Final Exam Môn Derivatives and Risk Management | Trường Đại học Quốc tế, Đại học Quốc gia Thành phố Hồ Chí Minh

Final Exam Môn Derivatives and Risk Management. Tài liệu được sưu tầm gồm 4 trang, giúp bạn ôn tập tốt hơn. Mời các bạn đón xem.

Môn: Derivatives and Risk Management 7 tài liệu

Trường: Trường Đại học Quốc tế, Đại học Quốc gia Thành phố Hồ Chí Minh 2 K tài liệu

Tác giả:

Preview text:

lOMoAR cPSD| 23136115 [‘SOLUTION

Question 1: An investor buys 4 ABC June 60 put for $0.5, sells 4 ABC June 65 put for $2, sells 4 ABC

June 70 put for $5, and at the same time buys 4 ABC June 75 put for $9. Suppose that the investor

holds options until the expiration.

a. Calculate the profit/loss of the strategy if the stock price at expiration is $78 per share?

b. Calculate the profit/loss of the strategy if the stock price at expiration is $ 67 per share?

c. Calculate the profit/loss of the strategy if the stock price at expiration is $ 55 per share?

d. Determine the breakeven price, maximum loss, and maximum profit at expiration. Show all yourcalculations?

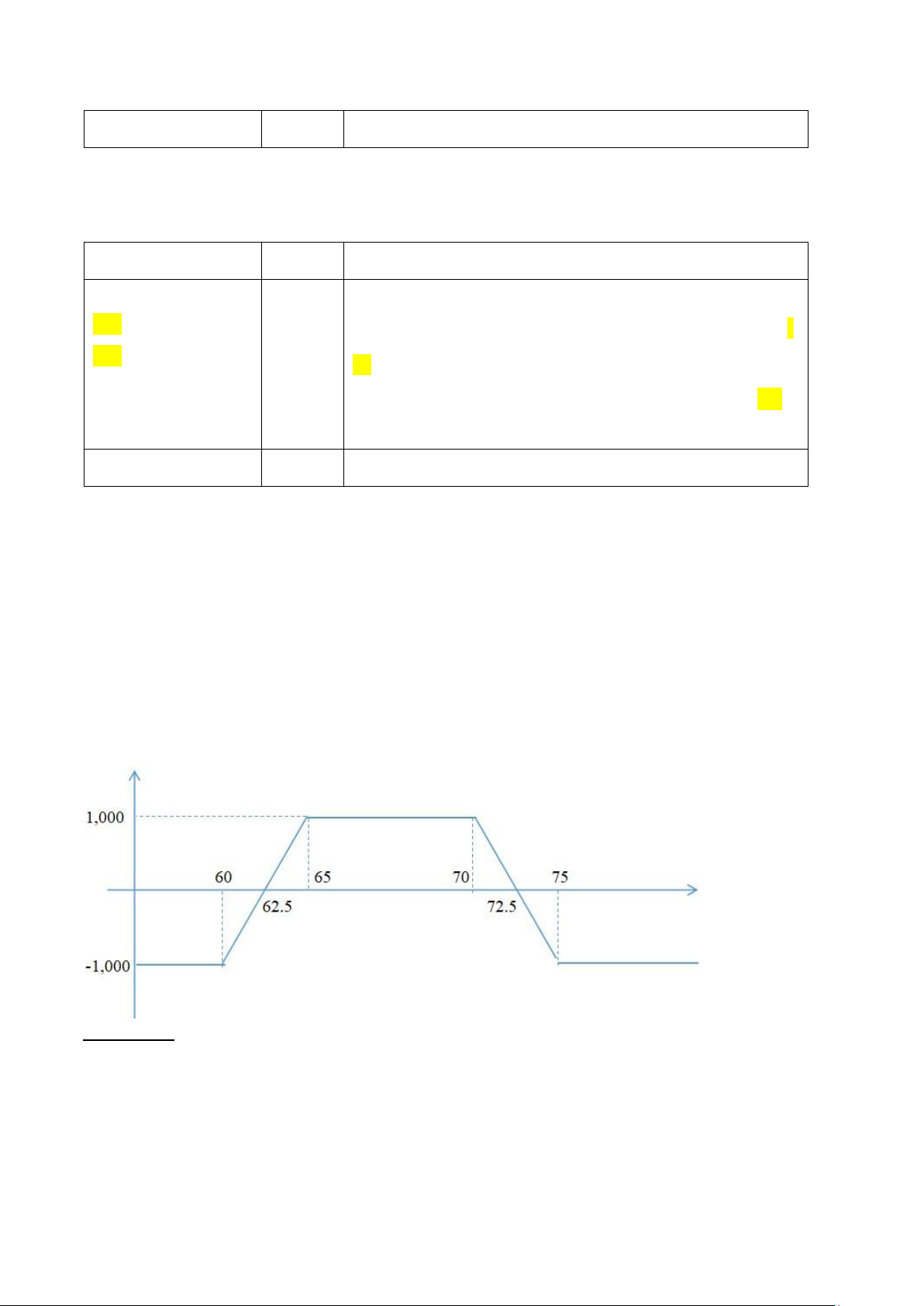

e. Draw the payoff graph for the above strategy at expiration? Buy 60 put $0.5 Sell 65 put $2.0 Sell 70 put $5.0 Buy 75 put $9.0

