Ôn chuẩn Chuẩn mực báo cáo tài chính quốc tế | Trường Đại học Công nghiệp TP.HCM

Ôn chuẩn Chuẩn mực báo cáo tài chính quốc tế môn Chuẩn mực báo cáo tài chính quốc tế của Trường Đại học Công nghiệp Thành phố Hồ Chí Minh. Hi vọng tài liệu này sẽ giúp các bạn học tốt, ôn tập hiệu quả, đạt kết quả cao trong các bài thi, bài kiểm tra sắp tới. Mời các bạn cùng tham khảo chi tiết bài viết dưới đây nhé.

Môn: Chuẩn mực báo cáo tài chính quốc tế (CMBC) 10 tài liệu

Trường: Trường Đại học Công nghiệp Thành phố Hồ Chí Minh 776 tài liệu

Tác giả:

Preview text:

lOMoARcPSD|44862240

III. CHANGES IN ACCOUNTING ESTIMATES

Ngày 1/1/20XX, cty mua 1 cái máy: + Trị giá $ 10,000

+ Thời gian sử dụng: 10 năm

+ Salvage value = Giá trị có thể thu hồi được = $ 1,000 Vào ngày 1/1/20XX + 5 (5 năm sau):

+ Last another 10 years = Kéo dài thêm 10 năm nữa

+ Salvage value = Giá trị có thể thu hồi được = $ 800

Câu hỏi: Định khoản nghiệp vụ ở từng năm

Solution

Year 1

Cost (Nguyên giá) – Residual value/ Salvage value (Giá trị có thể thu hồi Depreciation= (Khấu hao) Useful life (Thời gian sử dụng)

10,000 – 1,000

= = $ 900/year

10

Nợ 6….: $ 900 Dr Depreciation expense : $ 900

Có 214: $ 900 Cr Accumulated Depreciation : $ 900

Year 2 Year 5: Similar to Year 1:

+ Depreciation = $ 900/year

Nợ 6….: $ 900 Dr Depreciation expense : $ 900

Có 214: $ 900 Cr Accumulated Depreciation : $ 900

Year 6:

Accumulated Depreciation = Tổng Khấu hao = 900 x 5 = $ 4,500

Carrying amount of asset = Giá trị còn lại của TS = 10,000 – 4,500 = $ 5,500

Cost (Nguyên giá) – Residual value/ Salvage value (Giá trị có thể thu hồi)

Depreciation= (Khấu hao) Useful life (Thời gian sử dụng)

5,500 - 800

= = $ 470/year

10

Nợ 6….: $ 470 Dr Depreciation expense : $ 470

Có 214: $ 470 Cr Accumulated Depreciation : $ 470

Year 7 nine years later: Similar to Year 6

+ Depreciation = $ 470/year

Nợ 6….: $ 470 Dr Depreciation expense : $ 470

Có 214: $ 470 Cr Accumulated Depreciation : $ 470

Homework: Bài tập về nhà

ABC company purchase a machine with a price of $ 280,000 and the useful life is 20 years, and the salvage value is $ 4,000. After using 8 years, ABC company decided that this machine last another 30 years and the salvage value = $ 2,000 Require:

- Calculate depreciation for each year.

- Journalize transactions of depreciation for each year.

Solution:

- Year 1

Cost – Residual value/ Salvage value

Depreciation=

Useful life

280,000 – 4,000

= = $ 13,800/year

20

Dr Depreciation expense : $ 13,800

Cr Accumulated Depreciation : $ 13,800 Year 2 Year 8: Every year is similar to Year 1:

+ Depreciation = $ 13,800/year

Dr Depreciation expense : $ 13,800

Cr Accumulated Depreciation : $ 13,800

- Year 9:

Carrying amount = Cost – Total Depreciation = 280,000 – (13,800 x 8) = $ 169,600

Cost – Residual value/ Salvage value

Depreciation= Useful life

169,600 – 2,000

= = $ 5,587/year

30

Dr Depreciation expense : $ 5,587

Cr Accumulated Depreciation : $ 5,587

* All the Years after Year 9: |

Every year is similar to Year 9

+ Depreciation = $ 5,587/year

Dr Depreciation expense : $ 5,587

Cr Accumulated Depreciation : $ 5,587 Exercise 2:

On 1st January 2019, Company B acquired a specilised computer system from an international supplier with an amount of 3 million dollar. Company B decided to depreciate computer systems over its estimated useful life of 8 years, spanning from 2019 to 2026. At the time of purchase, it was anticipated that the computer system would have zero residual value. Nevertheless, on 1 January 2021, Company B conducted a thorough assessment of the computer systems’ s useful life and concluded that it could only be effectively utilized for the next two years .

