Retailing operations - Nguyên Lý Kế Toán | Trường Đại học Tôn Đức Thắng

Describe retailing operations, perpetual and periodic inventory systems and understand how to account for GST•Account for the purchase of inventory using a perpetual system•Account for the sale of inventory using a perpetual system. Tài liệu được sưu tầm và soạn thảo dưới dạng file PDF để gửi tới các bạn sinh viên cùng tham khảo, ôn tập đầy đủ kiến thức, chuẩn bị cho các buổi học thật tốt. Mời bạn đọc đón xem!

Môn: Nguyên Lý Kế Toán (NLKTTDT) 91 tài liệu

Trường: Trường Đại học Tôn Đức Thắng 4.5 K tài liệu

Tác giả:

Preview text:

Chapter 5 Retailing operations 201044 - Retailing operations 1 Learning objectives

• Describe retailing operations, perpetual and periodic inventory

systems and understand how to account for GST

• Account for the purchase of inventory using a perpetual system

• Account for the sale of inventory using a perpetual system

• Adjust and close the accounts of a retailing business

• Prepare a retailer’s financial statements

• Use gross profit percentage, inventory turnover and days in

inventory to evaluate a business 201044 - Retailing operations 2 4/6/2022

5.1. What are retailing operations?

• Retailing consists of buying and selling goods rather than services

• Retailers have some new balance sheet and income statement

items, for example Inventory, Sales revenue, and Cost of sales

