Đề ôn tập cuối kỳ Chuẩn mực báo cáo tài chính quốc tế | Trường Đại học Công nghiệp TP.HCM

Đề ôn tập cuối kỳ Chuẩn mực báo cáo tài chính quốc tế môn Chuẩn mực báo cáo tài chính quốc tế của Trường Đại học Công nghiệp Thành phố Hồ Chí Minh. Hi vọng tài liệu này sẽ giúp các bạn học tốt, ôn tập hiệu quả, đạt kết quả cao trong các bài thi, bài kiểm tra sắp tới. Mời các bạn cùng tham khảo chi tiết bài viết dưới đây nhé.

Môn: Chuẩn mực báo cáo tài chính quốc tế (CMBC) 10 tài liệu

Trường: Trường Đại học Công nghiệp Thành phố Hồ Chí Minh 791 tài liệu

Tác giả:

Preview text:

ĐỀ ÔN TẬP CUỐI KỲ

CHƯƠNG 6:

BÀI 1:

Bài giải:

a,

- 1 January 2020:

Dr Invesment in Associate and Joint Venture: $80,000

Cr Machine: $25,000

Cr Cash: $55,000

- 31 Dec 2020:

Dr Share of profit or loss of associate and joint venture: $60,000 x 30% = $18,000 Cr Invesment in associate and joint venture : $18,000

- Asset revaluation surplus:

Dr Invesment in associate and joint venture: $50,000 x 30% = $15,000

Cr Share of OCI of associate and joint venture: $15,000

Dr Share of OCI of associate and joint venture: $15,000 Cr Asset revaluation surplus: $15,000

- 31 Dec 2021:

Dr Invesment in associate and joint venture: ($80,000 - $80,000 x 20%)x30% = $19,200

Cr Share of profit or loss of associate and joint venture: $19,200

- Dividend:

Dr Cash: $20,000 x 30% x 50% = $3,000

Dr Dividends receivable: $3,000

Cr Invesment in associate and joint venture: $20,000 x 30% = $6,000

- Asset revaluation surplus:

Dr Share of OCI of associate and joint venture: $20,000 x 30% = $6,000

Cr Invesment in associate and joint venture: $6,000

Dr Asset revaluation surplus: $6,000

Cr Share of OCI of associate and joint venture: $6,000

B, At 31 Dec 2021 the Invesment in associate and joint venture measures is $84,200

(= $80,000 - $18,000 + $15,000 + $19,200 - $6,000 - $6,000)

C,

Share capitial $100,000

Asset revaluation $ 30,000

General reserve $ 6,000

Retained earning $ 98,000 ( = $120,000 – 60,000 + (80,000 – 80,000 x 20%) – 20,000 –

6,000) Bài 2:

Bài giải:

a,

- 1 January 2020:

Dr Invesment in Associate and Joint Venture: $80,000

Cr Equipment: $22,000

Cr Cash: $58,000

- 31 Dec 2020:

Dr Share of profit or loss of associate and joint venture: $50,000 x 30% = $15,000 Cr Invesment in associate and joint venture : $18,000

- Asset revaluation surplus:

Dr Invesment in associate and joint venture: $40,000 x 30% = $12,000

Cr Share of OCI of associate and joint venture: $12,000

Dr Share of OCI of associate and joint venture: $12,000 Cr Asset revaluation surplus: $12,000

- 31 Dec 2021:

Dr Invesment in associate and joint venture: ($60,000 - $60,000 x 20%)x30% = $14,400 Cr Share of profit or loss of associate and joint venture: $14,400

- Dividend:

Dr Cash: $12,000 x 30% x 50% = $1,800

Dr Dividends receivable: $1,800

Cr Invesment in associate and joint venture: $12,000 x 30% = $3,600

B, At 31 Dec 2021 the Invesment in associate and joint venture measures is $87,800

(= $80,000 - $18,000 + $12,000 + $14,400 - $3,600 )

C,

Share capitial $100,000

Asset revaluation $ 60,000

General reserve $ 6,000

Retained earning $ 80,000 ( = $100,000 – 50,000 + (60,000 – 60,000 x 20%) – 12,000 –

6,000)

Bài 3:

Bài giải:

a,

- 1 January 2015:

Dr Invesment in Associate and Joint Venture: $66,000 Cr Cash: $66,000

- 31 Dec 2015:

Dr Invesment in associate and joint venture: ($60,000 - $60,000 x 20%) x 30% = $14,400 Cr Share of profit or loss of associate and joint venture: $14,400

- Dividend:

Dr Cash: $20,000 x 30% = $6,000

Cr Invesment in associate and joint venture: $6,000

- Asset revaluation surplus:

Dr Invesment in associate and joint venture: $30,000 x 30% = $9,000

Cr Share of OCI of associate and joint venture: $9,000

Dr Share of OCI of associate and joint venture: $9,000 Cr Asset revaluation surplus: $9,000

- 31 Dec 2016:

Dr Share of profit or loss of associate and joint venture: $50,000 x 30% = $15,000 Cr Invesment in associate and joint venture: $15,000 - Asset revaluation surplus:

Dr Share of OCI of associate and joint venture: $20,000 x 30% = $6,000

Cr Invesment in associate and joint venture: $30,000 x 30% = $6,000

Dr Asset revaluation surplus: $6,000

Cr Share of OCI of associate and joint venture:$6,000

B, At 31 Dec 2021 the Invesment in associate and joint venture measures is $62,400

(= $66,000 - $6,000 + $14,400 + $9,000 - $15,000 - $6,000)

