Completing the accounting cycle - Nguyên Lý Kế Toán | Trường Đại học Tôn Đức Thắng

Prepare an accounting worksheet•Use the worksheet to prepare financial statements•Close the revenue, expense and drawings accounts•Prepare the post-closing trial balance. Tài liệu được sưu tầm và soạn thảo dưới dạng file PDF để gửi tới các bạn sinh viên cùng tham khảo, ôn tập đầy đủ kiến thức, chuẩn bị cho các buổi học thật tốt. Mời bạn đọc đón xem!

Môn: Nguyên Lý Kế Toán (NLKTTDT) 91 tài liệu

Trường: Trường Đại học Tôn Đức Thắng 4.5 K tài liệu

Tác giả:

Preview text:

Chapter 4

Completing the accounting cycle

201044 - Completing the accounting cycle Learning objectives

• Prepare an accounting worksheet

• Use the worksheet to prepare financial statements

• Close the revenue, expense and drawings accounts

• Prepare the post-closing trial balance

• Classify assets and liabilities as current or non-current

• Describe the effect of various transactions on the current ratio and the debt ratio

201044 - Completing the accounting cycle 4/6/2022 2 4.1. The accounting worksheet

• Accountants often use a worksheet to summarise data for the financial statements

• It is a summary device that helps identify the accounts that need adjustment

• The worksheet is an internal document

201044 - Completing the accounting cycle 4/6/2022 3 4.1. The accounting worksheet

• Step 1: Enter the account titles and their unadjusted balances in the

Trial balance columns of the worksheet and total the amounts

• Step 2: Enter the adjusting entries in the adjustments columns and total the amounts

• Step 3: Calculate each account’s adjusted balance by combining

the trial balance and adjustment figures. Enter each account’s

adjusted amount in the adjusted trial balance columns

201044 - Completing the accounting cycle 4/6/2022 4 4.1. The accounting worksheet

• Step 4: Draw an imaginary line above the first revenue account.

Every account above that line (assets, liabilities and equity

accounts) is copied from the adjusted trial balance to the balance sheet columns.

Every account below the line (revenues and expenses) is copied

from the adjusted trial balance to the income statement columns.

• Step 5: On the income statement, calculate profit or loss as total

revenues minus total expenses.

Enter profit (loss) as the balancing amount on the income statement.

Also enter profit (loss) as the balancing amount on the balance

sheet. Then total the financial statement columns.

201044 - Completing the accounting cycle 4/6/2022 5 4.1. The accounting worksheet • Worksheet SMART TOUCH LEARNING WORKSHEET

For the month ended 30 June 201N Accounts Trial Adjustments Adj-Trial Income Balance Balance Balance Statement sheet Debit Credit Debit Credit Debit Credit Debit Credit Debit Credit Cash Supplies Furniture …….

201044 - Completing the accounting cycle 4/6/2022 6 4.1. The accounting worksheet • Worksheet SMART TOUCH LEARNING WORKSHEET

For the month ended 30 June 201N Accounts Trial Adjustments Adj-Trial Income Balance Balance Balance Statement sheet Debit Credit Debit Credit Debit Credit Debit Credit Debit Credit Cash Supplies Furniture …….

201044 - Completing the accounting cycle 4/6/2022 7 4.1. The accounting worksheet

Ex: Continuing with the example of Smart Touch Learning. 4/6/2022 8

4.2. Completing the accounting cycle -

Preparing the financial statements from a worksheet -

Recording the adjusting entries from a worksheet

201044 - Completing the accounting cycle 4/6/2022 9 4.3. Closing the accounts

• Closing the accounts occurs at the end of the period

• It consists of journalising and posting the closing entries in order to

get the accounts ready for the next period

• It zeroes out all the revenues and all the expenses in order to

measure each period’s profit separately from all other periods and

updates the Capital account balance

201044 - Completing the accounting cycle 4/6/2022 10 4.3. Closing the accounts Temporary accounts Permanent accounts

Closed at the end of the period Not closed at the end of the period Examples include Revenues, Examples include Assets, Expenses, Drawings Liabilities, Capital Start next period with a zero