Require:

- Calculate depreciation for each year.

- Journalize transactions of depreciation for each year.

Solution:

- Year 1

Cost – Residual value/ Salvage value

Depreciation=

Useful life

3,000,000 - 0

8

Dr Depreciation expense : $ 375,000

Cr Accumulated Depreciation : $ 375,000 Year 2 is similar to Year 1:

+ Depreciation = $ 375,000

Dr Depreciation expense : $ 375,000

Cr Accumulated Depreciation : $ 375,000

- Year 3:

Carrying amount = Cost – Total Depreciation = 3,000,000 – (375,000 x 2) = $ 2,250,000

Cost – Residual value/ Salvage value

Depreciation= Useful life

2,250,000 - 0

= = $ 1,125,000/year

2

Dr Depreciation expense : $ 1,125,000

Cr Accumulated Depreciation : $ 1,125,000

Year 4 is similar to Year 3

+ Depreciation = $ 1,125,000

Dr Depreciation expense : $ 1,125,000

Cr Accumulated Depreciation : $ 1,125,000

Exercise 3:

In a manufacturing company, there is a machine on 1st January 2019 with information as follows: + Purchase price: $ 150,000

+ Useful life: 8 years

+ Company uses straight-line method

+ Salvage value: 0

However, after 3 years, the manager changes its estimate of the machine, determining that it can be used effectively for a total of 5 years.

Require:

- Calculate depreciation for each year.

- Journalize transactions of depreciation for each yearSolution:

- Year 1

Cost – Residual value/ Salvage value

Depreciation=

Useful life

150,000 - 0

= = $ 18,750/year

8

Dr Depreciation expense : $ 18,750 Cr Accumulated Depreciation : $ 18,750 Year 2 -> Year 3: Every year is similar to Year 1:

+ Depreciation = $ 18,750 /year

Dr Depreciation expense : $ 18,750 Cr Accumulated Depreciation : $ 18,750

- Year 4:

+ Carrying amount = Cost – Total Depreciation = 150,000 – (18,750 x 3) = $ 93,750

+ Useful life = 5 -3 = 2 years

Cost – Residual value/ Salvage value

Depreciation= Useful life

93,750 - 0

= = $ 46,875/year

2

Dr Depreciation expense : $ 46,875

Cr Accumulated Depreciation : $ 46,875

Year 5 -> Year 8: Every year is similar to Year 4 + Depreciation = $ 46,875 / year Dr Depreciation expense : $ 46,875

Cr Accumulated Depreciation : $ 46,875

Giải :

Ngày 1/7/2014, cty Ella mua 25% cổ phần của cty Emily với giá $ 42,500. Những thông tin về Equity (=VCSH = TK 4) của cty Emily là như sau:

+ Share capital = TK 411 | = $ 100,000 |

+ General reserve = Quỹ = TK 414 (Quỹ ĐTPT) + Asset revaluation surplus = Chênh lệch đánh giá lại TS = TK 412 = $ 20,000 | = $ 30,000 |

+ Retained earnings = Lợi nhuận = TK 421 | = $ 20,000 |

Cty Emily:

+ Ghi nhận Profit = Ghi nhận Lợi nhuận = $ 25,000

+ Asset revaluation surplus increase = TK 412 tăng = $ 5,000

+ Trả cổ tức = $ 4,000

+ Transfer to general reserve = Chuyển từ lợi nhuận sang quỹ = $ 3,000

Yêu cầu: Journalize the transactions, using the accounts as follows: Định khỏan nghiệp vụ kinh tế phát sinh bằng cách dùng các Tài khoản sau:

+ Investment in Associate and Joint Venture (TK 222)

+ Cash (TK 111, 112)

+ Share of profit or loss of Associate and Joint Venture (TK 515.1/635.1)

+ Share of other comprehensive income of Associate and Joint Venture (TK 515.2/635.2) + Asset revaluation surplus (TK 412)

Solution:

Step 1: Ella company invest Emily company (Cty Ella đầu tư vào cty Emily)

Nợ TK 222: $ 42,500 Dr Investment in Associate and Joint Venture: $ 42,500

Có TK 111, 112: $ 42,500 Cr Cash: $ 42,500

Step 2: Recognize Profit (Ghi nhận Lợi nhuận)

Nợ 222: 25,000 x 25% = $ 6,250

Có 515.1: 25,000 x 25% = $ 6,250

Dr Investment in Associate and Joint Venture: 25,000 x 25% = $ 6,250

Cr Share of profit or loss of Associate and Joint Venture: 25,000 x 25% = $ 6,250

Step 3: Recognize Asset revaluation surplus (Ghi nhận TK 412) a.

