Which of the following factors reflect pure market risk for a givencorporation?

Which of the following factors reflect pure market risk for a given corporation? Which of the following factors reflect pure market risk for a given corporation? Which of the following factors reflect pure market risk for a given corporation? Which of the following factors reflect pure market risk for a given corporation?

và thông tin bổ ích giúp sinh viên tham khảo, ôn luyện và phục vụ nhu cầu học tập của mình cụ thể là có định hướng, ôn tập, nắm vững kiến thức môn học và làm bài tốt trong những bài kiểm tra, bài tiểu luận, bài tập kết thúc học phần, từ đó học tập tốt và có kết qủa

Môn: Kinh tế quản trị, Quản trị kinh doanh (TV181) 475 tài liệu

Trường: Trường Đại học Hoa Sen 5.1 K tài liệu

Tác giả:

Preview text:

1.

Which of the following factors reflect pure market risk for a given corporation?

a) Increased short-term interest rates.

b) Fire in the corporate warehouse. c) Increased insurance costs. d) Death of the CEO. e) Increased labor costs. 2.

When adding real estate to an asset allocation program that currently

includes only stocks, bonds, and cash, which of the properties of real estate

returns affect portfolio risk? Explain. a) Standard deviation. b) Expected return.

c) Correlation with returns of the other asset classes.

Answer: After real estate is added to the portfolio, there are four asset classes

in the portfolio: stocks, bonds, cash, and real estate. Portfolio variance now

includes a variance term for real estate returns and a covariance term for real

estate returns with returns for each of the other three asset classes. Therefore,

portfolio risk is affected by the variance (or standard deviation) of real estate

returns and the correlation between real estate returns and returns for each of the other asset classes. 3.

Which of the following statements about the minimum variance portfolio of all risky securities

are valid? (Assume short sales are allowed.) Explain.

a) Its variance must be lower than those of all other securities or portfolios.

b) Its expected return can be lower than the risk-free rate.

c) It may be the optimal risky portfolio.

d) It must include all individual securities.

Answer: Its variance must be lower than those of all other securities or

portfolios. (a) is valid because it provides the definition of the minimum variance portfolio.

The following data apply to Problems 4 through 10: (Page 223) 4.

What are the investment proportions in the minimum-variance portfolio

of the two risky funds, and what is the expected value and standard deviation of its rate of return?

The parameters of the opportunity set are:

E(rS) = 20%, E(rB) = 12%, σS = 30%, σB = 15%, ρ = 0.10

From the standard deviations and the correlation coefficient we generate

the covariance [note that Cov(r , ) = S rB

x σS x σB ]: Cov(rS ,rB ) = 45

The minimum-variance portfolio is computed as follows: wMin(S) = = = 0.1739

wMin(B) = 1 - 0.1739 = 0.8261

The minimum variance portfolio mean and standard deviation are:

E(rMin) = (0.1739 × 20%) + (0.8261 × 12%) = 13.39% σMin =

= [(0.17392 x 900) + (0.82612 x 225) + (2 x 0.1739 x 0.8261 x 45)]1/2 = 13.92% 5.

