Final Exam Notes on Capital Budgeting & Investment Analysis | Môn Fundamentals of Financial Management - Trường Đại học Quốc tế, Đại học Quốc gia Thành phố Hồ Chí Minh

The process of identifying, analyzing, and selecting investment projects whose returns (cash flows) are expected to extend beyond one year. Tài liệu được sưu tầm gồm 23 trang, giúp bạn ôn tập tốt hơn. Mời các bạn đón xem.

Môn: Fundamentals of Financial Management 10 tài liệu

Trường: Trường Đại học Quốc tế, Đại học Quốc gia Thành phố Hồ Chí Minh 1.9 K tài liệu

Tác giả:

Preview text:

lOMoAR cPSD| 58562220

Capital Budgeting & Investment Criteria

I. What is capital budgeting decision? (Quyết định liên quan đến phân bố nguồn vốn doanh nghiệp)

- The process of identifying, analyzing, and selecting investment projects whose returns (cash

flows) are expected to extend beyond one year

+ Identify: Coi doanh nghiệp đang muốn đầu tư vào cái gì ( Chọn dự án liên quan đến mảng muốn làm)

+ Analyze: Profit, cash flow, pay back period (thời gian hoàn vốn, gian bắt đầu có profit) +

Selecting: Vì mỗi công ty có limit capital → Chọn dự án tốt nhất cho doanh nghiệp (choose

the most suitable, not the most profitable)

=> Capital budgeting/investment decision is the central to the success of any firm

→ 1 doanh nghiệp muốn thành công phải làm bước này tốt (chọn dự án phù hợp với khả năng

vốn để tạo ra lợi nhuận)

- Sau khi analyzing (Chọn ra project để đầu tư):

+ Mutually exclusive projects: Only one of several potential projects can be chosen

Ex: Acquiring an accounting system

=> Rank all alternatives & select the best one

→ Chọn 1 project tốt nhất trong những project

Ex: Trong 10 projects, chọn 2-3 projects tốt nhất do không đủ vốn

+ Independent projects: More than 1 promisi

ng projects can be chosen: Accepting/rejecting 1 project does not affect the

decision of the other projects → Chọn nhiều hơn 1 trong

số những projects đã lựa chọn

=> Rank all & choose good ones

Ex: Trong 10 projects, chọn 2-3 projects tốt nhất do không đủ vốn

- Net present value (NPV): Present value of all future cash flows & initial investments

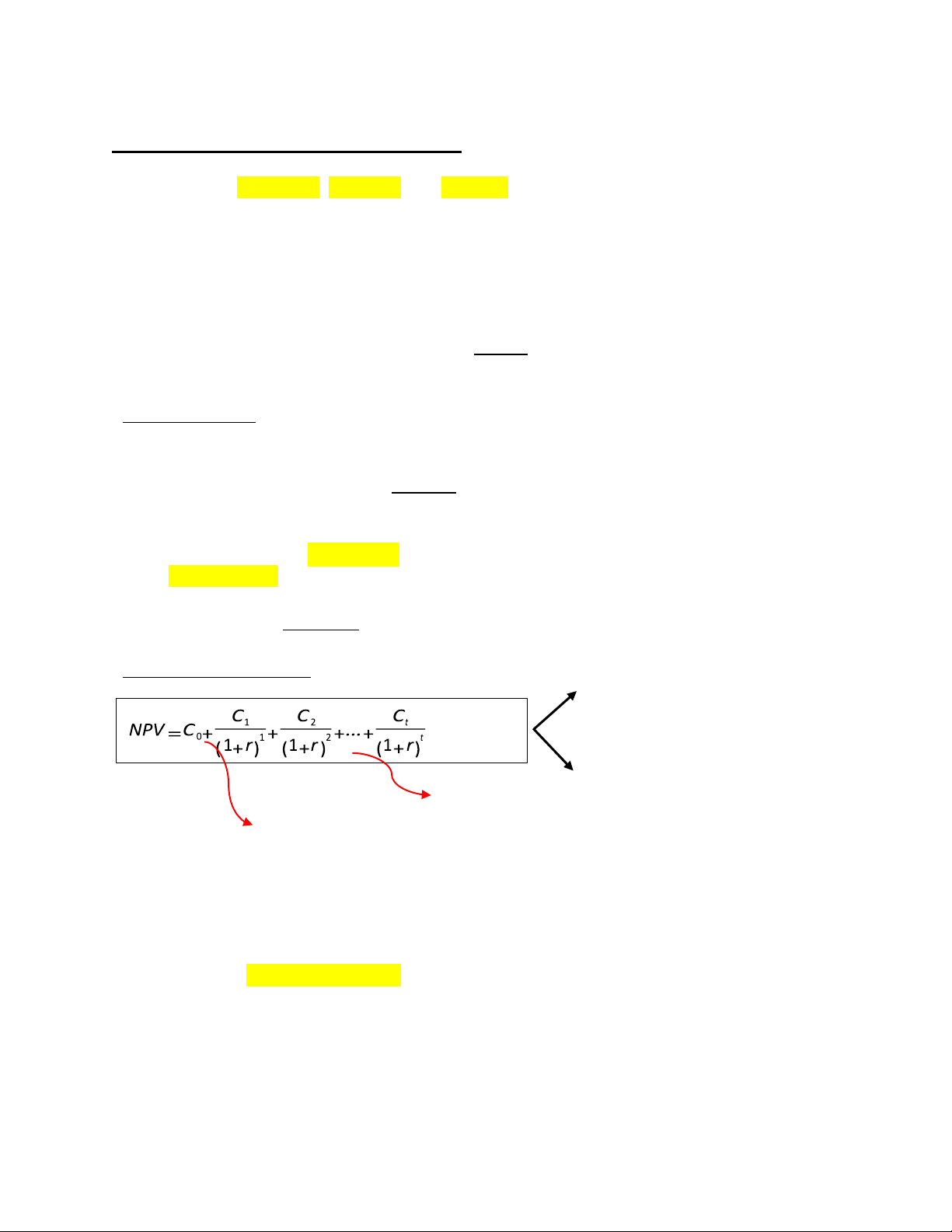

NPV > 0: Nên đầu tư

NPV > 0: Không nên đầu tư

Discount tất cả cash flows về present value

Initial investment: Số tiền đầu tư mình phải bỏ ra, thường mang dấu (- )

+ Cash outflow: Phải trả cho người ta: Pay → (-)

+ Cash inflow: Người ta trả cho mình: Recieve → (+)

Ex: Năm 0, công ty phải bỏ ra $200,000 để mua equipment, 3 năm đầu, mỗi năm mang lại lợi

nhuận $10,000 nhưng từ năm 4-10 lại mang lại lost $50,000 + C0: $200,000 + C1 = C2 = C3: $10,000

+ C4 = C5 = C6 = … = C10: - $50,000

Note: r thường là multiple interest rate

Ex: You have the opportunity to purchase an office building. You have a tenant lined up that will

generate $16,000 per year in cash flows for 3 years. At the end of 3 years you anticipate selling

the building for $450,000. Assume opportunity cost is 7%. How much would you be willing to pay for the building? lOMoAR cPSD| 58562220

If the building is being offered for sale at a price of $350,000, would you buy the building

and what is the added value generated by your purchase and management of the building?

+ -350,000: Initial investment = Market price

+ NPV = -350,000 + 409,323 = 59,323 > 0 => Buy house

Note: - PV > Market price: Decide to buy

- PV < Market price: Refuse to buy

Note: Luôn phải có conclusion (nên đầu tư hay không) sau khi tính ra NPV -

Accept if NPV≥0

- Ranking criteria: From the highest NPV Ex: Chọn 1 dự án Có NIV

cao nhất trong 10 dự án - Disadvantages: + Face capital rationing

→ Phân bổ nguồn vốn thế nào cho hợp lí

+ Choose mutually exclusive projects have different time life

→ Các projects so sánh thực hiện ở các năm khác nhau nhưng tính ra NPV = nhau thì không thể

lựa được - Advantages:

+ Uses all cash flows of the projects

→ Có thể sử dụng tất cả cash flows được đưa ra ở trong projects để tính NPV (Giá trị thực tế có

thể mang lại cho công ty)