Nợ 222: 5,000 x 25% = $ 1,250

Có TK 412: 5,000 x 25% = $ 1,250

Dr Investment in Associate and Joint venture: 5,000 x 25% = $ 1,250 Cr Asset revaluation surplus: 5,000 x 25% = $ 1,250 b.

Nợ 412: $ 1,250

Có 515.2: $ 1,250

Dr Asset Revaluation surplus: $ 1,250

Cr Share of other comprehensive income of Associate and Joint Venture Step 4: Recognize dividend (Ghi nhận cổ tức)

Nợ TK 635.2: 4,000 x 25% = $ 1,000

Có TK 222: 4,000 x 25% = $ 1,000

Dr Share of other comprehensive income of Associate and Joint Venture: 4,000 x 25% = $ 1,000 Cr Investment in Associate and Joint Venture: 4,000 x 25% = $ 1,000

Solution:

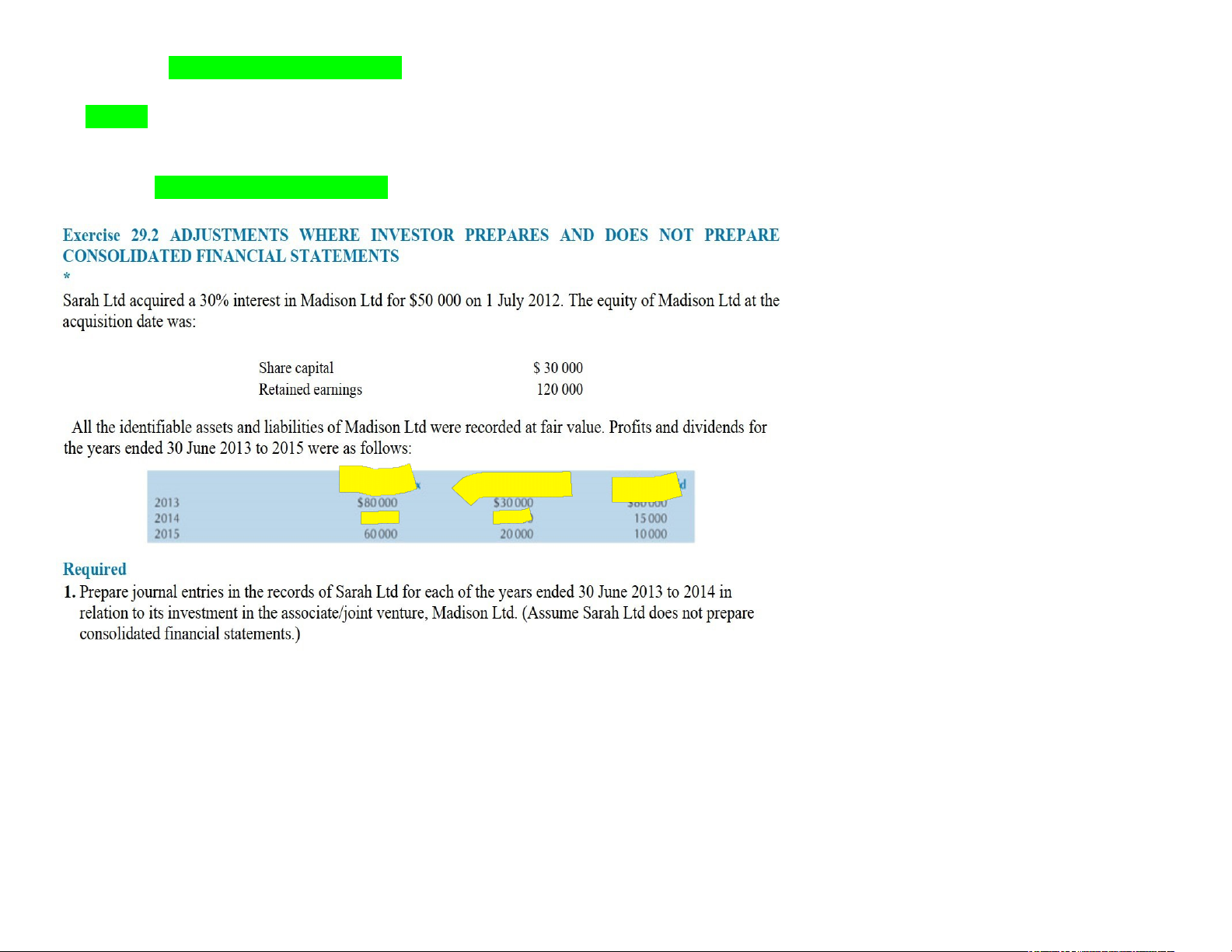

Step 1: Sarah company invest in Madison company

Dr Investment in Associate and Joint Venture: $50,000

Cr Cash: $ 50,000 Year 2013:

Step 2: Recognize Profit

Dr Investment in Associate and Joint Venture: (80,000 – 30,000) x 30% = 15,000

Cr Share of profit or loss of Associate and Joint Venture: (80,000 – 30,000) x 30% = 15,000

Step 3: Recognize Dividend

Dr Share of other comprehensive income of Associate and Joint Venture: 80,000 x 30% = $ 24,000 Cr Investment in Associate and Joint Venture: $ 24,000

Year 2014:

Step 4: Recognize Profit

Dr Investment in Associate and Joint Venture: (70,000 – 25,000) x 30% = $ 13,500

Cr Share of profit or loss of Associate and Joint Venture: $ $ 13,500

Step 5: Recognize Dividend

Dr Share of other comprehensive income of Associate and Joint Venture: 15,000 x 30% = 4,500 Cr Investment in Associate and Joint Venture: $ 4,500 Year 2015:

Step 6: Recognize Profit

Dr Investment in Associate and Joint Venture: (60,000 – 20,000) x 30%= $ 12,000

Cr Share of profit or loss of Associate and Joint Venture: $ 12,000

Step 7: Recognize Dividend

Dr Share of other comprehensive income of Associate and Joint Venture: 10,000 x 30% = 3,000 Cr Investment in Associate and Joint Venture: $ 3,000