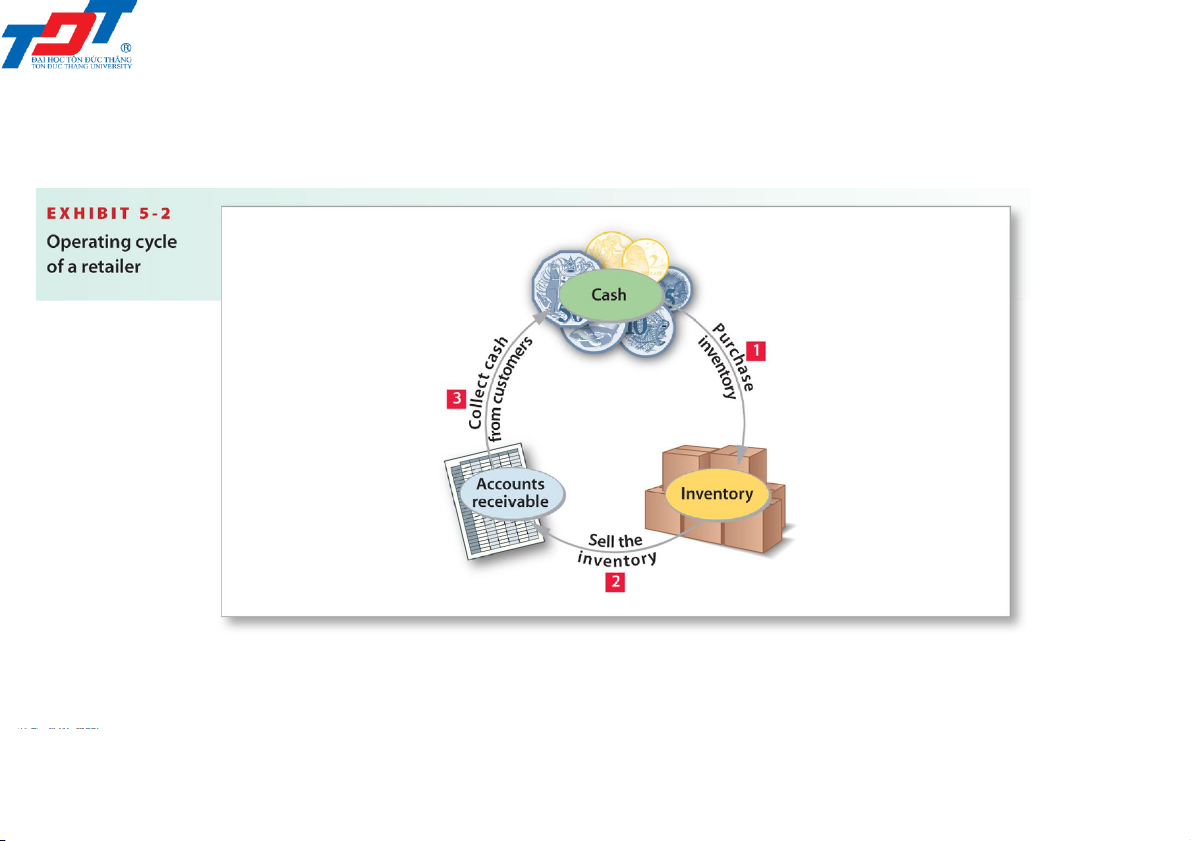

• The operating cycle of a retailing business begins when the business

purchases inventory from a vendor. It then sells the inventory to a

customer. Finally, the business collects cash from customers 201044 - Retailing operations 3 4/6/2022

5.1. What are retailing operations? 201044 - Retailing operations 4 4/6/2022

5.1. What are retailing operations?

Goods and services tax (GST)

• GST is a tax levied on the supply of goods and services

• The tax is a flat percentage charge

• Each firm registered for GST collects tax on the goods and services

it supplies and pays tax on the goods and services it buys

• The firm then deducts the tax it pays on purchases from the tax it

charges on sales and pays the balance to the Australian Taxation Office 201044 - Retailing operations 5 4/6/2022

5.1. What are retailing operations?

Inventory systems: Perpetual and Periodic

• The periodic inventory system is normally used for relatively inexpensive goods

• Goods are counted periodically to determine quantity

• The perpetual inventory system keeps a running computerised record of inventory

• The number of inventory units and the dollar amounts are

perpetually (constantly) updated

• It records units purchased and cost amount, units sold and sales

and cost amounts, and the quantity of inventory on hand and its cost 201044 - Retailing operations 6 4/6/2022

