Bài thuyết trình thống kê ứng dụng

bảng thuyết trình hoàn chỉnh thú vị

Môn: Xác suất thống kê (XSTK19) 39 tài liệu

Trường: Trường Đại học Mở Thành phố Hồ Chí Minh 704 tài liệu

Tác giả:

Preview text:

Statistic for economics and finance Instructor: Pham Ha Forecasting with Time Series Analysis Chapter 5 5-1 Learning Objectives

LO5-1 Identify and describe time series patterns.

LO5-2 Compute forecasting using simple moving averages.

LO5-3 Compute and interpret the Mean Absolute Deviation.

LO5-4 Compute forecasts using exponential smoothing.

LO5-5 Compute a forecasting model using regression analysis.

LO5-6 Apply the Durban-Watson statistic to test for autocorrelation.

LO5-7 Compute seasonal indexes and use the indexes to

make seasonally adjusted forecasts. 5-2 Components of a Time Series

A time series is a collection of data over a period of time

The trend is the long-run direction of the time series

TREND PATTERN The change of a variable over time.

The seasonal variation is a pattern that tends to repeat

itself from year to year for most businesses

SEASONALITY Patterns of highs and lows in a time series within a

calendar year. These patterns tend to repeat each year. 5-3

Components of a Time Series Continued

The cyclical component is the fluctuation above and

below the long-term trend line over a longer time period

CYCLES A pattern of highs and lows occurring over periods of many years.

The irregular variation is divided into episodic and residual components

IRREGULAR COMPONENT The random variation in a time series. 5-4 Secular Trend Examples

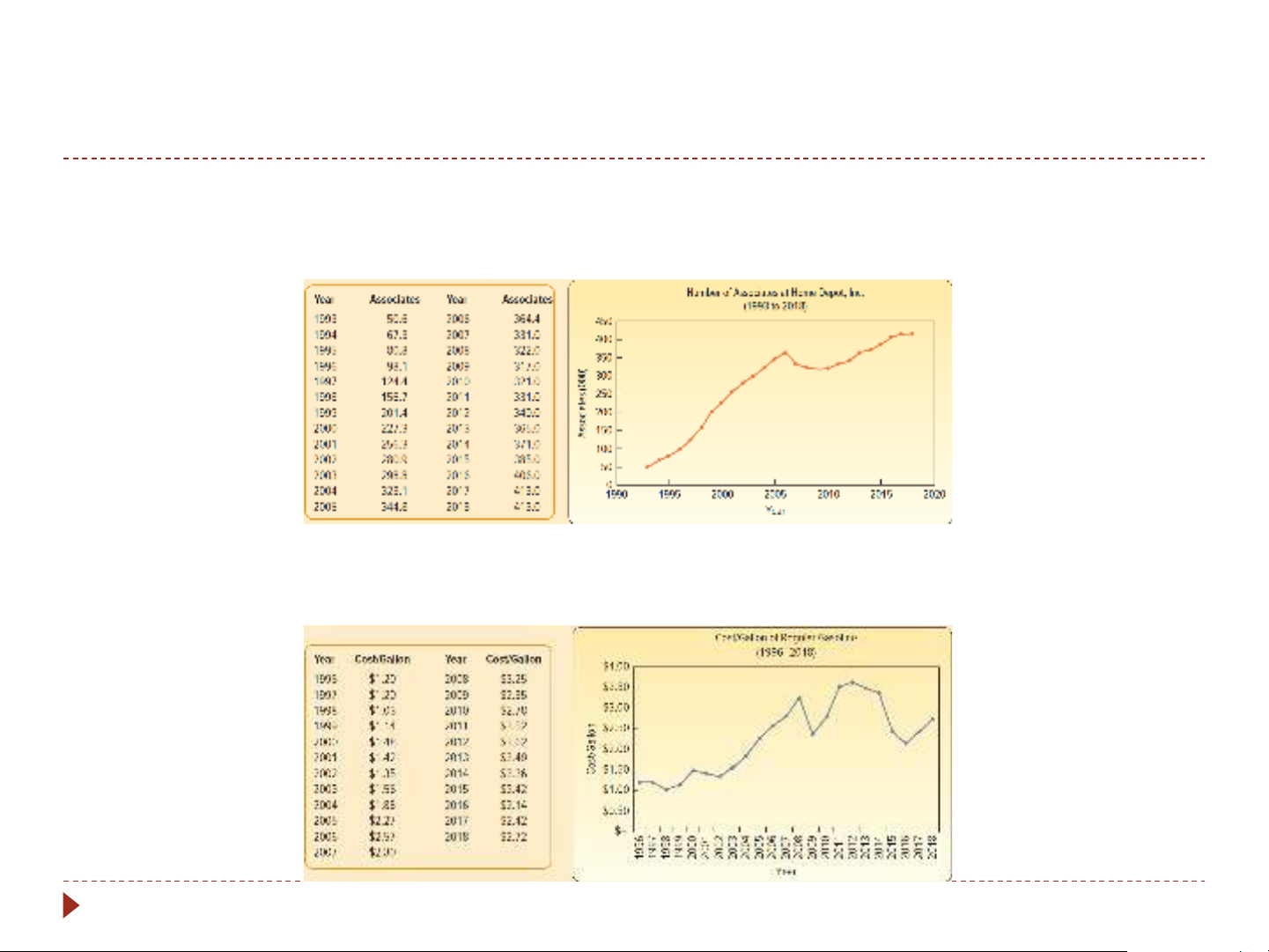

A graph of the secular trend of the number of Home Depot

associates shows how the number has increased over time

The average price of gasoline increased from 2005 to 2013 and since then has declined 5-5 Seasonality Example