Exercise 2:

Maridomo Ltd acquired a 30% interest in PA Ltd for $80,000 on 1 January 2020 by contributing a Equipment and cash. Know that, the Equipment has $22,000 in fair value. The equity of of PA Ltd at the acquisition date was:

Share capital $100.000

Asset revaluation surplus: 20,000

Retained earning $100.000

All the identifiable asset and liabilities of PA Ltd were recorded at fair value. Profit and dividends for the year end 31 Dec 2020 to 2021 were as follows:

Profit Before tax | Dividend | Asset Revaluation | |||||||

2020 | ($50,000) | $ 40,000 | |||||||

2021 | $60,000 | $12,000 | |||||||

Notes:

- The income tax rate is 20%.

- |

Dividend had been declared by Maridomo Ltd but only paid 50%

- In 2021, PA Ltd transferred $6,000 from retained earnings to general reserve.

Required:

- 1. Prepare journal entries in the records of Maridomo Ltd for each of the years ended 31 Dec 2020 and 2021 in relation to its investment in the associate, PA Ltd.

- 2. Measured of investment in associate of Maridomo Ltd at 31 Dec 2021

- 3. Show the equity of PA Ltd at 31 Dec 2021

Solution:

Step 1: Maridomo company invest in PA company

Dr Investment in Associate and Joint Venture: $ 80,000

Cr Cash: $ 58,000 (= 80,000 – 22,000)

Cr Equipment: $ 22,000

Year 2020

Step 2: Recognize Loss

Dr Share of profit or loss of Associate and Joint Venture: 50,000 x 30% = $ 15,000

Cr Investment in Associate and Joint Venture: $ 15,000

Step 3: Recognize Asset Revaluation

a.Dr Investment in Associate and Joint Venture: $ 40,000 x 30% = $ 12,000 Cr Asset Revaluation Surplus: $ 12,000 b.Dr Asset Revaluation Surplus: $ 12,000

Cr Share of other comprehensive income of Associate and Joint Venture: $ 12,000

Year 2021

Step 4: Recognize Profit

Dr Investment in Associate and Joint Venture: [(60,000 – (60,000 x 20%)] x 30% = $ 14,400

