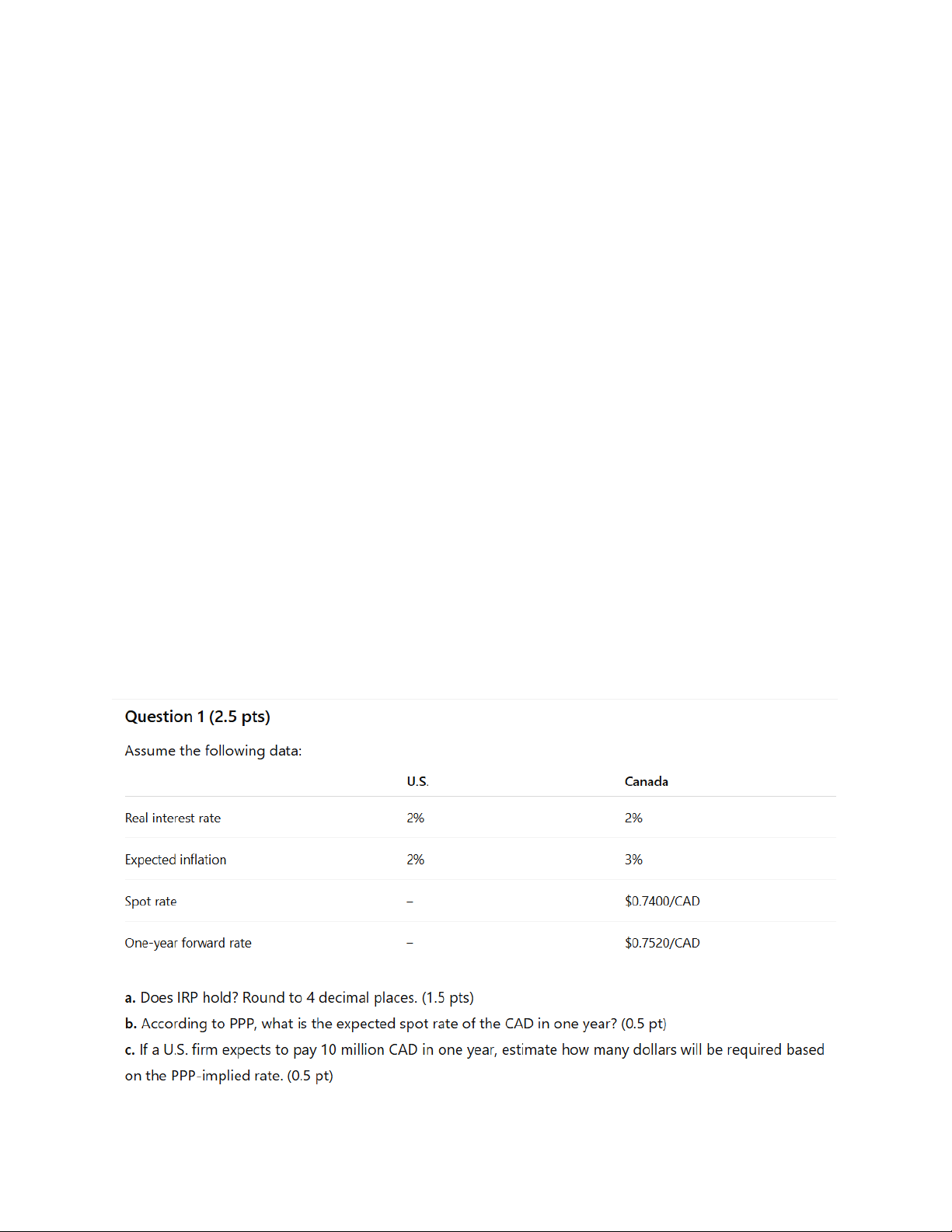

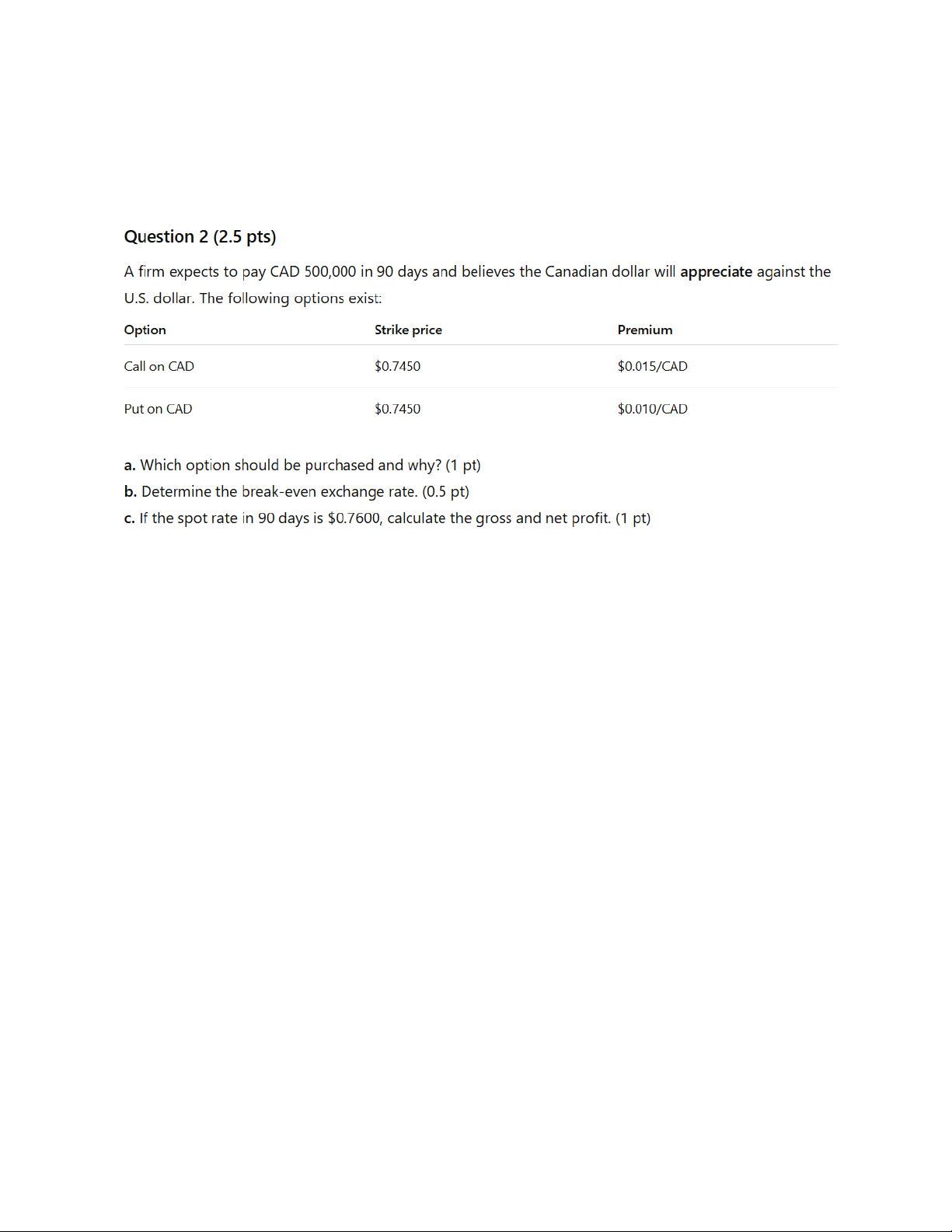

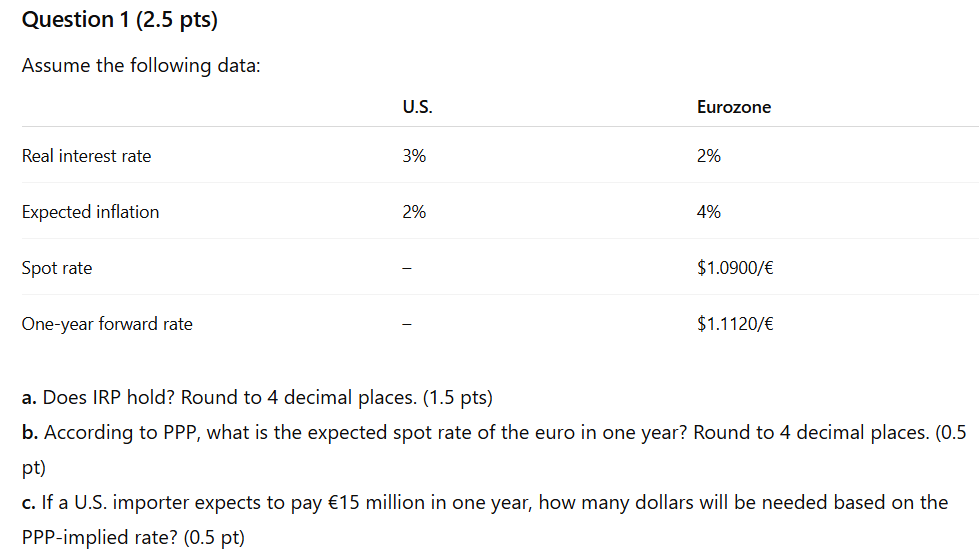