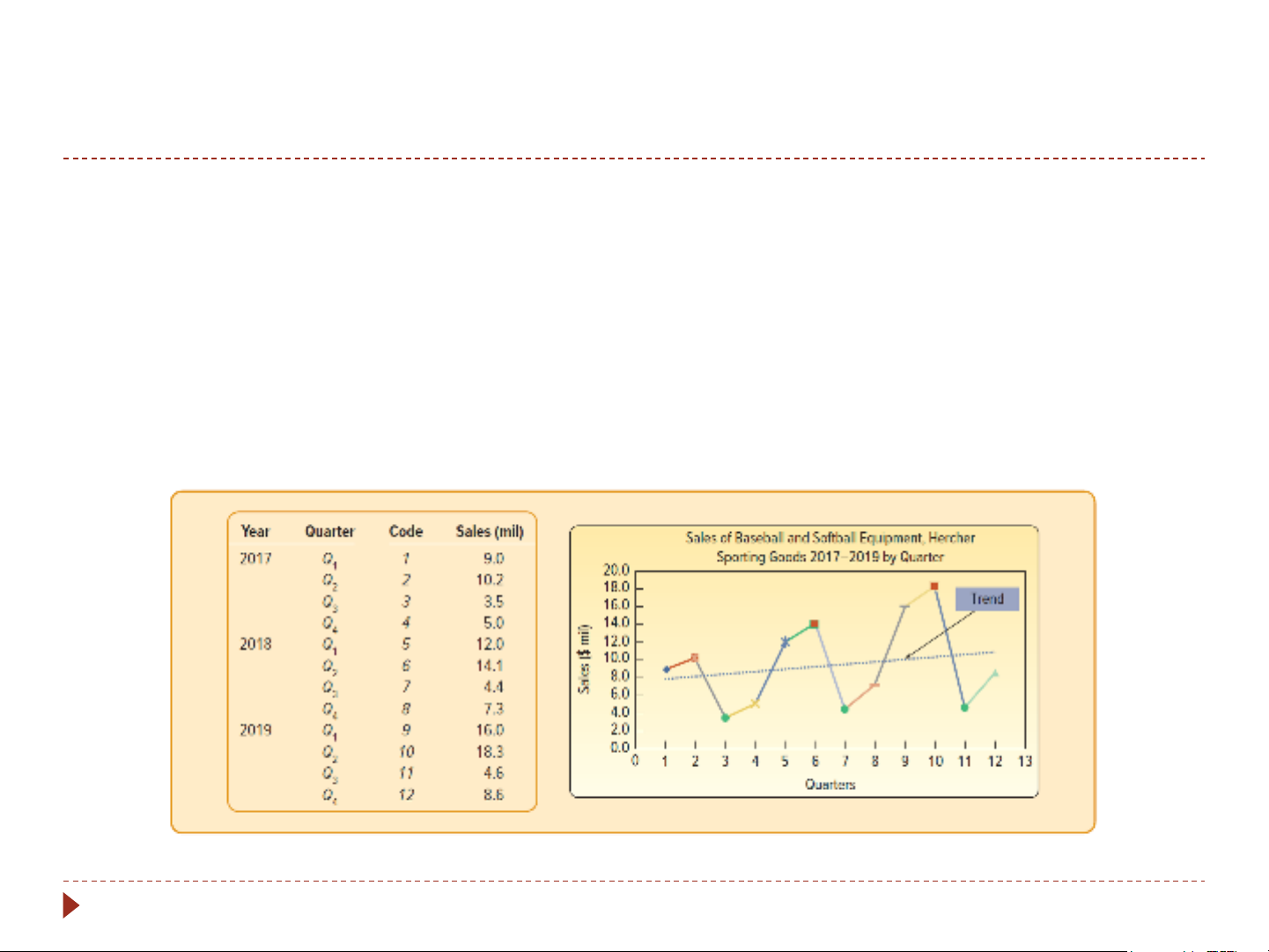

Almost all businesses tend to have recurring seasonal patterns

Men’s and women’s apparel have high sales right before

Christmas and low sales in January

Sporting good stores will have seasonal fluctuations 5-6 Cyclical Variation Example

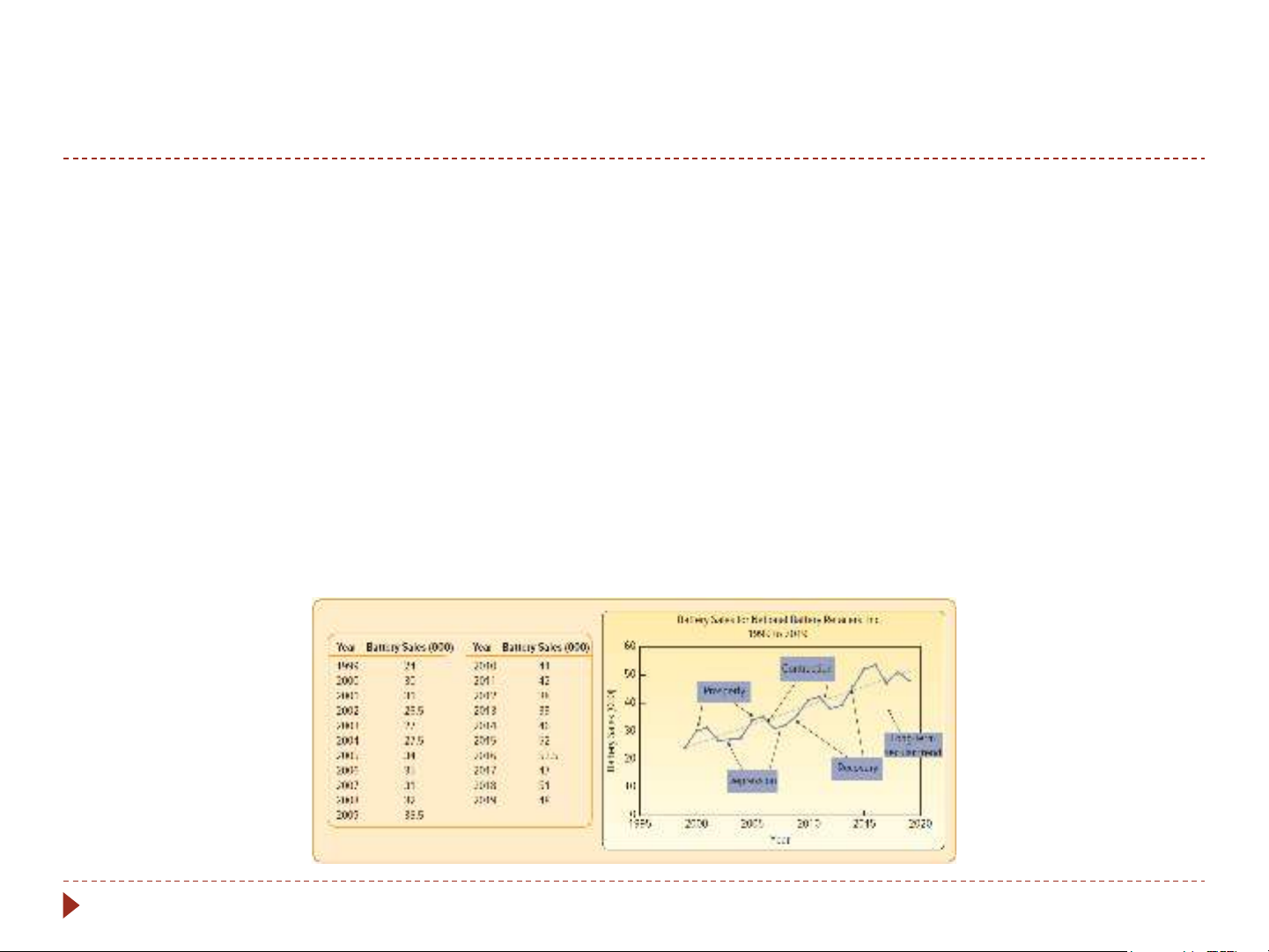

A typical business cycle consists of a period of prosperity

followed by periods of recession, depression, and then recovery

In periods of recession, employment, production, the

DJIA, and other business and economic series are below the long-term trend lines

In times of prosperity, they are above the long-term trend lines 5-7 Moving Averages

A moving average is used to smooth the trend in a time series

It is the basic method used in measuring seasonal fluctuation

To apply a moving average, the data needs to follow a

fairly linear trend and have a rhythmic pattern of fluctuations

This is accomplished by “moving” the mean values through the time series 5-8 Moving Average Example