+ Discounts all cash flows properly

+ Can apply for unconventional cash flows

→ Dòng tiền Không ổn định: Cash flows không bằng nhau

II. Internal rate of return (IRR)

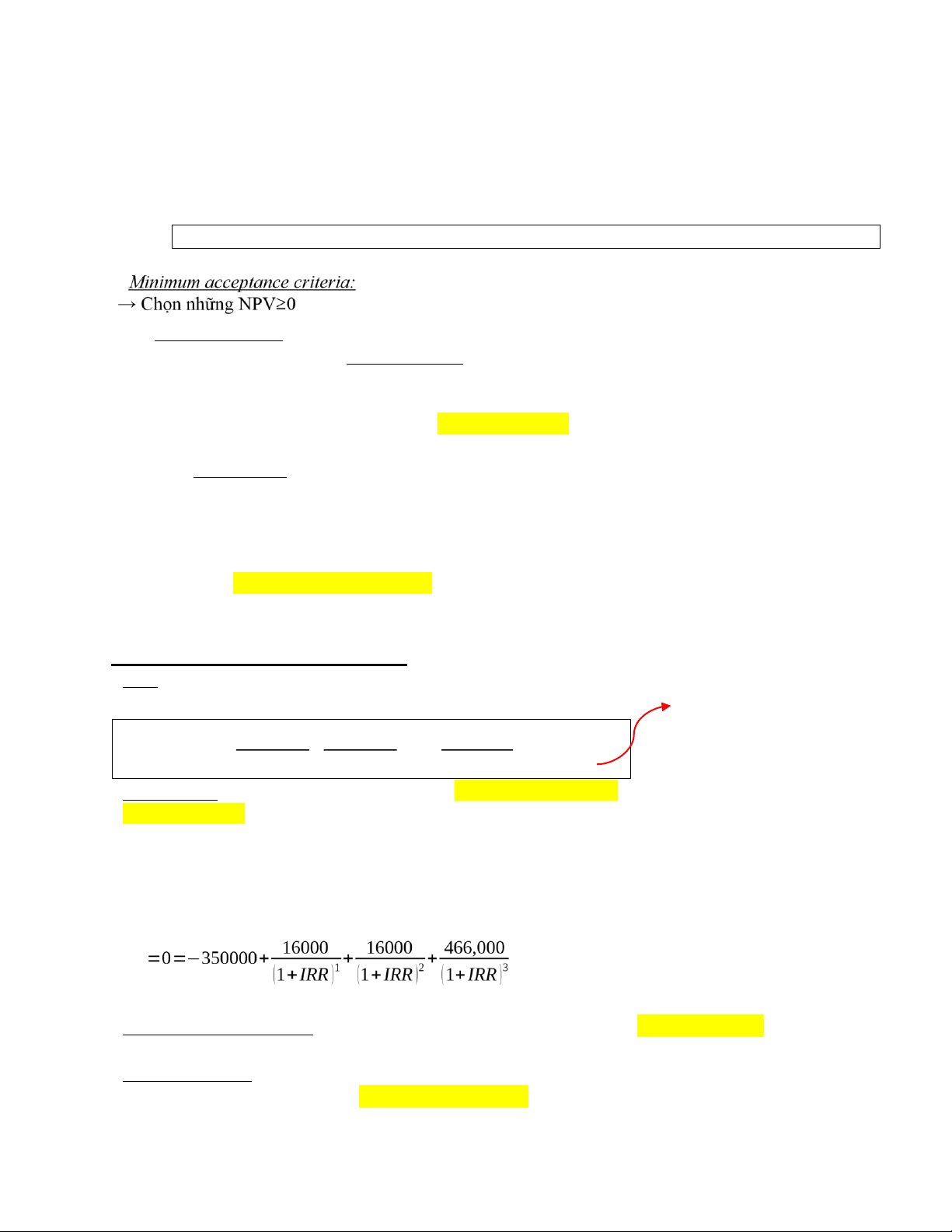

- IRR: Discount rate at which NPV = 0 (Huề vốn) Phải tính ra C1 C2 Ct NPV =0=C0+ 1+ 2+…+ t (1+IRR) (1+IRR) (1+IRR)

- IRR method: Select all projects that have an internal rate of return equal or greater than opportunity cost of capital

Ex: Opportunity cost: Có nhiều cash flows để finance 1 project: Internal cash flows, retained

earnings (Dòng tiền sẵn có: Đáp ứng required of return (ROR) của những cổ đông) thì ROR

được coi là opportunity cost

Ex: CF1= CF2 = 16,000; CF3 = 466,000; Opportunity cost = 7%. C0 (initial investment) = 350000. IRR=? NPV

=> IRR = 12.96% > Opportunity cost = 7% → Accept project

- Min acceptance criteria: Accept if IRR ≥ Required rate of return (Opportunity cost)

→ IRR > Cost of capital

- Ranking criteria: Choose the highest IRR

Note: NPV & IRR will generally give the same decision (Cho ra quyết định giống nhau), exceptions: lOMoAR cPSD| 58562220

+ Non-conventional cash flows: Cash flow signs change more than once

→ Nó là unconventional cash flows: NPV apply được còn IRR thì không

=> 2 phương pháp có thể đưa ra decision khác nhau +

Mutually exclusive projects:

_ Initial investments are substantially different

_ Timing of cash flows is substantially different

→ NPV apply được timing of cash flows (Thời điểm của dòng tiền) - Problems with IRR:

+ Multiple IRRs: Giải ra nhiều ẩn nằm trong mũ chẵn (Các IRR có mốc thời gian chẵn)

→ Gây khó khăn trong việc chọn projects

_ Conventional cash flow: Cash flow signs change only once

→ Chiều dòng tiền thay đổi 1 lần duy nhất

Ex: C0 = -2000; C1 = 500; C2 = 1800; C3 = 0 => Only 1 IRR

_ Unconventional cash flow: Cash flow signs change more than once

→ Dòng tiền có cả (-) & (+), chiều dòng tiền thay đổi hơn 1 lần Ex:

C0 = -60; C1 = 12;...; C9 = 12; C10 = -15

→ Đổi chiều 2 lần: Từ (-) sang (+) & từ (+) sang (-)

=> Multiple rate of return

→ IRR apply không hiệu quả

+ Not distinguish between Borrowing & Lending: Nên mượn hay nên cho vay

+ Borrowing from bank: Lãi suất ngân hàng thay đổi nên khó so sánh với opportunity cost

+ Lending: From internal cash flows 3) + The scale problem + The timing problem - Advantages:

+ Easy to understand & communicate

→ Dễ tính toán, understand & communicate

+ Information of safe margin

-> Khoảng an toàn = IRR - Opportunity cost

III. Payback period (PP)

- How long does it take the project to “pay back” its initial investment?

→ Khi nào tôi được hoàn trả số tiền ban đầu

Ex: Bỏ ra $500,000 cho dự án 5 năm, biết rằng mỗi năm hoàn $100,000 → Payback period = 5years

- Payback period = Number of years to recover initial costs: Thời gian hoàn vốn → Dựa trên cash flows

- Only accept projects that “payback” in the desired time frame (Cutoff period)

→ Chọn dự án có payback period ngắn nhất (In lowest year)

Note: Select a project with quickest payback when choosing among mutually exclusive projects

Ex: Examine the 3 projects & note the mistake we would make if we instead on only taking

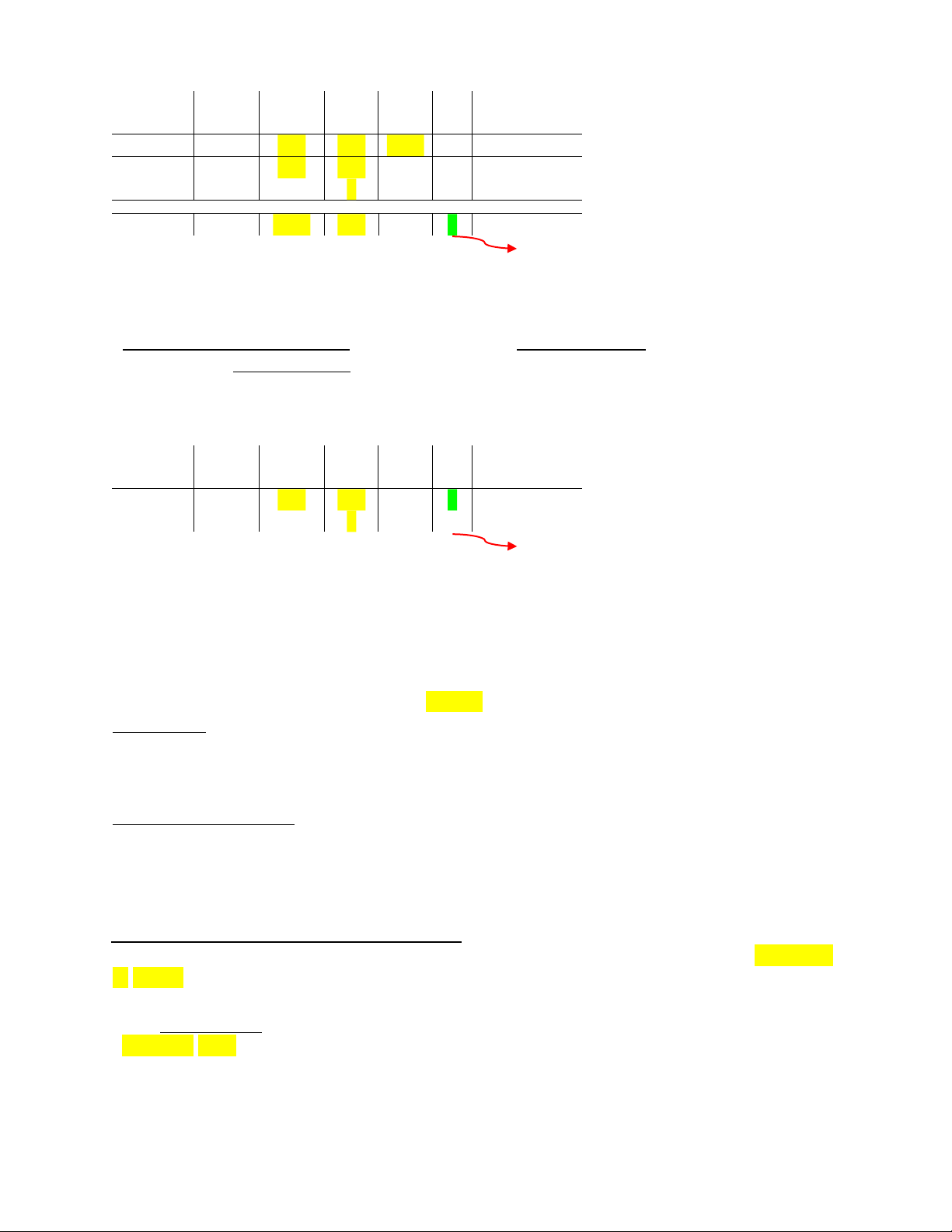

projects with a payback period of 2 years or less lOMoAR cPSD| 58562220 Project C s 0 C 1 C 2

C 3 PP NPV @10% A -2000 50 0 0 50 500 0 3 +2624 B -2000 50 0 18 0 0 2 -58 0 1800 + 500 = 2300 > C0 = 2000 C -2000 1800 500 0 2 +50 →PP: Choose B & C → NPV: Choose A

Note: PP & NPV luôn cho ra decision đối lập nhau

- Minimum acceptance criteria: Set by management - Ranking criteria: Set by

management - Disadvantages:

+ Ignores the time value of money

→ Bỏ qua bản chất của finance

+ Ignores cash flows after the payback period Ex: Project C 0 C 1 C 2

C 3 PP NPV @10% s B -2000 500 180 0 2 -58

Không quan tâm đến lời/lỗ của cash flow 0 từ năm 3 về sau

+ Biased against long-term projects

→ Prefer short-term projects

+ Requires an arbitrary acceptance criteria

→ Yêu cầu tiêu chí chấp nhận tùy ý

+ A project accepted based on the payback criteria may not have a positive NPV

→ Accept những projects mang lại giá trị NPV<0 (Không mang lại giá trị thực cho công ty) - Advantages: + Easy to understand + Biased toward liquidity

→ Có tính chất thanh khoản cao -

3 bản chất của Finance: + Time value of money (TVM)

+ High risk high return (Dự án với rủi ro càng cao sẽ mang lại lợi nhuận càng khổng lồ)

+ Value of assets equilibrium with cash flow received

IV. Discounted Payback Period (DPP) -

How long does it take the project to “pay back” its initial investment taking the time value of money into account?

