Chapter 5 Lecture Notes: DCF Valuation Analysis | Môn Investment Banking - Trường Đại học Quốc tế, Đại học Quốc gia Thành phố Hồ Chí Minh

DCF analysis is a fundamental valuation methodology broadly used. It is premised on the principle that the value of a company, division, business, or collection of assets (“target”) can be derived from the present value of its projected free cash flow (FCF). Tài liệu được sưu tầm gồm 11 trang, giúp bạn ôn tập tốt hơn. Mời các bạn đón xem.

Môn: Investment Banking 7 tài liệu

Trường: Trường Đại học Quốc tế, Đại học Quốc gia Thành phố Hồ Chí Minh 2 K tài liệu

Tác giả:

Preview text:

lOMoAR cPSD| 58562220

Chapter 5: Valuation: Discounted Cash Flow (DCF) Analysis 1.Definition

• DCF analysis is a fundamental valuation methodology broadly used. It

is premised on the principle that the value of a company, division,

business, or collection of assets (“target”) can be derived from the

present value of its projected free cash flow (FCF).

• Intrinsic value can be derived from PV of projected free cash flow

• Important alternative to market-based valuation techniques

• Typically, FCF is projected for 5 years. Terminal value (“going

concern” value) captures remaining value beyond projection period

• WACC is the discount rate commensurate with business and financial risks

• Sensitivity analysis is used to test assumptions 2.

Steps Step 1: Study the target and determine key performance drivers Study the Target

• Study and learn as much as possible about the target and its sector. A

thorough understanding of the target’s business model, financial profile,

value proposition for customers, end markets, competitors, and key

risks is essential for developing a framework for valuation. Source of

info: SEC filings, earnings call transcripts, investor presentations,

MD&A section, equity research reports.

Determine key performance drivers (sales growth, profitability, FCF generation):

• Internal: new facilities/stores/products/customer contracts, improve

operational and working capital efficiency lOMoAR cPSD| 58562220

• External: acquisitions, end market trends, consumer buying patterns,

macroeconomic factors, legislative/regulatory changes.

Step 2: Project Free Cash Flow

Free Cash Flow: cash generated after paying all cash operating expenses and

taxes and after funding capex and working capital, but before paying interest expense.

FCF is independent of capital structure.

FCF = EBIT – Taxes + D&A – Capex – Increase (Decrease) in Net WC

= EBIT(1-Tc) + D&A – Capex – Increase (Decrease) in Net WC

Considerations for Projecting Free Cash Flow

• Historical performance: Historical performance provides valuable

insight for developing defensible assumptions to project. The DCF

customarily begins by laying out the target’s historical financial data for

the prior three-year period financial statements with adjustments for

non-recurring items and recent events

• Projection period length: 5 years, or when financial performance reaches steady stage

• Alternative cases: Management case, Base case, and upside and downside cases

Projection of Sales, EBITDA, and EBIT Sale Projection

• Using consensus estimates, equity research, industry reports, consulting

studies. Be aware of cyclical business

• Compare projections with target’s historical growth rates, peer

estimates, sector/market outlook

• Growth assumptions need to be justifiable

• Sales projections are consistent with other related assumptions (capex, working capital) lOMoAR cPSD| 58562220

COGS and SG&A Projections

• Historical gross profit margin and SG&A as a percentage of sales

• For private companies, examine research estimates for peer companies

EBITDA and EBIT Projection

• For future 2 or 3 years: use consensus estimates

• For outer years: hold margins constant at the last year level provided by

consensus estimates, consider profitability increasing or decreasing

• For private companies: use historical trends and consensus estimates for peer companies Tax Projection

• The first step in calculating FCF from EBIT is to subtract estimated

taxes. The result is tax-effected EBIT, also known as EBIAT or NOPAT.

This calculation involves multiplying EBIT by (1 – t), where “t” is the target’s marginal tax rate.

• A marginal tax rate of 35% to 40% is generally assumed for modeling purposes.

