Recording business transactionsc - Nguyên Lý Kế Toán | Trường Đại học Tôn Đức Thắng

Explain accounts, journals and ledgers as they relate to recording transactions, and describe common accounts•Define debits, credits and normal account balances, and use double-entry accounting and T-accounts. Tài liệu được sưu tầm và soạn thảo dưới dạng file PDF để gửi tới các bạn sinh viên cùng tham khảo, ôn tập đầy đủ kiến thức, chuẩn bị cho các buổi học thật tốt. Mời bạn đọc đón xem!

Môn: Nguyên Lý Kế Toán (NLKTTDT) 91 tài liệu

Trường: Trường Đại học Tôn Đức Thắng 4.5 K tài liệu

Tác giả:

Preview text:

Chapter 2

Recording business transactions 2/23/2022

201039 _ Recording business transactions 1 Learning objectives

• Explain accounts, journals and ledgers as they relate to recording

transactions, and describe common accounts

• Define debits, credits and normal account balances, and use

double-entry accounting and T-accounts

• List the steps of the transaction recording process

• Post transactions from the journal to the ledger

• Prepare the trial balance from the T-accounts 2/23/2022

201039 _ Recording business transactions 2

2.1. The account, the ledger and the journal

• An account is the detailed record of all the changes that have

occurred in a particular asset, liability or owners’ equity during a period

• The journal is the chronological record of the transactions

• The ledger is the record holding all accounts

• A list of all the ledger accounts, along with their balances, is called a trial balance 2/23/2022

201039 _ Recording business transactions 3

2.1. The account, the ledger and the journal Prepare Collect Record Copy the source of transactions (post) to documents in the journal the ledger trial balance 2/23/2022

201039 _ Recording business transactions 4

2.1. The account, the ledger and the journal Assets

An asset is a resource controlled by an entity as a result of past

events that is expected to provide future economic benefits to the entity in the future • Cash • Prepaid expenses • Accounts receivable • Land • Bills receivable • Buildings • Inventories • Plant and equipment 2/23/2022

201039 _ Recording business transactions 5

2.1. The account, the ledger and the journal Liabilities

A liability is a present obligation of the entity arising from past

events, the settlement of which is expected to result in an outflow

from the entity of resources embodying economic benefits • Accounts payable • Bills payable

• Accrued liabilities (e.g. salary _______, interest _______, electricity ______, etc.) 2/23/2022