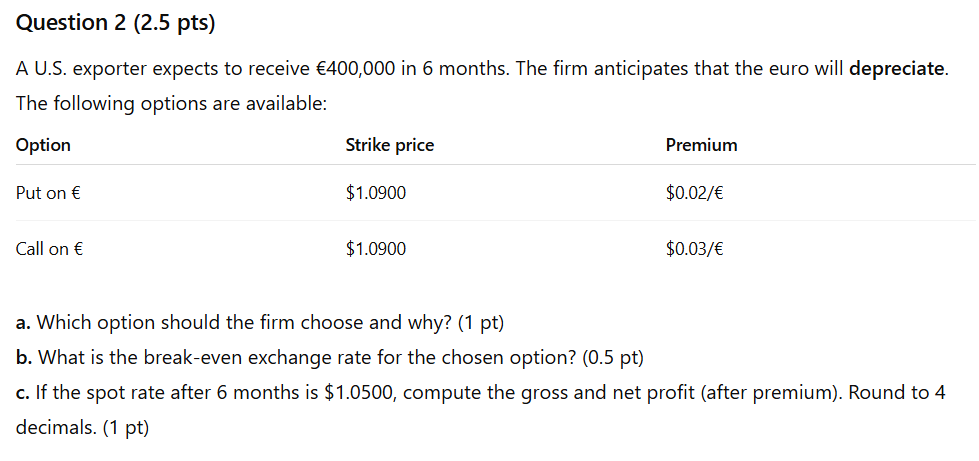

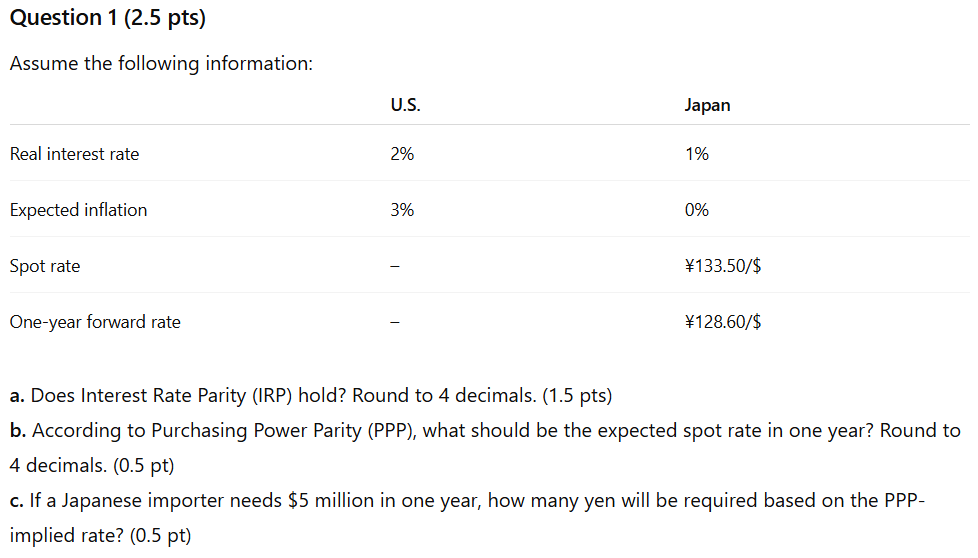

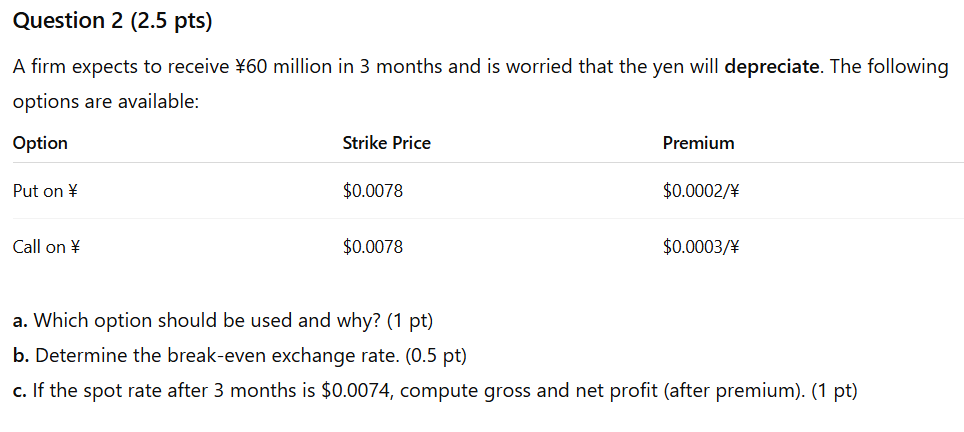