5.2. Accounting for inventory in the perpetual system 201044 - Retailing operations 7 4/6/2022

5.2. Accounting for inventory in the perpetual system Purchase of Inventory

• The inventory account is increased with each purchase

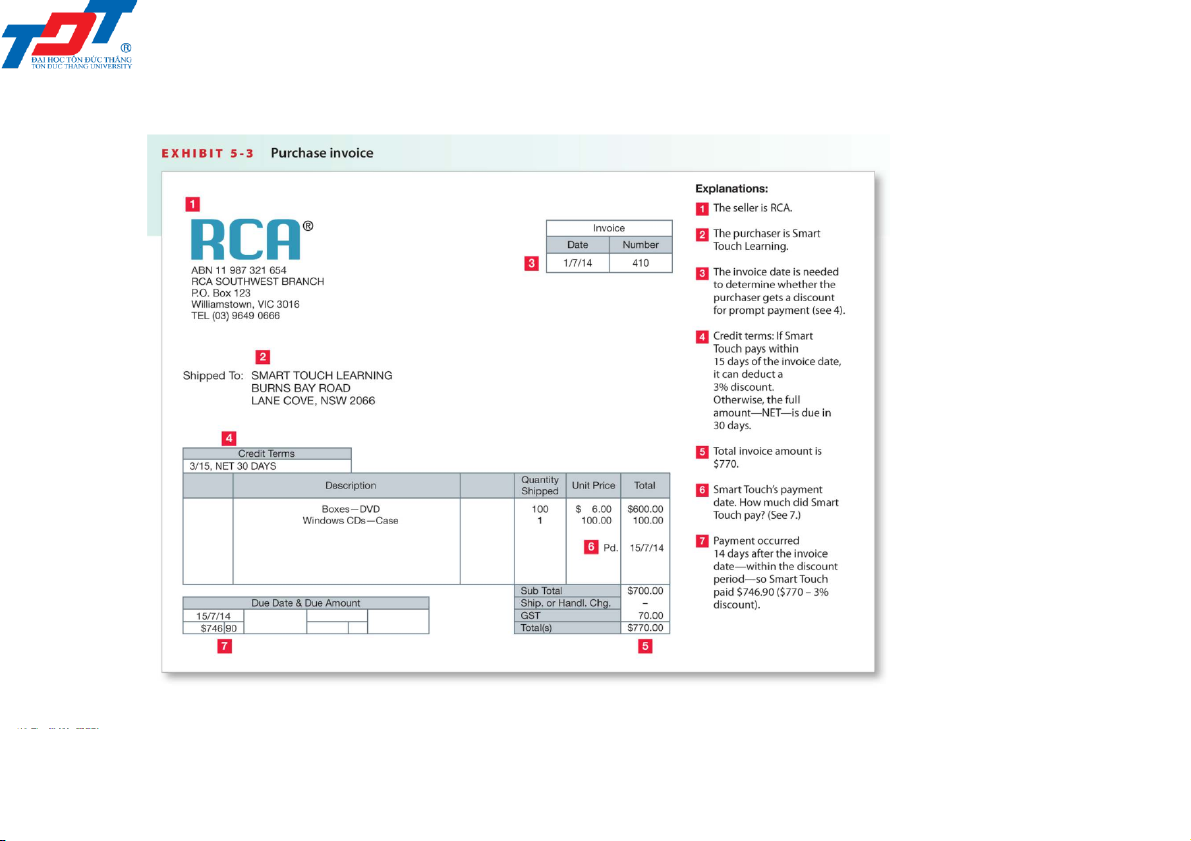

• The vendor submits an invoice for payment

• The inventory account is used for goods purchased

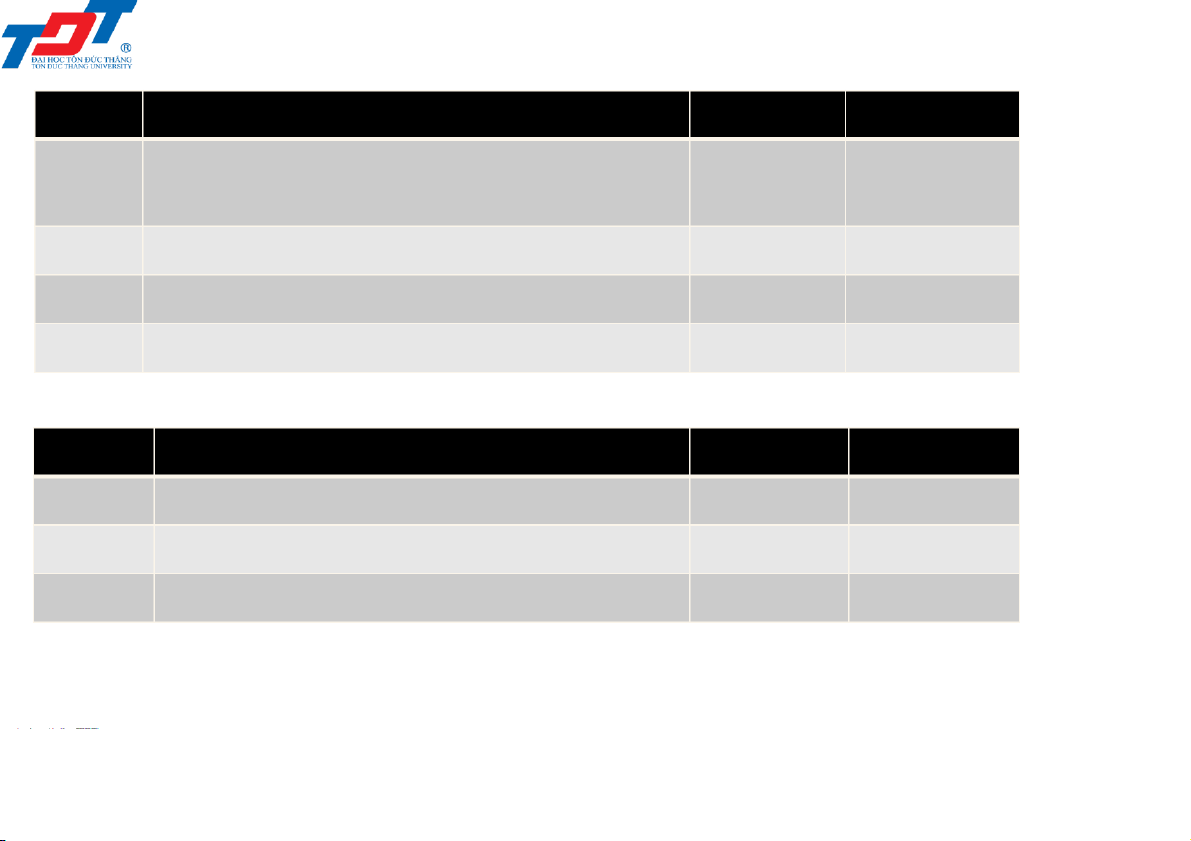

• The method of payment is credited Date Account title Dr Cr Jul 3 Inventory (770/1.1) (A+) 700 GST clearing (770/11) (A+) 70 Accounts payable (L+) 770

Purchased inventory on credit. 201044 - Retailing operations 8 4/6/2022

5.2. Accounting for inventory in the perpetual system

• Many businesses offer customers a settlement discount for early payment

• RCA’s credit terms of ‘3/15, Net 30 days’ mean that Smart Touch

can deduct 3% from the total bill (excluding freight charges, if any) if

the business pays within 15 days of the invoice date 201044 - Retailing operations 9 4/6/2022

5.2. Accounting for inventory in the perpetual system Date Account title Dr Cr Jul Accounts payable (L–) 770 15 Cash ($770 × 0.97) (A–) 746.90 Inventory 21.00 ($770×0.03×10/11) (A–) GST clearing 2.10 ($770×0.03×1/11) (A–/L+)

Paid within discount period. 201044 - Retailing operations 10 4/6/2022

5.2. Accounting for inventory in the perpetual system

• Businesses allow customers to return goods that are

defective, damaged or otherwise unsuitable – purchase returns

• The seller may also deduct an allowance from the amount

the buyer owes – purchase allowances Date Account title Dr Cr Jul 4 Accounts payable (L–) 110 Inventory (110/1.1) (A+) 100

GST clearing (110/11) (A–/L+) 10

Returned inventory to seller. 201044 - Retailing operations 11 4/6/2022

5.2. Accounting for inventory in the perpetual system

• The purchase agreement specifies FOB (free on board) terms to

determine when title to the good transfers to the purchaser and who pays the freight

• FOB delivery point means the buyer takes ownership (title) to the goods at the delivery point

• FOB destination means the buyer takes ownership (title) to the

goods at the delivery destination point

• Freight in is the transportation cost to ship goods into the

purchaser’s warehouse (part of the cost of inventory)

• Freight out is the transportation cost to ship goods out of the

warehouse and to the customer (selling expense) 201044 - Retailing operations 12 4/6/2022 5.3. Sale of inventory

• After a business buys inventory, the next step is to sell the goods

• The amount a business earns from selling inventory is called Sales revenue (Sales)

• At the time of the sale, two entries must be recorded in the perpetual

system: one entry records the sale and the cash (or receivable) at

the time of the sale; the second entry records Cost of sales (debit

the expense) and reduces the Inventory (credit the asset)