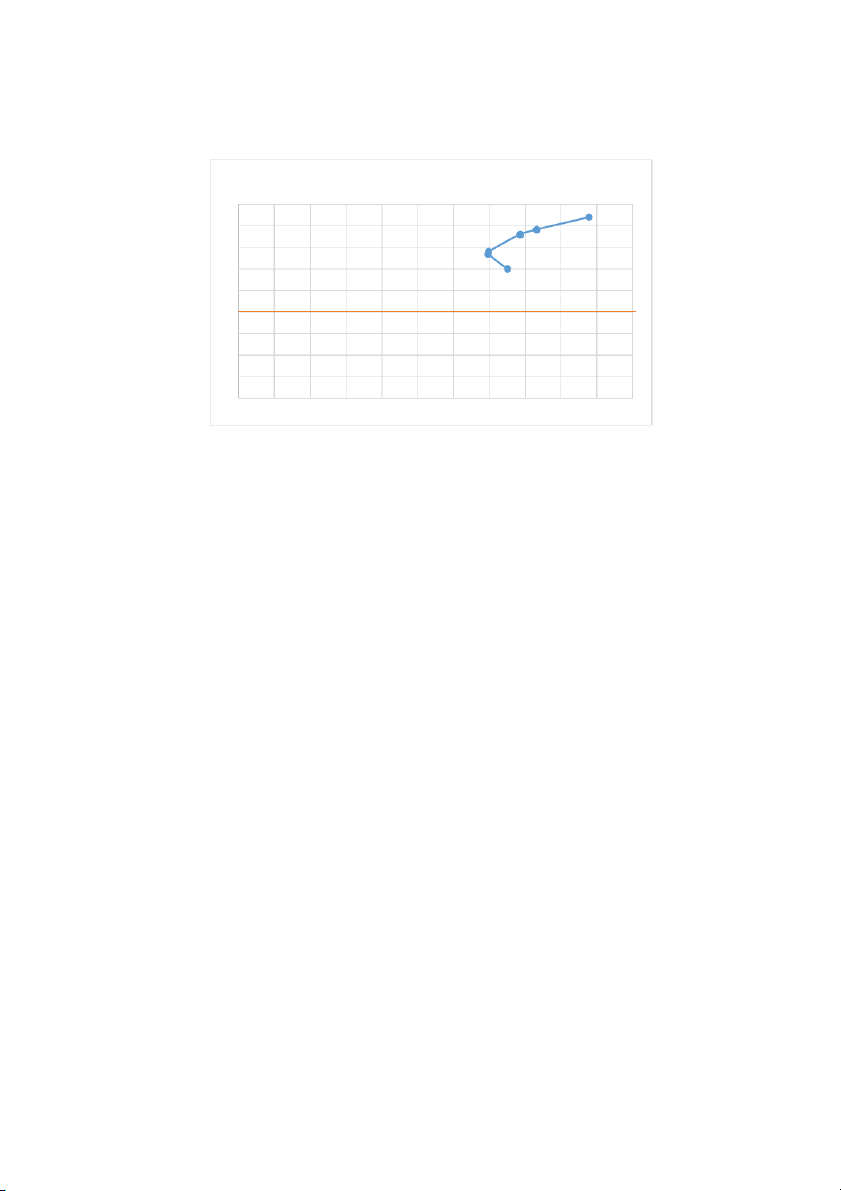

Tabulate and draw the investment opportunity set of the two risky funds.

Use investment proportions for the stock fund of zero to 100% in increments of 20%. Proporti Proporti Expect Standar on in on in ed d Stock Bond Return Deviati Fund (%) Fund (%) (%) on(% ) 0.00 100.00 12 15 17.39 82.61 13.3912 13.91746 Min. var. portfolio 20.00 80.00 13.6 13.94274 40.00 60.00 15.2 15.7035 45.6423 54.3577 15.65138 16.6223 Tangency portfolio 60.00 40.00 16.8 19.53458 80.00 20.00 18.4 24.48265 100.00 0.00 20 30

(Note that I have added two extra portfolios in the table above to set

apart the minimum variance portfolio and the tangency portfolio. I used

Excel to calculate the exact value. In an exam environment only

approximate values would suffice.) Graph shown below. Expected Return 18 16 14 12 10 8 6 4 2 0 0 2 4 6 8 10 12 14 16 18 20 22 6.

Draw a tangent from the risk-free rate to the opportunity set. What does

your graph show for the expected return and standard deviation of the optimal portfolio?

The above graph indicates that the optimal portfolio is the tangency

portfolio with expected return approximately 15.6% and standard deviation

approximately 16.5%. (Note that this problem is for your understanding. If

such question appears in the exam, then it would be designed such that the

answer would be more discernible.) 7.

Solve numerically for the proportions of each asset and for the expected

return and standard deviation of the optimal risky portfolio ws = = wB = 1- 0.4516 = 0.5484

The proportion of the optimal risky portfolio invested in the stock fund is given by:

E(rP) = (0.4516 × 20%) + (0.5484 × 12) = 15.61%

σp = [(0.45162 × 900) + (0.54842 × 225) + (2 x 0.4516 × 0.5484 x 45)]1/2 = 16.54% 8.

What is the reward-to-volatility ratio of the best feasible CAL?

The reward-to-volatility ratio of the optimal CAL is: = = 0.46 9.

You require that your portfolio yield an expected return of 14%, and that

it be efficient, on the best feasible CAL.

a. What is the standard deviation of your portfolio?

b. What is the proportion invested in the T-bill fund and each of the two risky funds? Answer: a.