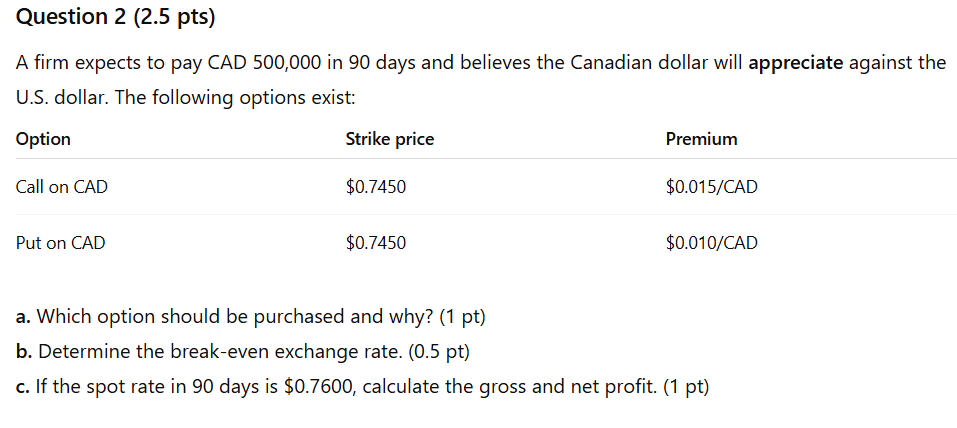

Bài tập về tài chính quốc tế

Bài tập về tài chính quốc tế. Tài liệu được tổng hơp và sưu tầm. Mời các bạn tham khảo

Môn: Tài chính quốc tế (TCQT) 14 tài liệu

Trường: Học viện Tài chính 1.1 K tài liệu

Tác giả:

Preview text:

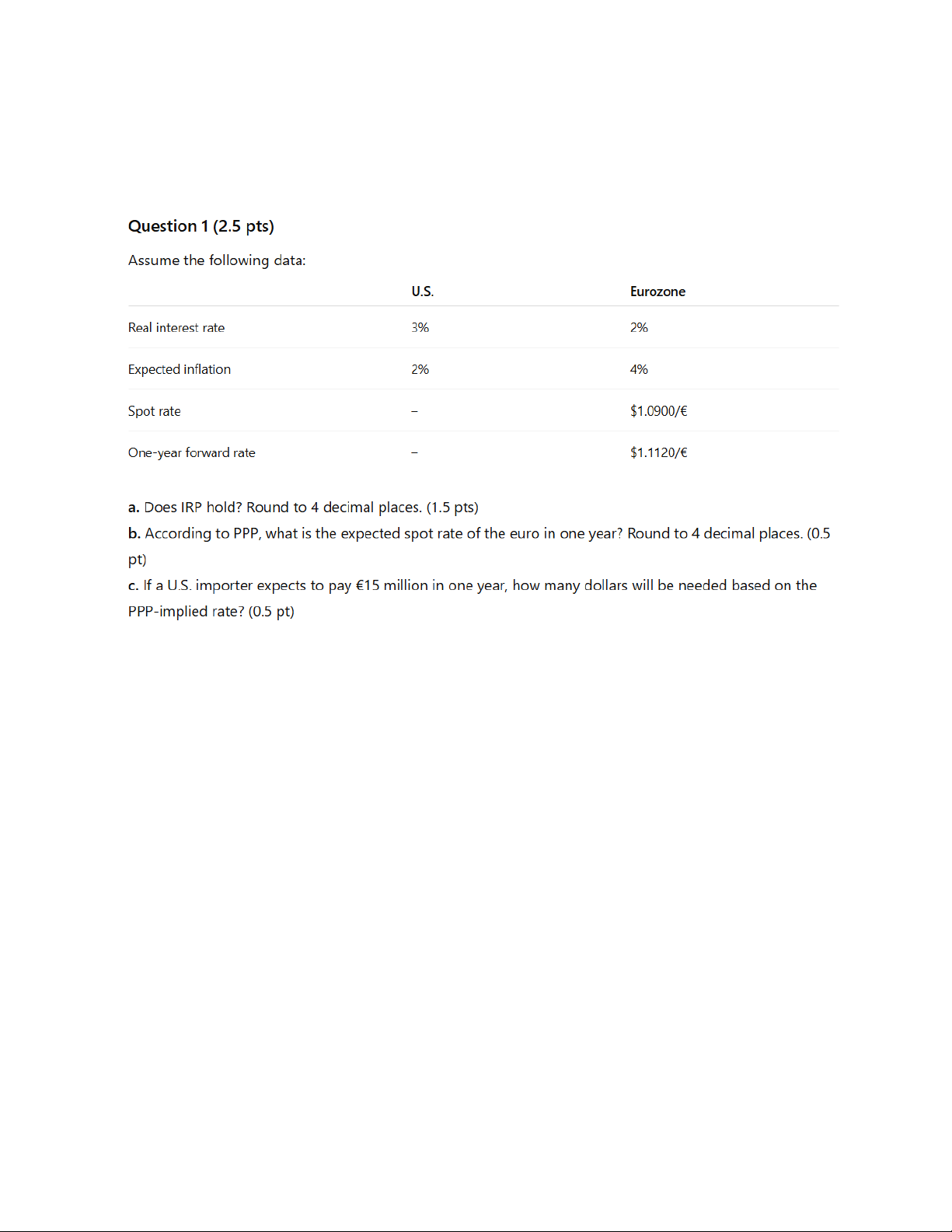

Q1.

The main goal of a multinational corporation (MNC) is:

a) To minimize global taxes.

b) To expand foreign operations.

c) To maximize shareholder wealth.

d) To maximize social welfare.