• Cost of sales (COS) is the cost of inventory that has been sold to customers 201044 - Retailing operations 13 4/6/2022 5.3. Sale of inventory 201044 - Retailing operations 14 4/6/2022

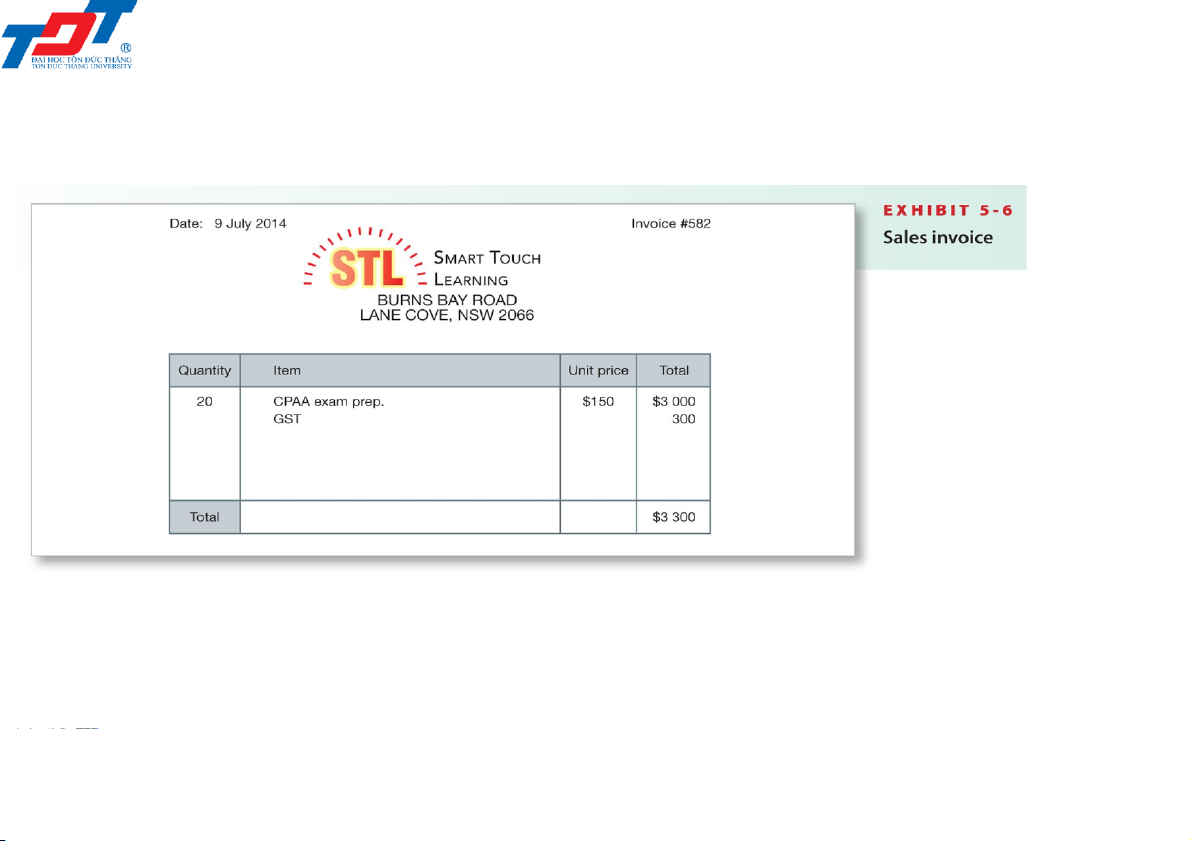

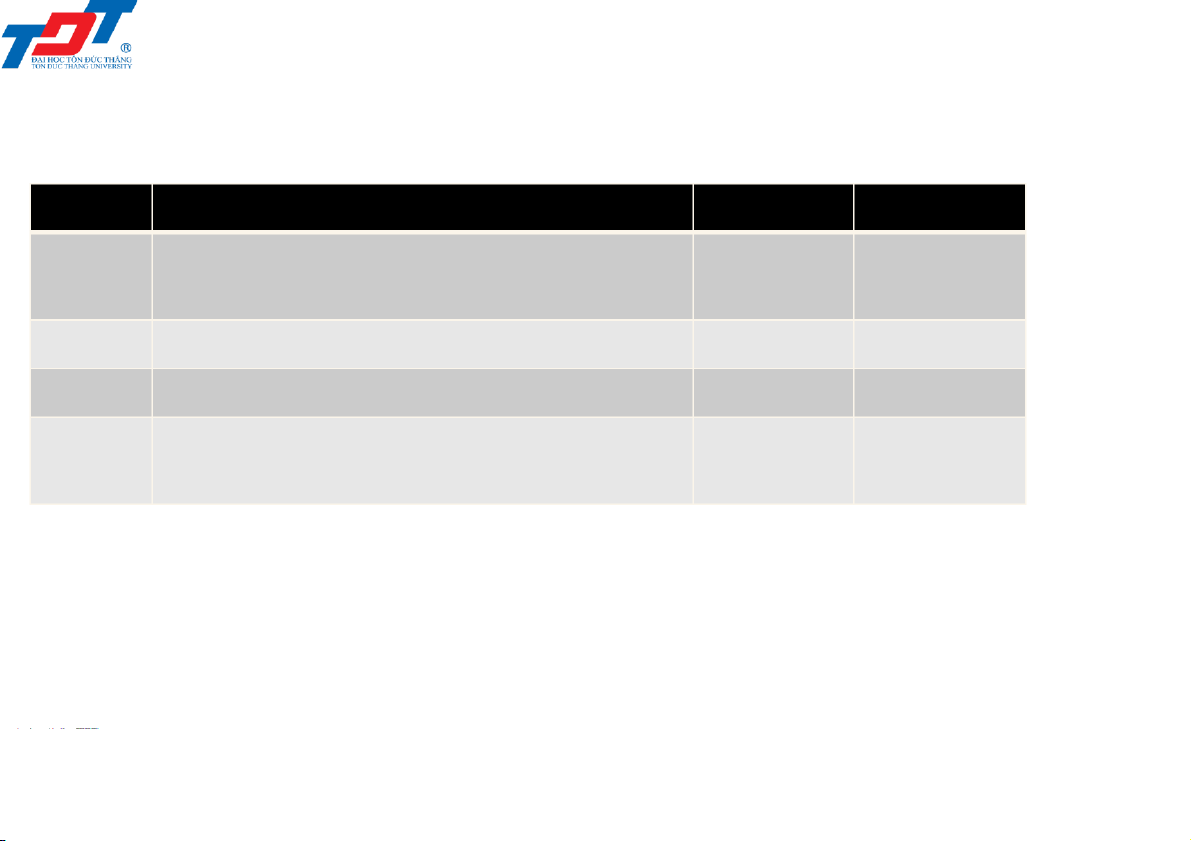

5.3. Sale of inventory: Cash sale Date Account title Dr Cr Jul 9 Cash (A+) 3 300 Sales revenue (3 300/1.1) (R+) 3 000

GST clearing (3 300/11) (A–/L+) 300 Cash sale. Date Account title Dr Cr Jul 9 Cost of sales (E+) 1 900 Inventory (A–) 1 900

Recorded the cost of goods sold. 201044 - Retailing operations 15 4/6/2022

5.3. Sale of inventory: Credit sale Date Account title Dr Cr Jul 11 Accounts receivable (A+) 5 500 Sales revenue (5 500/1.1) (R+) 5 000

GST clearing (5 500/11) (A–/L+) 500 Sale on credit. Jul 11 Cost of sales (E+) 2 900 Inventory (A–) 2 900 2 900