→ Giống PP nhưng quan tâm time value of money -

DPP method: A project accepted if the time of recovering initial investment on the

discounted basic equal or less than specified number of years

→ Một dự án được chấp nhận nếu thời gian thu hồi đầu tư ban đầu trên cơ bản chiết khấu bằng

hoặc ít hơn số năm được chỉ định lOMoAR cPSD| 58562220

Ex: CF1= 20,000 ; CF2 = 10,000; CF3 = 10,000; CF4 = 5,000; C0 (initial investment) = 350,000; Opportunity cost = 7%

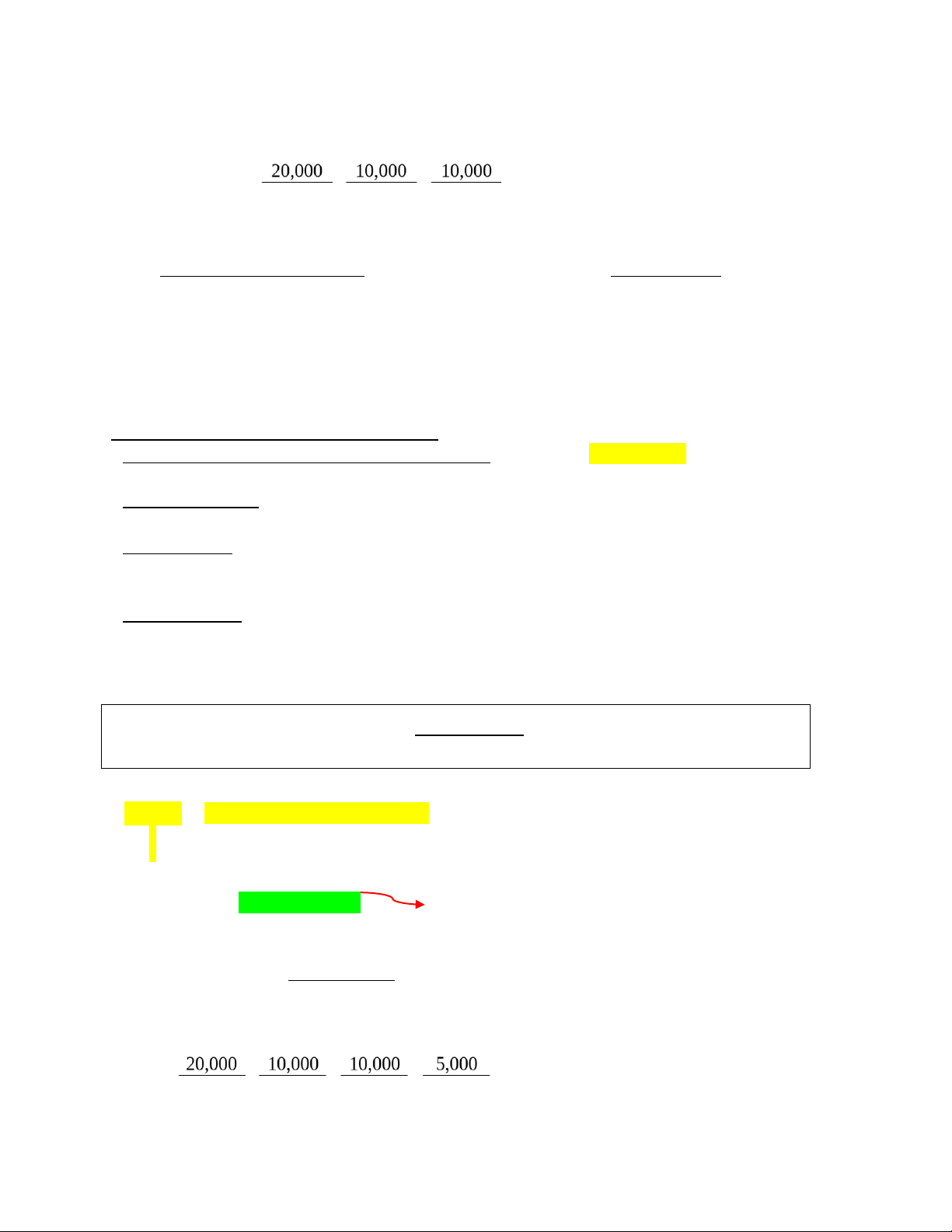

_ CF1 + CF2 + CF3 + CF4 = 20,000 + 10,000 + 10,000 = 40,000 > 35,000 → PP = 3 years DPP=−350,000+ 1+ 2+ 3 (1+7%) (1+7%) (1+7%)

→ Trong 3 năm đã đủ cover initial investment -

Advanced compared to PP: Consider time value of money - Disadvantage:

+ Still ignore any cash flows after pay back period

+ Biased against long-term projects

+ Requires an arbitrary acceptance criteria

+ A project accepted based on the payback criteria may not have a positive NPV => Giống PP

V. The Profitability Index (PI) Rule

- What happen if firms faces the capital rationing? Cannot use NVP method to rank the projects

→ Nên phân bổ vốn như thế nào để nó mang lại hiệu quả lợi ích cho công ty?

- Capital rationing: Limit set on the amount of funds available for investment

→ Giới hạn khả năng vốn, tài chính của công ty

- Soft rationing: Limits on available funds imposed by management

→ Giới hạn đối với các quỹ có sẵn do ban quản lý áp đặt (Internal source: Công ty quản trị số

tiền từ net income, e etained earnings thế nào để dư)

- Hard rationing: Limits on available funds imposed by the unavailability of funds in the capital market

→ Bị giới hạn bởi external source/cash flows, mượn bank, capital market (money market,

financial firms, các công ty hợp tác)

PI= PV of futureCF Initialinvestment

Ex: We only have $10 million to invest. Which do we select?

Project PV of CF Investment PI s J 8 6 1.33 K 10 5 1.2 L 6 7 1.43 Choose L M 8 6 1.33 N 7.2 6 1.2 25

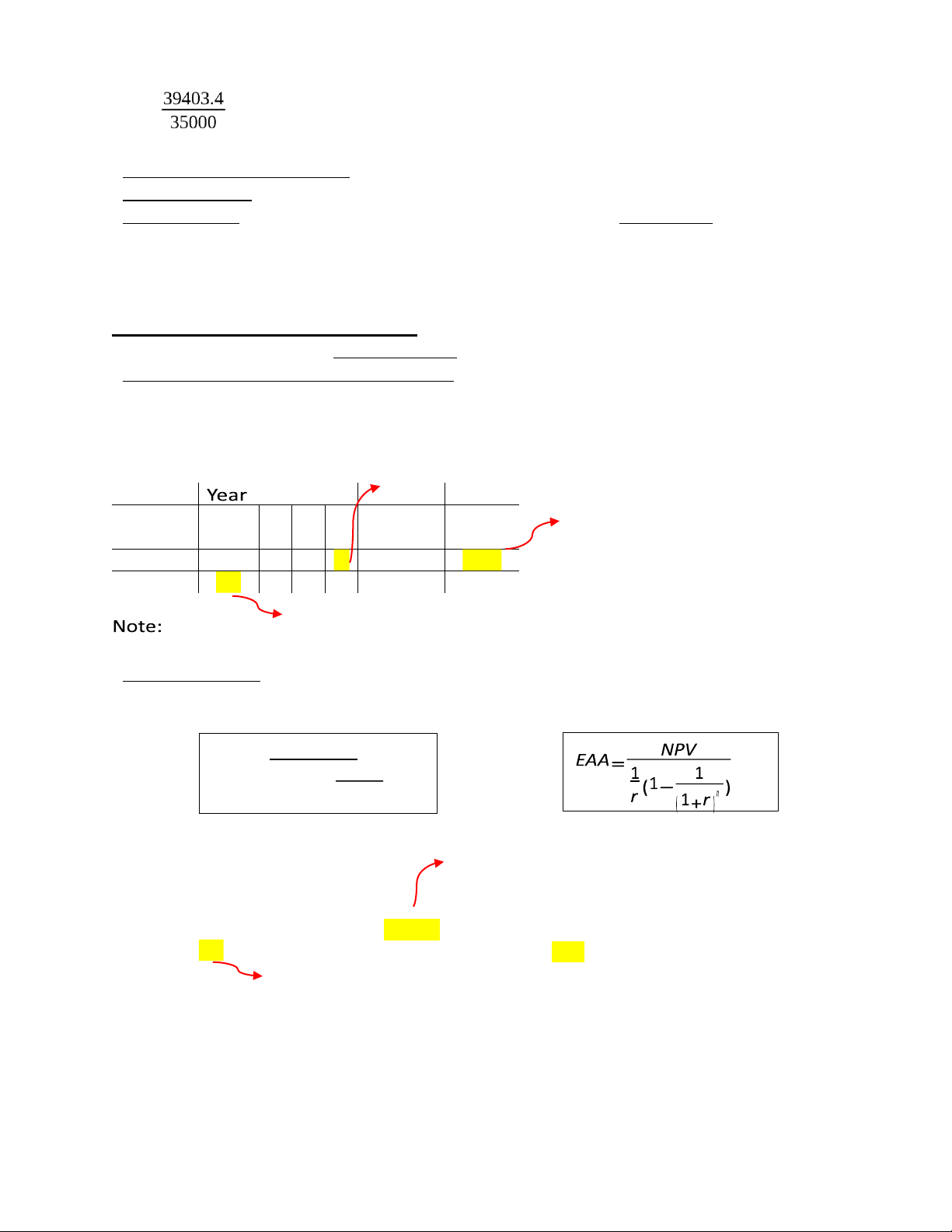

Ex: CF1= 20,000 ; CF2 = 10,000; CF3 = 10,000; CF4 = 5,000; C0 (initial investment) = 35,000; Opportunity cost = 7% +DPP= 1+ 2+ 3+ 4=39403.4 (1+7%) (1+7%) (1+7%) (1+7%) lOMoAR cPSD| 58562220 +DPP= =1.13>1 → Accept the project

- Minimum acceptance criteria: Accept if PI > 1

- Ranking criteria: Select alternative with highest PI

- Disadvantages: Problems with mutually exclusive investments - Advantages:

+ May be useful when available investment funds are limited

+ Easy to understand and communicate

+ Correct decision when evaluating independent projects

VI. Equivalent Annual Annuity (EAA)

- What happen if firm have 2 unequal projects?