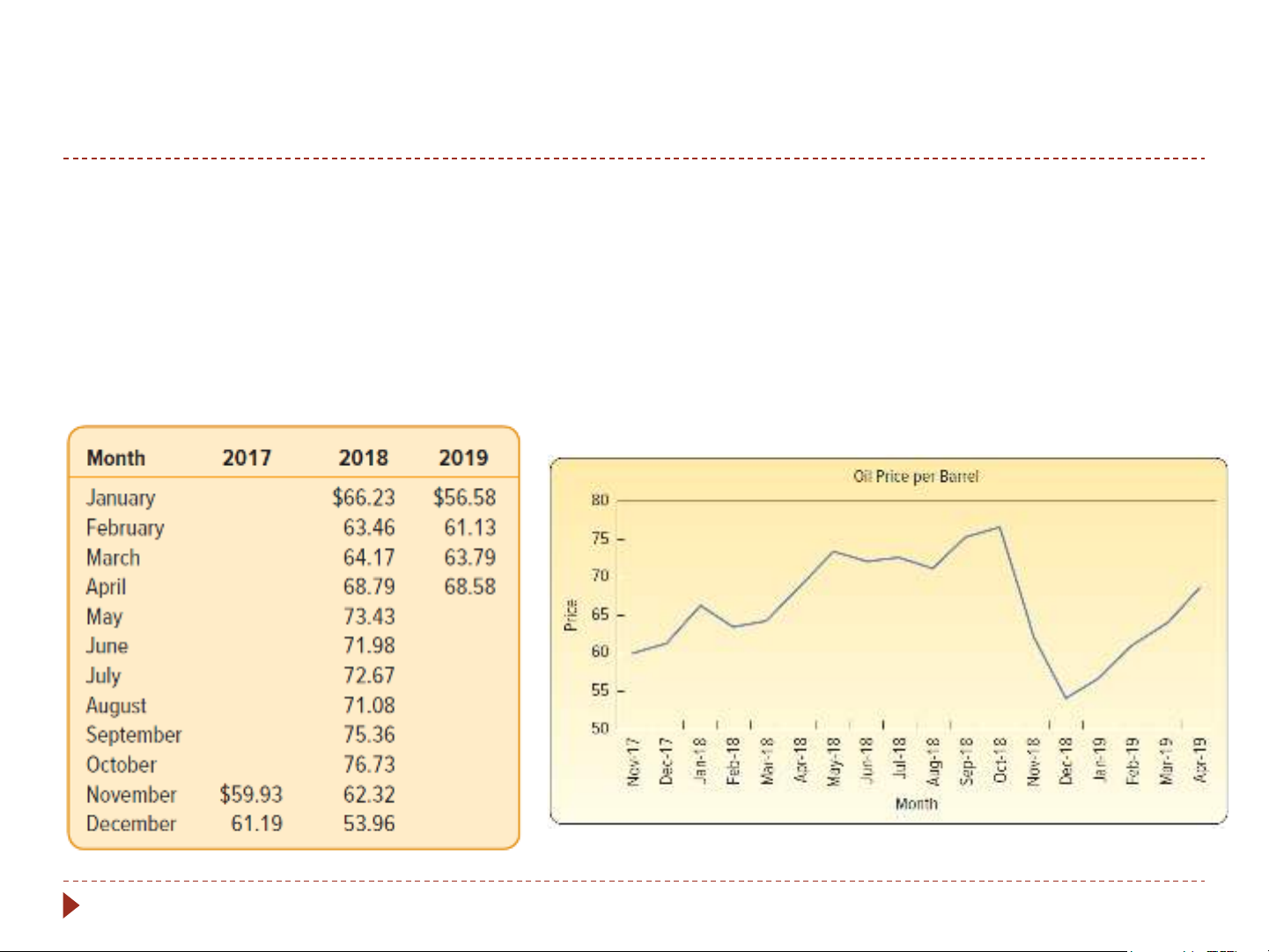

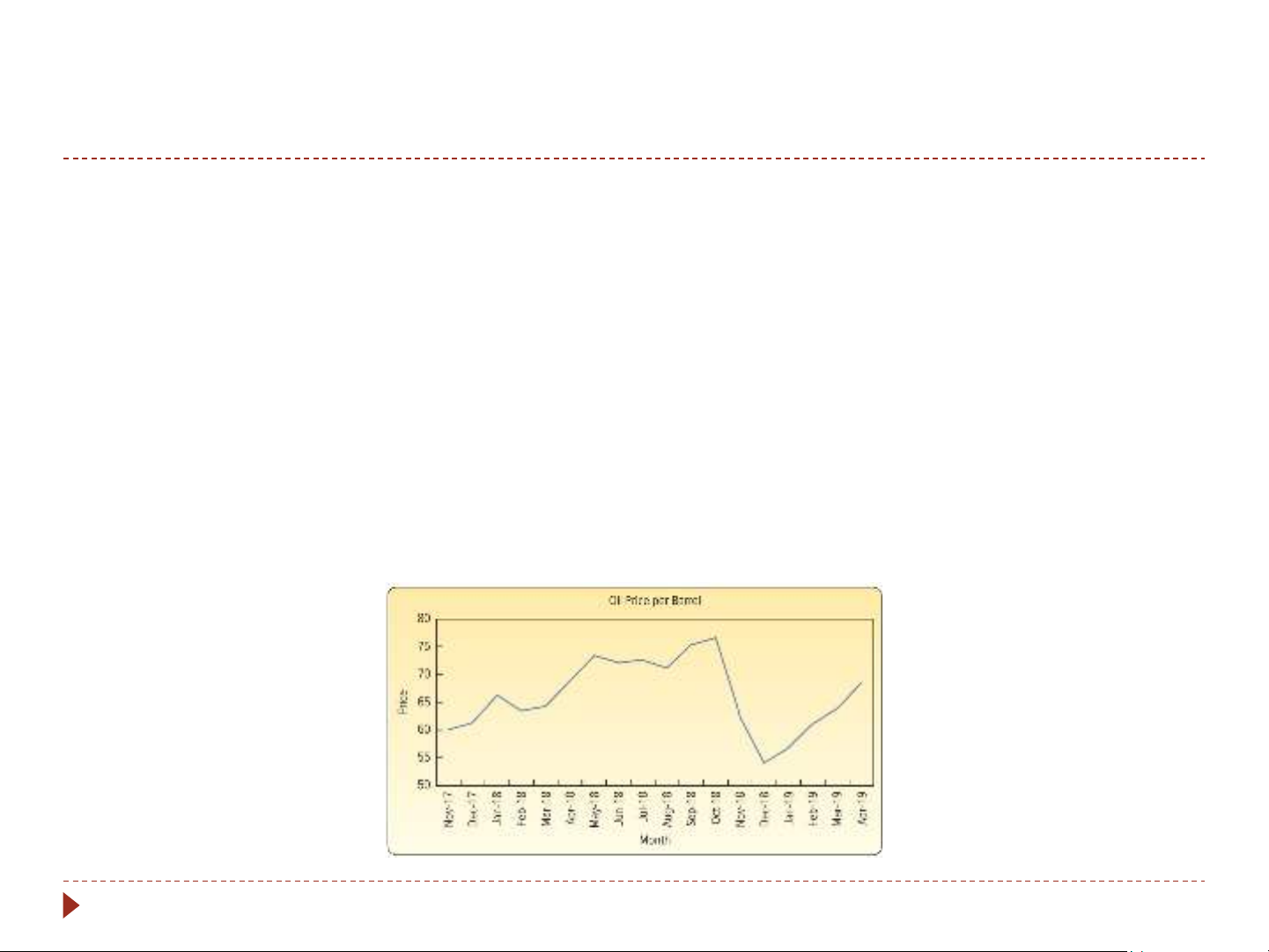

Shown is a time series of the monthly market price for a

barrel of oil over 18 months. Use a three-period and a six-

period simple moving average to forecast the oil price for May 2019. 5-9

3- and 6- Period Moving Average Example

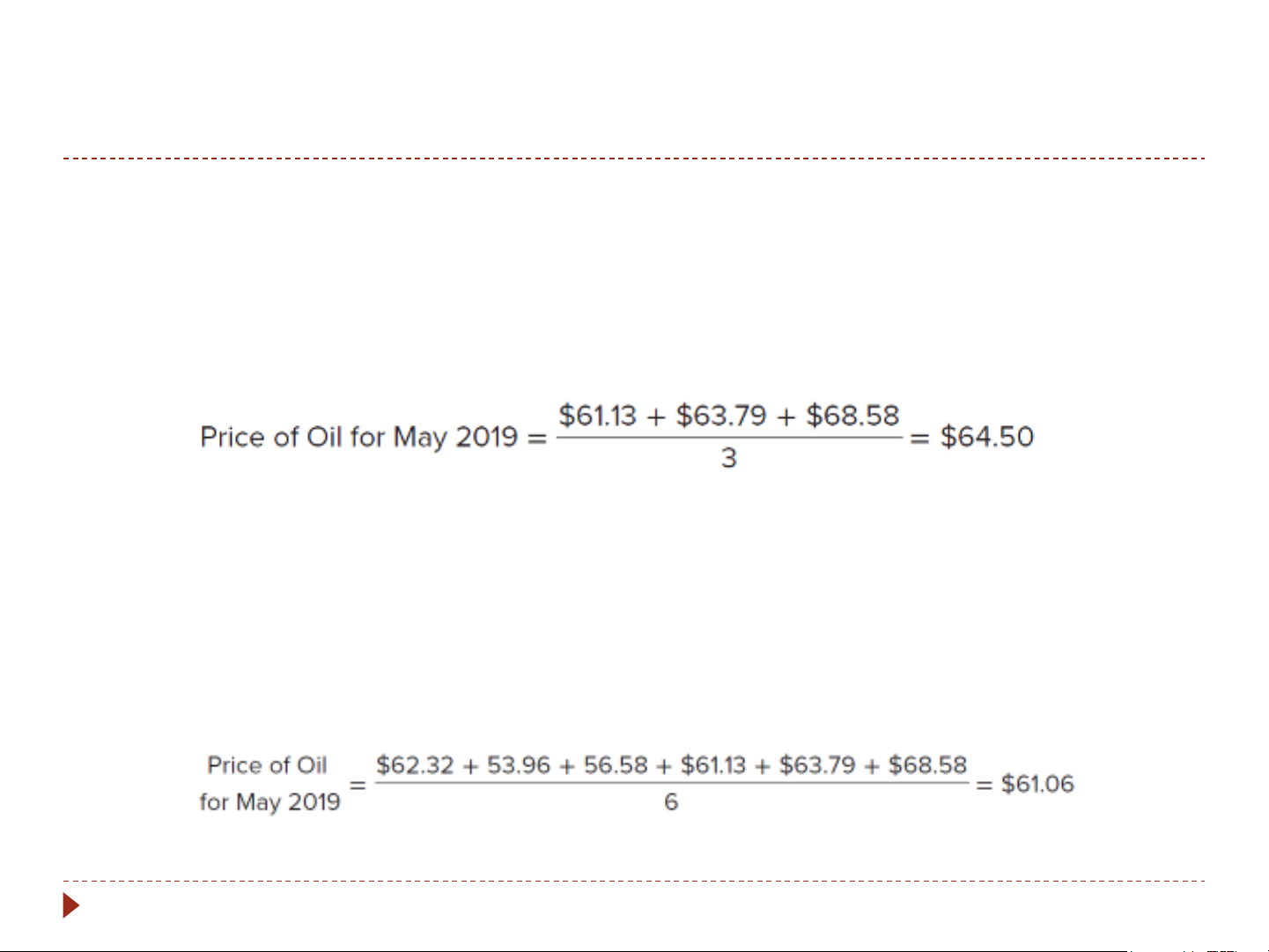

Using a three-period simple moving average, the forecast for

May 2019 would be the average of the prices from the most

recent 3 months: February, March, and April of 2019. The