If you require that your portfolio yield an expected return of 14%, then

you can find the corresponding standard deviation from the optimal CAL. The equation for this CAL is:

E(rc ) = rf + = 0.08 + 0.4601σc

If E(rC) is equal to 14%, then the standard deviation of the portfolio is 13.04%. b.

To find the proportion invested in the T-bill fund, remember that the mean

of the complete portfolio (i.e., 14%) is an average of the T-bill rate and the

optimal combination of stocks and bonds (P). Let y be the proportion invested

in the portfolio P. The mean of any portfolio along the optimal CAL is: E(r y

c ) = (1- ) × rf + y × E(rp ) = r +

f y × [E(r ) - ] = 8 + p rf y × (15.61 - 8)

Setting E(rC) = 14% we find: y = 0.7884 and (1 − y) = 0.2116 (the proportion invested in the T-bill fund).

To find the proportions invested in each of the funds, multiply 0.7884 times the

respective proportions of stocks and bonds in the optimal risky portfolio:

Proportion of stocks in complete portfolio = 0.7884 × 0.4516 = 0.3560

Proportion of bonds in complete portfolio = 0.7884 × 0.5484 = 0.4324 10.

If you were to use only the two risky funds, and still require an expected

return of 14%, what would be the investment proportions of your portfolio?

Compare its standard deviation to that of the optimized portfolio in Problem 9. What do you conclude?

Using only the stock and bond funds to achieve a portfolio expected return of

14%, we must find the appropriate proportion in the stock fund (w ) S and the

appropriate proportion in the bond fund (wB = 1 − w ) as follows: S

14% = 20% × w + 12% × (1 − S w ) = 12% + 8% × S wS w = S 0.25

So the proportions are 25% invested in the stock fund and 75% in the

bond fund. The standard deviation of this portfolio will be:

σP = [(0.252 × 900) + (0.752 × 225) + (2 × 0.25 × 0.75 × 45)]1/2 = 14.13%

This is considerably greater than the standard deviation of 13.04% achieved

using T-bills and the optimal portfolio. 11.

Stocks offer an expected rate of return of 18%, with a standard deviation

of 22%. Gold offers an expected return of 10% with a standard deviation of 30%.

a. In light of the apparent inferiority of gold with respect to both mean return

and volatility, would anyone hold gold? If so, demonstrate graphically why one would do so.

b. Given the data above, reanswer (a) with the additional assumption that the

correlation coef- ficient between gold and stocks equals 1. Draw a graph

illustrating why one would or would not hold gold in one’s portfolio. Could this

set of assumptions for expected returns, standard deviations, and correlation

represent an equilibrium for the security market? Answer: a.

Even though it seems that gold is dominated by stocks, gold might still be

an attractive asset to hold as a part of a portfolio. If the correlation between gold

and stocks is sufficiently low, gold will be held as a component in a portfolio,

specifically, the optimal tangency portfolio. b.

If gold had a correlation coefficient with stocks of +1, it would not be

held. The set of risk/return combinations of stocks and gold would plot as a

straight line with a negative slope (see the following graph). The graph shows

that in this case, any portfolio that contains any gold is dominated by the stock-

only portfolio. Therefore, no one will hold gold. Stated differently, the CAL for

the portfolio with stock only is steeper than any other CAL passing through all

other possible portfolios on the portfolio frontier. (Of course, this situation

could not persist. If no one desired gold, its price would fall and its expected

rate of return would increase until it became an attractive enough asset to hold).

The graph shows that in this case, any portfolio that contains any

gold is dominated by the stock-only portfolio. Therefore, no one will hold gold.

Stated differently, the CAL for the portfolio with stock only is steeper than any

other CAL passing through all other possible portfolios on the portfolio frontier.

(Of course, this situation could not persist. If no one desired gold, its price

would fall and its expected rate of return would increase until it became an

attractive enough asset to hold.) 12.

Suppose that there are many stocks in the security market and that the

characteristics of Stocks A and B are given as follows: Stock Expected Return Standard Deviation A 10% 5% B 15 10 Correlation –1

Suppose that it is possible to borrow at the risk-free rate, rf. What must be the

value of the riskfree rate? (Hint: Think about constructing a risk-free portfolio

from stocks A and B.) Answer:

Since Stocks A and B are perfectly negatively correlated, a risk-free portfolio

can be constructed and its rate of return in equilibrium will be the risk-free rate.

To find the proportions of this portfolio (wA invested in Stock A and wB = 1 -

wA in Stock B), set the standard deviation equal to zero.