• The company’s actual tax rate (effective tax rate) in previous years can

also serve as a reference point D&A Projections

• Depreciation: projected as percentage of sales or capex based on

historical levels. Or build a detailed PP&E schedule. Ensure

depreciation and capex are in line by the final year of projection period

• Amortization: projected as percentage of sale, or build detailed

schedule based on existing intangible assets

• For some companies, D&A is a separate line item on income statement.

But more commonly included in COGS or SG&A. lOMoAR cPSD| 58562220

• D&A as one line-item: projected using 2 methods for depreciation

above, or D&A = EBITDA - EBIT

• D&A is non-cash expense. It is added back to EBIAT in the calculation

of FCF. Hence, while D&A decreases a company’s reported earnings, it does not decrease its FCF.

Capital expenditure Projection

• Historical capex is a reliable proxy

• Consider company’s strategy, sector, or phase of operations

• Future planned capex can be found in MD&A section, research reports

• Generally driven as percentage of sales in line with historical levels

Change in net working capital Projections

• An increase in NWC is a use of cash. A decrease in NWC is a source of cash

• NWC is projected as percentage of sales

• Recommended approach is to project each component of current assets

and current liabilities which is projected based on historical ratios from

prior year level or 3-year average

Change in NWC = NWC in year n – NWC in year (n-1)

NWC = Non-cash current assets – Non-interest-bearing current liabilities

= (A/R + Inventory + Prepaid expenses and Other current assets) – (A/P

+ Accrued liabilities + Other current liabilities)

• Accounts receivable: use DSO

• Inventory: use DIH or Inventory turns

• Prepaid expenses and Other current assets: projected as percentage of

sales in line with historical levels lOMoAR cPSD| 58562220 • Accounts payable: use DPO

• Accrued liabilities and Other current liabilities: projected as percentage

of sales in line with historical levels

DSO (Day sale outstanding) = (A/R / Sales)*365

DIH (Days inventory held) = (Inventory/COGS)*365 Inventory Turns =

COGS/Inventory DPO = (A/P / COGS) * 365 Step 3: Calculate

Weighted Average Cost of Capital

WACC is also called opportunity cost of capital Steps for calculating WACC:

• Determine target capital structure

• Estimate cost of debt (rd)

• Estimate cost of equity (re)

Calculate WACC : rWACC = rd* (1-T) * D/(D+E) + re * E/(E+D)

Often use WACC range by sensitizing its key inputs

Target capital structure: is consistent with long-term strategy. Use company’s

current and historical debt-to-total capitalization ratios, or mean and median

of its peers. Target capital structure is held constant throughout projection period.

Cost of debt (rd): if company is currently at its target capital structure, , cost

of debt is derived from blended yield on outstanding debt instruments

(public and private debt). Otherwise, cost of debt is derived from peer companies