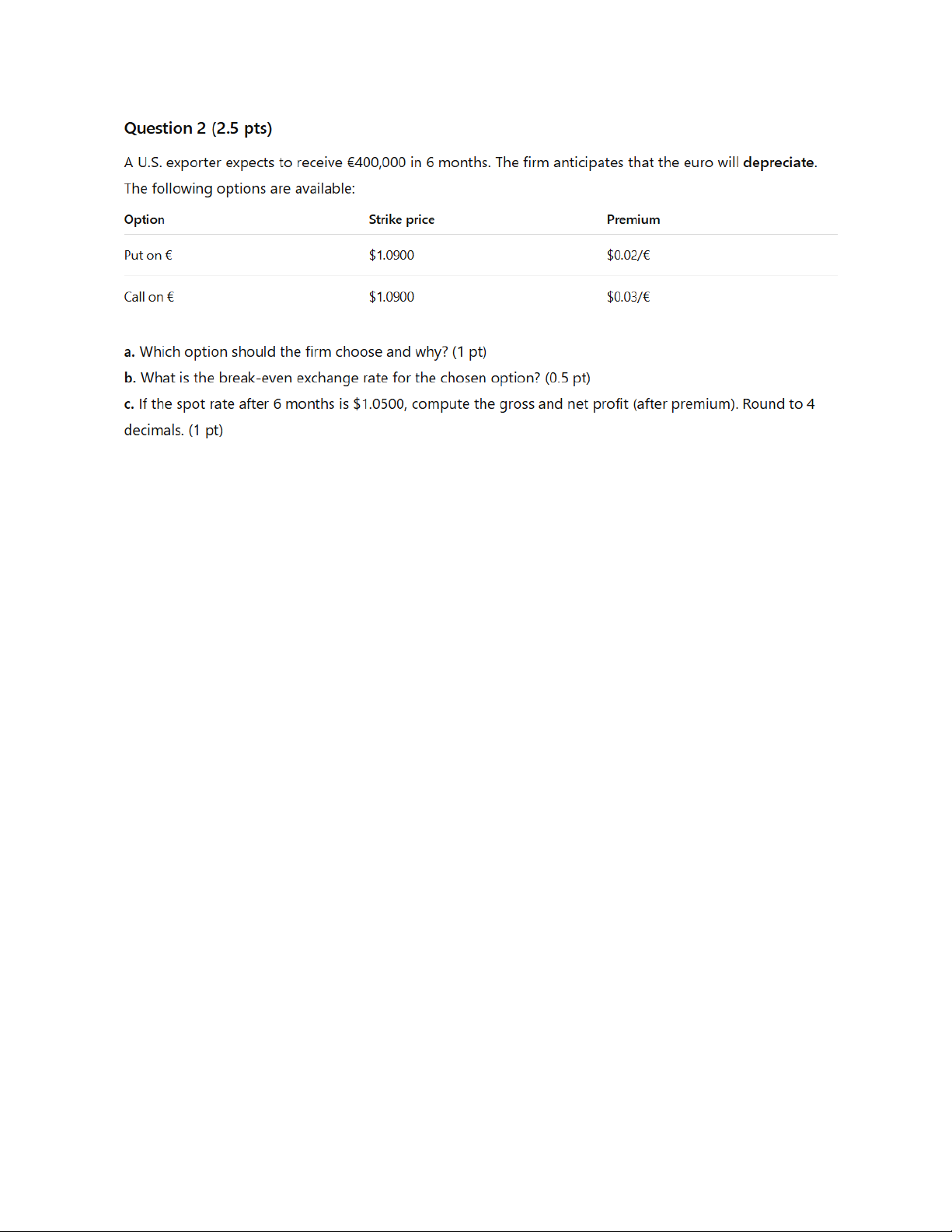

Q2.

A country's balance of payments (BOP) includes:

a) Only the current account.

b) Only the capital account.

c) Only the financial account.

d) All of the above components.

Q3.

A syndicated loan represents:

a) A loan by a single bank to a syndicate of firms.

b) A loan by a group of banks to a single borrower.

c) A loan between two governments.

d) A loan to a syndicate of exporters.

Q4.

If the bid rate for the euro is $1.10 and the ask rate is $1.12, the bid–ask spread (%) is:

a) 1.79%

b) 1.79% (≈ (1.12–1.10)/1.12×100)

c) 1.64%

d) 1.85%

Q5.

If 1 CAD = $0.75 and 1 MXN = $0.05, the value of the peso in Canadian dollars is:

a) 0.0600 CAD

b) 0.0375 CAD

c) 0.0667 CAD

d) 0.0750 CAD

Q6.

If a government imposes tariffs on imports, its current account balance will likely:

a) Decrease.

b) Remain unchanged.

c) Increase.

d) Turn into deficit.

Q7.

The difference between exports and imports of goods is called the:

a) Capital account.

b) Current account.

c) Balance of payments.

d) Balance of trade.

Q8.

A U.S. firm needing €200,000 in 60 days to pay suppliers should:

a) Sell euros forward.

b) Buy euros forward.

c) Buy euros at spot in 60 days.

d) Borrow euros.

Q9.

If a call option on the British pound costs $0.03 with a strike of $1.30, and the spot rate at expiration is $1.35, the profit per unit is:

a) $0.02

b) $0.03

c) $0.02 ($1.35 − $1.30 − $0.03)

d) $0.05

Q10.

Futures contracts are traded on organized exchanges and are therefore:

a) More standardized than forward contracts.

b) Less standardized.

c) Private agreements.

d) Always settled in cash.

Q11.

If the one-year forward rate for GBP is $1.56 and the spot rate is $1.60, the forward rate shows a:

a) 2.56% premium.

b) 2.5% discount.

c) 2.6% discount.

d) 3.0% discount.

Q12.

Which of the following is NOT a type of international arbitrage?

a) Locational arbitrage.

b) Triangular arbitrage.

c) Transactional arbitrage.

d) Covered interest arbitrage.

Q13.

Locational arbitrage exists when:

a) One bank’s bid price > another bank’s ask price.

b) One bank’s ask > another’s bid.

c) All banks quote the same price.

d) The spot rate equals forward rate.

Q14.

If interest rate parity holds and U.S. rate = 8%, U.K. rate = 5%, the forward rate on GBP should exhibit a:

a) 3% premium.

b) 3% discount.

c) 5% premium.

d) 5% discount.

Q15.

According to Purchasing Power Parity (PPP), the percentage change in the spot rate should equal:

a) Interest rate differential.

b) Exchange rate differential.

c) Inflation differential.

d) Real income differential.

Q16.

If U.S. inflation = 2%, Eurozone = 6%, and the current € rate = $1.10, the expected future rate (PPP) is:

a) $1.142

b) $1.050

c) $1.060

d) $1.120

Q17.