- Equivalent annual annuity/cost (EAA/EAC): The cash flow period with the same present value

as the cost of buying & operating a machine

→ Liên quan đến cost of machine, equipment mình sử dụng

Ex: Given the following costs of operating 2 machines & a 6% cost of capital, select the lower

cost machine using equivalent annual annuity method Depreciation: Khấu hao Machin 0

1 2 3 PV @6% EAC Cho lowest cost (-) e F -15 -4 -4 -4 -25.69 -9.61 G -10 -6 -6 -21.00 -11.45 Chi phí mua máy

+ EAC: Choose the lowest

+ Machine: Cash flows < 0 - Steps to find EAA:

+ Step 1: Calculate NPV

+ Step 2: Calculate EAA/EAC: The equal per period with the same present value of project EAA 1 NPV= [1− n ] r (1+r) =>

Ex: Select one of the 2 following projects, based on highest “equivalent annual annuity” (r=9%) Mang lại lợi nhuận Projec C0 C1 C2 C3 C4 NPV@6% EAA t A -15 4.9 5.2 5.9 6.2 2.82 0.87 B -20

8.1Chi phí bỏ ra mua dự án8.7 10.4 2.78 1.10 Note:

- EAA: Choose the highest - Cash flow > 0: Dự án thu được lợi nhuận Ex: Opportunity cost = 7%

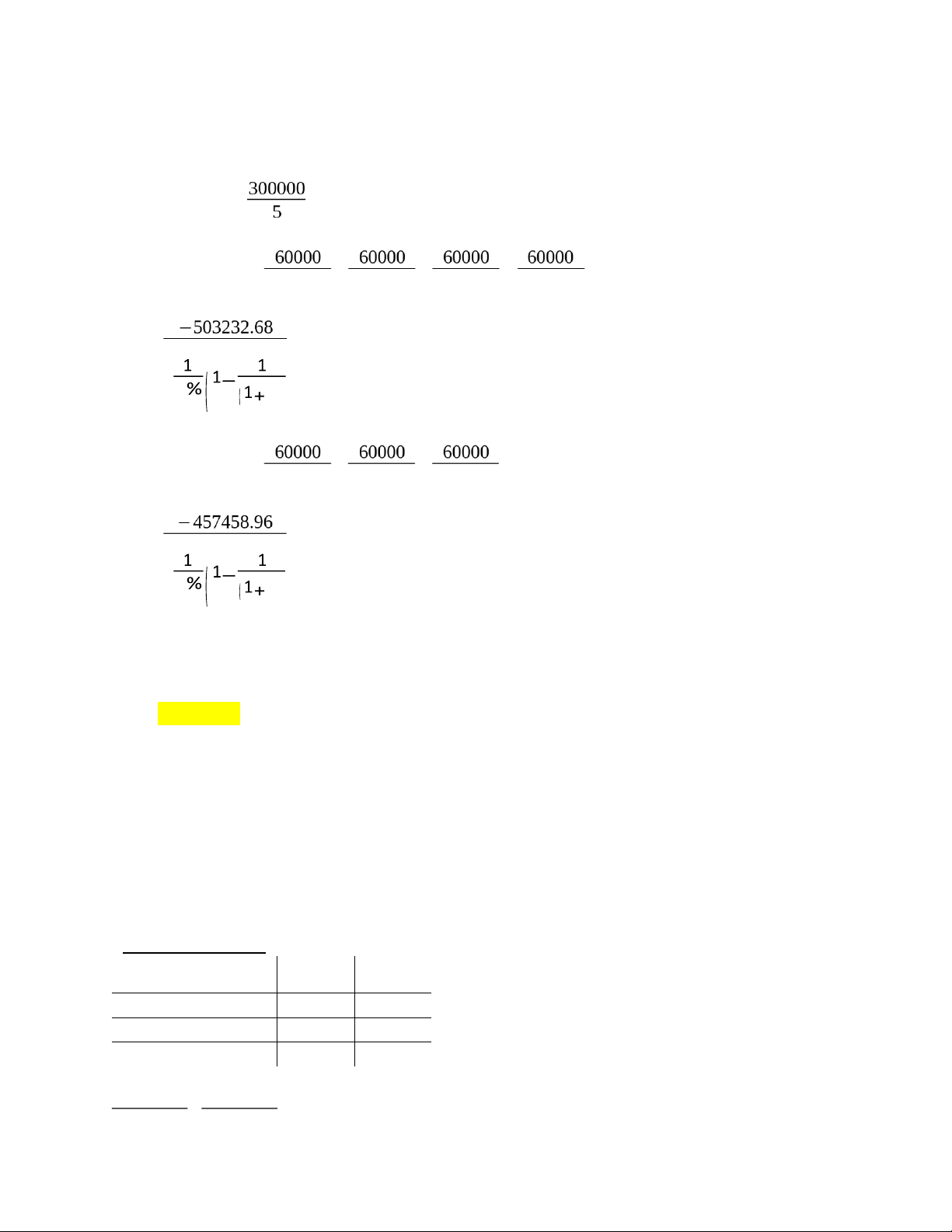

+ Project A: The purchase machine's initial investment is $300,000, the project life is 4 years, useful life in 5 years lOMoAR cPSD| 58562220

+ Project B: The purchase machine's initial investment is $300,000, the project life is 3 years, useful life in 5 years

Which one should you choose? + Depreciation = 5 years + Cash outflow = =60000 + Project A: ¿NPV=−300000− 1− 2− 3− 4=−503232.68 (1+7%) (1+7%) (1+7%) (1+7%) ¿ EAC= =−148568.44 7 r) ) 4 + Project B: ¿NPV=−300000− 1− 2− 3=−457458.96 (1+7%) (1+7%) (1+7%) ¿ EAC= =−147315.5 7 r) ) 3 → Choose project B

Capital Budgeting & Cash Flow Projection

No.1: Cash flows (Not accounting income): Only cash flows relevant

→ Không include các cash flows luôn được trả dù project có được thực hiện không (Sunk cost)

Ex: A project costs $2,000 and is expected to last 2 years, producing cash income of $1,500 and

$500 respectively. The cost of the project can be depreciated at $1,000 per year. Given a 10%

required return, compare the NPV using cash flow to the NPV using accounting income. Tax rate 0%

-> Trả $2000 cho equipment, useful life = 2 năm

+ Tại thời điểm đầu chưa tạo ra income cho doanh nghiệp nên chưa được ghi nhận là expense

+ Sau 1 năm tạo ra income cho doanh nghiệp thì ghi nhận khấu hao là $1,000

→ Không ghi nhận là expense mà chia nhỏ nó dưới dạng depreciation, ghi nhận cho kế toán

- Accounting income (Capitalizing expenses): Expenses luôn follow revenue Year 1 Year 2 Cash income $1500 $500 Depreciation -$1000 -$1000 Accounting income +$500 -$500 500 500 NPV = 1+ 2=$41.32 lOMoAR cPSD| 58562220 (1+10%) (1+10%)

- Cash flows (Expensing expenses): Chỉ quan tâm real cash flows

-> Ghi nhận luôn tại thời điểm 0, ghi nhận correct results

=> Khi làm bài, chỉ follow CFs approach Year 0 Year 1 Year 2 Cash income $1500 $500 Project cost -$2000

Free cash flow -$2000 +$1500 $500 1500 500 NPV=−2000+ 1+ 2=−$223.14 (1+10%) (1+10%)

No.2: Incremental cash flow: Dòng tiền chỉ tồn tại khi thực hiện project

- Incremental cash flow: Cash flows chênh lệch khi thực hiện với không thực hiện project

Incremental cash flow = Cash flow with project - Cash flow without project Ex:

+ Cash flows khi thực hiện project = $20,000,000

+ Cash flows khi không thực hiện project = $10,000,000

=> Incremental cash flows = $20,000,000 - $10,000,000 = $10,000,000

Important: Ask yourself this question: Would the cash flow still exist in the project does not exist?

→ Khi làm bảng Budgeting Evaluation, cash flow có được ghi vào bảng hay không? +

If yes: Do not include it in your analysis + If no: Include it

Money that has already been spent and cannot be recovered → Costs

already exists regardless of project is undertake or not - Ignore sunk costs:

Just because “We have come this far” does not mean that we

should continue to throw good money after bad

Ex: Research market cost = $15000

+ Not undertake: Still exist + Undertake: Still exist => Not incremental cost

Ex: Chi phí đã bỏ ra từ năm trước

- Include all O pportunity cost (-): What you have to give up to buy what you want in terms of other goods or services

Ex: Thay vì dùng chi phí đó để xây nhà, bán đất, cho thuê,…

- Include P roject-driven changes in W orking C apital

→ Vốn lưu động doanh nghiệp: Sử dụng khi thực hiện các hoạt động kinh doanh của công ty - After-tax flows (It gặp)

- Include S ide effects: Conduct new project will affect existing project (+)/(-)

-> Tiến hành dự án mới sẽ ảnh hưởng đến dự án hiện tại, ảnh hưởng lợi nhuận của các mặt hàng trước đó lOMoAR cPSD| 58562220

(+): Project increase demand for existing (-): Project influences on demand of existing goods goods Ex:

+ (-): Đưa iPhone 16 ra ngoài thị trường thì các dòng sản phẩm cũ với revenue sẽ bị giảm xuống

+ (+): Fraizer tung ra thị trường vaccine COVID-19 thì rất nhiều người biết đến brand & để ý đến existing products

→ Tăng revenue của existing products

No.3: Separate financing & Investment decision

- Financing: Where cash flows come from

+ Focus only the value of project

+ Ignore all financing costs (Vốn, khả năng chi trả của doanh nghiệp)