Recorded the cost of sales. Date Account title Dr Cr Jul 19 Cash (A+) 5 500 Accounts receivable (A–) 5 500 Collection on account. 201044 - Retailing operations 16 4/6/2022 5.3. Sale of inventory

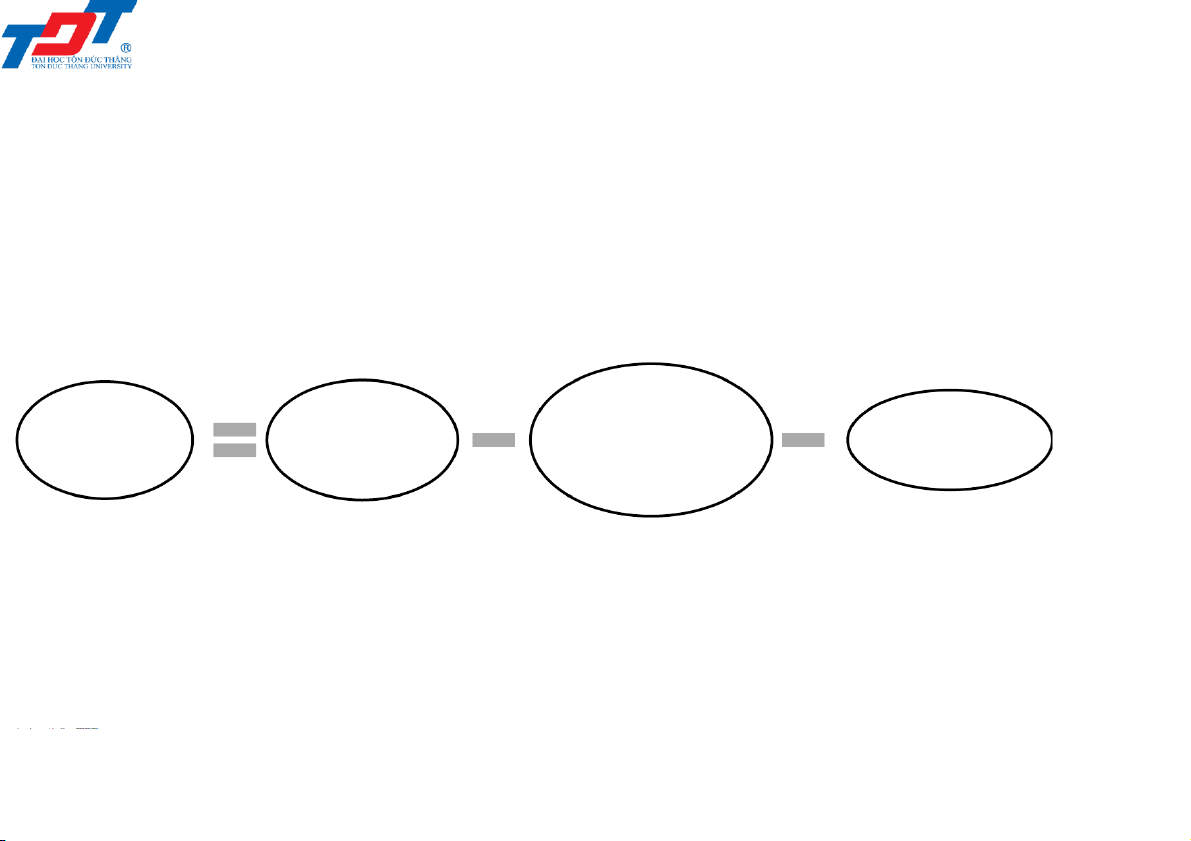

• Sales returns and allowances and sales settlement discounts

decrease the net amount of revenue earned on sales

• Sales returns and allowances and Sales discounts are contra accounts to Sales revenue Net Sales Sales Sales sales returns and revenue discounts revenue allowances 201044 - Retailing operations 17 4/6/2022

