Tự Luận Vimo: Phân Tích Cung, Cầu và Thị Trường Cạnh Tranh| Microeconomics | Trường Đại học Quốc tế, Đại học Quốc gia Thành phố Hồ Chí Minh

Firms are “price taker” -> at every level of output thay have to sell with the same price -> Price remains unchanged.There is a substantial number of firms in the market-> Consumer also have a numerous number of choices-> quantity demanded is prone to change. Tài liệu được sưu tầm và soạn thảo dưới dạng file PDF để gửi tới các bạn cùng tham khảo, ôn tập đầy đủ kiến thức, chuẩn bị cho các buổi học thật tốt. Mời bạn đọc đón xem!

Môn: Microeconomics 613 tài liệu

Trường: Trường Đại học Quốc tế, Đại học Quốc gia Thành phố Hồ Chí Minh 1.9 K tài liệu

Tác giả:

Preview text:

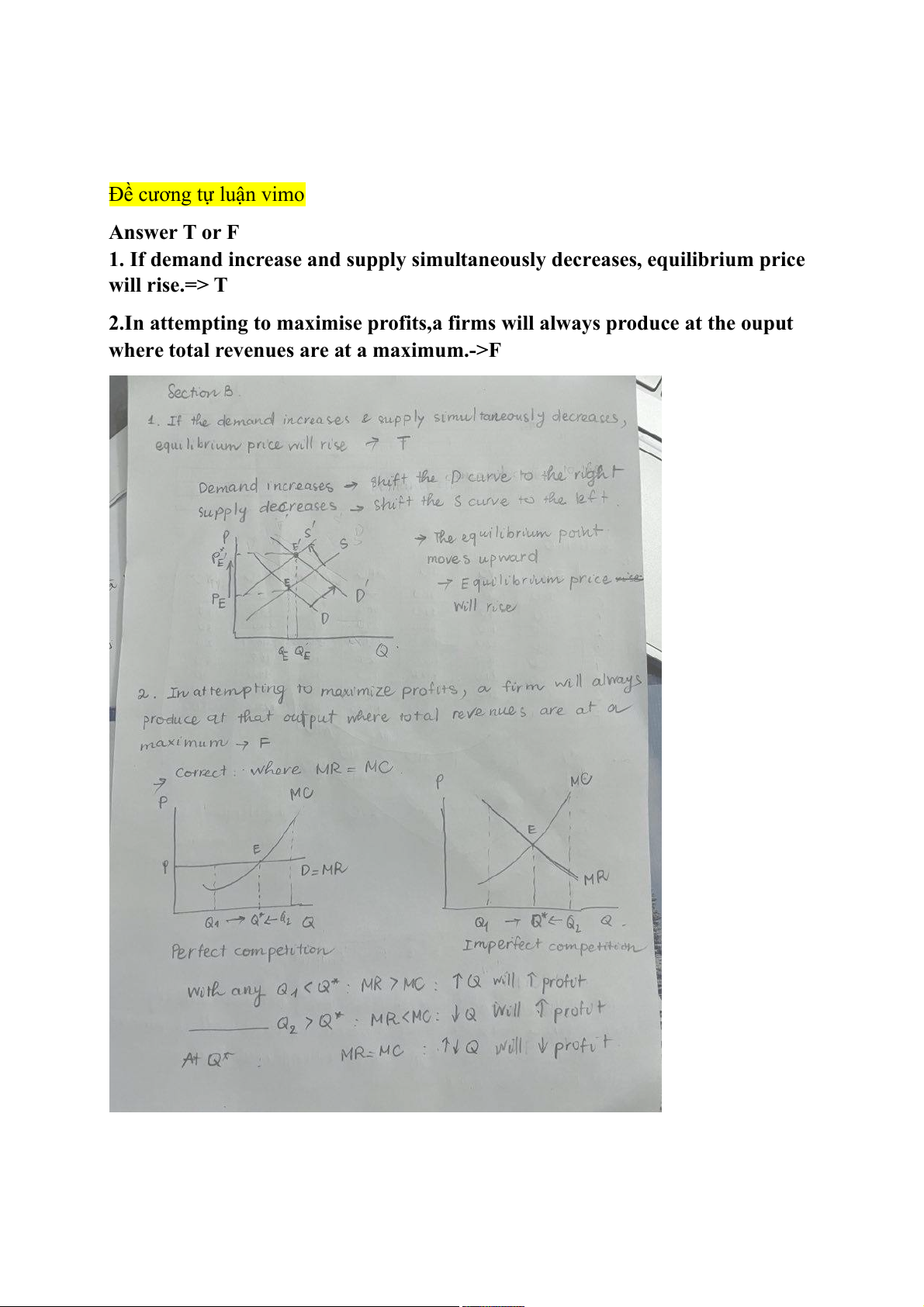

Đề cương tự luận vimo Answer T or F

1. If demand increase and supply simultaneously decreases, equilibrium price will rise.=> T

2.In attempting to maximise profits,a firms will always produce at the ouput

where total revenues are at a maximum.->F

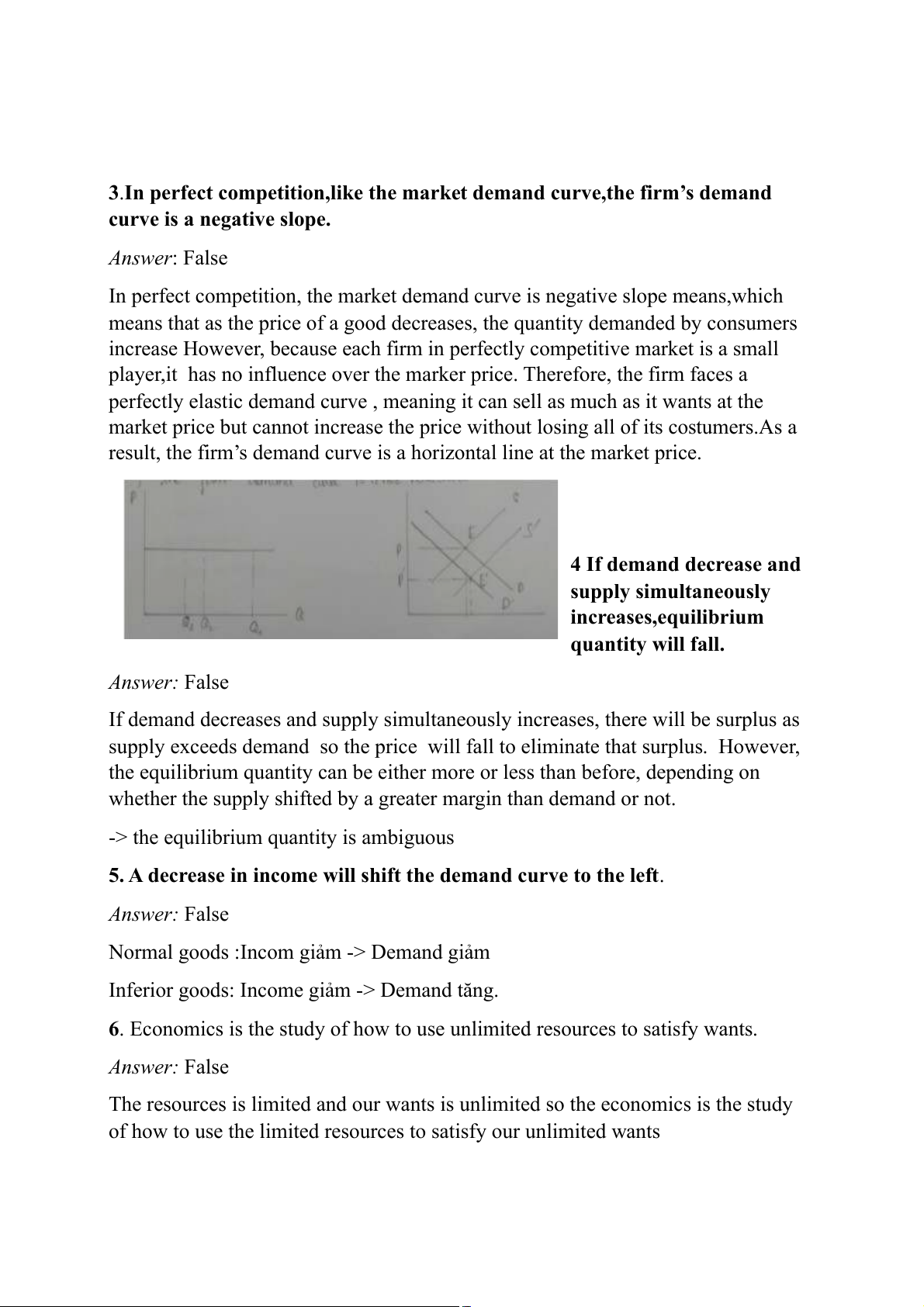

3.In perfect competition,like the market demand curve,the firm’s demand

curve is a negative slope. Answer: False

In perfect competition, the market demand curve is negative slope means,which

means that as the price of a good decreases, the quantity demanded by consumers

increase However, because each firm in perfectly competitive market is a small

player,it has no influence over the marker price. Therefore, the firm faces a

perfectly elastic demand curve , meaning it can sell as much as it wants at the

market price but cannot increase the price without losing all of its costumers.As a

result, the firm’s demand curve is a horizontal line at the market price. 4 If demand decrease and supply simultaneously increases,equilibrium quantity will fall. Answer: False

If demand decreases and supply simultaneously increases, there will be surplus as

supply exceeds demand so the price will fall to eliminate that surplus. However,

the equilibrium quantity can be either more or less than before, depending on

whether the supply shifted by a greater margin than demand or not.

-> the equilibrium quantity is ambiguous

5. A decrease in income will shift the demand curve to the left. Answer: False

Normal goods :Incom giảm -> Demand giảm

Inferior goods: Income giảm -> Demand tăng.

6. Economics is the study of how to use unlimited resources to satisfy wants. Answer: False

The resources is limited and our wants is unlimited so the economics is the study

