Inflation and Exchange Rate Dynamics Analysis | Kinh tế chính trị Mác - Lênin | Đại học Tôn Đức Thắng

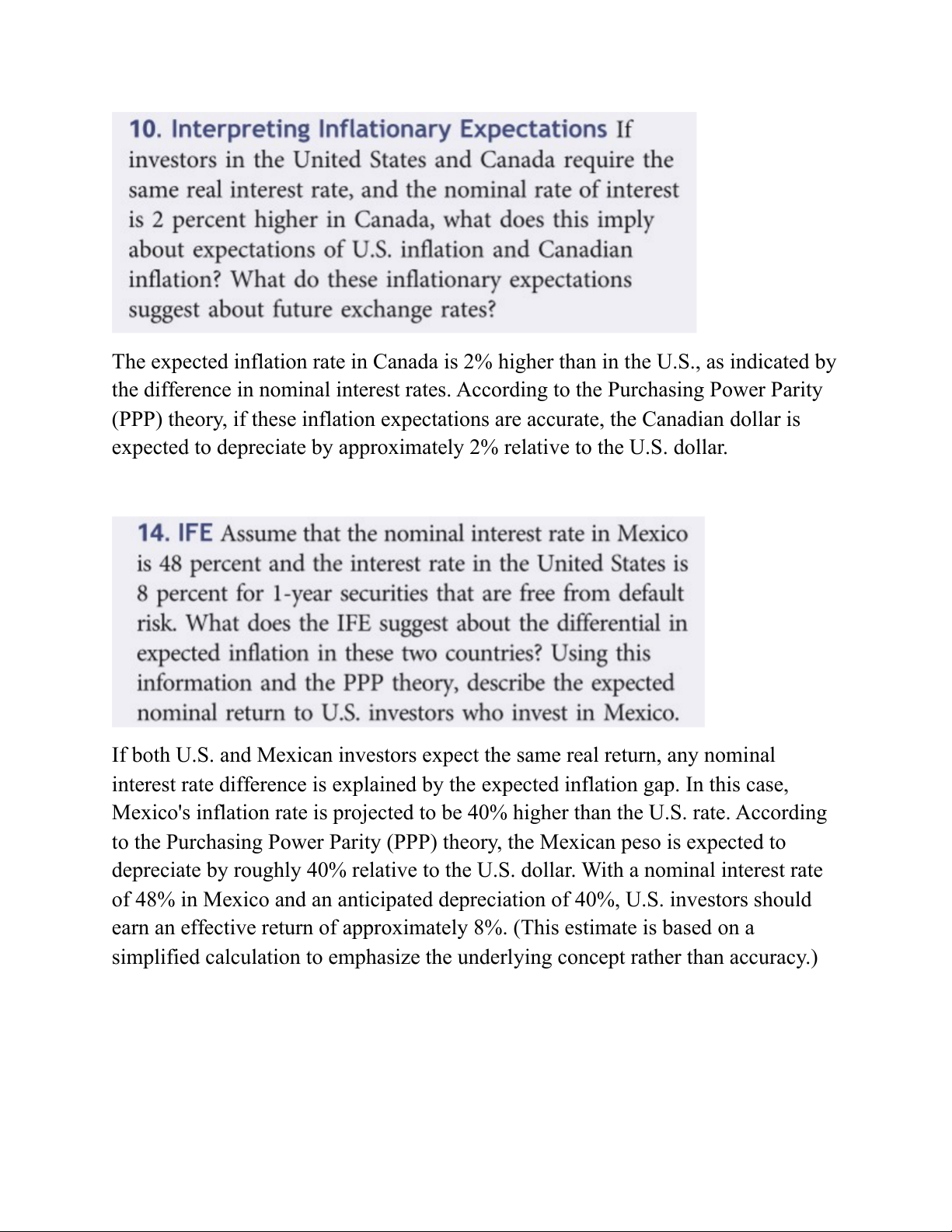

The expected inflation rate in Canada is 2% higher than in the U.S., as indicated by the difference in nominal interest rates. According to the Purchasing Power Parity (PPP) theory, if these inflation expectations are accurate, the Canadian dollar is expected to depreciate by approximately 2% relative to the U.S. dollar. Tài liệu được sưu tầm và soạn thảo dưới dạng file PDF để gửi tới các bạn cùng tham khảo, ôn tập đầy đủ kiến thức, chuẩn bị cho các buổi học thật tốt. Mời bạn đọc đón xem!