Ending balance carries forward to balance next period

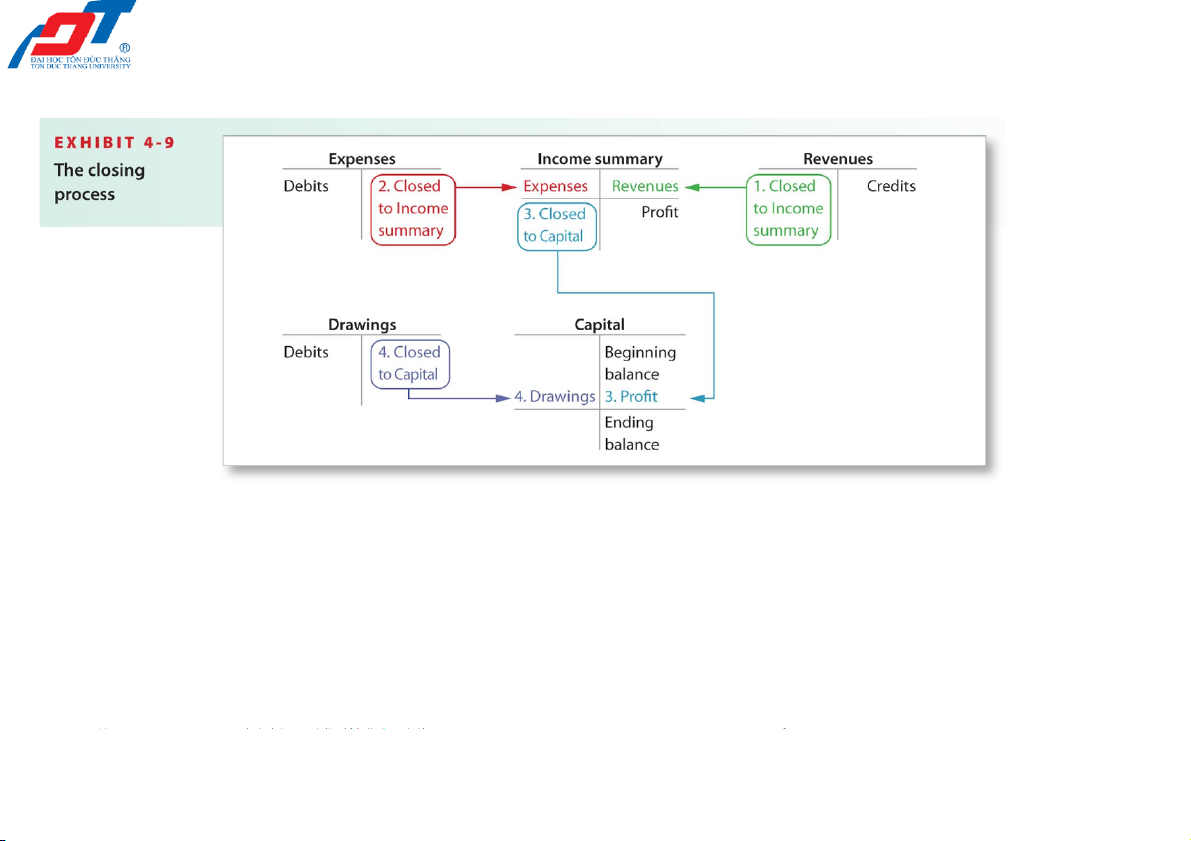

201044 - Completing the accounting cycle 4/6/2022 11 4.3. Closing the accounts

• Step 1: Make the revenue accounts equal zero via the Income summary account

• Step 2: Make expense accounts equal zero via the Income summary account

• Step 3: Make the Income summary account equal zero via the Capital account

• Step 4: Make the Drawings account equal zero via the Capital account

201044 - Completing the accounting cycle 4/6/2022 12 4.3. Closing the accounts

201044 - Completing the accounting cycle 4/6/2022 13 4.3. Closing the accounts

Ex: Prepare the closing entries and post to the T-

accounts for Smart Touch Learning. 4/6/2022 14

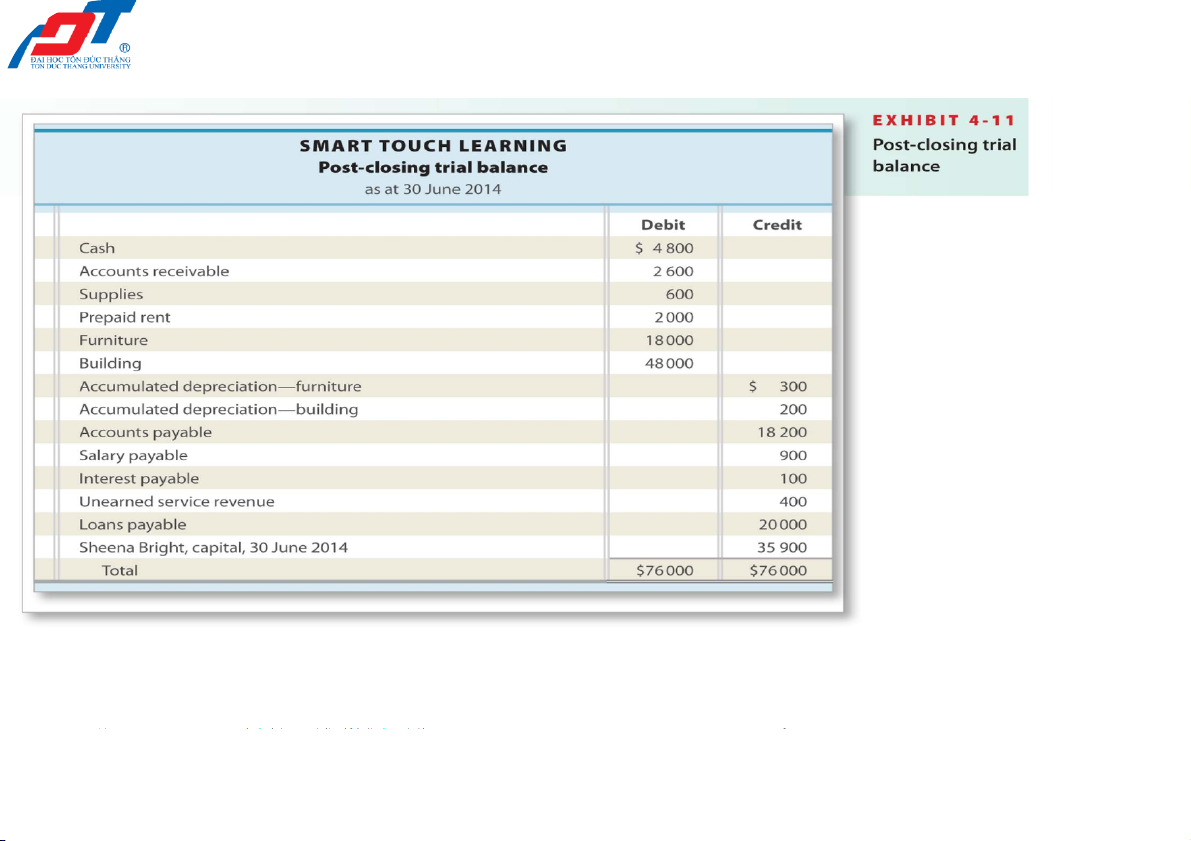

4.4. Post-closing trial balance

• The accounting cycle can end with a post-closing trial balance

• This optional step lists the accounts and their adjusted balances after closing

• Only assets, liabilities and capital accounts appear on the post- closing trial balance

• No temporary accounts are included (revenues, expenses, drawings)

201044 - Completing the accounting cycle 4/6/2022 15

4.4. Post-closing trial balance

201044 - Completing the accounting cycle 4/6/2022 16

4.5. Classifying assets and liabilities

• Assets and liabilities are usually classified in balance sheets as either current or noncurrent

• Under each heading it is also usual to list assets and liabilities in order of decreasing liquidity

• Liquidity is a measure of how quickly an item can be converted to cash

• An alternative balance sheet format is to list assets and liabilities in

order of decreasing liquidity without the division into current and non-current assets.

