GR-3- Exercise-2.10-3.4 20.1A - Tài liệu tham khảo | Đại học Hoa Sen

GR-3- Exercise-2.10-3.4 20.1A - Tài liệu tham khảo | Đại học Hoa Sen và thông tin bổ ích giúp sinh viên tham khảo, ôn luyện và phục vụ nhu cầu học tập của mình cụ thể là có định hướng, ôn tập, nắm vững kiến thức môn học và làm bài tốt trong những bài kiểm tra, bài tiểu luận, bài tập kết thúc học phần, từ đó học tập tốt và có kết quả cao cũng như có thể vận dụng tốt những kiến thức mình đã học.

Môn: Corporate Finance (CF2033) 92 tài liệu

Trường: Trường Đại học Hoa Sen 5.3 K tài liệu

Tác giả:

Preview text:

Group 3: Vũ Trần Nhã Đoan Nguyễn Phạm Thanh Phương Nguyễn Thành Mỹ Duyên Nguyễn Minh Nguyệt Mai Tấn Quân Nguyễn Tiến Dũng Nguyễn Ngọc Như Ý Nguyễn Lê Ngọc Diễm Lê Thị Kim Quý EXERCISE 2.10

1. With the recognition of increase in land value by $1.5 million and decrease in

building value by 1.7 million dollars, this allocation will increase future income as the

land is non-asset depreciated. Thus, the company's pre-tax profit will increase to $0.5 million.

2. The assistant faces an ethical dilemma because if he does according to the

controller's allocation method, will not meet the principle of recognizing assets as

“Cost must be determined reliably” and does not follow the accounting principle

maths. But if the assistant doesn't follow through, he may be disciplined for

increasing the difficulty problems with the company's profitability. EXERCISE 3.4 (i)

In this case, CGU is a plant in Alandia as a whole, as individual assets do not generate

cash inflows largely independently from others.

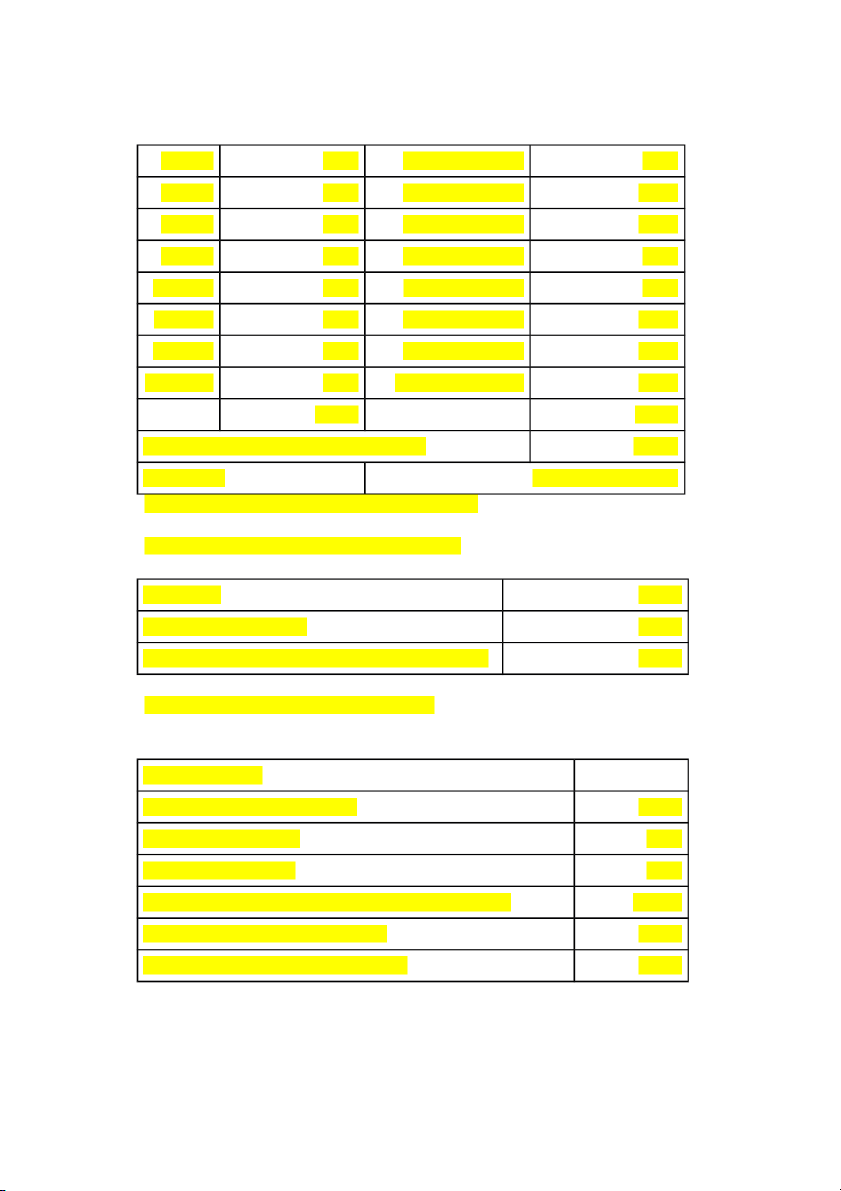

Calculation of value in use (EUR ‘000) Year Cash flow Discount factor at 5% Present value 1- 20X4 10,200 1/(1+5%)=0,952 9,714 2- 20X5 9,550 1/(1+5%)^2=0,907 8,662 3- 20X6 8,900 1/(1+5%)^3=0,864 7,688 4- 20X7 8,250 1/(1+5%)^4=0,823 6,787 5- 20X8 7,600 1/(1+5%)^5=0,784 5,955 6- 20X9 6,950 1/(1+5%)^6=0,746 5,186 7- 20X10 6,300 1/(1+5%)^7=0,711 4,477 8- 20X11 5,650 1/(1+5%)^8=0,677 3,824 9- 20X12 5,000 1/(1+5%)^9=0,645 3,223 10- 20X13 4,350 1/(1+5%)^10=0,614 2,671 72,750 58,188