Ex: Interest payment from debt, dividend from equity, financing size

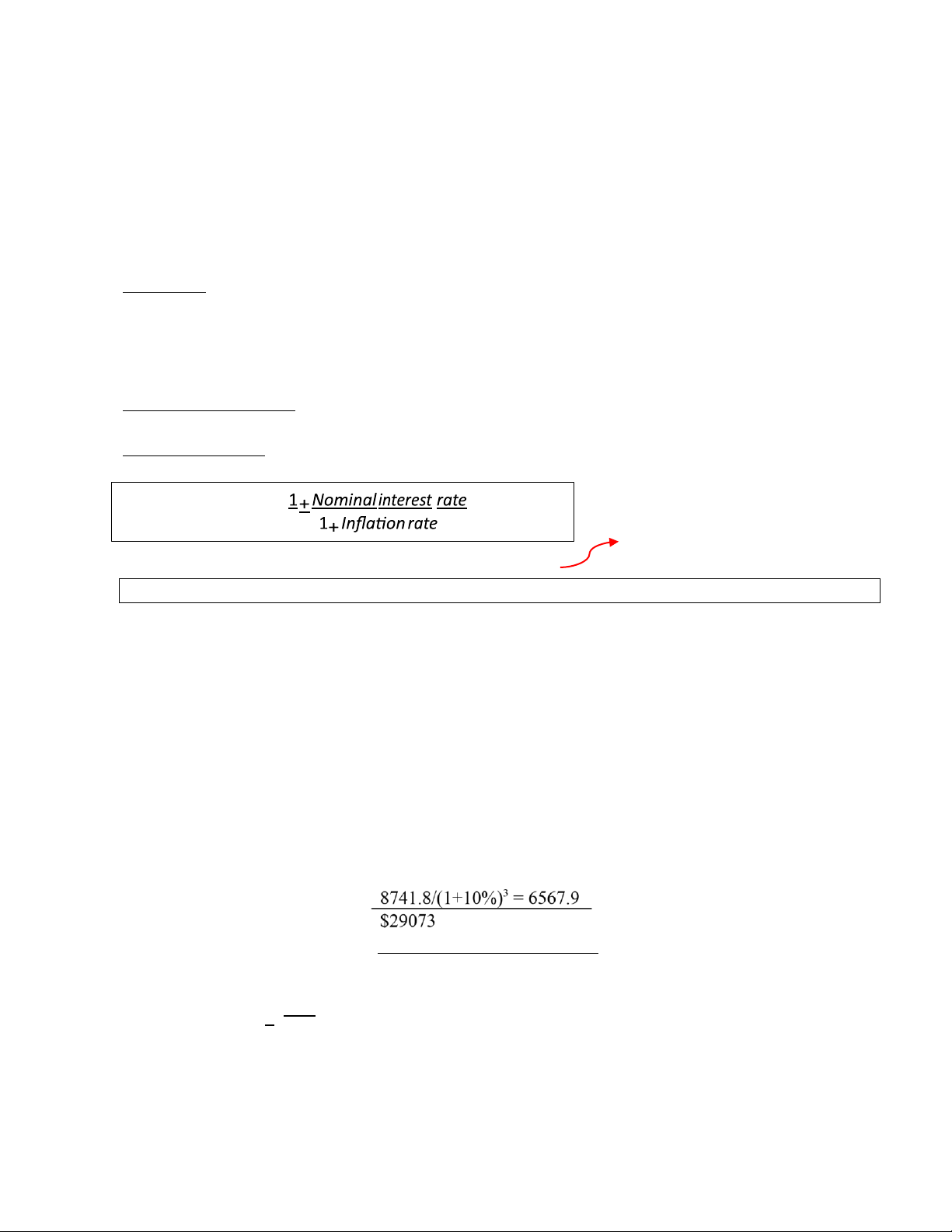

No.4: Interest rate & cash flows must be measured on the same basis

- Nominal interest rates: Discount nominal cash flows (Not include Time Value of Money) → Include inflation rate

- Real interest rates: Discount real cash flows → Exclude inflation rate 1+Realinterest rate= Cho ra kết quả gần đúng

Real interest rate = Nominal interest rate – Inflation rate

Ex: Sales revenue = $5/unit nhưng do inflation rate = 20%:

+ Nominal interest rate: Điều chỉnh sales revenue & những chi phí khác theo inflation rate 2)

+ Real interest rate: Nếu muốn sử dụng sales revenue ở mức $5/unit

→ You will get the same results, whether you use nominal or real figures

Ex: You own a lease that will cost you $8000 next year, increasing at 3% a year (The forecasted

inflation rate) for 3 additional years (4 years total). If discount rates are 10%, what is the present value cost of the lease? + Nominal cash flows: Yea Cash flow PV@10% r 0 8000 8000 1 8000 x (1+3%) = 8240 8240/(1+10%) = 7490.9 2

8000 x (1+3%)2 = 8487.2 8487.2/(1+10%)2 = 7014.2 3 8000 x (1+3%)3 = 8741.8 + Real cash flows:

1+Realinterest rate=1+10%=¿Real interestrate=6.8% 1+3% Year Cash flow PV@10% 0 8000 8000 1 8000 8240/(1+6.8%) = 7490.9 lOMoAR cPSD| 58562220 2 8000 8487.2/(1+6.8%)2 = 7014.2 3 8000

No.5: Estimating project: “After- tax incremental operating cash flows” -

Major cash flow components: + Capital investments: _ Cost of buying fixed asset _ Capitalized expenditures

→ Fund để mua fixed assets: Equipment, land,…

_ Cash from replacement (Máy xài đến lúc hư thì phải bỏ chi phí mua kẻ máy

khác) + Cash flows from operations: Income method, Tax shield method (Không

ra) + Investment in working capital:

_ Capital covered within one year

→ Nguồn vốn lưu động ngắn hạn

_ Fully recovered at the end of the project

→ Working capital năm trước được sử dụng cho năm này nên working capital năm cuối luôn = 0

Change in working capital: Dòng vốn lưu động để thực hiện kinh doanh của công ty

(Inventory, accounts payable, accounts receivable)

+ The sale of a asset fixed assets: Capital gain, Capital loss →

Khi machine/project hết giá trị sử dụng thì bán cho 1 bên khác Ex:

_ Costs of test marketing (Already spent): $250,000 = Sunk cost → Not include

_ Current market value of proposed factory site (which we own): $150,000 = Opportunity costs

→ Nếu thực hiện project thì Không thể bán machine với giá $150,000 → (-)

_ Cost of bowling ball machine: $100,000 (depreciated according to MACRS 5-year)

Quantity of good solds: Mỗi năm bán được là … units

_ Production (in units) by year during 5-year life of the machine: 5,000; 8,000; 12,000; 10,000;

6,000. Price during first year is $20; price increases 2% per year thereafter.

_ Production costs during first year are $10 per unit and increase 10% per year thereafter. _

Initial working capital requirement: $10,000. Working capital requirement is 10% of revenue each year.

_ After 5 years, market value of proposed factory site is expected to sell @$150,000, and

machine will be sold at $30,000. Tax rate is 34%

- MACRS sample schedules: Thường được cho bảng sẵn, quy định sẵn máy được sử dụng trong bao nhiêu năm

Depreciable cost = Depreciable basis x % x-recover year

Ex: Suppose a machine that has cost of baying is $100 mil is depreciated by 5-year MACRS schedule lOMoAR cPSD| 58562220

Recovery year 3-Year 5-Year 7-Year 1 33.33% 20% 14.29% 2 44.45 32 24.49 3 14.81 19.2

17.49 Khấu hao đến năm n+1 vì 4 7.41 11.52 12.49

mục đích kế toán, lợi 5 11.52 8.93

nhuận, thuế của công ty 6 5.76 8.92 7 8.93 8 4.46 Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Depreciatio 20 32 19.2 11.52 11.52 5.76 n

Note: Trong trường hợp số năm của Useful life < MACRS đề yêu cầu thì chỉ cần tính theo useful

life là được, không tính hết

Model:Tác dụng phụ: Khi 1 hoạt động được đưa vào thực hiện sẽ - Machine/Equipment cost (-)

ảnh nướng doanh thu hoạt động khác

- Shipping & Installation cost (-)

Ex: Khi đưa project iPhone 16 đi vào hoạt động thì sẽ ảnh - Opportunity cost (-)

hưởng sales of iPhone 15 xuống $500,000/year vì người

- Side effects (-)tiêu dùng chuyển sang xài iPhone 16

1) Initial investment (Sum)

-> Tổng những chi phí liên quan đến việc đưa dự án vào hoạt động - Depreciable basis

Note: Nếu đề không nói gì thì Depreciable basis = Initial investment - Quantity good sold - Selling price - Revenue

(Quantity x Selling price/unit) - Variable cost (-) - Fixed cost (-)

- Depreciation cost (-): Tính theo 2 phương pháp: Depreciable basis

+ Straight line: Depreciationcost= + MACRS Usefullife

Ex: Useful life là 7 năm mà project line của máy là 4 năm thì follow theo 4 năm

Note: Follow project line not machine useful life

- EBIT (Earning before interest & taxes) = Revenue + Variable cost + Fixed cost + Depreciation cost - Tax (Tc = x%) (-) - Net income lOMoAR cPSD| 58562220 (EBIT x (1 – Tax rate))

2) Cash flows from operation: Những dòng tiền liên quan đến hoạt động công ty

(CFO = Net income + |Depreciation cost|) - Net working capital + Năm cuối luôn = 0

3) Change in networking capital: Sự thay đổi trong nguồn vốn ngắn hạn/vốn lưu động (Năm trước – Năm sau)

+ Năm đầu = - Net working capital của nó

+ Change in networking capital năm cuối = Net working capital năm kế cuối

+ Nếu đề cho “Fully recovered upon closure of the project”: Chỉ điền số năm đầu (-) vs cuối (+) - Selling price - Book value of assets

(Depreciable basis + Total of depreciable cost) Note: Salvage value:

+ TH1: Fully depreciated: Book value = 0 & Salvage value = Selling price

+ TH2: Useful life = The year of MACRS: Book value = 0 & Salvage value = Selling price

Ex: Useful life = 4 & MACRS 3-year

+ TH3: Đề đã cho selling price: Salvage value = Book value - Capital gain/loss - Tax/Tax saving (Tc = x%)

+ Tax < 0: Gain mới phải trả tax

+ Tax saving > 0: Loss

4) Cash flow from selling assets

(Selling price + Tax/Tax saving)

Note: Cả mục (4) là ghi tại năm cuối 5)

Cash flows = (1) + (2) + (3) + (4)

Note: Luôn phải có conclusion sau khi tính NPV:

+ NPV > 0: Undertake the project

+ NPV < 0: Not accept the project

Ex: Abbott Corp analyzes a capital budgeting case where the company wants to add a new

product. The following information about the product is estimated by Abbott’s financial manager

and passed on to you: - Project life : 3 years

- The production would need to use currently available, existing machinery of the company. The

company spent $10,000 last year to renovate this machinery (for some repainting and

maintenance). If the machinery is not used for this project, Tuong An Corp. would lease it on a

5-year contract for $45,000 (after-tax) each year, starting one year from now. After 5 years of

being leased, the machine would have no value to the company. Book value of the existing machine is $180,000

- If the company decides to use the machinery for this project, it would be depreciated according

to a 3-year property MACRS schedule. At the end of the project life, it could be sold as scrap for $ 15,000.

- The project requires an initial investment in working capital of $15,000, which is fully

recovered upon closure of the project lOMoAR cPSD| 58562220

- This project is expected to generate sales of 1,450 bottles per year at a cost of $120 per bottle in

the first year, excluding depreciation. Each bottle can be sold for $200 in the first year. The

sales price and cost are expected to increase by 10% per year due to inflation.

- The company takes a bank loan to finance the project, and is expected to pay $2,500 as interest

expense per year over the life of the project.

