế của một công ty

bằng cách tách thu nhập ròng khỏi các khoản mục phi hoạt động và các khoản điều

chỉnh kế toán không liên quan đến các hoạt động kinh doanh cốt lõi của công ty.

A low QoE ratio does not necessarily indicate malpractice within the company.

Tỷ lệ QoE thấp không nhất thiết chỉ ra sai phạm trong công ty. *** Formula:

𝐶𝑎𝑠ℎ 𝑓𝑟𝑜𝑚 𝑂𝑝𝑒𝑟𝑎𝑡𝑖𝑜𝑛𝑠

𝑄𝑢𝑎𝑙𝑖𝑡𝑦 𝑜𝑓 𝑒𝑎𝑟𝑛𝑖𝑛𝑔𝑠 (𝑄𝑜𝐸) =

𝑁𝑒𝑡 𝑖𝑛𝑐𝑜𝑚𝑒

Chất lượng thu nhập (QoE)= Tiền mặt từ Hoạt động/Lợi nhuận ròng

The general rules for interpreting the quality of earnings (QoE) ratio are the following:

+ A higher QoE ratio: Cash flow operating exceeds net income, not distorted by

earnings manipulation Information is more Reliable earnings

+ A lower QoE ratio: signals that accounting adjustments significantly impact reported

earning Raise concerns about corporate governance and internal policies.

Tỷ lệ QoE cao hơn: Lưu chuyển tiền tệ từ hoạt động kinh doanh vượt quá thu nhập ròng,

không bị bóp méo bởi thao túng lợi nhuận → Thông tin về thu nhập đáng tin cậy hơn

Tỷ lệ QoE thấp hơn: báo hiệu rằng các điều chỉnh kế toán tác động đáng kể đến thu

nhập được báo cáo → Làm dấy lên lo ngại về quản trị doanh nghiệp và các chính sách nội bộ.

2. Alternative Account Methods: (Phương pháp tài khoản thay thế)

The modified accrual accounting method created by the Governmental Accounting

Standards Board (GASB) is an alternative accounting method. It uses cash accounting to

record short-term events and accrual accounting to record long-term events.

Different approaches companies use to record transactions under Generally

Accepted Accounting Principles (GAAP) or International Financial Reporting Standards (IFRS).

Variations among companies in the application of generally accepted accounting principles

may hamper comparability and reduce quality of earnings.

Sự khác biệt giữa các công ty trong việc áp dụng các nguyên tắc kế toán

được chấp nhận chung có thể cản trở khả năng so sánh và làm giảm chất lượng thu nhập.

Ví dụ: một công ty có thể sử dụng phương pháp FIFO để tính giá hàng

tồn kho, trong khi một công ty khác trong cùng ngành có thể sử dụng

LIFO. Nếu hàng tồn kho là một tài sản quan trọng đối với cả hai công ty,

thì tỷ lệ thanh toán hiện hành của họ khó có thể so sánh được.

In addition to differences in inventory costing methods, differences also exist in reporting

such items as depreciation, depletion, and amortization. Although these differences in

accounting methods might be detectable from reading the notes to the financial statements,

adjusting the financial data to compensate for the different methods is often difficult, if not impossible.

Ngoài sự khác biệt về phương pháp tính giá hàng tồn kho, còn có sự khác

biệt trong việc báo cáo các khoản mục như khấu hao tài sản cố định, khấu

hao tài nguyên và phân bổ dần. Mặc dù những khác biệt trong phương

pháp kế toán này có thể được phát hiện khi đọc các thuyết minh báo cáo

tài chính, nhưng việc điều chỉnh dữ liệu tài chính để bù đắp cho các

phương pháp khác nhau thường rất khó khăn, nếu không muốn nói là không thể.

3. Pro forma Income:

Unlike standard accounting statements that follow strict rules, pro forma statements

offer a customized view of a company's finances.

A pro forma income statement is a projection of an income statement based on historical

data and performance assumptions. Startups, small businesses, and large companies can all

benefit from generating pro forma reports for decision-making.

Báo cáo thu nhập pro forma là một dự báo về báo cáo thu nhập dựa trên

dữ liệu lịch sử và các giả định về hiệu suất. Các công ty khởi nghiệp,

doanh nghiệp nhỏ và các công ty lớn đều có thể hưởng lợi từ việc tạo ra

các báo cáo pro forma để đưa ra quyết định.

Companies exclude certain items when calculating pro forma income, claiming it

reflects sustainable earnings. However, analysts criticize this practice for potentially

misleading investors, calling it “earnings before bad stuff” (EBS). Cisco defends its

approach, stating that pro forma income clarifies normal business operations. DO IT!