of how to use the limited resources to satisfy our unlimited wants

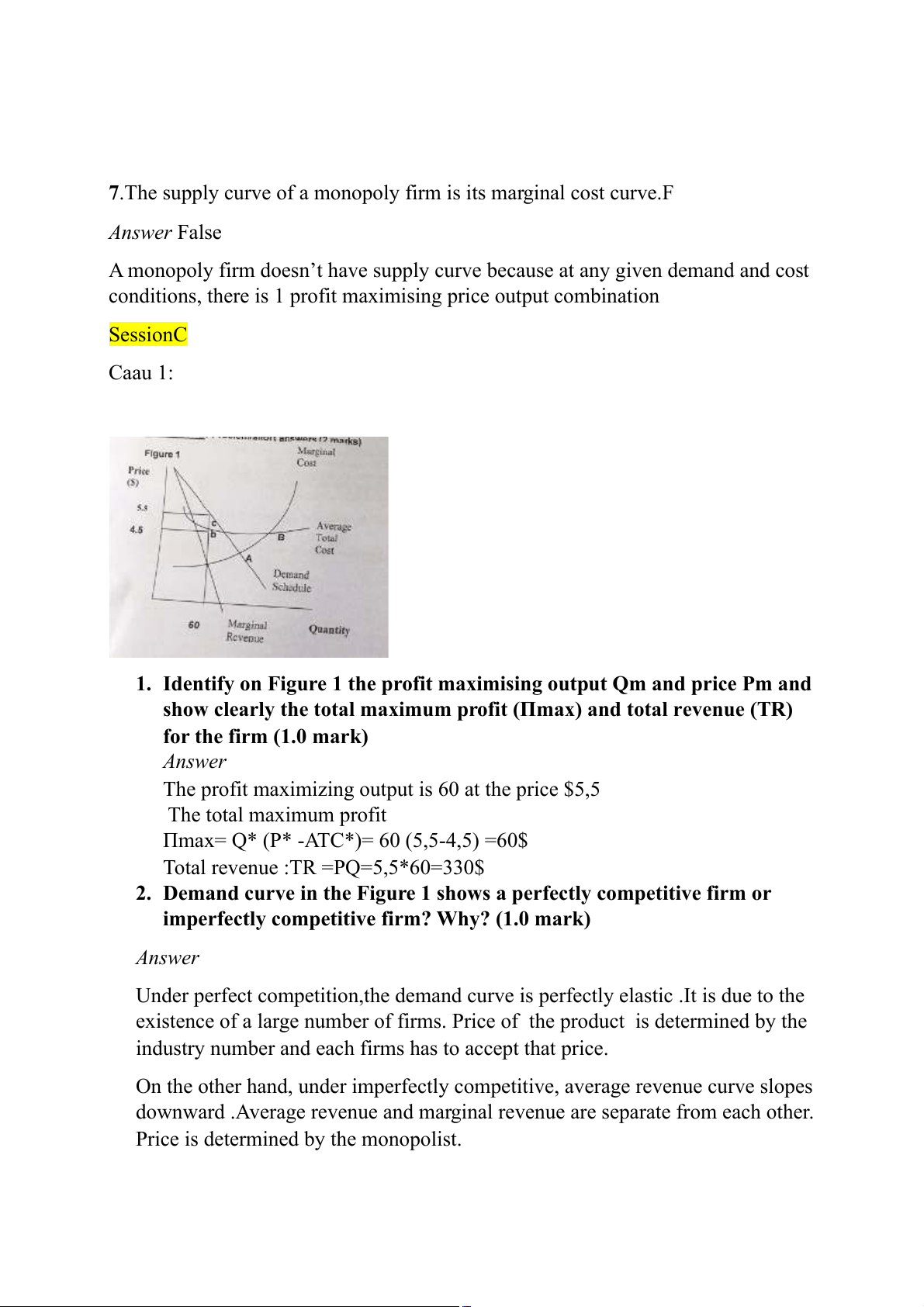

7.The supply curve of a monopoly firm is its marginal cost curve.F Answer False

A monopoly firm doesn’t have supply curve because at any given demand and cost

conditions, there is 1 profit maximising price output combination SessionC Caau 1:

1. Identify on Figure 1 the profit maximising output Qm and price Pm and

show clearly the total maximum profit (Пmax) and total revenue (TR) for the firm (1.0 mark) Answer

The profit maximizing output is 60 at the price $5,5 The total maximum profit

Пmax= Q* (P* -ATC*)= 60 (5,5-4,5) =60$

Total revenue :TR =PQ=5,5*60=330$

2. Demand curve in the Figure 1 shows a perfectly competitive firm or

imperfectly competitive firm? Why? (1.0 mark) Answer

Under perfect competition,the demand curve is perfectly elastic .It is due to the

existence of a large number of firms. Price of the product is determined by the

industry number and each firms has to accept that price.

On the other hand, under imperfectly competitive, average revenue curve slopes

downward .Average revenue and marginal revenue are separate from each other.

Price is determined by the monopolist.

3.Explain why the demand schedule in Figure 1 differs from that of a perfectly competive firm?

+)Firms are “price taker” -> at every level of output thay have to sell with the

same price -> Price remains unchanged.

There is a substantial number of firms in the market-> Consumer also have a

numerous number of choices-> quantity demanded is prone to change.

->Perfectly competitive D curve is perfectly elastic. +) Imperfect competitive

Firms have more market power-> they can now determine the price.

The number of firms is less than that of perfect competition market -> Consumers

also have less choices-> quantity demanded is less prone to change.

Imperfect competive D curve is more inelastic than the perfect competitive one. 3Caau 2:

A monopoly faces a demand function as follow: D: P ($) =50-Q

The firm's total cost function is given by: TC ($) =Q^2+6Q+40

1. Assuming that the firm wants to maximize its profit, determine the

quantity and price? Find the profit of the firm. Answer: Πmax MR=MC 2 +6Q+40)’ ((50-Q).Q)’=(Q 50-2Q=2Q+6 => Q* =11 (units) => P*=50-11=39 ($)

Πmax=TR-TC=39.11-(112+6.11+40) =202($)