(AASB 101, Presentation of Financial Statements)

201044 - Completing the accounting cycle 4/6/2022 17

4.5. Classifying assets and liabilities Assets

• Current assets are assets that are expected to be converted to

cash, sold or consumed during the next 12 months, or within the

business operating cycle if longer than a year

• The operating cycle is the time span during which (1) cash is used

to acquire goods and services, and (2) these goods and services

are sold to customers, from whom (3) the business collects cash

• Non-current assets are all assets other than current assets

201044 - Completing the accounting cycle 4/6/2022 18

4.5. Classifying assets and liabilities Liabilities

• Current liabilities are debts that are due to be paid with cash or with

goods and services within one year, or within the business operating cycle if longer than a year

• All liabilities that aren’t current are classified as non-current liabilities

201044 - Completing the accounting cycle 4/6/2022 19

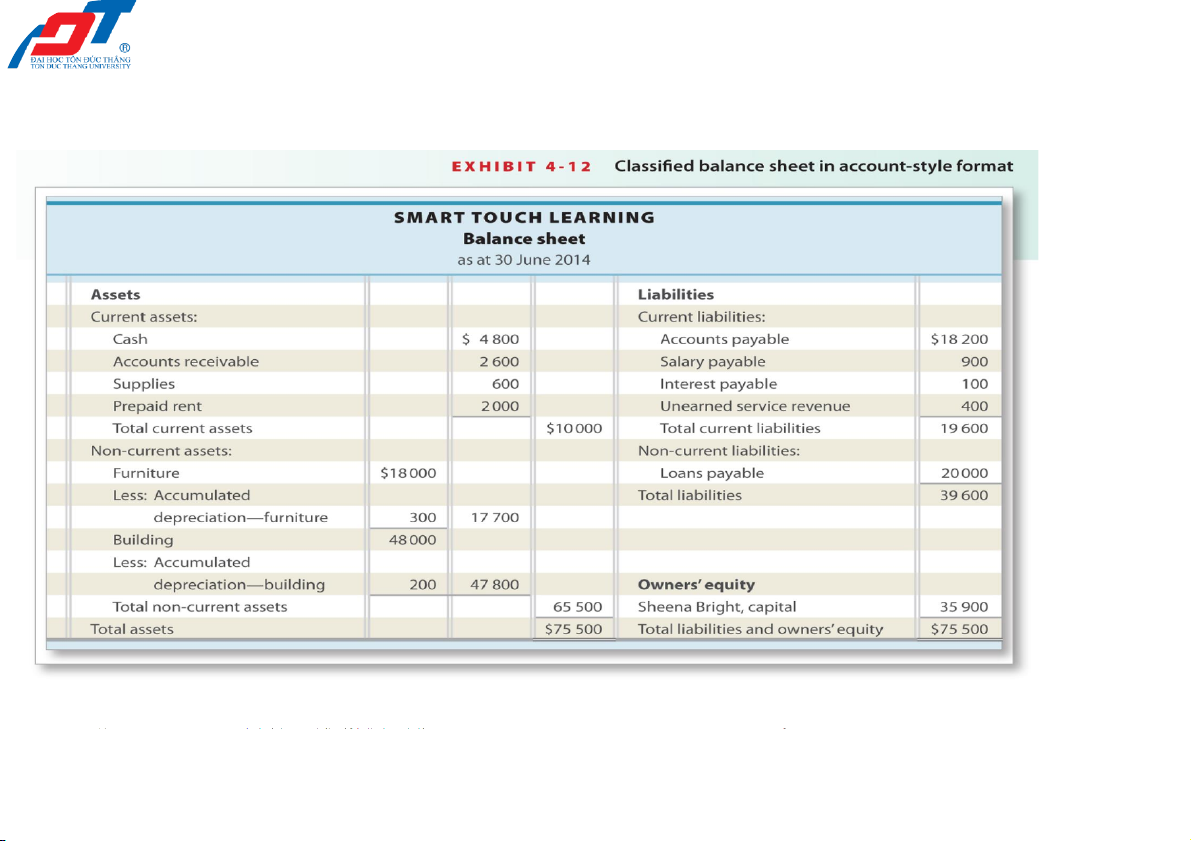

4.5. Classifying assets and liabilities The classified balance sheet

201044 - Completing the accounting cycle 4/6/2022 20

Tài liệu liên quan:

-

Bài giảng Chapter 6: Audit cash and cash equivalents môn Nguyên lý kế toán | Trường Đại học Tôn Đức Thắng

35 18 -

Bài giảng Chapter 5: Audit completion and audit report môn Nguyên lý kế toán | Trường Đại học Tôn Đức Thắng

33 17 -

Tài liệu Nguyên Lý Kế Toán

36 18 -

Tài liệu NLKT - Trường Đại học Tôn Đức Thắng

32 16 -

Trắc nghiệm ôn tập - Nguyên Lý Kế Toán | Trường Đại học Tôn Đức Thắng

610 305