Present value of decommissioning in 20X13 -15000 Value in use 58,188 -15000=43,188

Discount Factor Formula used: DF= 1/(1+r)^year

Calculation of recoverable amount (EUR ‘000) Value in use 43,188 Fair value less cost to sell 42,000

Recoverable amount as of 30 Dec 20X3 (higher of): 43,188

Calculation of impairment loss (EUR ‘000) Carrying amount

Reactors, tower, store, equipment 55,000 Other technical facilities 8,000 Administrative building 2,000

Less Provision for decommissioning and restoration costs -15,000

Carrying amount as of 31 Dec 20X3 50,000

Recoverable amount as of 31 Dec 20X3 43,188

Impairment loss as of 31 Dec 20X3 6,812

Allocation of impairment loss (EUR ‘100) Asset Carrying % of total value Allocated Amount (G) impairment loss (G*E) Reactors, tower, store, 55,000 55,000/65,000*100 5,758 equipment %= 84,62% Other technical facilities 8,000 8,000/65,000*100% 838 = 12,31% Administrative building 2,000 2,000/65,000*100% 209 = 3,08% 65,000 100,00% 6.805

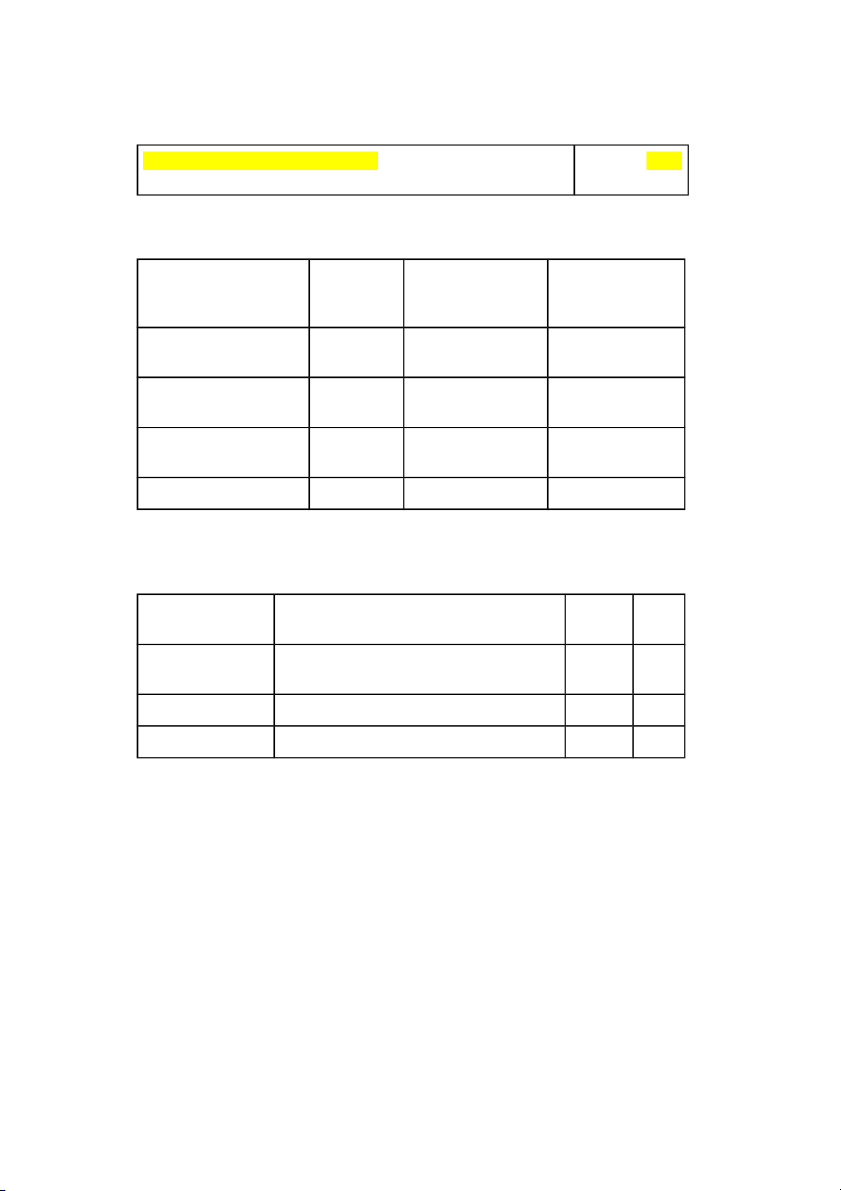

(ii) Prepare journal entries to record the Impairment loss DR Profit or loss - 6,805 Impairment loss

CR PPE (Reactors, tower, store, 5,758 equipment)

CR PPE (Other technical facilities) 838

CR PPE (Administrative building) 209

Tài liệu liên quan:

-

Lý do chọn đề tài báo cáo trong công việc - Tài liệu tham khảo | Đại học Hoa Sen

466 233 -

Models for warehouse management Classification and Project - Tài liệu tham khảo | Đại học Hoa Sen

222 111 -

Project Report Room for rent Group 4 - Tài liệu tham khảo | Đại học Hoa Sen

306 153 -

Brealey Fo CF 8ed Chapter 5 - Tài liệu tham khảo | Đại học Hoa Sen

291 146 -

Top 200 câu hỏi trắc nghiệm phân tích đầu tư và chứng khoán - Tài liệu tham khảo | Đại học Hoa Sen

1 K 481