• Publicly traded bonds: current yield on all outstanding issues

• Private debt (revolving credit facilities and term loans): consults with

debt capital markets specialist for current yield lOMoAR cPSD| 58562220

• If no current market data, use at-issuance coupons of current debt

maturities, or estimate company’s credit rating at target capital structure

and use cost of debt for comparable credits

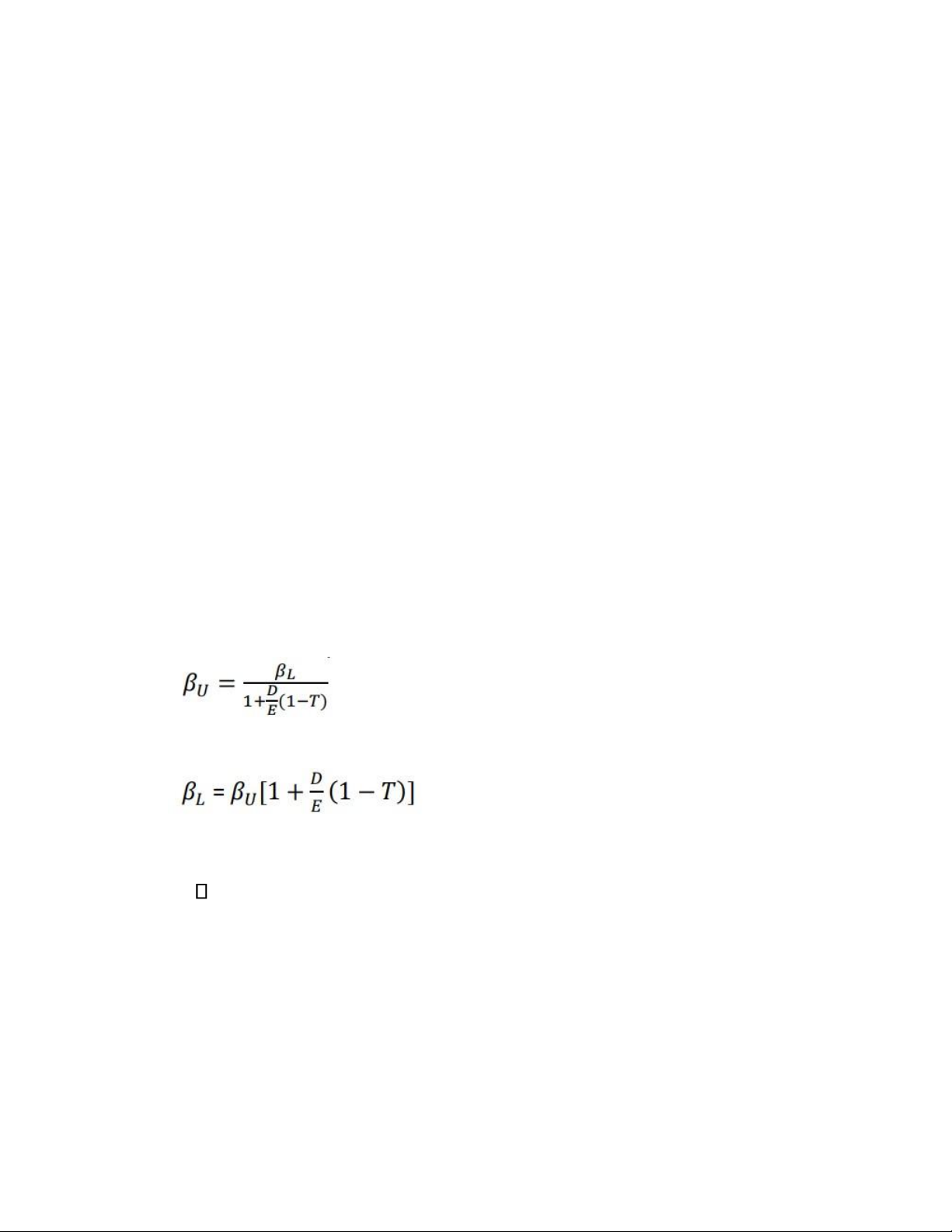

Cost of equity (re): use CAPM

• Cost of equity = Risk-free rate + Levered beta x Market risk premium

• Beta for public company: use historical beta

• Beta for private company: is derived from a group of publicly traded

peer companies, but need to neutralize the effects of different capital structures:

✓ Calculate unlevered beta (asset beta) of each peer, then take the average

✓ Calculate relevered beta using company’s target capital structure and marginal tax rate

How to calculate levered beta for private company:

Unlevered beta (asset beta) of each peer:

Relevered beta of the target company:

Note: Use avarege 𝛽𝑈 to calculate

Size premium (SP): added to cost of equity of CAPM

re = rf + 𝛽L * (rm –rf) + SP lOMoAR cPSD| 58562220

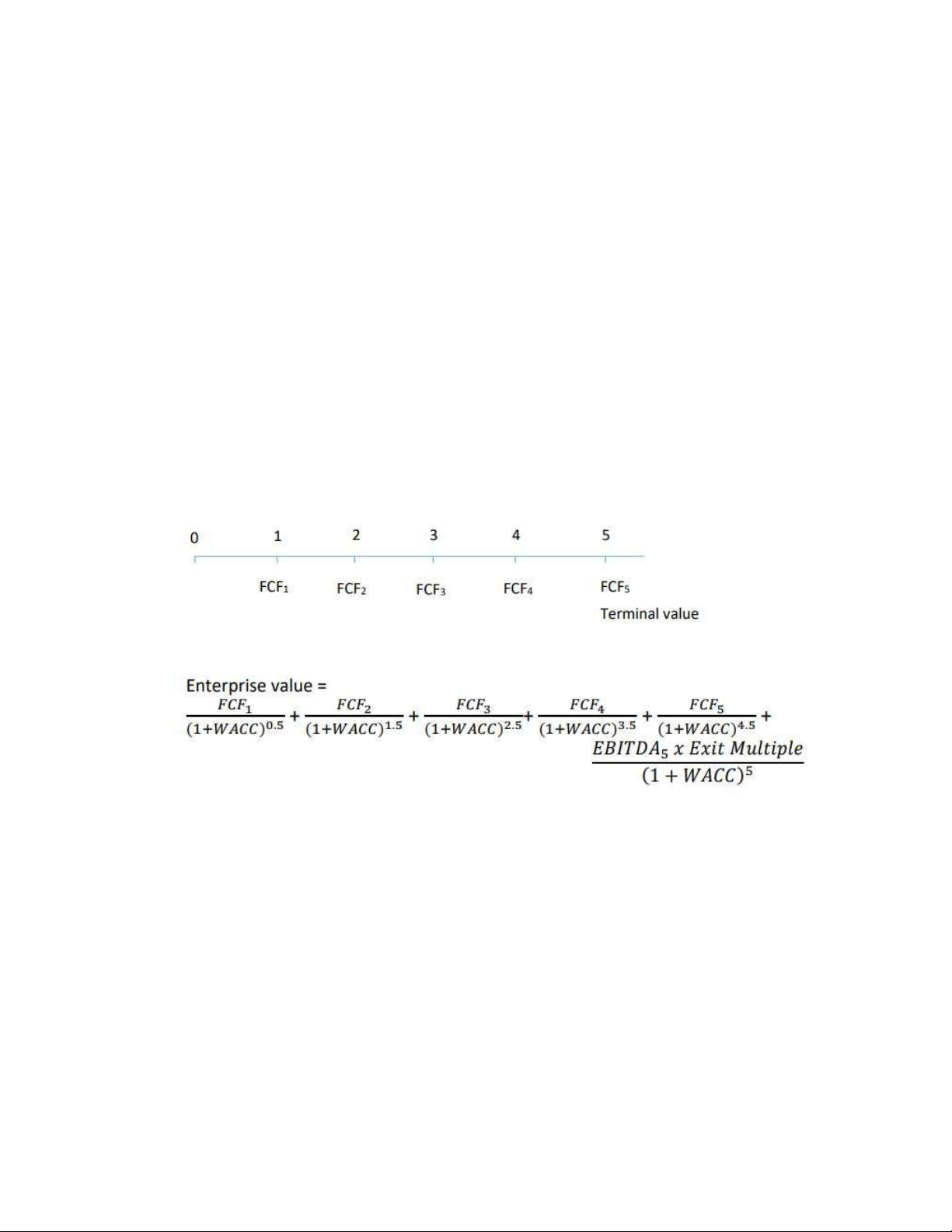

Step 4: Determine Terminal Value

Terminal value is typically calculated on the basis of the company’s FCF (or

a proxy such as EBITDA) in the final year of the projection period.