forecast is computed as follows:

Using a six-period simple moving average, the forecast for May

2019 would be the average of the prices from the most recent

6 months: November, December, January, February, March, and

April of 2019. The forecast is computed as follows: 5-10 Forecasting Error

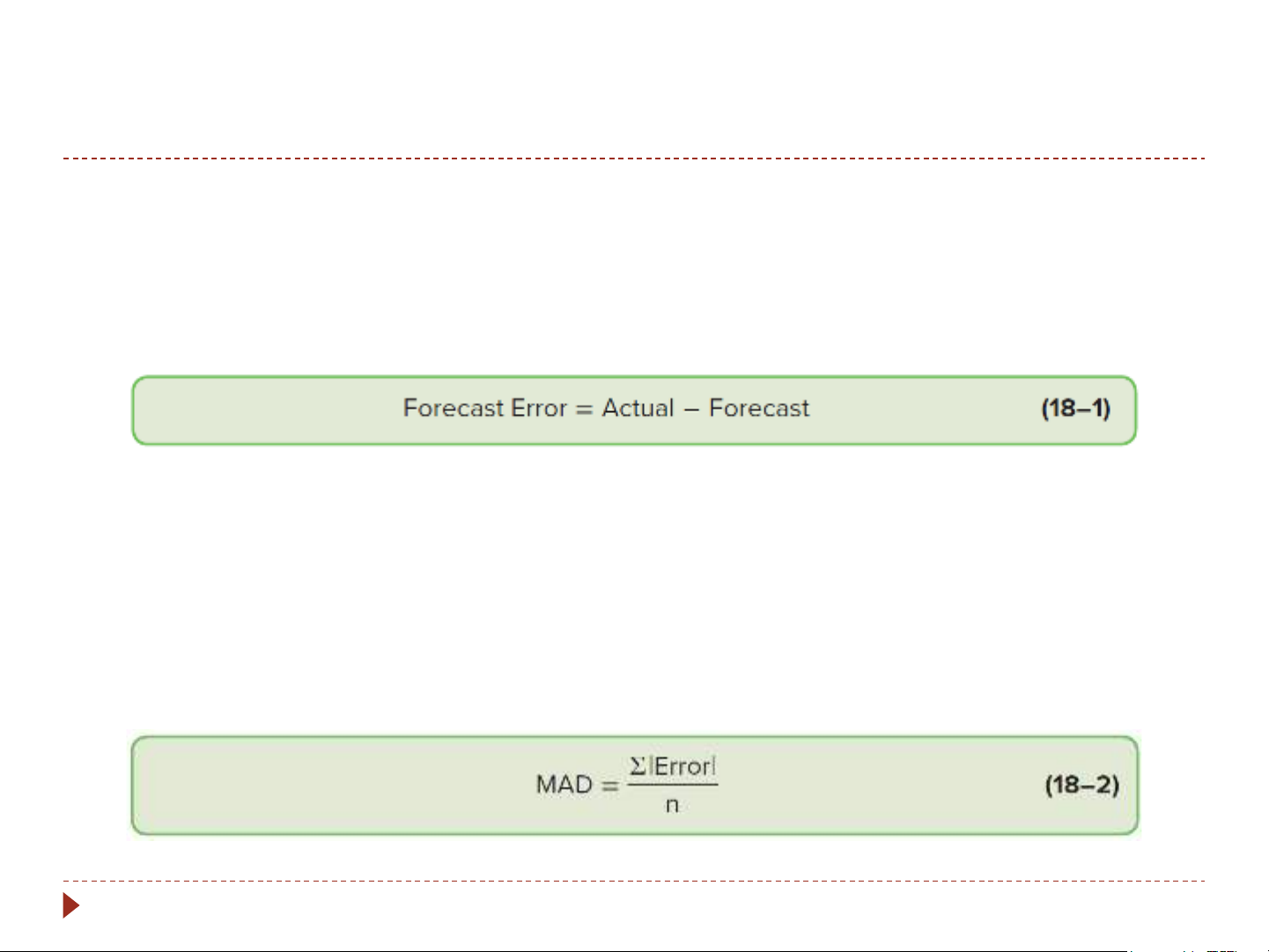

Any estimate or forecast is likely to be imprecise. The

error, or lack of precision, is the difference between the

actual observation and the forecast.

This difference is called a deviation of the forecast from the actual value.