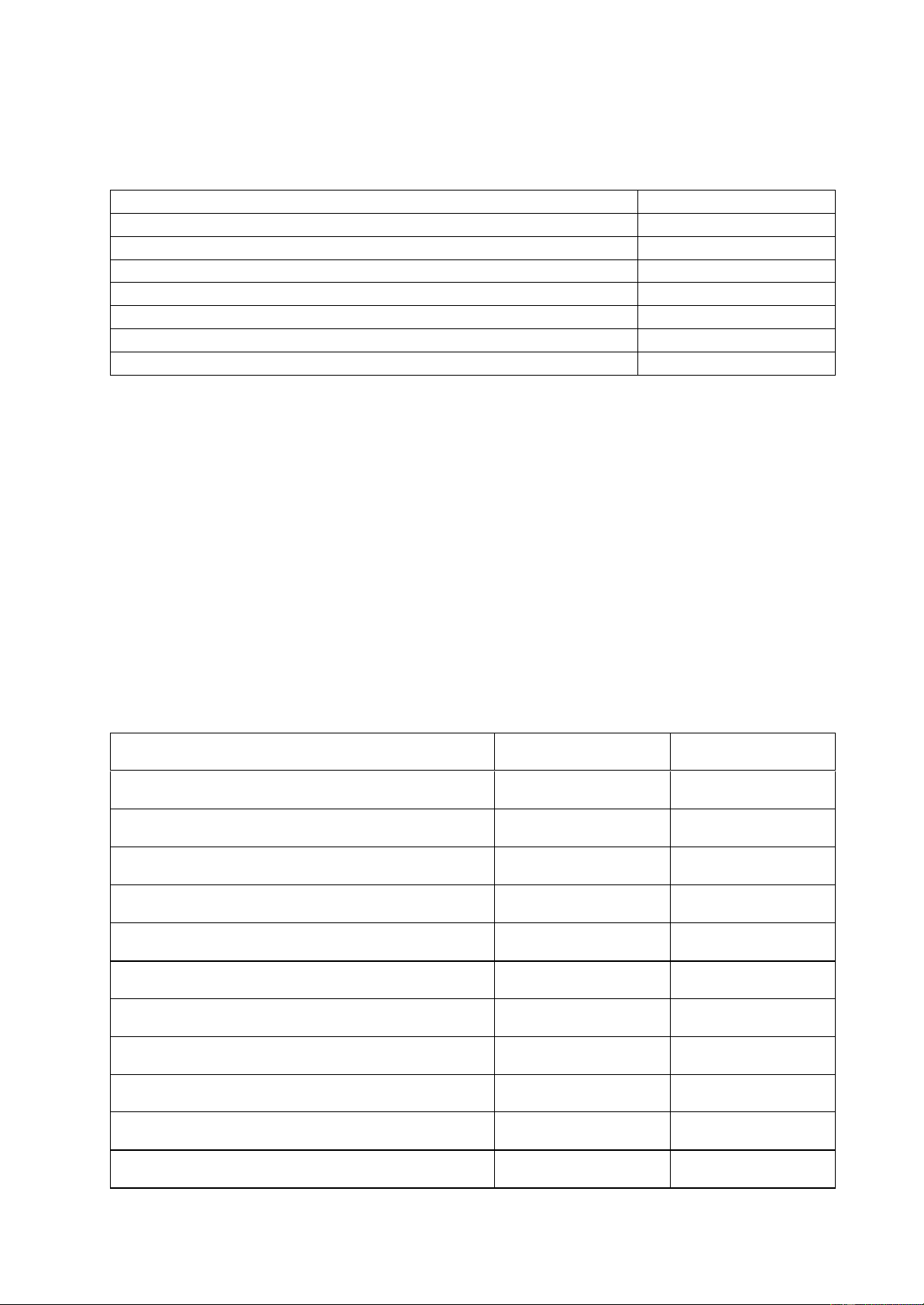

The events and transactions of Dever Corporation dor the year anding December

31, 2010, resulted in the following data. Cost of goods sold $ 2,600,000 Net Sales $ 4,400,000 Other expenses and losses $ 9,600 Other revenues and gains $ 5,600

Selling and administrative expenses $ 1,100,000 Income from operation $ 70,000

Gain from disposal of plastics division $ 500,000 Loss from tornado disaster $ 600,000 Analysis reveals that:

1. All items are before the applicable income tax rate of 30%.

2. The plastics division was sold on July 1.

3. All operating data for the plastics division have been segregated.

Instructions: Prepare an income statement for the year. DEVER CORPORATION Income Statement

For the Year Ended December 31,2010 Net Sales $ 4,400,000 Cost of Goods Sold $ 2,600,000 Gross fit $1,800,000

Selling and administrative expenses $ 1,100,000 Income from operation $ 700,000 Other revenues and gains $ 5,600 Other expenses and losses $ 9,600 $ 4,000

Income before income taxes $ 696,000 Income tax expense $ 208,800

Income from continuing operations $ 487,200 Discontinued operation

Income from operations of plastics division $ 49,000

Gain from disposal of plastics division $ 350,000 $ 399,000

Income before extraordinary item $ 886,200 Extraordinary item Tornado loss $ 420,000 Net income $ 466,200

Tài liệu liên quan:

-

BÀI TẬP TỰ LUẬN VỀ THUẾ XUẤT NHẬP KHẨU - MÔN THUẾ 01

41 21 -

Đánh Giá Kỹ Năng Làm Việc Nhóm Môn Lý thuyết xác xuất và thống kê ứng dụng | Trường Đại học Tài chính - Marketing

89 45 -

Đề số 1: Tác phẩm và Khát vọng sống trong văn học Việt Nam Môn Lý thuyết xác xuất và thống kê ứng dụng | Trường Đại học Tài chính - Marketing

84 42 -

Bài tập nhóm 3: Chiến lược marketing thương mại quốc tế Môn Lý thuyết xác xuất và thống kê ứng dụng | Trường Đại học Tài chính - Marketing

80 40