- The company‘s tax rate is 35%, and its overall cost of capital (WACC) is 10%. 0 1 2 3 Opportunity cost -45000 -45000 -45000 1) Initial investment -45000 -45000 -45000 Depreciable basis 180000 Quantity of good sold 1450 1450 1450 Cost/unit -120 -132 -145.2 Total cost -174000 -191400 -210540 Selling price/unit 200 220 242 Revenue 290000 319000 350900 Depreciation cost -59994 -80010 -26658 EBIT 56006 47590 113702 Tax (Tc = 35%) -19602.1 16656.5 39795.7 Net income 36403.9 30933.5 73906.3

2) Cash flows from operation 96397.9 110943.5 100564.3 Net working capital 15000 0 0 0

3) Change in net working capital -15000 15000 Selling price 15000 Book value of assets 13338 Capital gain 1662 Tax (Tc = 35%)

-581.7 4) Cash flows from selling assets 14418.3

5) Cash flows -15000 51397.9 65943.5

84982.6 Introduction To Risk & Return

I. Measuring risk & return for individual investment

- Individual investments: Đầu tư vào 1 dự án

- Historical rates of return: Rate of return on investing in a stock for a year (or a period) lOMoAR cPSD| 58562220 Capital gain Dividend =Capital yield =Dividend yield Initial share price Initial share price

Percentagereturn=Capitalgain+Dividend=Capital yield+Dividend yield Initial share price =

Sự tăng giá của cổ phiếu: Công ty sẽ giữ lại để tái đầu tư

Giá trị cổ phiếu trong tương lai

Dividend được trả mỗi năm trong tương lai

Percentagereturn=(Pt−Pt−1)+Dt Pt−1

- Khi mua cổ phiếu, người ta sẽ chú ý đến Capital yield hơn là Dividend yield

Ex: An investor bought a stock of Wall-Mart one year ago at $31.12. Dividend is paid at $0.82

one and now the investor sell the stock at $36.59. How much rate of return over 1 year does investor earn? Percentage return = =20.2%

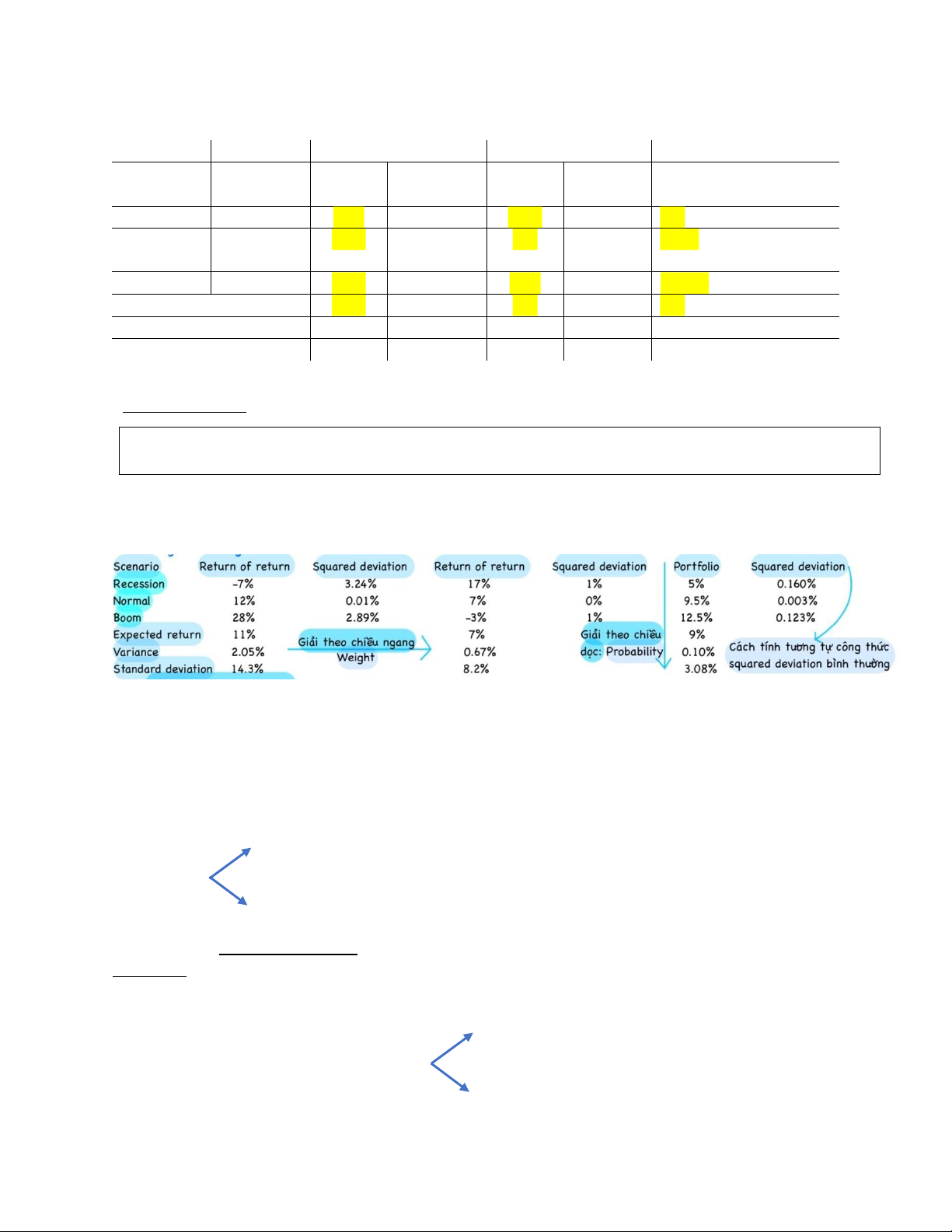

- Expected return, variance, and coefficient of variation: Phải đặt những expect vào từng scenario: Scenario Probaility Return stock fund

Recession: Kinh tế suy thoái 1/3 -7%

Normal: Kinh tế phát triển bình thường 1/3 12%

Boom: Kinh tế phát triển mạnh 1/3 28%

Để tính xem có nên đầu tư hay không

Expected return: E(r) = (Probability x Return stock fund) of Recession + (Probability x

Return stock fund) of Normal + (Probability x Return stock fund) of Boom

Sum of potential returns multiplied with the corresponding

E(rprobability of the returns)= 1/3 x (-7%) + 1/3 x 12% + 1/3 x 28% = 11%

- Variance (Phương sai): A measure of the variance of possible rates of return Ri from the

expected rates of return or mean return

- Standard deviation (Độ lệch chuẩn): Measures how far (risk) each random variable (possible

return) varies from the mean (expected return)

-> Đo lường mức độ (rủi ro) mỗi biến ngẫu nhiên (lợi nhuận có thể) thay đổi so với giá trị

trung bình (lợi nhuận dự kiến) + B1: Tính Expected return: E(r)

+ B2: Tính Squared deviation of each scenario = (Expected return - Rate of return of each)2

+ B3: Variance = Squared deviation x Probability of each scenario

+ B4: Standard deviation (σ) = √Variance = Volatility = Measurement of risks Small SD: Less risk Large SD: High risk lOMoAR cPSD| 58562220

→ The greater SD of returns, the greater variability of returns, the greater risk of the investment

→ SD căng cao, risk càng lớn -> Yêu cầu return cao tương ứng

=> High risk, high returns Ex: Scenario Probailit y Rate of return Squared deviation Recession 1/3 -7% 3.24% = (11% - (-7%))2 Normal 1/3 12% 0.01% = (11% - 12%)2 Boom 1/3 28% 2.89% = (11% - 28%)2 Expected Return 11% Variance (σ2) 1 1 1 2.05% =

×3.24 %+ ×0.01%+ ×2.89% 3 3 3

Standard deviation (σ) 14.3% = √2.05%

Ex: If the economy is normal, Charleston Freight stock is expected to return 15.7 percent. If the

economy falls into a recession, the stock's return is projected at a negative 11.6 percent. The

probability of a normal economy is 80 percent while the probability of a recession is 20 percent.

What is the variance of the returns on this stock? + rnormal = 15.7% + Pnormal = 80% + Precession = 20% + rrecession = -11.6%

+ E(r) = 15.7% x 80% - 11.6% x 20% = 10.24%

+ Squared deviation (normal) = (10.24% - 15.7%)2 = 2.98x10-3

+ Squared deviation (recession) = (10.24% + 11.6%)2 = 0.048

+ Variance = 80% x 2.98x10-3 + 20% x 0.048 = 0.012

- Coefficient of variation (CV): Measure of the risk per unit of return

→ Đo lường rủi ro trên mỗi đơn vị lợi nhuận

→ SD đo lường tổng, CV đo return/unit σ CV= r

=> Choose the project with lowest CV

- Providing a more meaningful risk measure (Unit free measure): When expected return on 2 assets are not the same

II. Portfolio analysis: The two - Asset portfolio -

Portfolio: A combination of two or more assets (>=2 assets)

→ Cụm đầu tư, có nhiều dạng đầu tư

Ex: Có thể đầu tư stock của cả firm A & B, đồng thời đầu tư bond

- Diversification: Strategy designed to reduce (unsystematice) risk by spreading the portfolio across many investments

→ Benefit của portfolio: Đa dạng hoá nguồn đầu tư, tài sản để giảm rủi ro & có được lợi ích, return tốt nhất

Note: Không eliminate mà chỉ reduce, không dùng cho systematic risk lOMoAR cPSD| 58562220

Ex: The risk-return trade off of a portfolio that is 50% invested in bonds & 50% invested in stocks (weight of money) Stock fund Bond fund

Scenario Probaility Rate of Squared Rate of Squared Portfolio return deviation return deviation Recession 1/3 -7% 3.24% 17% 1% 5% = (-7% - 17%)/2 Normal 1/3 12% 0.01% 7% 0% 9.5% = (12% + 17%)/2 Boom 1/3 28% 2.89% -3% 1% 12.5% = (28% - 3%)/2 Expected return 11% 7% 9% = (11% + 7%)/2 Variance 2.05% 0.67% Standard deviation 14.3% 8.2%

Note: Stocks have a higher expected return & risk than bonds

- Weight of money: Tỉ lệ chia tiền vào bonds & stocks dựa trên tổng số tiền đang có

+ Portfolio = wB x rB + wS x rS

+ E(rp) = wB x E(rB) + wS x E(rS)

→ Based on market value investment of each stocks

Note: Weighted average: Chia 50-50

Note: Equally invested: Các w bằng nhau

Ex: You have $10,000 to invest in a stock portfolio. Your choices are Stock X with an expected

return of 13 percent and Stock Y with an expected return of 8 percent. Your goal is to create a

portfolio with an expected return of 12.4 percent. All money must be invested. How much will you invest in Stock X?