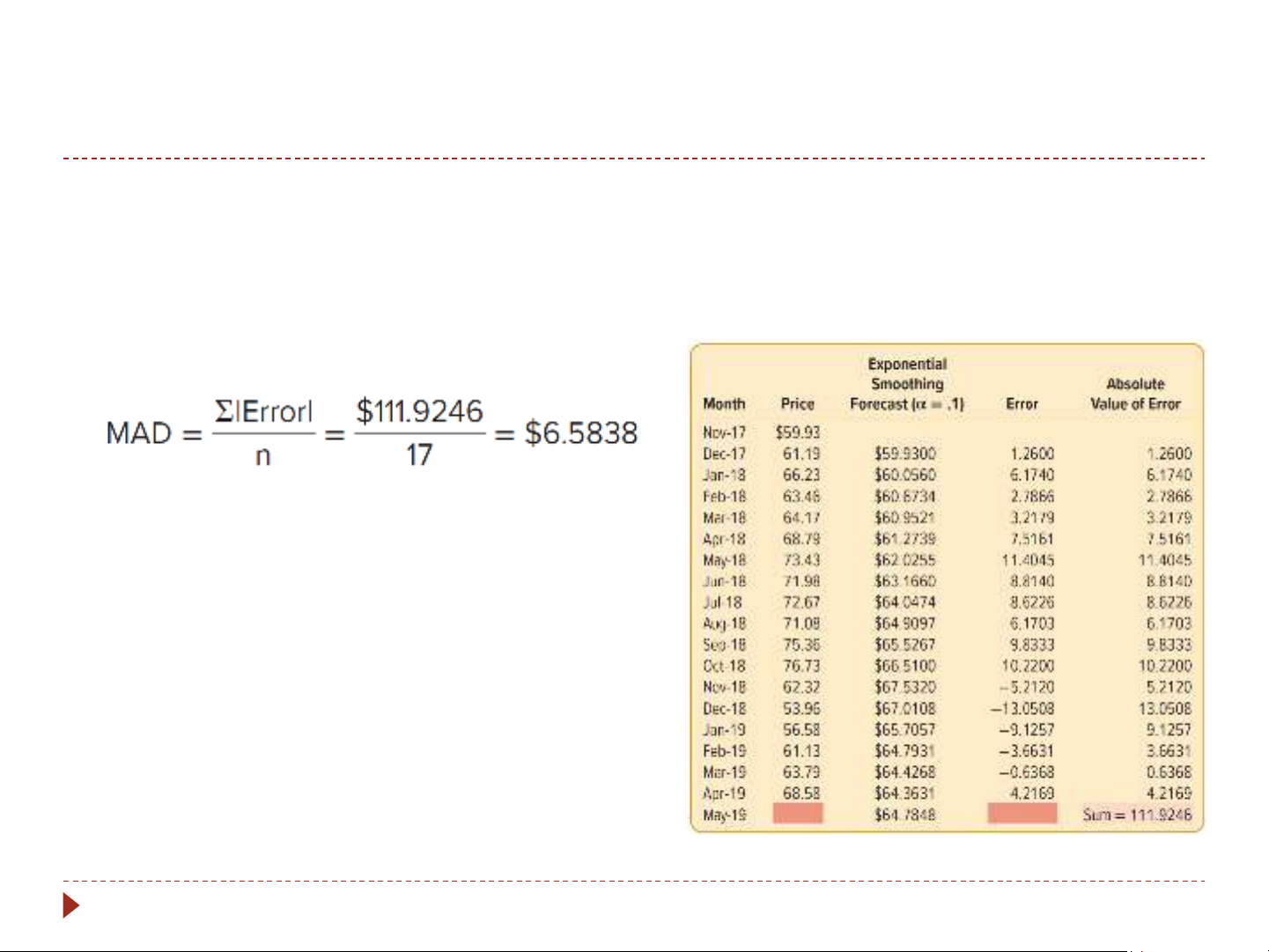

The mean of the absolute errors is called the mean absolute deviation (MAD). 5-11

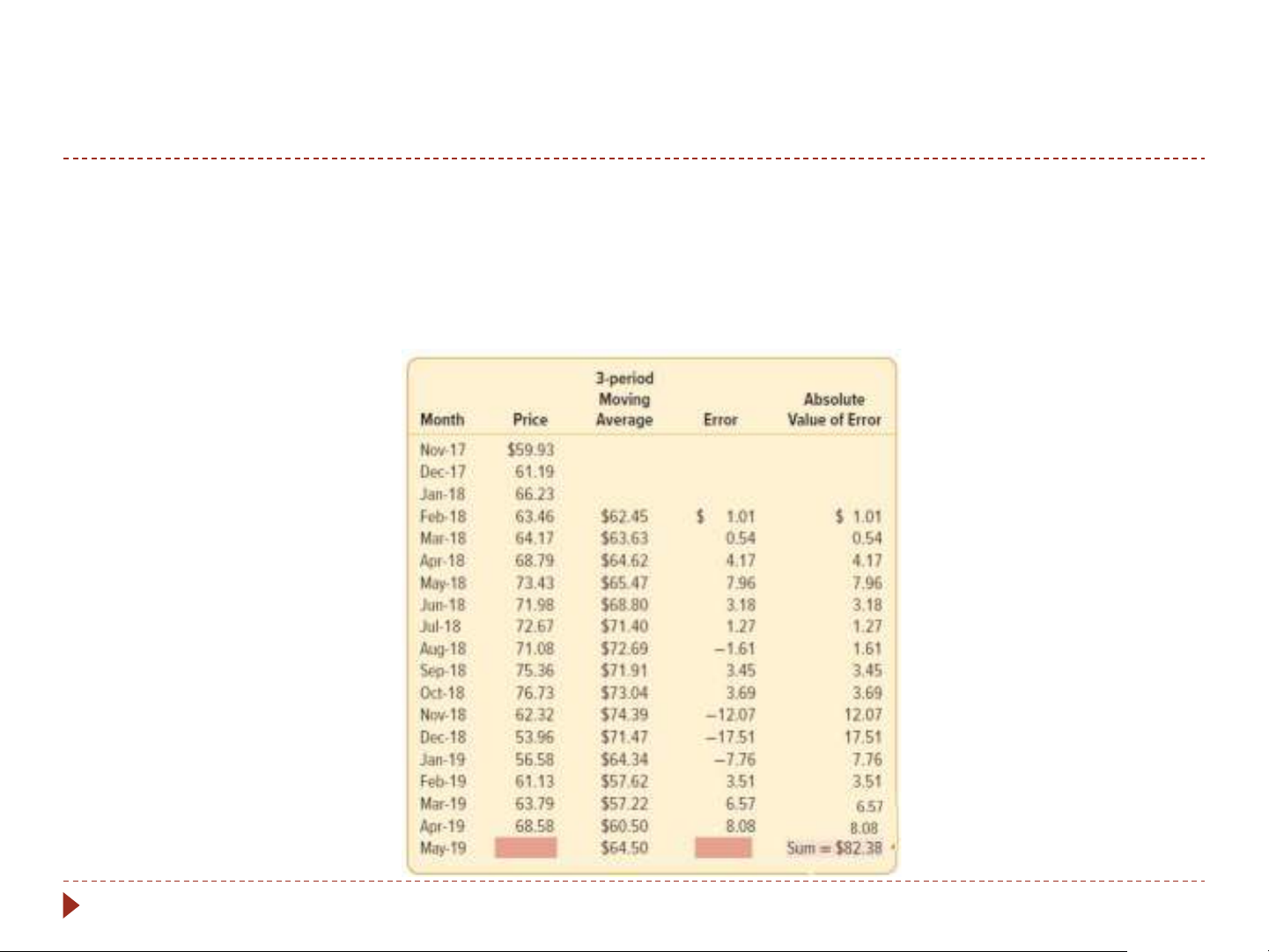

3-Period Moving Average Including Error

We report that the forecast for May 2019 is $64.50 with a MAD of $5.49.