(X1 < X2 < X3 < X4) (P1 < P2 < P3 < P4) => Long put condor a) ST = 78 t = 0 t = T Buy 4 60 put $0.5 -0.5

ST > X (78 > 60) => No exercise => Profit = 0 Sell 4 65 put $2.0 2.0

ST > X (78 > 65) => No exercise => Profit = 0 Sell 4 70 put $5.0 5.0 S Buy 4 75 put $9.0 -9.0

T > X (78 > 70) => No exercise => Profit = 0

ST > X (78 > 75) => No exercise => Profit = 0 -2.5 0

=> Total profit = -2.5 * 4 * 100 = -$1,000 b) ST = 67 t = 0 t = T Buy 4 60 put $0.5 -0.5

ST > X (67 > 60) => No exercise => Profit = 0 Sell 4 65 put $2.0 2.0

ST > X (67 > 65) => No exercise => Profit = 0 Sell 4 70 put $5.0 5.0

ST < X (67 < 70) => Exercise => Profit = - (70 - 67) = -3 Buy 4 75 put $9.0 -9.0

ST < X (67 < 75) => Exercise => Profit = 75 - 67 = 8 lOMoAR cPSD| 23136115 -2.5 5

=> Sum = -2.5 + 5 = 2.5 => Total profit = 2.5 * 4 * 100 = $1,000 c) ST = 55 t = 0 t = T Buy 4 60 put $0.5 -0.5

ST < X (55 < 60) => Exercise => Profit = 60 - 55 = 5 Sell 4 65 put $2.0 2.0

ST < X (55 < ok 65) => Exercise => Profit = -(65 - 55) = - Sell 4 70 put $5.0 5.0 10 Buy 4 75 put $9.0 -9.0

ST < X (55 < 70) => Exercise => Profit = - (70 - 55) = -15

ST < X (55 < 75) => Exercise => Profit = 75 - 55 = 20 -2.5 0

=> Total profit = -2.5 * 4 * 100 = -$1,000 d)

Maximum profit = 5 - 2.5 = 2.5 => Total = 2.5 * 4 * 100 = $1,000

Maximum loss = 2.5 => Total = 2.5 * 4 * 100 = $1,000

Downside BEP = 60 + 2.5 = 62.5 Upside BEP = 75 - 2.5 = 72.5 e)

Question 2: An investor buys 3 XYZ August 50 put for $0.5, sells 3 XYZ August 55 put for $2.75.

Suppose that the investor holds the option until the expiration.

a. Calculate the profit/loss of the strategy if the stock price at expiration is $58 per share?

b. Calculate the profit/loss of the strategy if the stock price at expiration is $ 53 per share?

c. Calculate the profit/loss of the strategy if the stock price at expiration is $ 48 per share? lOMoAR cPSD| 23136115

d. Determine the breakeven price, maximum loss, and maximum profit at expiration. Show all yourcalculations?