+ E(rp) = wX x E(rX) + wY x E(rY)

=> 12.4% = wX x 13% + wY x 8% (1) + wX + wY = 1 (2) wX = 88% + (1), (2) =>

wY = 12% + Invest in X: 10000 x

88% = 8800 - Các bước tính cho Portfolio:

+ B1: Tính Rate of return of portfolio

+ B2: Tính Expected return of portfolio

+ B3: Tính Squared deviationTính theo công thức bình thường

+ B4: Tính Variance & Standard deviation lOMoAR cPSD| 58562220

Tính theo Weight x Variance hoặc Weight x Standard

deviation từng thành phần

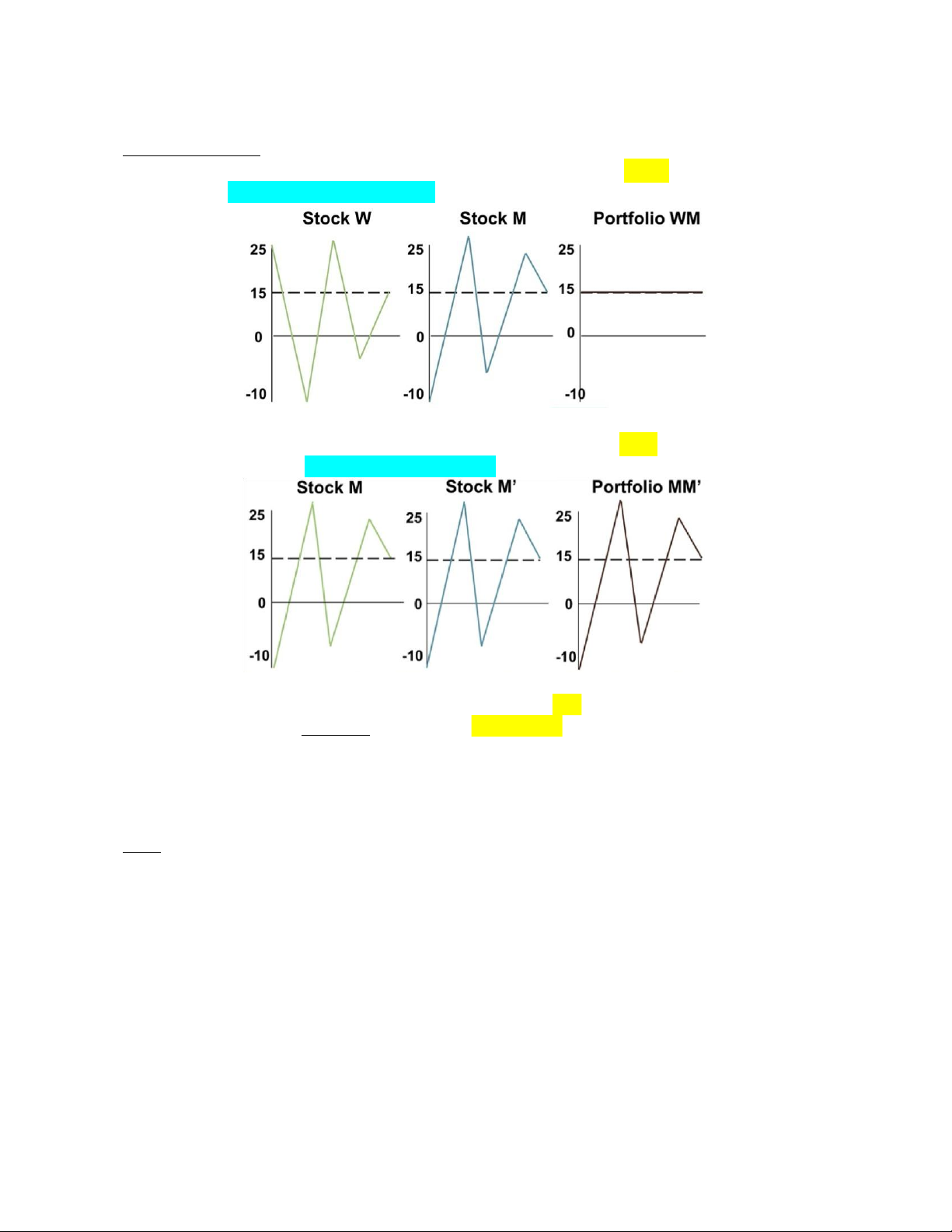

- Correlated stocks: Relationship between 2 or 3 stocks

+ Returns distribution for 2 perfectly negatively correlated stocks p = -1() : Return for the 2

assets have the same percentage movement, but in opposite direction

→ W & M move in the opposite direction

+ Returns distribution for 2 perfectly positively correlated stocks p = 1() : Return for the 2

assets move together in a completely linear manner

→ W & M move in the same direction

+ Returns distribution for no relations correlated stocks ( p= 0 ): There is no linear relationship

between two returns, but not mean that they are independen t

Note: Investor should invest in negatively correlated stocks:

+ Positively: 2 stocks thực tế là cùng 1 stock (cùng tăng/lời, cùng giảm/lỗ)

→ Không thể giảm rủi ro

+ Negatively: 1 tăng, 1 giảm: Giảm rủi ro bị lỗ quá nhiều

- Risk: The probability that some unfavorable event will happen

→ Xác suất của những sự kiện không mong muốn sẽ xảy ra

+ Market Risk/Systematic risk/Undiversible risk: Economy-wide sources of risk that affect the overall stock market

→ Rủi ro không thể tránh được, ảnh hưởng đến toàn bộ các công ty trên thị trường

Ex: COVID khiến các công ty trên thế giới phá sản hoàn toàn; các loại tax; inflation

_ The only relevant risk for consideration: Rủi ro liên quan duy nhất cần xem xét

+ Unique Risk/Diversifiable risk/Unsystematic risk/Firm specific risk: Risk factors affecting only that firm

→ Rủi ro chỉ ảnh hưởng đến 1 hoặc 1 vài công ty, có thể tránh khỏi

Ex: Trong năm 2023, người dân VN có xu hướng giảm xem chương trình giải trí → Chỉ có ngành

giải trí ảnh hưởng (Specific field) lOMoAR cPSD| 58562220

The greater the systematic risk, the greater the

return that investor will expect from security

Total risk = Unsystematic risk + Systematic risk = Beta

Investors are not rewarded or bearing risk Porfolio risk = σ

that can be eliminated through diversification

- Portfolio risk as a function of the number of stocks in the portfolio:

+ In a large portfolio, the

terms are effectively diversified v ariance away, but the

covariance terms are not

→ Trong một danh mục đầu tư lớn, các số hạng phương sai được đa dạng hóa một cách hiệu quả,

nhưng các số hạng hiệp phương sai thì không.

+ Thus, diversification can eliminate some, but not all of the risk of individual securities

→ Chỉ có thể giảm thiểu rủi ro, cannot delete total unsystematic risks

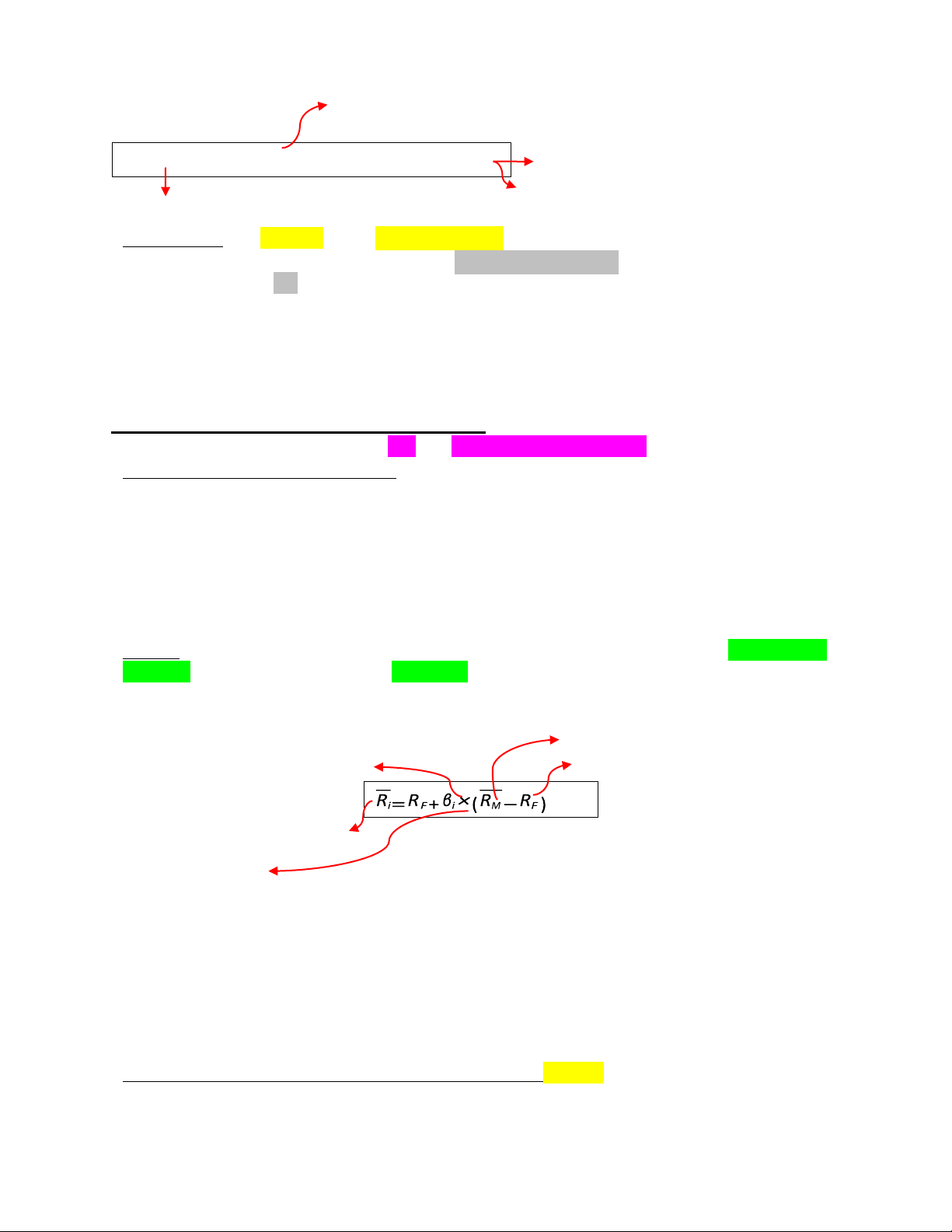

III. Capital asset pricing model (CAPM)

- Describe the relationship between risk and expected (required) return

- One practical application of CAPM: Its use in calculating the required rate of return for an

investment proposal, which then becomes the discount rate, or cost of capital

→ Một ứng dụng thực tế của CAPM là việc sử dụng nó trong việc tính toán tỷ suất lợi nhuận cần

thiết cho một đề xuất đầu tư, sau đó trở thành tỷ lệ chiết khấu hoặc chi phí vốn

- Provide a way to calculate the return that market is expected to deliver for bearing systematic risk