With perfect negative correlation, the portfolio standard deviation reduces to: σp = | wAσA - wBσB| => 0 = | 5wA - 10 (1-wA) | => wA =0.6667

The expected rate of return on this risk-free portfolio is:

E(R) = 0.6667 x 10% + (0.3333 x 15%) ≈ 11.67%.

=>To avoid arbitrage, the risk-free rate must also be 11.67%. 13.

Assume that expected returns and standard deviations for all securities

(including the risk-free rate for borrowing and lending) are known. In this

case all investors will have the same optimal risky portfolio. (True or false?)

Assume that expected returns and standard deviations for all securities

(including the risk-free rate for borrowing and lending) are known. In this case

all investors will have the same optimal risky portfolio. (True or false?)

Answer: False. If the borrowing and lending rates aren’t identical, then

depending on the tastes of the individuals (that is, the shape of their indifference

curves), borrowers and lenders could have different optimal risky portfolios.

The portfolio standard deviation equals the weighted average of the component-

asset standard deviations only in the special case that all assets are perfectly positively correlated. 14.

The standard deviation of the portfolio is always equal to the weighted

average of the standard deviations of the assets in the portfolio. (True or false?)

Answer: False. Only in the special case that all assets are perfectly

positively correlated, will the portfolio standard deviation reduce the weighted

average of the component-asset standard deviations. Otherwise, as the formula

for portfolio standard deviations show, the portfolio standard deviations. The

portfolio variance will be a weighted sum of the elements in the covariance

matrix, with the products of the portfolio proportions as weights. 15.

Suppose you have a project that has a .7 chance of doubling your

investment in a year and a .3 chance of halving your investment in a year. What

is the standard deviation of the rate of return on this investment? Answer: Probability Rate of return 0.7 100% 0.3 -50%

Mean = (0.7 x 100%) + (0.3 x (-50%)) = 0.55 = 55%

Variance = [0.7 x (100-55)2] + [0.3 x (-50-55)2] = 4725 Standard deviation = 68.738% 16.

Suppose that you have $1 million and the following two opportunities

from which to construct a portfolio:

a. Risk-free asset earning 12% per year.

b. Risky asset with expected return 30% per year and standard deviation of 40%.

If you construct a portfolio with a standard deviation of 30%, what is its expected rate of return? Answer:

y = σc/σP = 0.30/0.40 = 0.75

E(rC) = rF + y[E(rP) – rf] = 0.12 + 0.75[0.30 – 0.12] = 25.50%

The following data are for Problems 17 through 19: The correlation

coefficients between pairs of stocks are as follows: Corr(A,B) = .85;

Corr(A,C) = .60; Corr(A,D) = .45. Each stock has an expected return of 8%

and a standard deviation of 20%. 17.

If your entire portfolio is now composed of stock A and you can add some of only one stock to

your portfolio, would you choose (explain your choice): a. B. b. C. c. D. d. Need more data.

Answer: Choose C. D because it has the lowest correlation of 0.45 which

in turn lower the risk by the largest amount. 18.

Would the answer to Problem 17 change for more risk-averse or risk- tolerant investors? Explain.

Answer: No, it wouldn’t change because it isn’t a factor when deciding

between risk-averse or risk-tolerant investor. This is because the lower the risk

better no matter what level of risk you are on. 19.

Suppose that in addition to investing in one more stock you can invest in

T-bills as well. Would you change your answers to Problems 17 and 18 if the T- bill rate is 8%?

Answer: No, neither part would change because the T-Bills rate would

stay stagnant at 8% since both stocks have the same expected returns but

different SDs. Meaning that the most profitable porfolio would be one that has

the least amount of deviation. Also, a portfolio is dependent on someone’s risk profile.

Tài liệu liên quan:

-

Đề tài: “Lập kế hoạch marketing cho dự án Asian Lake View” - Tài liệu tham khảo | Đại học Hoa Sen

227 114 -

2 Achoo Baocao Damkt 2131MK ECON847 - Tài liệu tham khảo | Đại học Hoa Sen

228 114 -

Tìm hiểu về cấu trúc email - Tài liệu tham khảo | Đại học Hoa Sen

275 138 -

Bài tập ôn tập thi lần 3 năm 2022 p2 - Tài liệu tham khảo | Đại học Hoa Sen

236 118 -

The Language Lab Library - Ielts Introduction Study Skill - Tài liệu tham khảo | Đại học Hoa Sen

382 191