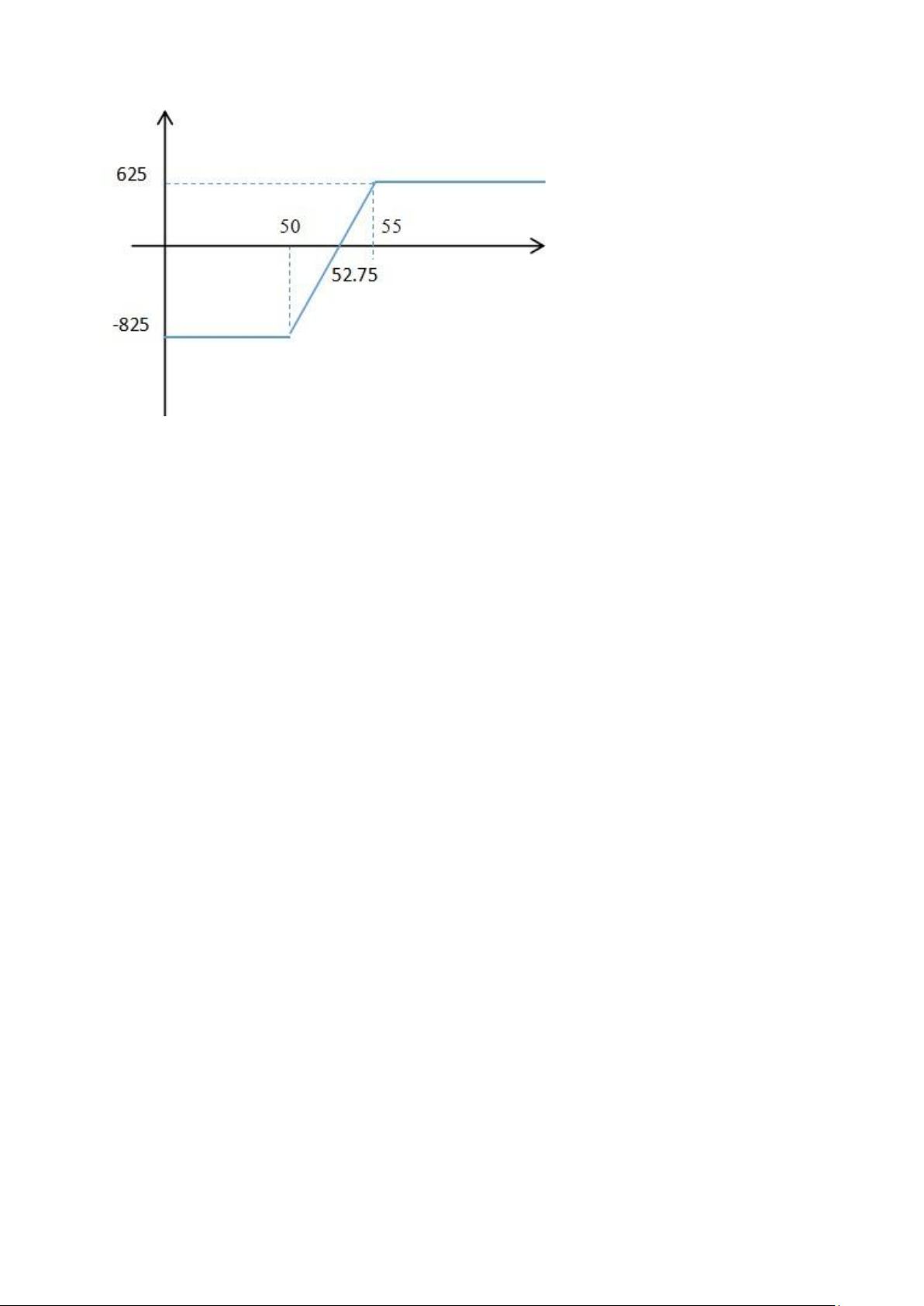

e. Draw the payoff graph for the above strategy at expiration? Buy 50 put $0.5 Sell 55 put $2.75

(X1 < X2) (P1 < P2) => Bull put spread a) ST = 58 t = 0 t = T Buy 3 50 put $0.5 -0.5

ST > X (58 > 50) => No exercise => Profit = 0 Sell 3 55 put $2.75 2.75

ST > X (58 > 55) => No exercise => Profit = 0 2.25 0

=> Total profit = 2.25 * 3 * 100 = $625 b) ST = 53 t = 0 t = T Buy 3 50 put $0.5 -0.5

ST > X (53 > 50) => No exercise => Profit = 0 Sell 3 55 put $2.75 2.75

ST < X (53 < 55) => Exercise => Profit = - (55 - 53) = - 2 2.25 -2

=> Sum = 2.25 - 2 = 0.25 => Total profit = 0.25 * 3 * 100 = $75 c) ST = 48 t = 0 t = T Buy 3 50 put $0.5 -0.5

ST < X (48 < 50) => Exercise => Profit = 50 - 48 = 2 Sell 3 55 put $2.75 2.75

ST < X (48 < 55) => Exercise => Profit = - (55 - 48) = -7 2.25 -5

=> Sum = 2.25 - 5 = -2.75 => Total profit = -2.75 * 3 * 100 = -$825 d)

Maximum profit = 2.75 - 0.5 = 2.25 => Total = 2.25 * 3 * 100 = $625

Maximum loss = (55 - 50) - (2.75 - 0.5) = 2.75 => Total = 2.75 * 3 * 100 = $825 BEP

= X2 - (P2 - P1) = 55 - 2.25 = 52.75 e) lOMoAR cPSD| 23136115

Tài liệu liên quan:

-

AAPL Industry Overview: Tech Advancements & Consumer Behavior Insights | Môn Derivatives and Risk Management - Trường Đại học Quốc tế, Đại học Quốc gia Thành phố Hồ Chí Minh

101 51 -

Investment Portfolio Analysis: Amazon (AMZN) & Apple (AAPL) Insights | Môn Derivatives and Risk Management - Trường Đại học Quốc tế, Đại học Quốc gia Thành phố Hồ Chí Minh

124 62 -

Homework Review: Key Concepts in Volatility and Risk Management | Môn Derivatives and Risk Management - Trường Đại học Quốc tế, Đại học Quốc gia Thành phố Hồ Chí Minh

130 65 -

Tài liệu ôn tập chap 5 | Môn Derivatives and Risk Management - Trường Đại học Quốc tế, Đại học Quốc gia Thành phố Hồ Chí Minh

123 62