201039 _ Recording business transactions 6

2.1. The account, the ledger and the journal Owners’ equity

The financial estimate of owners’ claims to the value in a business

is called owners’ equity. It is the residual interest in the assets of

an entity after deducting all liabilities •Capital •Drawings •Income

•Service revenue/ sale revenue •Expenses 2/23/2022

201039 _ Recording business transactions 7

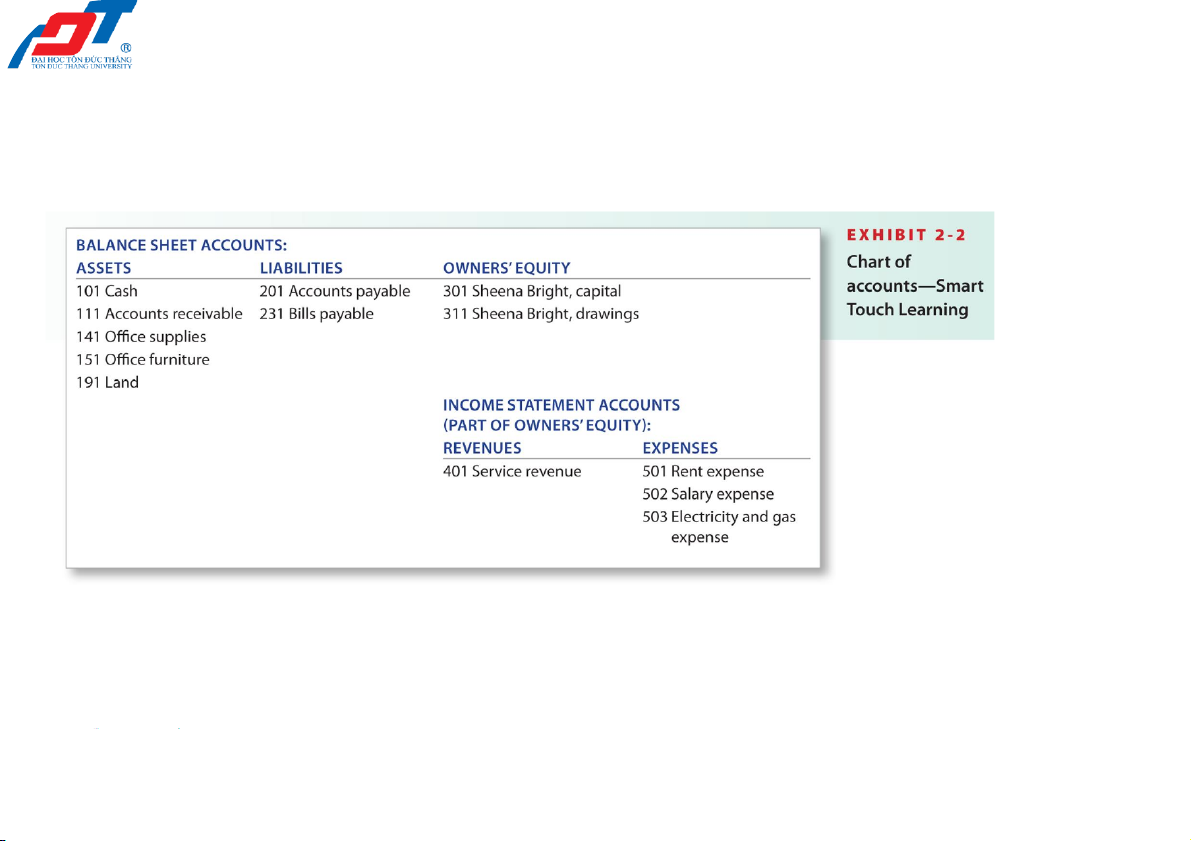

2.1. The account, the ledger and the journal Chart of accounts 2/23/2022

201039 _ Recording business transactions 8

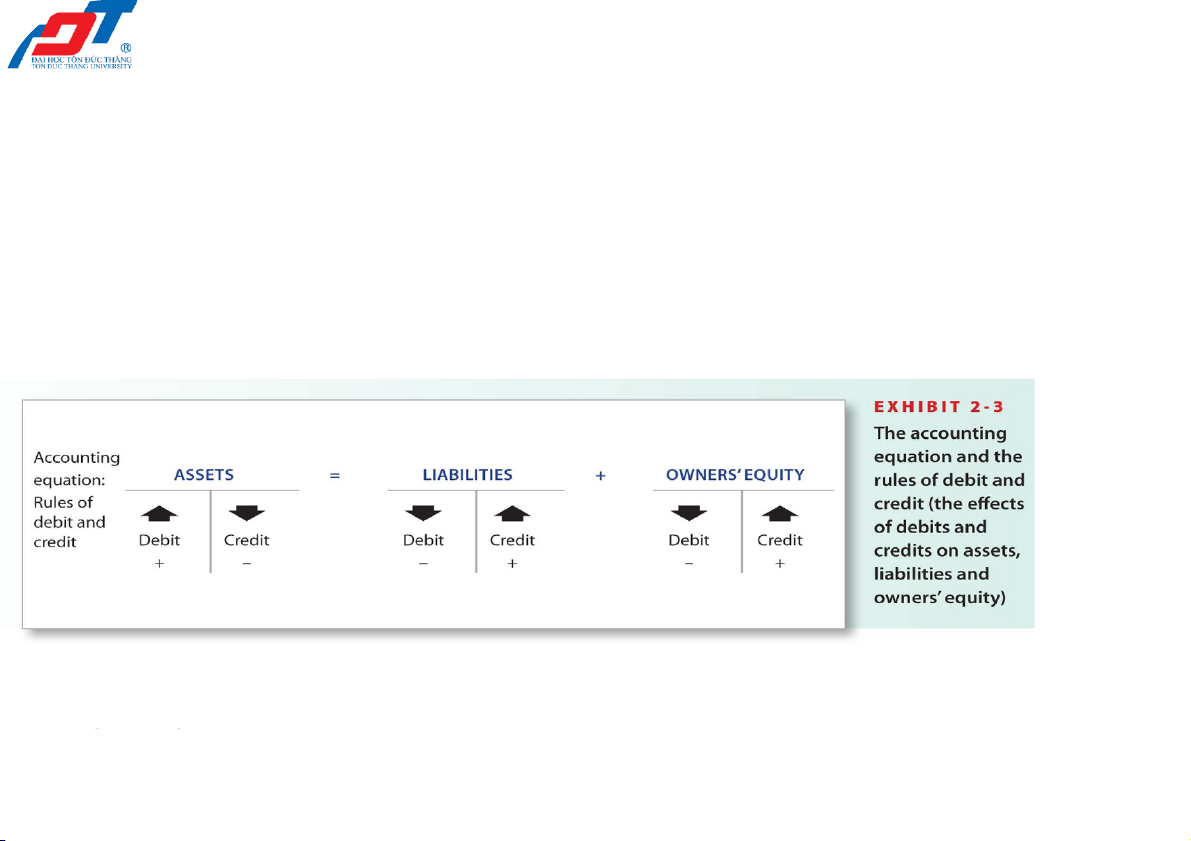

2.2. Debits, credits and double-entry accounting

• Accounting is based on a double-entry system

• Each transaction affects at least two accounts

• A popular account format is called T-account Debit Account Title Credit 2/23/2022

201039 _ Recording business transactions 9

2.2. Debits, credits and double-entry accounting

• The account category determines how increases and

decreases in the account are recorded as debits and credits

• The pattern of recording debits and credits is based on the accounting equation 2/23/2022

201039 _ Recording business transactions 10 Minigame 2/23/2022

201039 _ Recording business transactions 11

2.3. Recording transactions in the journal Specify Determine each whether Enter the Identify the account each transaction transaction affected by account is in the from the increased journal, source transaction or including a documents and decreased brief classify it by the explanation by type transaction 2/23/2022