→ Cung cấp một cách để tính toán lợi nhuận mà thị trường dự kiến sẽ mang lại cho việc chịu rủi ro có hệ thống

- CAPM: Theory of the relationship between risk and return which states that the expected risk

premium on any security equals its beta times the market risk premium

→ Lý thuyết về mối quan hệ giữa rủi ro và lợi nhuận nói rằng phần bù rủi ro dự kiến đối với bất

kỳ chứng khoán nào bằng với phần bù rủi ro thị trường của nó Market risk premium Risk-free rate Return of market Expected return on a security Beta of the security:

Số liệu đo lường rủi ro, mức độ nhạy cảm của stock với thị trường (Sensitivity to the market) →

Beta càng thấp thì expected return càng ít bị thay đổi bởi thị trường khủng hoảng, dùng để đo systematic risk

+ Average stock & Market portfolio: Beta =1

+ High-beta stocks (Beta >1): Market-sensitive: Go up a lot when the market is up & down a lot when the market is down

+ Low-beta stocks (Beta <1): Much less sensitive to movements in the broad market

Note: Stock nào has more systematic risk/risker: Chọn Beta lớn

- Relationship between each elements to expected return: Positive relationship (cùng tăng, cùng giảm)

+ Beta=0: Expected return = Risk-free rate lOMoAR cPSD| 58562220

+ Beta=1: Expected return = Return of market: Market porfolio

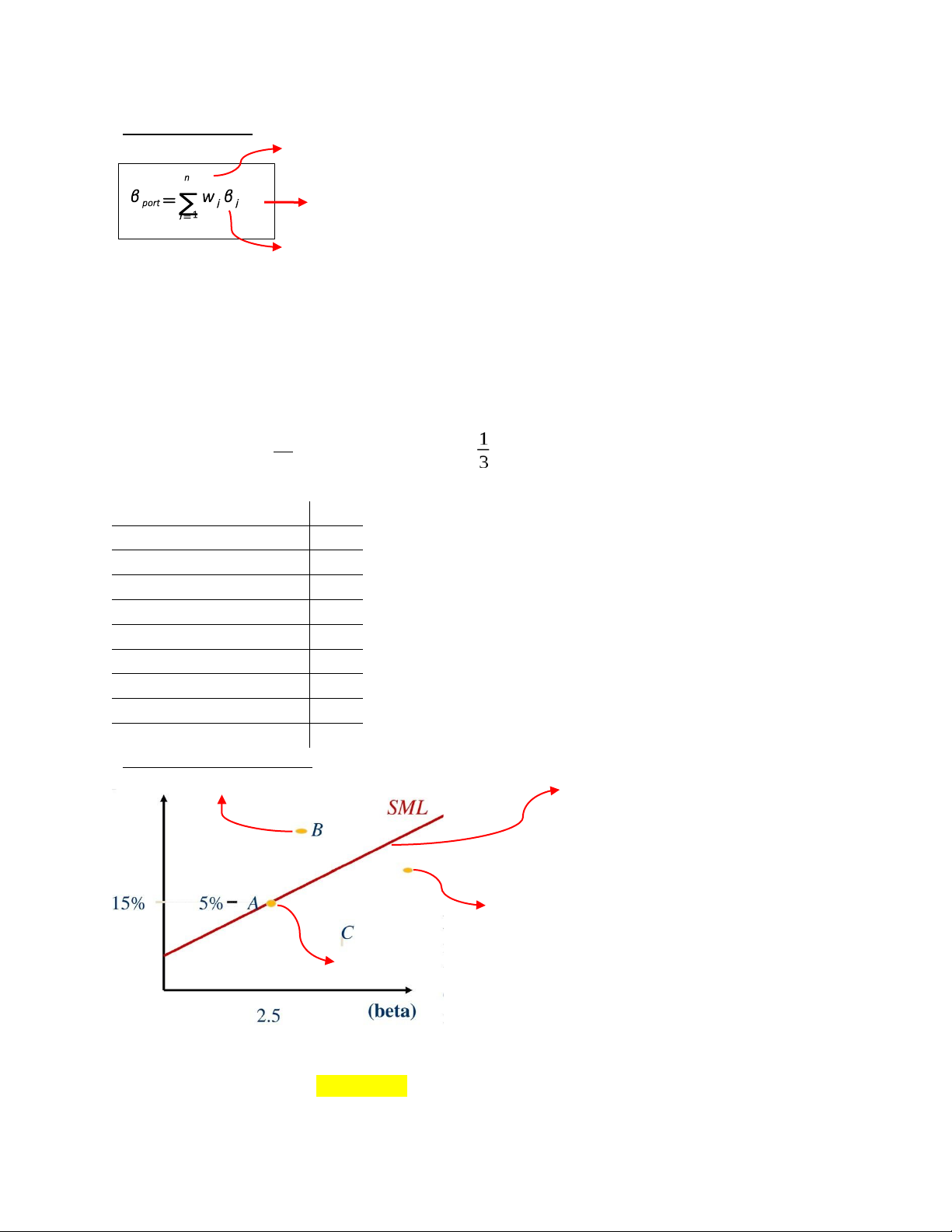

- Beta of portfolio: A weighted average of beta of each securities/scenarios in the portfolio

Number of fund invested in asset j

Tổng của Beta of each securities x Weight

The proportion of fund invested in assets j

Note: Total portfolio is equally as risky as the market: β p=1

Ex: You own a portfolio equally invested in a risk-free asset and two stocks (Ws1= Ws2 = Wa

⅓). One of the stocks has a beta of 1.9 and the total portfolio “is equally as risky as the

market” (Bp = 1). What is the beta of the second stock?

+ Risk-free asset => βa=0 + ws1 = ws2 = wa = ⅓ + βs1=1.9 11

+ β p=1=ws1×βs1+βs2×ws2+βa×wa=3 ×1.9+×

βs2+3 ×0=¿βs2=1.1 Ex: Stock Beta Beta Bank of America 1.55 Borland international 2.35 Travelers, Inc. 1.65

+ 9 stocks -> Probability = 1/9 Du Pont

1.00 + Beta of portfolio = 1/9x1.55 + 119x2.35 + 1/9x1.65 + 1/9 x

Kimberly - Clark Corp. 0.9 1+ 1/9 x 0.9 + 1/9x1.05 + 1/9x0.55 + 1/9x0.2 + 1/9x0.49 = Microsoft 1.05 1.082 Green Mountain Power 0.55 Homestake Mining 0.2 Oracle, Inc. 0.49 - Ov

er/Under price stocks :

Price Price > Expected return: Over price/value Trục của expected return ( value )

Price < Expected return: Under price/value

Price = Expected return: Tại điểm equilibrium

+ Basic principle in finance: The inverse relationship between (estimated) return & price (value)

_ Higher estimated return: Lower price (Under-valued compared to equilibrium price shown in SML lOMoAR cPSD| 58562220

→ Beta càng cao, expected return càng cao stock đang nhạy cảm với thị trường nên sẽ cho actual price < expected return

_ Lower estimated return: Higher price (Over-valued compared to equilibrium price shown in SML

Capital Structure – Cost of Capital I. Capital structure

- Capital structure: The firm's mix of long term debt financing & equity financing

→ Sự kết hợp giữa tài trợ nợ dài hạn và tài trợ vốn chủ sở hữu của công ty

+ Debt: Nợ, trả interest spend, chủ nợ công ty, lower risks

+ Equity (được prefer hơn): Vốn chủ sở hữu, trả dividends, một trong nhiều chủ sở hữu công ty, high risks

- Cost of capital: The return the firm's investors could expect to earn if they invested in the

securities having comparable degree risk

→ Lợi nhuận mà các nhà đầu tư của công ty có thể mong đợi kiếm được nếu họ đầu tư vào

chứng khoán có rủi ro tương đương

+ Cost of equity: Common stock

+ Cost of preferred stock: Stock không có voting rights trong doanh nghiệp

+ Cost of debts (Bank loans): Mượn tiền từ ngân hàng, doanh nghiệp, công ty tài chính

+ Cost of debts (Bonds): Có quyền phát hành trái phiếu & cổ phiếu

→ Đầu tư vào nhiều nguồn, mỗi dạng tiền có different required of returns

Note: Bond € debts, Share (cổ phiếu) € equity

- The Weighted Average Cost of Capital (WACC) is given by: Weighted of equity

Equity Debt rWACC= Equity+Debt

×rEqtuity+Equity+Debt ×rDebt ×(1−T C)

Discount rate: Đưa stock & bond về chỉ số chung Tax rate

- Because interest espense is tax-deductible that we multiply the last term by (1 – TC)

→ Khi trả lãi suất của debt sẽ được giảm thuế

- Taxes: An important consideration in the company cost of capital because interest payments

are deducted from income before tax is calculated

→ Cái quan trọng để tính cost of capital vì các khoản thanh toán lãi được khấu trừ từ thu nhập trước khi tính thuế

Ex: Taxes giảm từ 10% còn 8% nhưng các doanh nghiệp không muốn vì khi trả lãi suất cho ngân

hàng sẽ được miễn thuế dựa trên tax (Tax căng cao càng được miễn nhiều), lợi của giảm lãi suất

ngân hàng > lợi của đóng thuế

Note: Tax của doanh nghiệp dao động từ 20-30%, thường là 25%

After - Tax cost of debt = Pretax cost x (l - Tax rate) = rdebt x (1 - TC) Cost of equity

Tài liệu liên quan:

-

Time Value of Money: Review Notes for Exam Preparation | Môn Fundamentals of Financial Management - Trường Đại học Quốc tế, Đại học Quốc gia Thành phố Hồ Chí Minh

88 44 -

Midterm Exam Notes Môn Fundamentals of Financial Management | Trường Đại học Quốc tế, Đại học Quốc gia Thành phố Hồ Chí Minh

109 55 -

Practise Môn Fundamentals of Financial Management | Trường Đại học Quốc tế, Đại học Quốc gia Thành phố Hồ Chí Minh

75 38 -

Payback Period and Investment Analysis Fundamentals | Môn Fundamentals of Financial Management - Trường Đại học Quốc tế, Đại học Quốc gia Thành phố Hồ Chí Minh

87 44