Exit multiple method (EMM):

Terminal value = EBITDAn x Exit Multiple

n: terminal year of projection period. Multiple is the current LTM trading

multiples for comparable companies

Use normalized trading multiple, normalized EBITDA

Sensitivity analysis: range of exit multiple Perpetuity growth method (PGM):

Terminal value = [FCFn x (1+g)] / (r-g)

FCF: unlevered free cash flow n: terminal

year of projection period FCF: unlevered free

cash flow g: perpetuity growth rate (2% to 4%) r: WACC

Perpetuity growth rate:

• Based on company’s expected long-term industry growth rate (2%-4%)

• Is sensitized to produce valuation range

The followings are calculated to check between EMM and PGM: lOMoAR cPSD| 58562220

Implied perpetuity growth rate (end-of-year discounting and mid-year

discounting) Implied exit multiple (end-of-year discounting and mid-

year discounting) Step 5: Calculate Present Value and Determine Valuation

Discount factor: year-end and mid-year convention

• Year end: Discount factor = 1/(1+WACC)n

• Mid year: Discount factor = 1/(1+WACC)n-0.5

Terminal value considerations: if using mid-year convention for FCF of

projection period, use mid-year discounting for terminal value under PGM,

but use year-end discounting under EMM Enterprise value

Using mid-year discounting with EMM method:

Implied equity value = Enterprise Value + Prefrerred Stock + Noncontrolling Interest

Implied share price = Implied equity value/Fully Diluted Shares Outstanding

• Sensitivity analysis: The exercise of deriving a valuation range by

varying key inputs is called sensitivity analysis. Key valuation drivers

such as WACC, exit multiple, and perpetuity growth rate are the most

commonly sensitized inputs in a DCF lOMoAR cPSD| 58562220 Key Pros

• Cash flow-based: reflects value of projected FCF, a more fundamental approach to valuation

• Market independent: more insulated from market bubbles and distressed periods

• Self-sufficient: DCF is important when there are limited or no “pure play” public comparables

• Flexibility: can run multiple financial performance scenarios (growth

rates, margins, capex requirements, working capital efficiency) Key cons

• Dependence on financial projections: accurate forecasting of financial

performance is challenging, especially as projection period lengthens

• Sensitivity to assumptions: small changes in key assumptions (growth

rates, margins, WACC, exit multiple) can produce different valuation ranges

• Terminal value: accounts for three-quarters or more of DCF valuation

=> decrease the relevance of FCF of projection period

• Assumes constant capital structure: no flexibility to change capital

structure over projection period

1.Calculate FCF using the information below Assumptions EBIT $300 D&A 50 Capex 25