201039 _ Recording business transactions 12

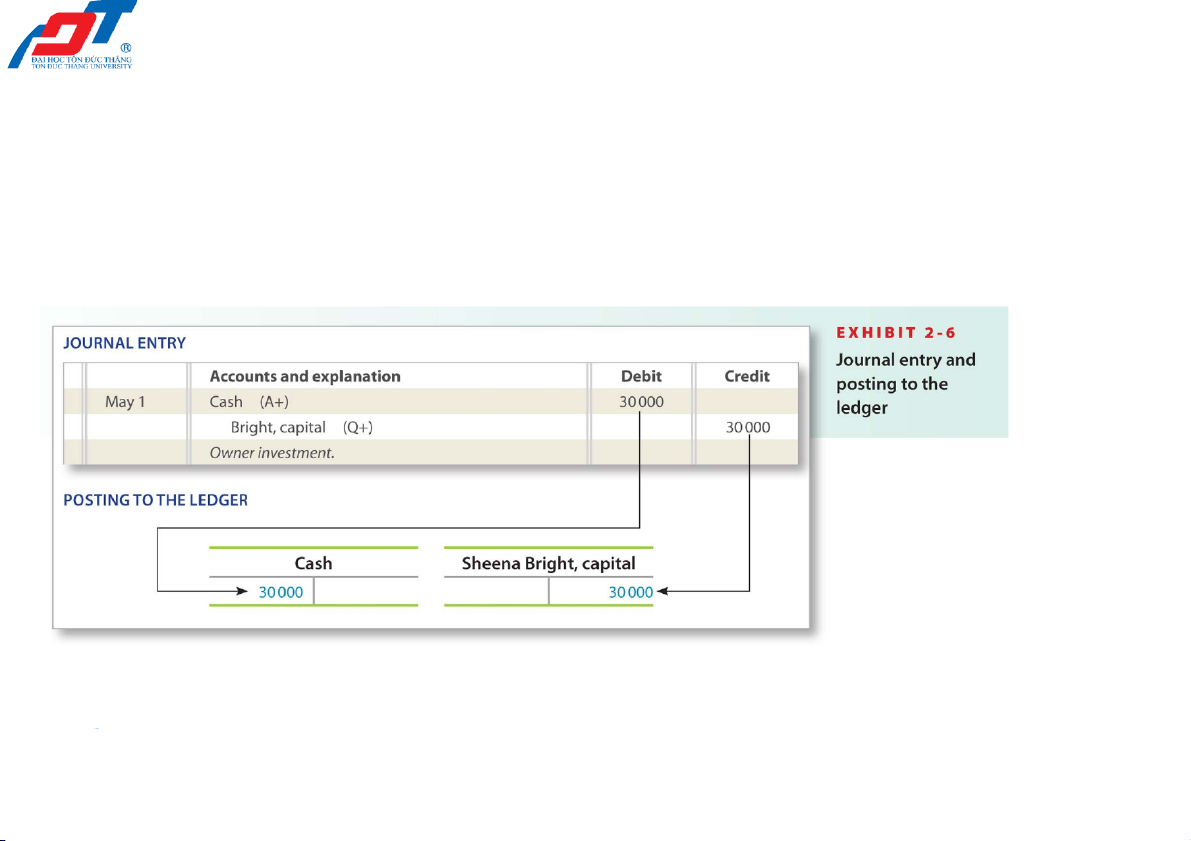

2.3. Recording transactions in the journal

Eg: The Smart Touch business received of Sheena Bright’s

$30,000 cash investment in the business.