Cr Share of profit or loss of Associate and Joint Venture: $ 14,400

Step 5: Recognize Dividend

Dr Share of other comprehensive income of Associate and Joint Venture: (12,000 x 50%) x 30% = $ 1,800

Cr Investment in Associate and Joint Venture: $ 1,800

- Measured of investment in associate of Maridomo Ltd at 31 Dec 2021= 80,000-15,000+12,000 +14,400 -3,600 = $87,800

- Show the equity of PA Ltd at 31 Dec 2021

Share capital $100.000

Asset revaluation surplus : 60,000 (20,000 +40,000)

General reserve 6,000

Retained earning 80,000 ($100.000- 50,000+60,000*80%-6,000-12,000)

Bai tap on – Chuong 6 Question:

A Ltd acquired 30% interest in B Ltd for 60,000 on 1 January 2015 by contributing a machine and cash. Know that, the machine has $ 20,000 in fair value. The equity of B Ltd at the acquisition date was:

+ Share capital = $ 40,000

+ Retained earnings = $ 120,000

All the identifiable assets and liabilities of B Ltd were recorded at fair value. Profits and dividends for the years ended 31 December 2015 to 2016 were as follows:

Profit | before tax | Dividend paid | Asset Revaluation | ||||

2015 | ($40,000) | 0 | $18,000 | ||||

2016 | $ 90,000 | $21,000 | ($15,000) | ||||

Notes: The | income tax rate is 30% | ||||||

In 2016, B Ltd transferred $ 8,000 from retained earnings to general reserves Require:

Prepare journal entries from 2015 to 2016

Dich De:

Nam 2015:

Cty A Mua 30% Von = Cty B + LN truoc thue = (40,000) TK 421 (LN sau thue)

$ 60,000 Nam 2016: + TK 412 (Asset Revaluation Surplus) 18,000

+ TK 411 = $ 40,000

+ TK 421 = $ 120,000 + LN truoc thue = 90,000 TK 421 = 90,000 – 30% x 90,000

+ Tra co tuc = 21,000

+ TK 412 (Asset Revaluation Surplus) (15,000)

+ Chuyen tu LN sang quy: 8,000Thue Thu nhap doanh nghiep: 30%

Solution:

Year 2015:

Step 1: A Ltd invested in B Ltd: Cty A dau tu vao cty B

No 222: 60,000 Dr Investment in Associate and Joint Venture: $ 60,000

Co 111, 112: 40,000 Cr Cash: $ 40,000

Co 211: 20,000 Cr Machine: $ 20,000

Step 2: Recognize Loss = Ghi nhan 1 khoan LO

No 635: 40,000 x 30% = 12,000

Co 222: 40,000 x 30% = 12,000

Dr Share of profit or loss of Associate and Joint Venture: 40,000 x 30% = 12,000

Cr Investment in Associate and Joint Venture: 40,000 x 30% = 12,000

Step 3: Recognize Asset Revaluation surplus = Ghi nhan TK 412 a.No 222: 18,000 x 30% = 5,400 Co 515: 18,000 x 30% = 5,400

Dr Investment in Associate and Joint Venture = 18,000 x 30% = 5,400

Cr Share of other comprehensive income of Associate and Joint Venture = 18,000 x 30% = 5,400 b.No 515: 5,400

Co 412: 5,400

Dr Share of other comprehensive income of Associate and Joint Venture: 5,400 Cr Asset Revaluation Surplus: 5,400 Year 2016:

- Recognize Profit = Ghi nhan Loi Nhuan

No 222: (90,000 – 30% x 90,000) x 30% = 63,000 x 30% = $ 18,900

Co 515: $ 18,900

Dr Investment in Associate and Joint Venture: (90,000 – 30% x 90,000) x 30% = 63,000 x 30% = $ 18,900 Cr Share of Profit or Loss of Associate and Joint Venture : 18,900

- Recogize “Dividend” = Ghi nhan “Tra co tuc”

No 111 , 112: 21,000 x 30% = $ 6,300

Co 222: $ 6,300

Dr Cash: 21,000 x 30% = $ 6,300

Cr Investment in Associate and Joint Venture: $ 6,300

- Recogize “Asset Revaluation Surplus”

c.1 No 635: 15,000 x 30% = 4,500

Co 222: 15,000 x 30 % = 4,500

Dr Share of other comprehensive income of Associate and Joint Venture: 15,000 x 30% = 4,500 Cr Investment in Associate and Joint Venture: 15,000 x 30 % = 4,500 c.2 No 412: 4,500 Dr Asset Revaluation Surplus: 4,500