Using a three-period simple moving average, we can expect the forecasted

May 2019 oil price to be between $59.01 (found by $64.50 − $5.49) and

$69.99 (found by $64.50 + $5.49). 5-12

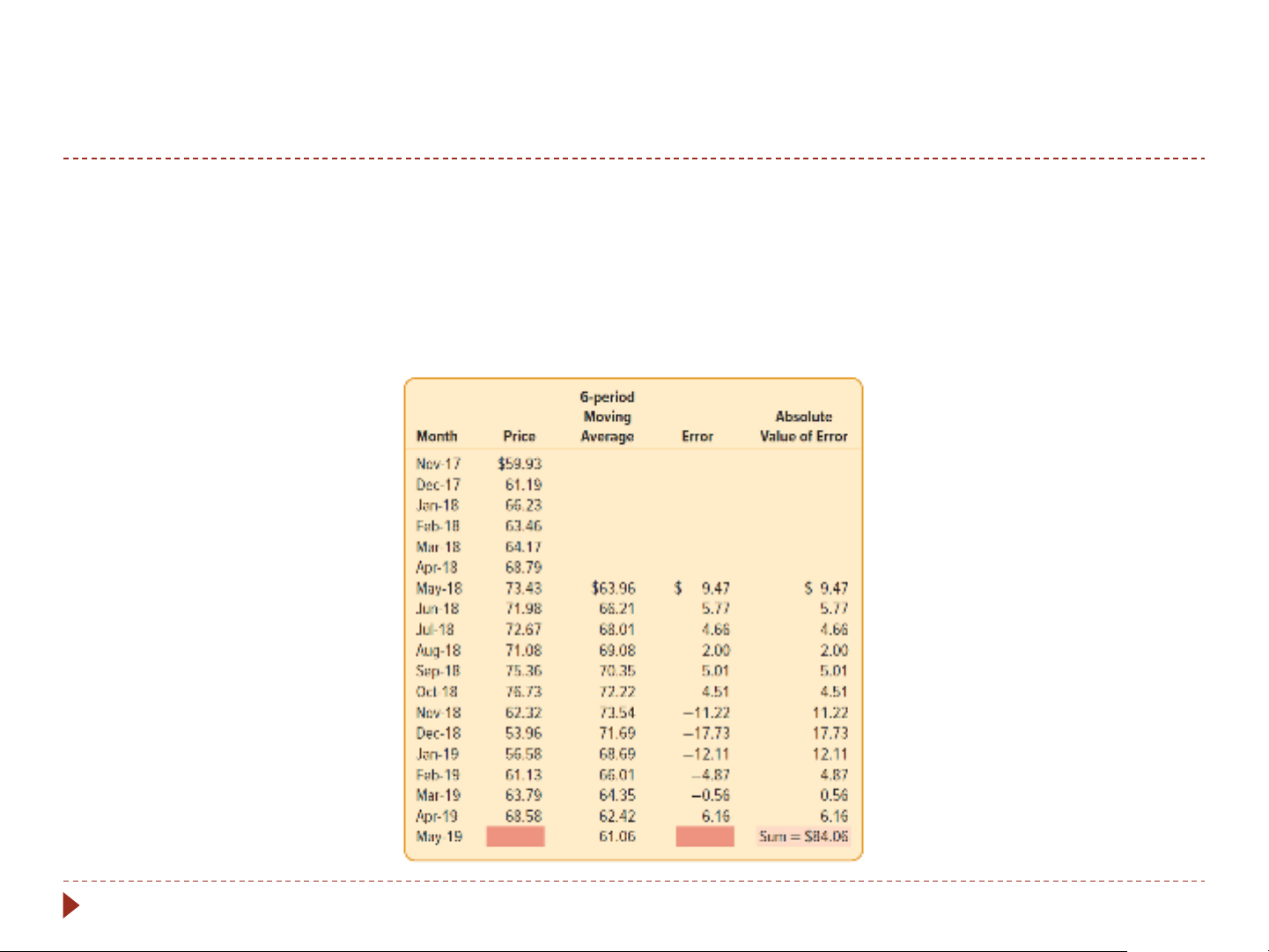

6-Period Moving Average Including Error

Using a 6-month moving average model, the MAD or the average variability

of forecast error is $7.01. Recalling that the 6-month moving average

forecast for May 2019 is $61.06, we can expect the forecasted May 2019 oil

price to be between $54.05 (found by $61.06 − $7.01) and $68.07 (found by $61.06 + $7.01). 5-13

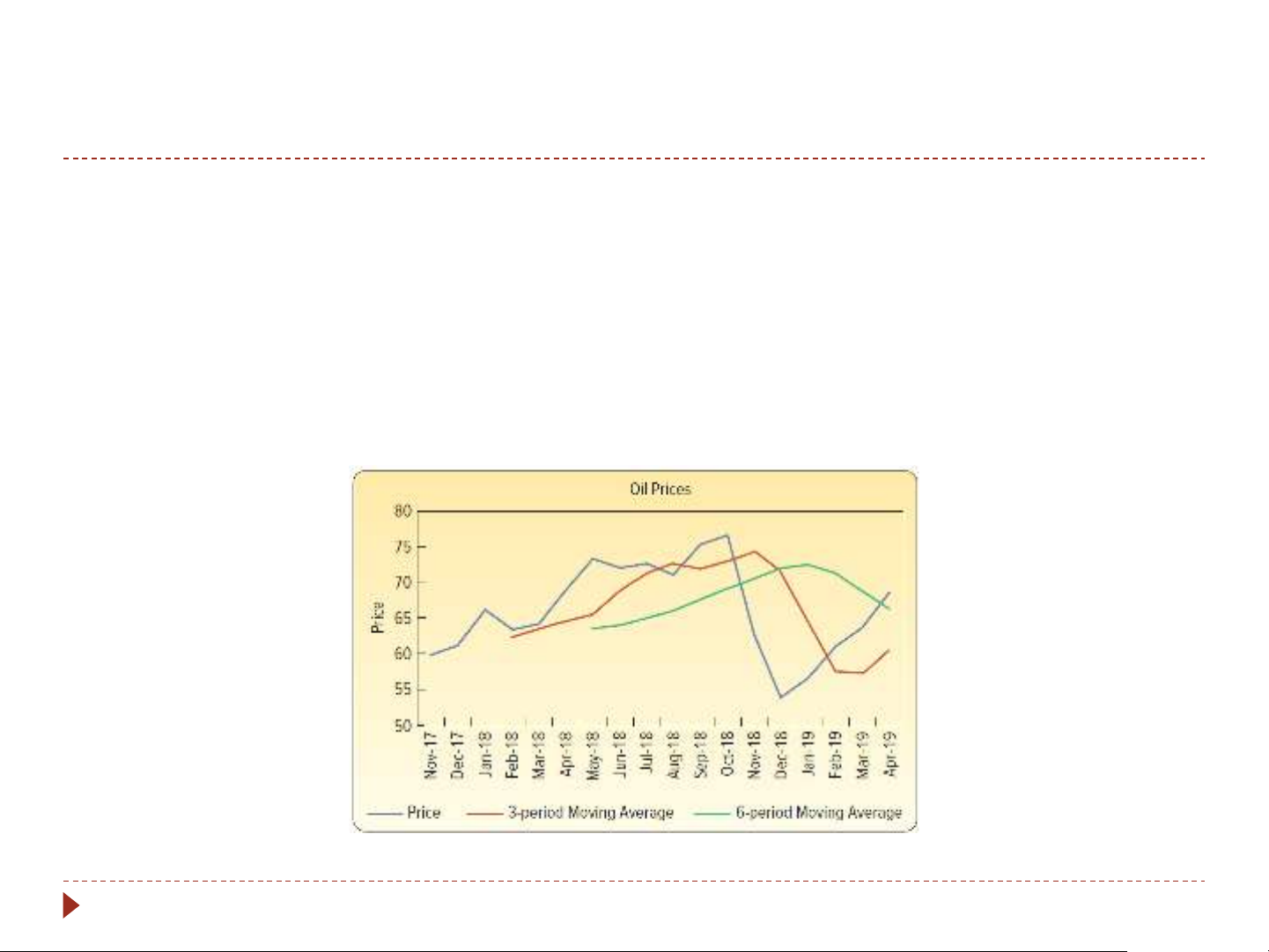

Simple Moving Average Comparison

An outcome of using more periods in a simple moving average

is its effect on the variation of the forecasts.