1. The source documents: ___(1)_________

2. The accounts affected: ____(2)_____________

3. The accounts increased/decreased: ____(3)_________ 4.

Date Accounts & Explanations Debit (Dr.) Credit (Cr.) 2/23/2022

201039 _ Recording business transactions 13

2.4. Transactions analysis, journalizing

and posting to the accounts

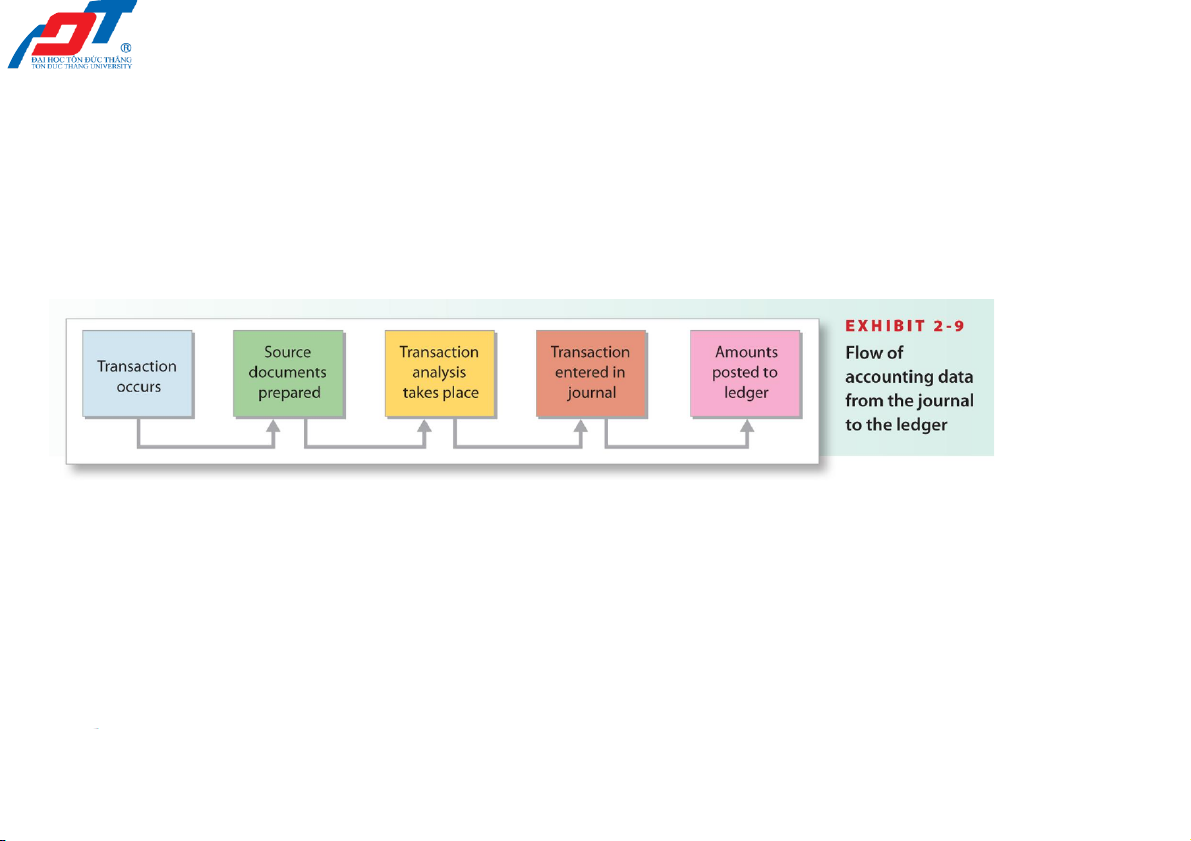

Copying information (posting) from the journal to the ledger 2/23/2022

201039 _ Recording business transactions 14

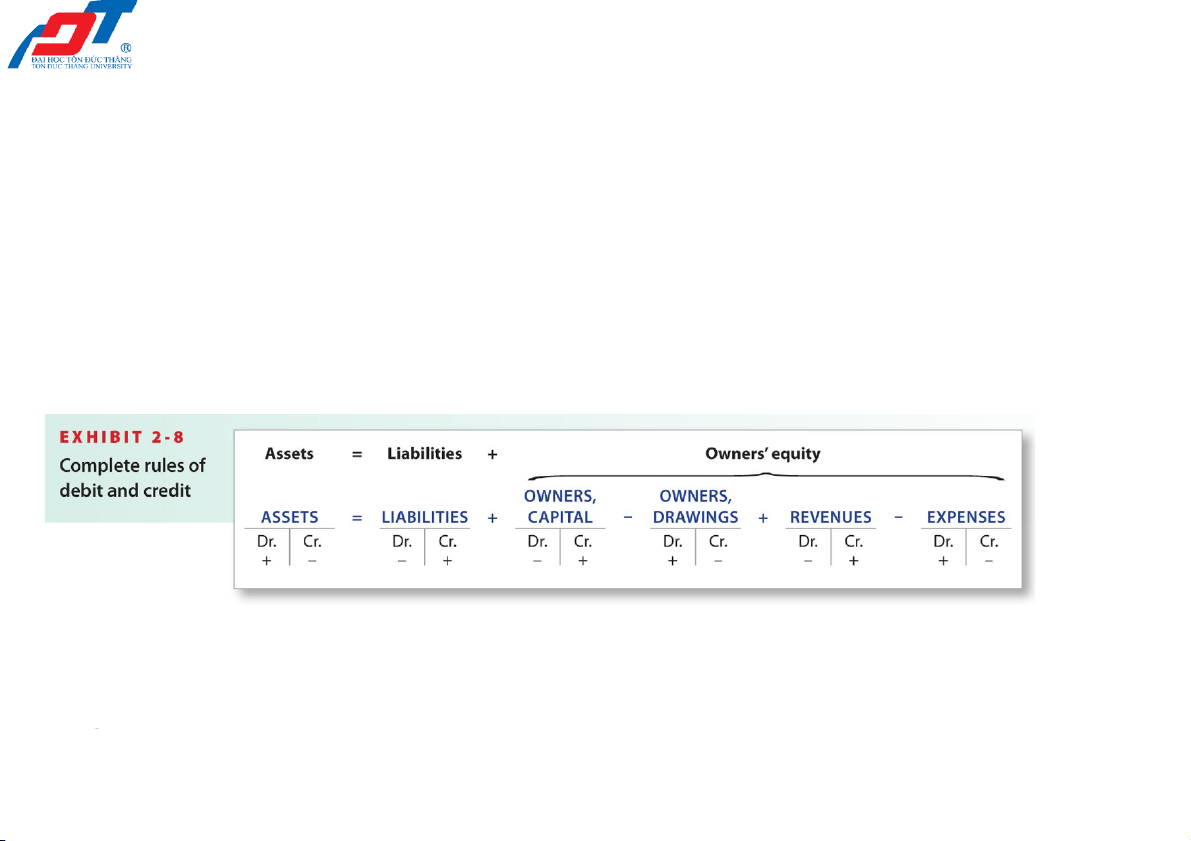

2.4. Transactions analysis, journalizing

and posting to the accounts

The normal balance of an account

(Expanding the accounting equation to

account for revenues and expenses) 2/23/2022

201039 _ Recording business transactions 15

2.4. Transactions analysis, journalizing

and posting to the accounts

Summarise: Flow of accounting information 2/23/2022

201039 _ Recording business transactions 16

2.4. Transactions analysis, journalizing

and posting to the accounts

Eg: Practice journalizing and posting with specific examples:

Details of transactions occurred at Smart Touch business on May 20X2

(1) Sheena Bright invested $30,000 cash in the business.

(2) Paid $20,000 cash for land.

(3) Bought $500 of office supplies on credit.

(4) Received $5,500 cash from clients for service revenue earned.

(5) Performed training service for clients on credit, $3,000.