Inc/(Dec) in Net Working Capital 10 Tax Rate 38% lOMoAR cPSD| 58562220

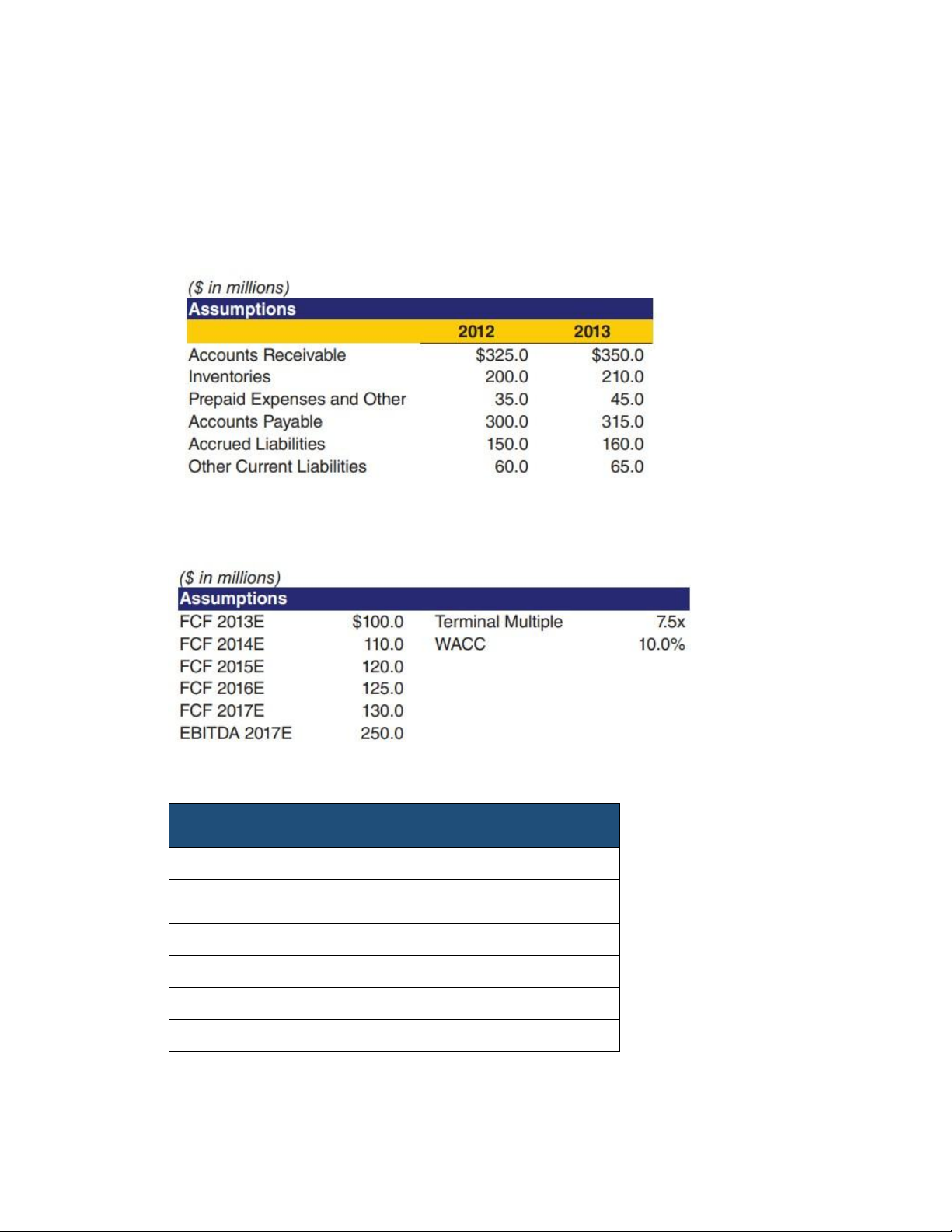

2. Calculate the (increase) / decrease in net working capital from 2012 to 2013

based on the following assumptions

3. Using a mid-year convention and the assumptions below,calculate enterprise value

4. Using the information below to answer question Enterprise Value Cumulative PV of FCF $1,600 Terminal Value Terminal year EBITDA $929.2 Exit Multiple 7.5x Terminal Value Discount Factor 0.62 lOMoAR cPSD| 58562220 PV of Terminal Value % of Enterprise Value Enterprise Value a) Calculate Terminal Value b) Calculate Enterprise Value

c) Calculate the percentage of enterprise value represented by the terminal value

Tài liệu liên quan:

-

Discussion Questions Lecture 3 | Môn Investment Banking - Trường Đại học Quốc tế, Đại học Quốc gia Thành phố Hồ Chí Minh

95 48 -

Focus Notes: Key Concepts & Analysis Techniques | Môn Investment Banking - Trường Đại học Quốc tế, Đại học Quốc gia Thành phố Hồ Chí Minh

93 47 -

Law on Credit instituion | Môn Investment Banking - Trường Đại học Quốc tế, Đại học Quốc gia Thành phố Hồ Chí Minh

80 40 -

Cost of Equity Calculation | Môn Investment Banking - Trường Đại học Quốc tế, Đại học Quốc gia Thành phố Hồ Chí Minh

83 42 -

Portfolio Risk and Return Part II - Exam Questions and Answers | Môn Investment Banking - Trường Đại học Quốc tế, Đại học Quốc gia Thành phố Hồ Chí Minh

87 44