The variation in the forecasts is related to the number of

observations in a simple moving average. More periods will

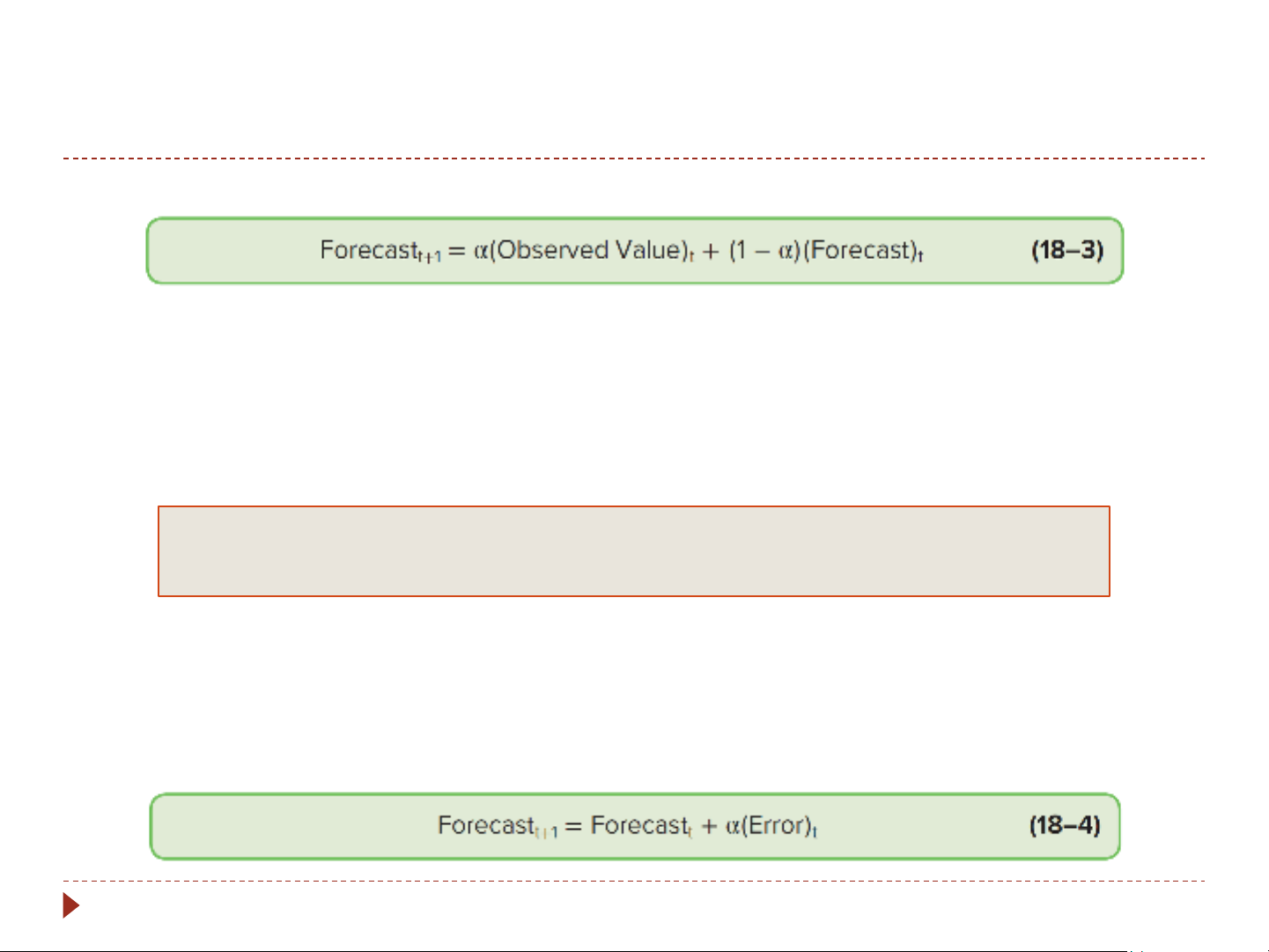

reduce the variation in the forecasts. 5-14 Simple Exponential Smoothing t = time period t+1 = next time period

Alpha (α) = smoothing constant

SMOOTHING CONSTANT A value applied in exponential smoothing

to determine the weights assigned to past observations.

Smoothing constant is between 0 and 1

Selecting a smoothing constant value near 1 means that recent

data will receive more weight than older data. 5-15

Simple Exponential Smoothing Example

Using simple exponential smoothing with a smoothing

constant of 0.1, the exponential smoothing equation would be: Forecast = Forecast + 0.1(error) t+1 t t

The forecast for January 2018 is: Forecast = Forecast + 0.1(error) January December December Forecast

= $59.93 + 0.1($1.26) = $60.0560 January Forecast Error

= $66.23 − $60.06 = $6.1740 January 5-16

Simple Exponential Smoothing Example Continued

The smoothing formula is applied through the time series

data until the last possible forecast for May 2019 is made. MAD is then computed: 5-17

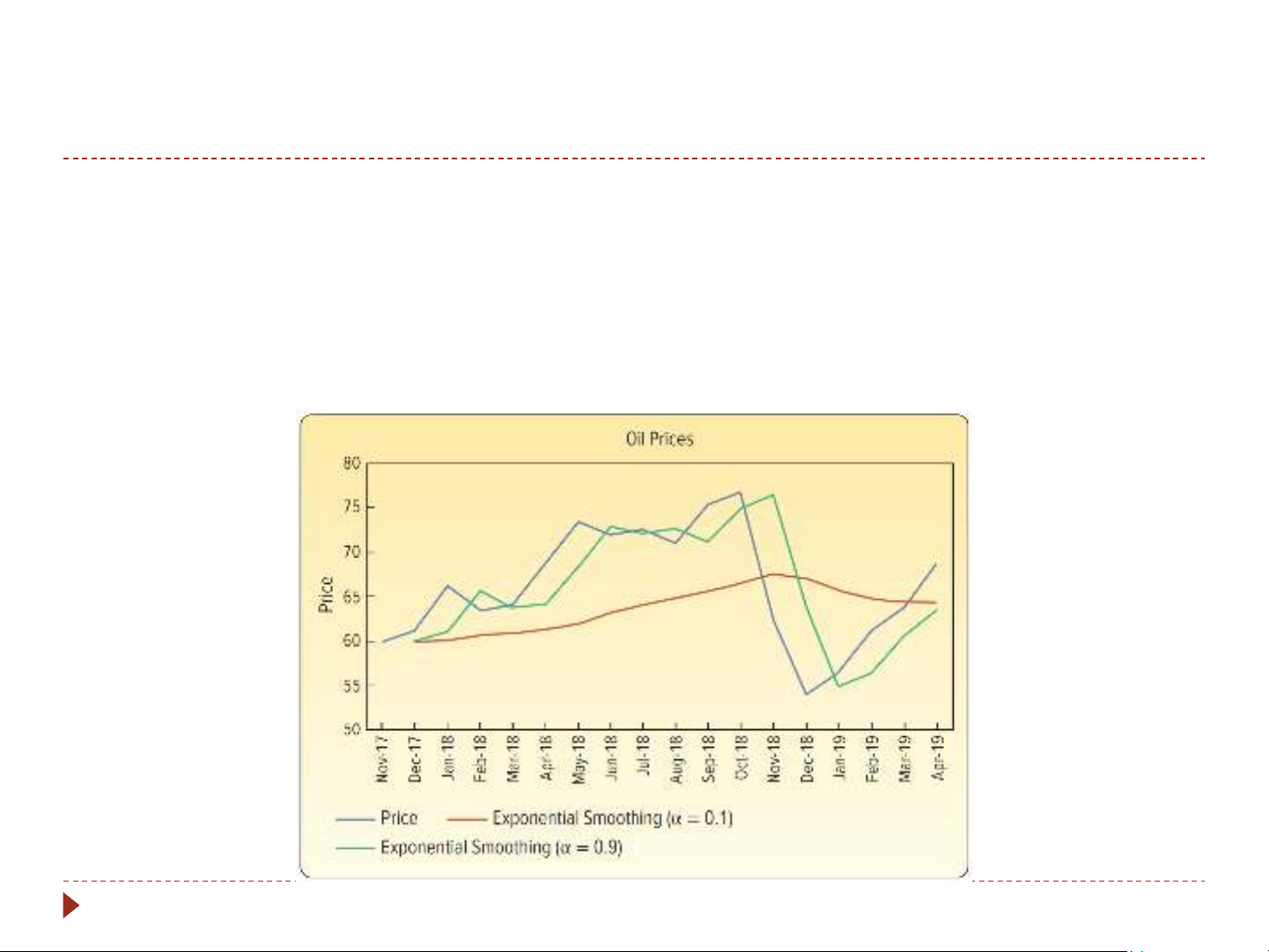

Simple Exponential Smoothing Example Concluded

The forecast with the high alpha value, the green line graph, is

very responsive to the most recent oil price.