(6) Paid cash expenses: computer lease, $600; office rent, $1,100;

employee salary, $1,200; electricity and gas, $400. 2/23/2022

201039 _ Recording business transactions 17

2.4. Transactions analysis, journalizing

and posting to the accounts

E.G (Cont.) Practice journalizing and posting with specific examples:

(7) Paid $300 on the account payable created in transaction 3.

(8) Remodelled Sheena Bright’s personal residence. This is not a transaction of the business.

(9) Collected $1,000 on the account receivable created in transaction 5.

(10) Sold land for cash at its cost of $9,000.

(11) Withdrew $2,000 cash for personal expenses. 2/23/2022

201039 _ Recording business transactions 18 Record to the JOURNAL Smart Touch Learning May 20X2 Journal

No. Accounts & Explanation Debit Credit (1) (2) (3) (4) 2/23/2022

201039 _ Recording business transactions 19

Record to the JOURNAL (Cont.)

No. Accounts & Explanation Debit Credit (5) (6) (7) (8) (9) 2/23/2022

201039 _ Recording business transactions 20

Tài liệu liên quan:

-

Bài giảng Chapter 6: Audit cash and cash equivalents môn Nguyên lý kế toán | Trường Đại học Tôn Đức Thắng

35 18 -

Bài giảng Chapter 5: Audit completion and audit report môn Nguyên lý kế toán | Trường Đại học Tôn Đức Thắng

33 17 -

Tài liệu Nguyên Lý Kế Toán

36 18 -

Tài liệu NLKT - Trường Đại học Tôn Đức Thắng

32 16 -

Trắc nghiệm ôn tập - Nguyên Lý Kế Toán | Trường Đại học Tôn Đức Thắng

610 305