The real interest rate equals:

a) Nominal rate minus inflation rate.

b) Nominal rate plus inflation rate.

c) Inflation rate minus nominal rate.

d) Real GDP minus nominal GDP.

Q18.

If the U.S. imposes strict import quotas from Brazil and Brazil does not retaliate, U.S. demand for Brazilian real will:

a) Decline, and the real will depreciate.

b) Decline; real appreciates.

c) Increase; real appreciates.

d) Increase; real depreciates.

Q19.

To strengthen the domestic currency using sterilized intervention, the central bank should:

a) Buy domestic currency and sell government securities.

b) Buy foreign currency and buy securities.

c) Sell domestic currency and sell securities.

d) Sell foreign currency and buy securities.

Q20.

Under a floating exchange rate system:

a) Central bank intervention is prohibited.

b) Exchange rates are determined by market forces, but intervention is allowed.

c) The rate is fixed by government decree.

d) The exchange rate never fluctuates.

Đề số 2

Q1.

The foreign exchange market is:

a) Located only in New York and London.

b) A global network of financial institutions trading currencies.

c) A physical market for exchanging banknotes.

d) Controlled entirely by central banks.

Q2.

A direct quotation in the U.S. means:

a) The amount of U.S. dollars per one unit of foreign currency.

b) The number of foreign currency units per dollar.

c) The domestic interest rate.

d) None of the above.

Q3.

An increase in the U.S. interest rate, ceteris paribus, will likely cause the dollar to:

a) Depreciate.

b) Appreciate.

c) Stay constant.

d) Be unaffected.

Q4.

Which of the following would most likely decrease the value of a country’s currency?

a) A decrease in inflation.

b) Higher interest rates.

c) A decrease in exports.

d) A trade surplus.

Q5.

The spot rate of a currency is:

a) The future expected rate.

b) The rate for immediate delivery.

c) The average of bid and ask quotes.

d) The long-term equilibrium rate.

Q6.

If a euro is quoted at $1.20 in New York and $1.18 in London, arbitrageurs can:

a) Buy euros in London and sell them in New York.

b) Buy in New York and sell in London.

c) Buy dollars in London.

d) None of the above.

Q7.

The forward rate usually differs from the spot rate due to:

a) Inflation differential.

b) Interest rate differential.

c) Political risk.

d) Market manipulation.

Q8.

Interest Rate Parity (IRP) implies:

a) Equal interest rates across countries.

b) Equal inflation rates.

c) Covered interest arbitrage is not possible.

d) Forward rate = spot rate.

Q9.

If the U.S. inflation rate is lower than Japan’s, the dollar should:

a) Appreciate.

b) Depreciate.

c) Remain constant.

d) Have no relation.

Q10.

A currency option gives the holder the right to:

a) Buy or sell a currency at a specified price.

b) Exchange interest rates.

c) Force another party to transact.

d) Avoid all losses.

Q11.

A call option on the euro benefits the holder if:

a) The euro depreciates.

b) The euro appreciates.

c) The euro is stable.

d) Volatility decreases.

Q12.

A put option on the British pound benefits the holder if:

a) The pound appreciates.

b) It is stable.

c) The pound depreciates.

d) Inflation rises.

Q13.

The primary purpose of a forward hedge is to:

a) Eliminate exchange rate risk.

b) Increase profits from speculation.

c) Exploit arbitrage.

d) Reduce transaction volume.

Q14.

The Fisher Effect suggests:

a) Nominal interest rates reflect expected inflation plus real rate.

b) Real rates equal nominal rates.

c) Inflation equals nominal minus real rates.

d) Interest rates are unrelated to inflation.

Q15.

If IRP holds and the U.S. rate is 4%, the U.K. rate is 6%, then the pound should sell at a:

a) 1.89% forward discount.

b) 2% premium.

c) 1.5% discount.

d) 3% premium.

Q16.

If the spot rate of the yen = $0.0090 and the 6-month forward rate = $0.0093, the forward:

a) Shows a 3.3% premium.

b) Shows a 3.3% discount.

c) Equals spot.

d) Is undervalued.

Q17.

When a currency is overvalued, its exports become:

a) More expensive abroad.

b) Cheaper abroad.

c) Unchanged.

d) Subsidized by the government.

Q18.

The current account includes:

a) Trade in goods and services.

b) Income receipts and payments.

c) Transfers (like remittances).

d) All of the above.

Q19.

A capital account surplus indicates:

a) More inflows of capital than outflows.

b) Net inflow of capital investment.

c) More imports than exports.

d) A trade surplus.