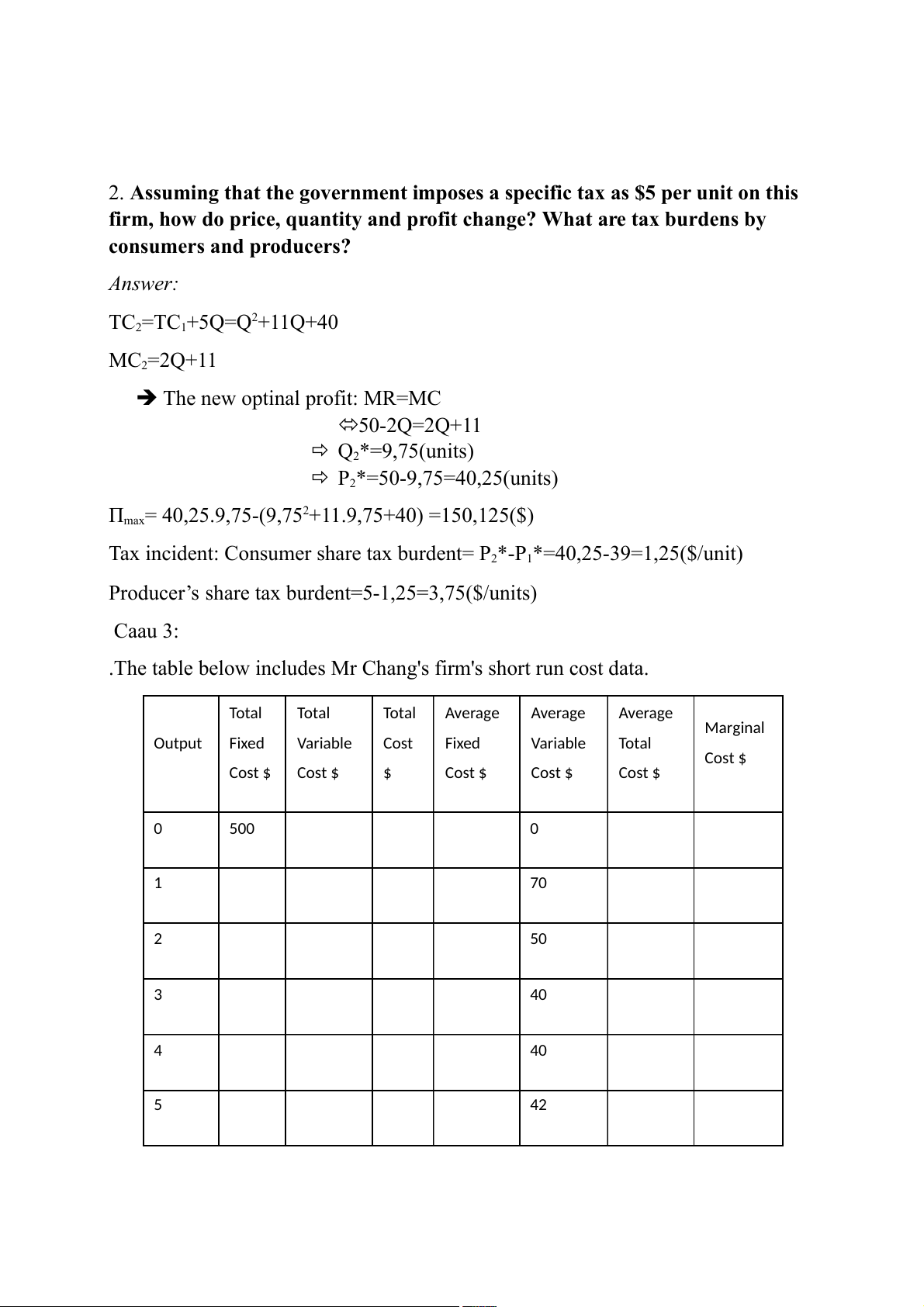

2. Assuming that the government imposes a specific tax as $5 per unit on this

firm, how do price, quantity and profit change? What are tax burdens by consumers and producers? Answer: TC 2 2=TC1+5Q=Q +11Q+40 MC2=2Q+11

The new optinal profit: MR=MC 50-2Q=2Q+11 Q2*=9,75(units) P2*=50-9,75=40,25(units) Π 2

max= 40,25.9,75-(9,75 +11.9,75+40) =150,125($)

Tax incident: Consumer share tax burdent= P2*-P1*=40,25-39=1,25($/unit)

Producer’s share tax burdent=5-1,25=3,75($/units) Caau 3:

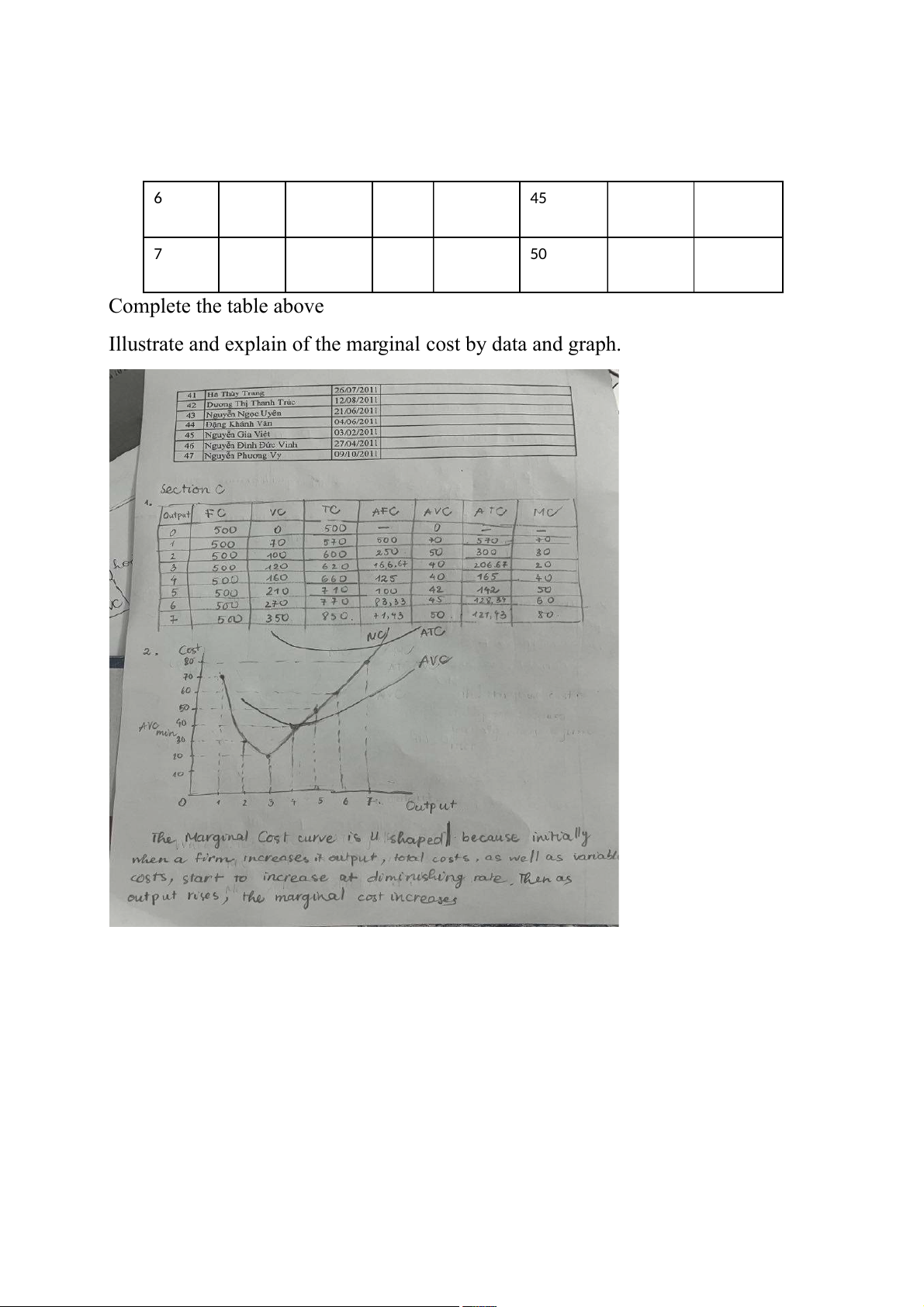

.The table below includes Mr Chang's firm's short run cost data. Total Total Total Average Average Average Marginal Output Fixed Variable Cost Fixed Variable Total Cost $ Cost $ Cost $ $ Cost $ Cost $ Cost $ 0 500 0 1 70 2 50 3 40 4 40 5 42 6 45 7 50 Complete the table above

Illustrate and explain of the marginal cost by data and graph.

Tài liệu liên quan:

-

Review Questions: Thinking Like an Economist | Microeconomics | Trường Đại học Quốc tế, Đại học Quốc gia Thành phố Hồ Chí Minh

4 2 -

Final Exam Quizlet Questions & Answers | Microeconomics | Trường Đại học Quốc tế, Đại học Quốc gia Thành phố Hồ Chí Minh

5 3 -

Đề thi giữa kỳ II | Microeconomics | Trường Đại học Quốc tế, Đại học Quốc gia Thành phố Hồ Chí Minh

4 2 -

Final Group Project_ The Beer Industry | Microeconomics | Trường Đại học Quốc tế, Đại học Quốc gia Thành phố Hồ Chí Minh

3 2