The forecast with the low alpha value, the red line graph, is

much smoother and follows the average of oil prices over time. 5-18

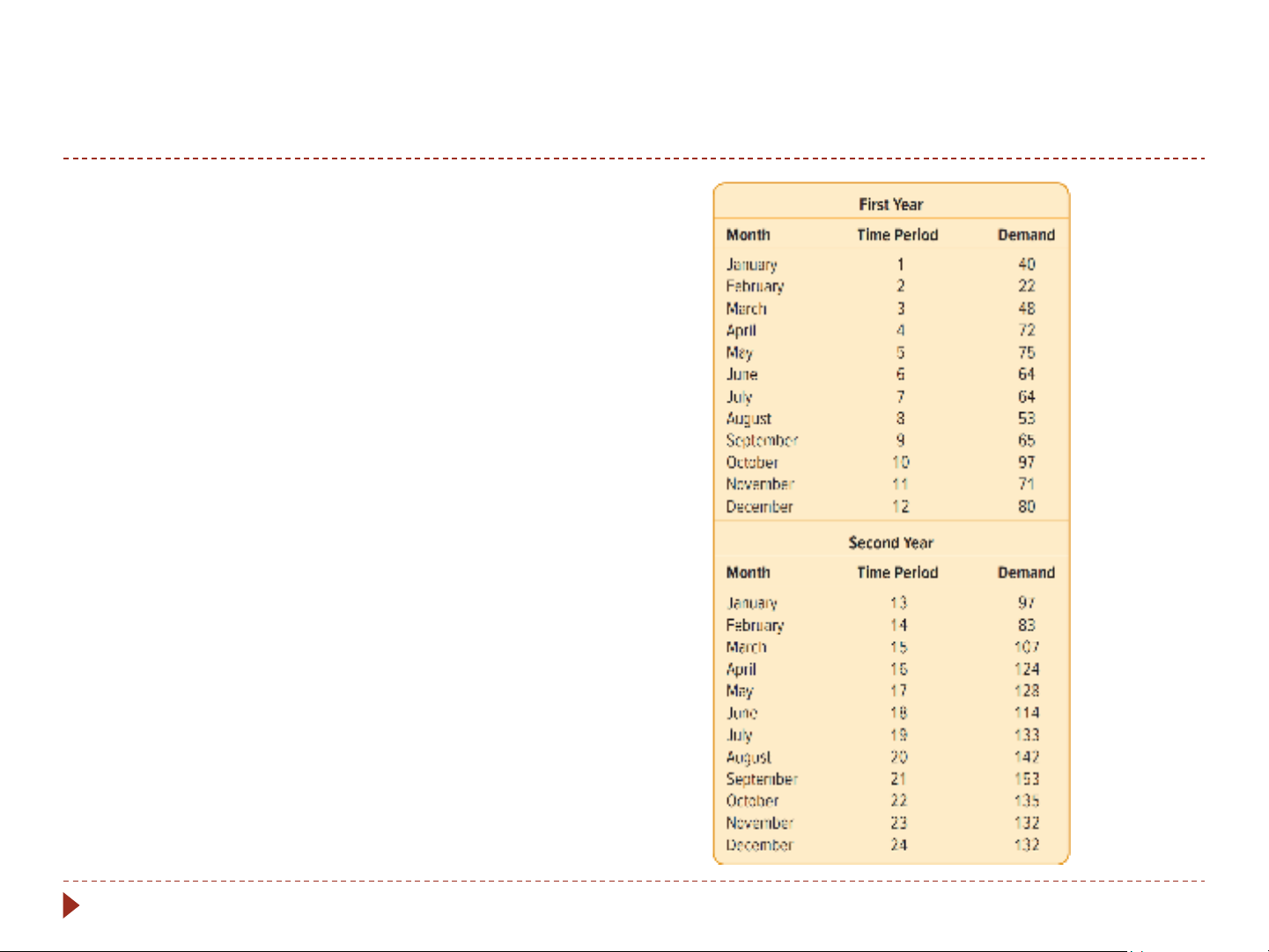

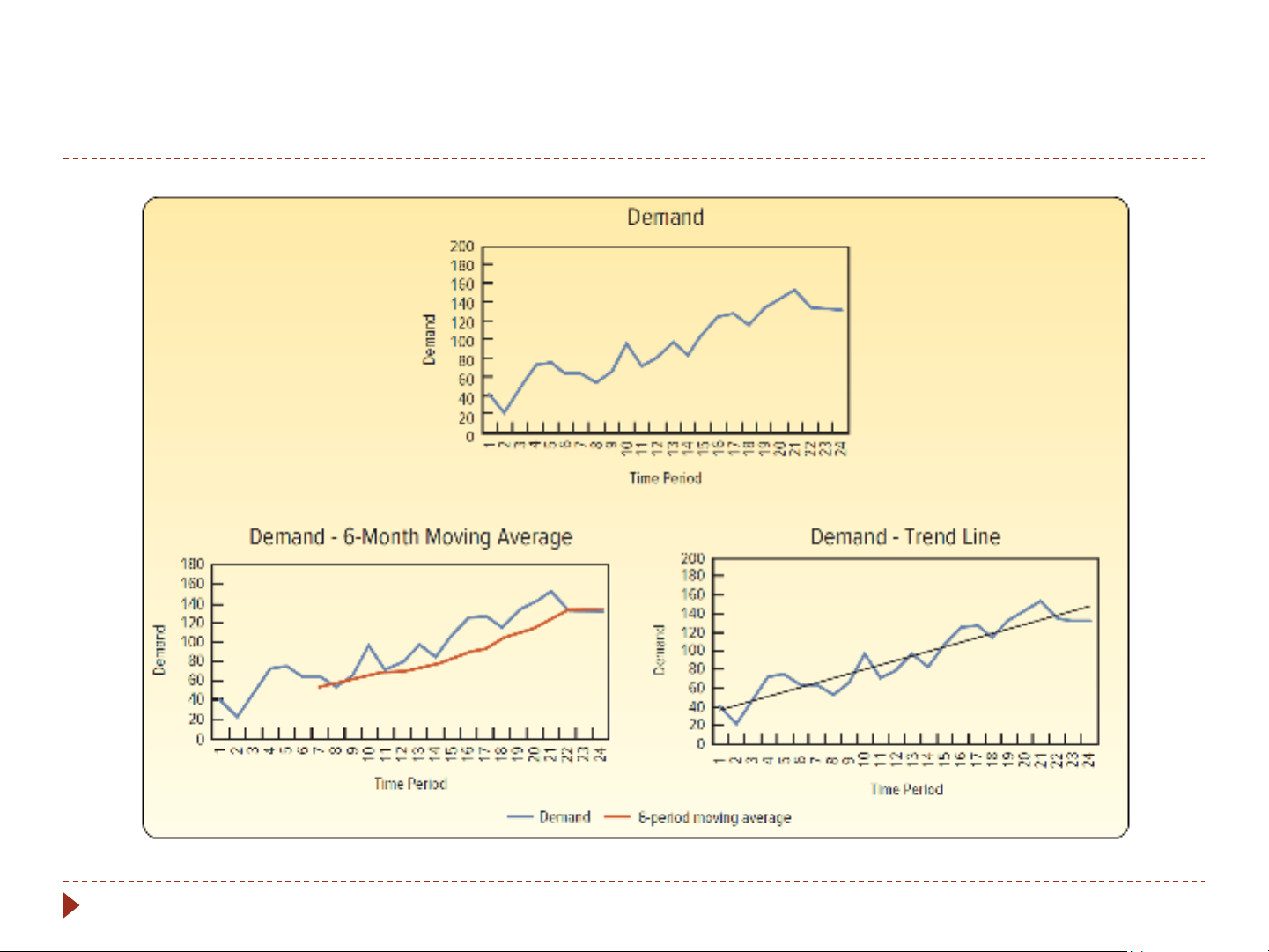

Time Series with a Trend: Regression Analysis If the trend is linear, regression analysis is used to fit a linear trend model to the time series. This time series is two years of monthly demand data. Each observation is labeled with the month. 5-19 Regression Analysis Example 5-20

Tài liệu liên quan:

-

Thống kê các ưng dụng của kinh tế

14 7 -

Vấn đề tôn giáo trong thời kì quá độ lên chủ nghĩa xã hội - Xác suất thống kê | Đại học Mở Thành phố Hồ Chí Minh

266 133 -

Đề cương Thống kê ứng dụng - Xác suất thống kê | Đại học Mở Thành phố Hồ Chí Minh

779 390 -

Phân tích Báo cáo tài chính - Xác suất thống kê | Đại học Mở Thành phố Hồ Chí Minh

418 209