Q20.

Under a fixed exchange rate system, the central bank must:

a) Intervene to maintain the target rate.

b) Allow free market forces.

c) Never buy or sell reserves.

d) Abolish monetary policy.

Đề số 3

Q1.

The law of one price assumes:

a) Transportation costs exist.

b) Goods are non-tradable.

c) Identical goods should cost the same in different countries when priced in the same currency.

d) Exchange rates are fixed.

Q2.

The covered interest arbitrage condition ensures that:

a) Interest rate differentials are offset by forward premiums or discounts.

b) Inflation is equal across countries.

c) Exchange rates are fixed.

d) Central banks intervene constantly.

Q3.

If the spot USD/CHF = 0.9000 and the 1-year forward = 0.9180, the franc exhibits a:

a) 2% premium.

b) 2% discount.

c) 1.8% discount.

d) 1.8% premium.

Q4.

If the euro interest rate = 3% and the dollar rate = 5%, IRP implies the euro forward rate should be:

a) At a 1.94% premium.

b) 2% discount.

c) Equal to spot.

d) 3% discount.

Q5.

An appreciation of the home currency will:

a) Increase export competitiveness.

b) Reduce export competitiveness.

c) Have no effect on imports.

d) Increase inflation.

Q6.

A depreciation of the domestic currency tends to:

a) Lower import prices.

b) Increase export competitiveness.

c) Reduce inflation.

d) Lower interest rates.

Q7.

If the U.S. runs a current account deficit, it must:

a) Be a net lender to the world.

b) Finance it with a financial account surplus.

c) Have a balanced capital account.

d) Reduce government spending.

Q8.

The spot rate between two currencies changes mainly due to:

a) Changes in supply and demand.

b) Central bank regulation only.

c) Random fluctuations only.

d) Fixed government policy.

Q9.

An investor expecting the euro to appreciate should:

a) Buy euros forward or buy euro call options.

b) Sell euros forward.

c) Buy euro puts.

d) Borrow euros.

Q10.

A country with high inflation relative to others will see its currency:

a) Depreciate.

b) Appreciate.

c) Unchanged.

d) Strengthened by exports.

Q11.

An increase in income levels in a country typically causes its currency to:

a) Depreciate due to higher imports.

b) Appreciate.

c) Remain stable.

d) Strengthen from capital inflows.

Q12.

A floating exchange rate means:

a) Fixed by central bank.

b) Determined by market forces.

c) Always stable.

d) Set by IMF rules.

Q13.

A currency board system is:

a) A freely floating system.

b) A fixed-rate system backed by foreign reserves.

c) A monetary union.

d) Managed float.

Q14.

Which of the following increases demand for a foreign currency?

a) Higher domestic inflation.

b) Increase in domestic income.

c) Trade restrictions.

d) Lower foreign interest rates.

Q15.

A country’s currency depreciates when its interest rate:

a) Rises relative to others.

b) Falls relative to others.

c) Is equal to foreign rates.

d) Becomes negative.

Q16.

In an efficient foreign exchange market, exchange rates:

a) Are predictable using past prices.

b) Already reflect all available information.

c) Are controlled by the IMF.

d) Follow fixed government rules.

Q17.

If the U.S. dollar strengthens against the yen, Japanese imports into the U.S. become:

a) Cheaper in dollar terms.

b) More expensive.

c) Unchanged.

d) Subsidized.

Q18.

The exchange rate risk faced by a firm with future foreign-currency payables is:

a) None.

b) Transaction exposure.

c) Translation exposure.

d) Economic exposure only.

Q19.

The purchasing power parity theory fails in the short run mainly because:

a) Market frictions and non-traded goods.

b) Inflation always identical.

c) No speculative flows.

d) Interest parity fails.

Q20.

When a central bank buys foreign currency in the market, its own currency tends to:

a) Depreciate.

b) Appreciate.

c) Stay constant.

d) Strengthen.

Tài liệu liên quan:

-

Phân Tích Báo Cáo Tài Chính Công Ty Vinamilk - Tiểu Luận UEH

28 14 -

Tài liệu tài chính quốc tế | Học viện Tài chính

45 23 -

Trắc nghiệm Thị trường Tài chính Quốc tế và Đầu tư | Tài chính quốc tế | Học viện Tài chính

84 42 -

Ôn tập tài chính quốc tế và tỉ giá hối đoái | Tài chính quốc tế | Học viện Tài chính

70 35