Môn: Kinh tế chính trị Mác - Lênin (306103) 253 tài liệu

Trường: Trường Đại học Tôn Đức Thắng 4.5 K tài liệu

Tác giả:

Preview text:

The expected inflation rate in Canada is 2% higher than in the U.S., as indicated by

the difference in nominal interest rates. According to the Purchasing Power Parity

(PPP) theory, if these inflation expectations are accurate, the Canadian dollar is

expected to depreciate by approximately 2% relative to the U.S. dollar.

If both U.S. and Mexican investors expect the same real return, any nominal

interest rate difference is explained by the expected inflation gap. In this case,

Mexico's inflation rate is projected to be 40% higher than the U.S. rate. According

to the Purchasing Power Parity (PPP) theory, the Mexican peso is expected to

depreciate by roughly 40% relative to the U.S. dollar. With a nominal interest rate

of 48% in Mexico and an anticipated depreciation of 40%, U.S. investors should

earn an effective return of approximately 8%. (This estimate is based on a

simplified calculation to emphasize the underlying concept rather than accuracy.)

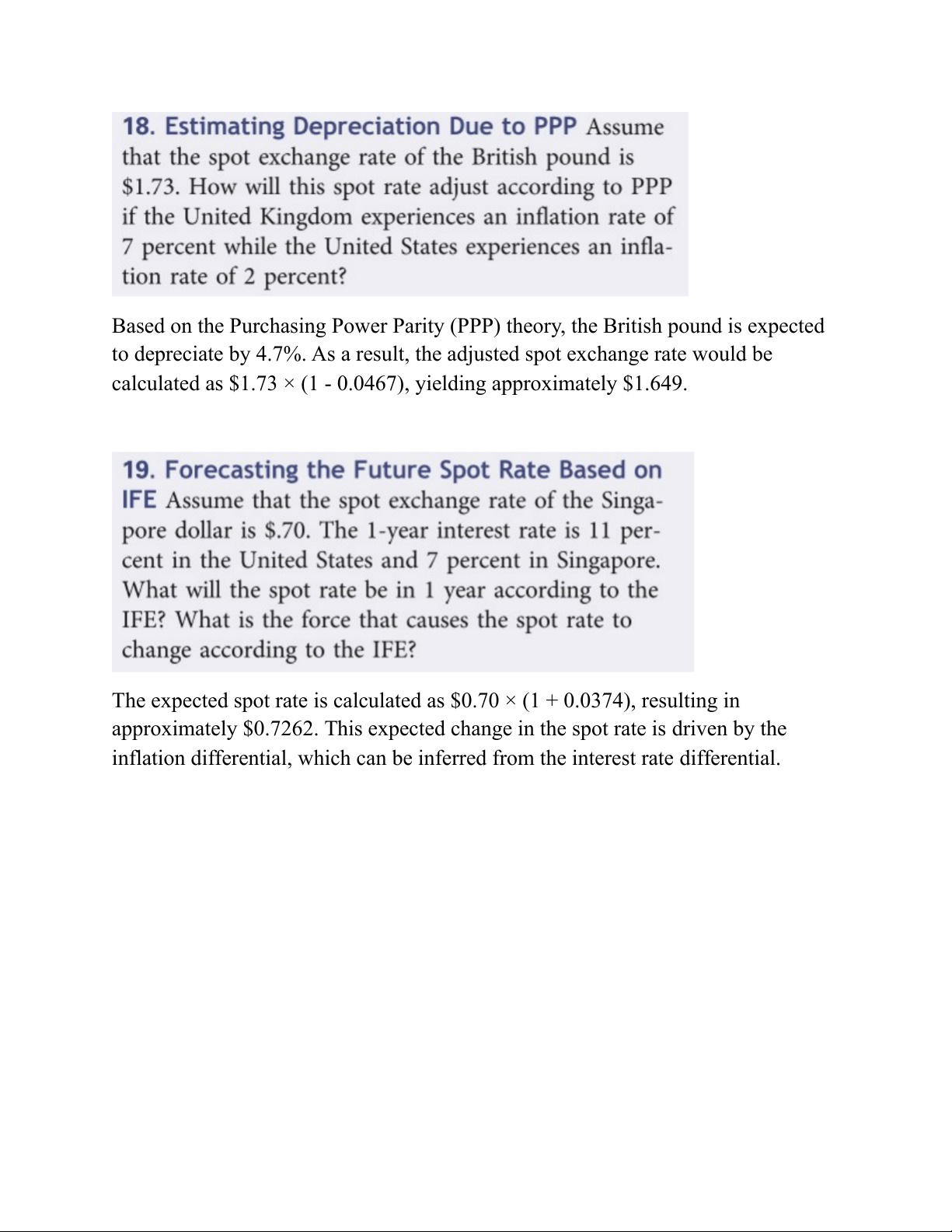

Based on the Purchasing Power Parity (PPP) theory, the British pound is expected

to depreciate by 4.7%. As a result, the adjusted spot exchange rate would be

calculated as $1.73 × (1 - 0.0467), yielding approximately $1.649.

The expected spot rate is calculated as $0.70 × (1 + 0.0374), resulting in

approximately $0.7262. This expected change in the spot rate is driven by the

inflation differential, which can be inferred from the interest rate differential.