C,

Share capitial $100,000

Asset revaluation $ 10,000

General reserve $ 3,000

Retained earning $ 95,000 ( = $120,000 - 50,000+ (60,000 – 60,000 x 20%) – 20,000 – 3,000)

CHƯƠNG 5:

Bài 1:

1,

Building $20,000

Depreciation year 2010 (($20,000 - $2,000)/ 10)/2 = $900

Depreciation year 2011 ($20,000 - $2,000)/ 10 = $1,800

Depreciation year 2012 ($20,000 - $2,000)/ 10 = $1,800

Depreciation year 2013 ($20,000 - $2,000)/ 10 = $1,800

Carrying amount $20,000 – $1,800 x 3 - $900 = $13,700

The manager reconsiders the residual value and changes it to $3,000

After reconsidering

Depreciation for the year ($13,700 - $3,000)/6.5 = $1,646

Dr Depreciation expense $1,646

Cr Accumulated Depreciation $1,646

2,

Building $300,000

Depreciation year 2020 ($300,000 - $2,000)/ 10 = $29,800

Depreciation year 2021 ($300,000 - $2,000)/ 10 = $29,800

Depreciation year 2022 ($300,000 - $2,000)/ 10 = $29,800

Depreciation year 2023 (($300,000 - $2,000)/ 10)/2 = $14,900

Carrying amount $300,000 – S29,800 x 3 - $14,900 = $195,700

The depreciation rates for similar buildings used in its industry and decided that the building should be depreciated 10 years

After reconsidering

Depreciation for the year ($195,700 - $2,000)/16.5 = $11,739

Dr Depreciation expense $11,739 Cr Accumulated Depreciation $11,739

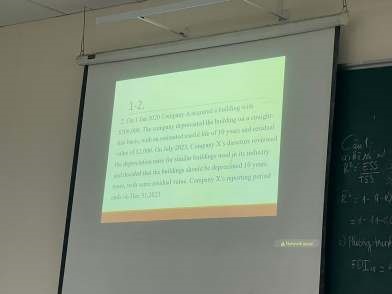

Bài 2:

Bài giải:

Cost 100,000

Depreciation year 1 ( 100,000 – 0)/ 10 = 10,000

Depreciation year 2 10,000

Carrying amount 100,000 – 10,000 x 2 = 80,000

The management revises its estimate of useful life to a total of 6 years

After revising

Depreciation for the year (80,000 – 0)/ 4 = 20,000

Dr Depreciation expense 20,000 Cr Accumulated Depreciation 20,000 Bài 3:

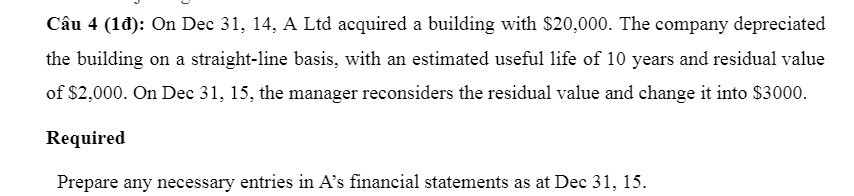

Bài giải:

Building $20,000

Depreciation year 14 ($20,000 - $2,000)/ 10 = $1,800

Carrying amount $20,000 - $1,800 = $19,200

The managar reconsiders the residual value and change it into $3000

After Reconsidering

Depreciation for the year ($19,200 - $3,000)/ 9 = $1,800

Dr Depreciation expense $1,800 Cr Accumulated Depreciation $1,800

Bài 4:

Bài giải:

Cost 3,600,000

Depreciation year 2009 (3,600,000 – 0)/ 10 = 360,000

Depreciation year 2010 (3,600,000 – 0)/ 10 = 360,000

Depreciation year 2011 (3,600,000 – 0)/ 10 = 360,000

Carrying amount 3,600,000 – 360,000 x 3 = 2,520,000

The directors deceided the the remaining useful life of the machine at 1 January 2012 was three years

After revising

Depreciation for the year (2,520,000 – 0)/ 3 = 840,000

Dr Depreciation expense 840,000 Cr Accumulated Depreciation 840,000

Bài 5:

Bài giải:

Building $30,000

Depreciation year 10 ($30,000 - $3,000)/5 = $5,400

Depreciation year 11 $5,400

Depreciation year 12 $5,400

Carrying amount $30,000 - $5,400 x 3 = $13,800

The manager reconsider the residual value and change it into $5,000

After reconsidering

Depreciation for the year ( 13,800 – 5,000)/ 2 = 4,400

CHƯƠNG 4

- Có bankruptcy, lower, sale of inventory, discovery, disposal, settlement -> Adjusting events -> This event provides evidence of conditions that existed at the reporting date.

- Còn lại là -> non – adjusting -> This event provides evidence of conditions that existed after the reporting date.

CHƯƠNG 3:

Tài liệu liên quan:

-

Tài liệu Chuẩn mực báo cáo tài chính quốc tế | Trường Đại học Công nghiệp TP.HCM

251 126 -

Đề ôn giữa kỳ Chuẩn mực báo cáo tài chính quốc tế | Trường Đại học Công nghiệp TP.HCM

472 236 -

Bài tập ôn tập chương 6 | Chuẩn mực báo cáo tài chính quốc tế | Trường Đại học Công nghiệp TP.HCM

285 143 -

Ôn thi giữa kỳ Chuẩn mực báo cáo tài chính quốc tế | Trường Đại học Công nghiệp TP.HCM

406 203