Co 635: 4,500 Cr Share of other comprehensive of Associate and Joint Venture: 4,500

Bai on tap – Chuong 4:

Adjusting events vs Non-adjusting events

(Nhung su kien duoc dieu chinh va Nhung su kien khong duoc dieu chinh)

1. Adjusting events: Những sự kiện được điều chỉnh

- Mỗi tình huống đều phải giải thích. Nếu là adjusting events thì sự giải thích luôn là “This event provides evidence of conditions

that | existed at | the reporting date.” |

- The bankruptcy of a customer: Nếu khách hàng bị phá sản sau ngày lập báo tài chính It is an adjusting event

Dr Uncollectible account expense No TK 6….:

Cr Allowance for uncollectible account Co 2293:

Explain: This event provides evidence of conditions that existed at the reporting date

- The sale of inventory at a price substantially lower than its cost: Bán 1 HTK tại mức giá thấp hơn giá gốc It is an adjusting event

Dr Cost of Goods Sold No TK 632

Cr Inventory Co 156

Explain: This event provides evidence of conditions that existed at the reporting date

- The sale of property, plant, and equipment for a net selling price that is lower than the carrying amount: Bán 1 TSCDHH ( nhà xưởng , máy móc ) với giá thấp hơn giá trị còn lại của tài sản

It is an adjusting event

Explain: This event provides evidence of conditions that existed at the reporting date

- The determination of an incentive or bonus payment: Nhận đc tiền thưởng cho 1 sáng kiến It is an adjusting event

Explain: This event provides evidence of conditions that existed at the reporting date

- The discovery of a fraud which had occurred during the year: Phát hiện 1 lỗi đã xảy ra trong năm It is an adjusting event

Explain: This event provides evidence of conditions that existed at the reporting date f. The disposal of inventory: Bỏ hàng tồn kho

It is an adjusting event

Dr Cost of goods sold No 632

Cr Inventory Co 156

Explain: This event provides evidence of conditions that existed at the reporting date g. The settlement of court case : Việc thanh toán nghĩa vụ từ 1 phiên tòa It is an adjusting event

Dr Expense Cr Provision

Explain: This event provides evidence of conditions that existed at the reporting date

2. Non-adjusting events: Những sự kiện không được điều chỉnh

- Mỗi tình huống đều phải giải thích. Nếu là adjusting events thì sự giải thích luôn là “This event provides evidence of conditions

that existed | after | the reporting date.” |

a. Stock split = Right issue = Announce a bonus issue = Dividend : Quyền nhận được thêm cổ phiếu / Thông báo cổ phiếu thường /

Chia cổ tức

It is a non-adjusting event

Explain: This event provides evidence of conditions that existed after the reporting date b. A change in tax rate = Sự thay đổi về thuế suất thuế TNDN

It is a non-adjusting event

Explain: This event provides evidence of conditions that existed after the reporting date

- Announcing a plan to discontinue on operation: Doanh nghiệp / Bộ phận không thể hoạt động It is a non-adjusting event

Explain: This event provides evidence of conditions that existed after the reporting date

- The destruction of a building by fire/by flood/by earthwake: 1 tòa nha bị hủy hoại bởi hỏa hoạn / động đất / lũ lụt It is a non-adjusting event

Explain: This event provides evidence of conditions that existed after the reporting date

Tài liệu liên quan:

-

Tài liệu Chuẩn mực báo cáo tài chính quốc tế | Trường Đại học Công nghiệp TP.HCM

248 124 -

Đề ôn giữa kỳ Chuẩn mực báo cáo tài chính quốc tế | Trường Đại học Công nghiệp TP.HCM

459 230 -

Bài tập ôn tập chương 6 | Chuẩn mực báo cáo tài chính quốc tế | Trường Đại học Công nghiệp TP.HCM

278 139 -

Đề ôn tập cuối kỳ Chuẩn mực báo cáo tài chính quốc tế | Trường Đại học Công nghiệp TP.HCM

494 247 -

Ôn thi giữa kỳ Chuẩn mực báo cáo tài chính quốc tế | Trường Đại học Công nghiệp TP.HCM

394 197