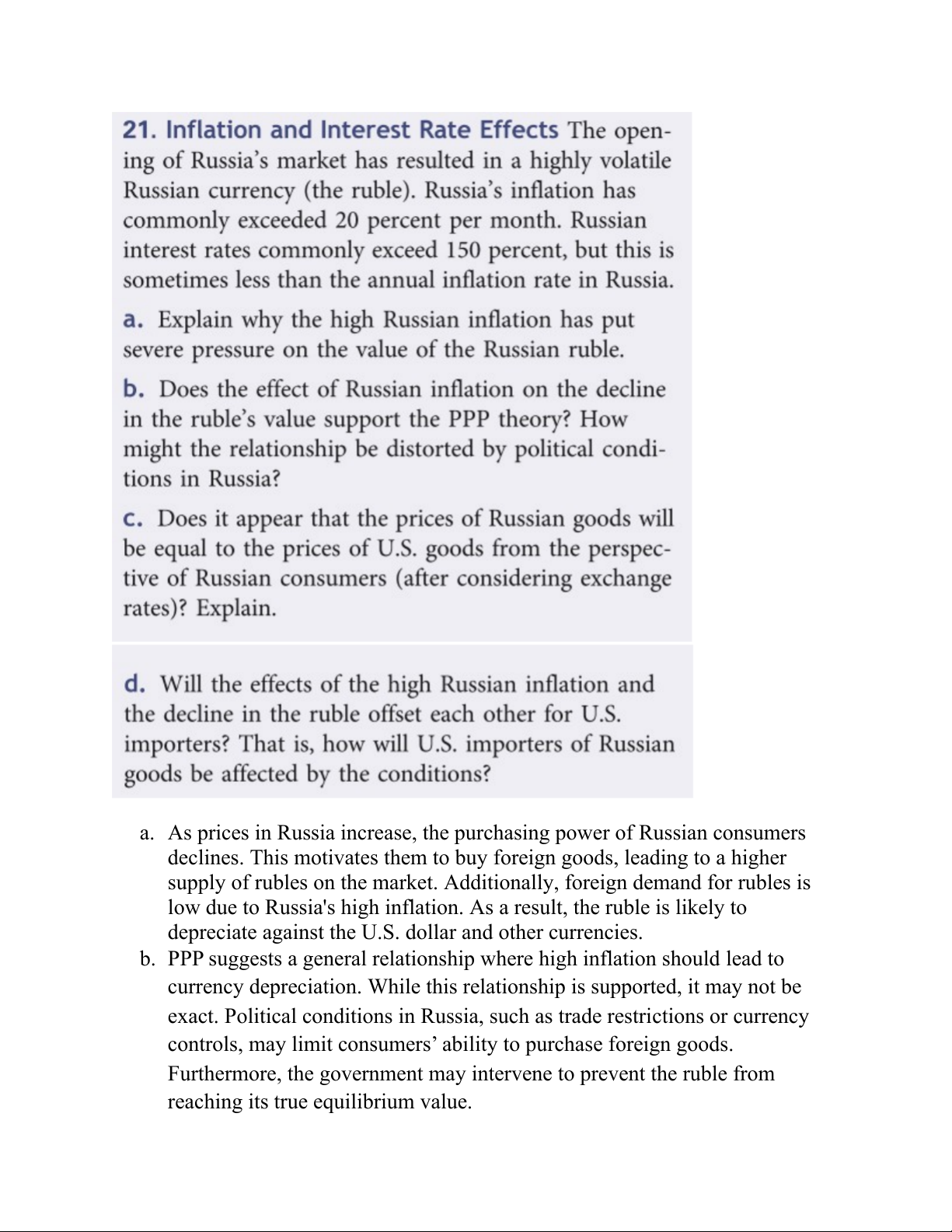

a. As prices in Russia increase, the purchasing power of Russian consumers

declines. This motivates them to buy foreign goods, leading to a higher

supply of rubles on the market. Additionally, foreign demand for rubles is

low due to Russia's high inflation. As a result, the ruble is likely to

depreciate against the U.S. dollar and other currencies.

b. PPP suggests a general relationship where high inflation should lead to

currency depreciation. While this relationship is supported, it may not be

exact. Political conditions in Russia, such as trade restrictions or currency

controls, may limit consumers’ ability to purchase foreign goods.

Furthermore, the government may intervene to prevent the ruble from

reaching its true equilibrium value.

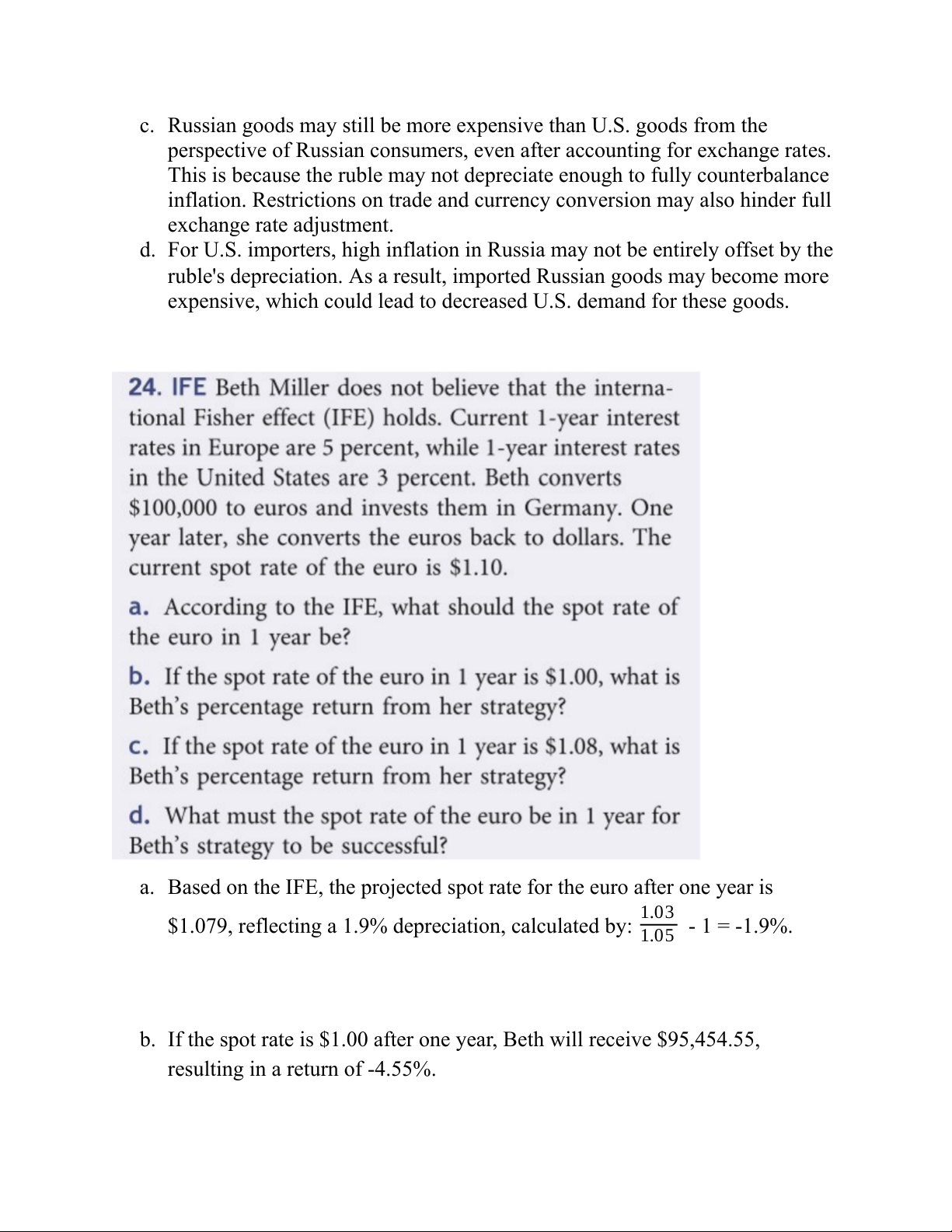

c. Russian goods may still be more expensive than U.S. goods from the

perspective of Russian consumers, even after accounting for exchange rates.

This is because the ruble may not depreciate enough to fully counterbalance

inflation. Restrictions on trade and currency conversion may also hinder full exchange rate adjustment.

d. For U.S. importers, high inflation in Russia may not be entirely offset by the

ruble's depreciation. As a result, imported Russian goods may become more

expensive, which could lead to decreased U.S. demand for these goods.

a. Based on the IFE, the projected spot rate for the euro after one year is 1.03

$1.079, reflecting a 1.9% depreciation, calculated by: - 1 = -1.9%. 1.05

b. If the spot rate is $1.00 after one year, Beth will receive $95,454.55,

resulting in a return of -4.55%.

c. With a spot rate of $1.08 after one year, Beth would have a 3.09% return on her investment.

d. For Beth’s strategy to succeed, the euro must trade above $1.079 after one year. 1.07

Using the PPP formula, the expected change in the exchange rate is - 1 = 1.03

3.8835%. Therefore, the future spot rate is projected to be $0.1038835 per peso.

Carolina would need $.1038835 × 20 million pesos = $2,077,710 to pay for 20 million pesos.

Tài liệu liên quan:

-

Tóm tắt lý thuyết môn Kinh tế chính trị Mác-Lênin | Trường Đại học Tôn Đức Thắng

71 36 -

Bài tập ôn giữa kì chương 1-4 | Kinh tế vĩ mô | Đại học Tôn Đức Thắng

204 102 -

Bài tập trắc nghiệm đúng sai chương 18: Nền kinh tế mở | Kinh tế vĩ mô | Đại học Tôn Đức Thắng

128 64 -

Trắc nghiệm ôn tập cuối kỳ môn Kinh Tế | Kinh tế vĩ mô | Đại học Tôn Đức Thắng

143 72 -

Giả sử trong trường hợp kinh doanh của chủ tư bản | Kinh tế chính trị Mác - Lênin | Đại học Tôn Đức Thắng

238 119