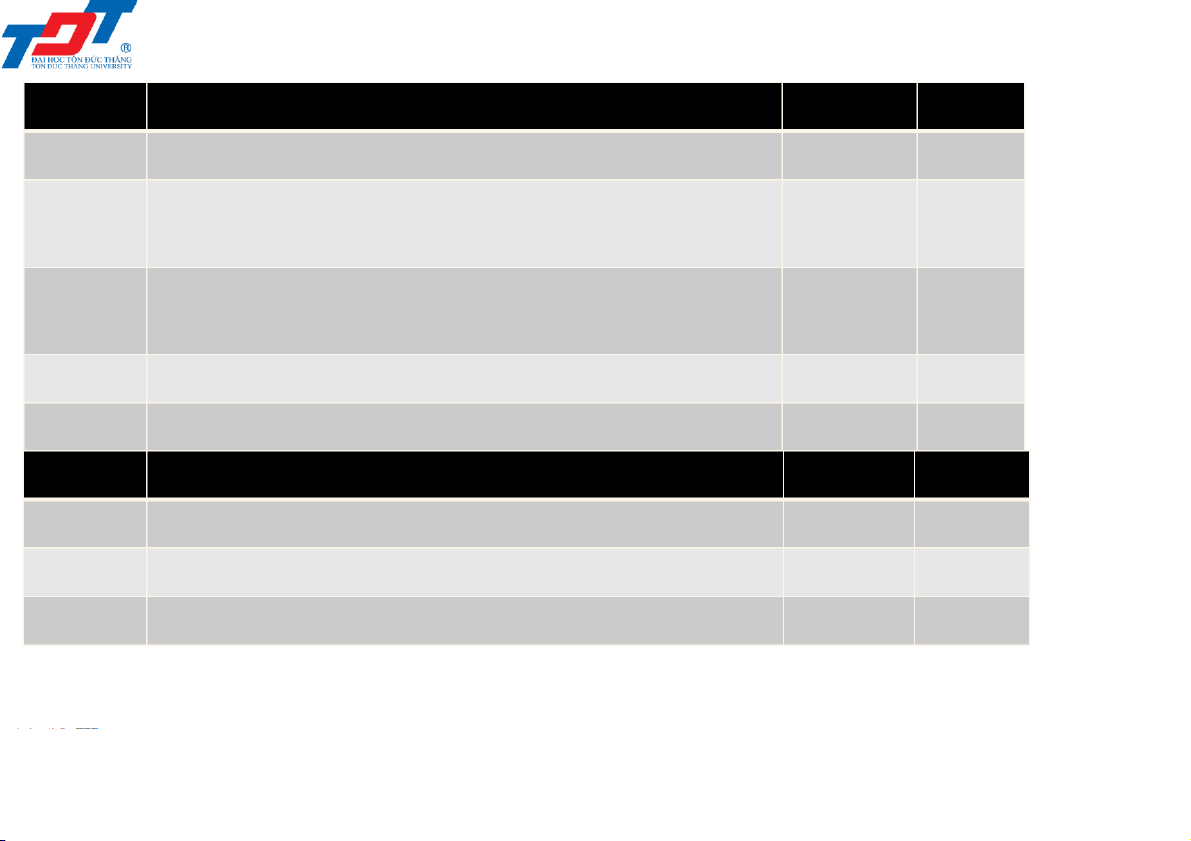

5.3. Sale of inventory: Sales returns Date Account title Dr Cr

Jul 12 Sales returns and allowances 600 (660/1.1) (CR+)

GST clearing (660/11) (A+/L–) 60 Accounts receivable (A–) 660

Received returned goods. Date Account title Dr Cr Jul 12 Inventory (A+) 400 Cost of sales (E–) 400

Placed goods back in inventory. 201044 - Retailing operations 18 4/6/2022

5.3. Sale of inventory: Sales allowances Date Account title Dr Cr Jul 15 Sales returns and allowances 100 (110/1.1) (CR+)

GST clearing (110/11) (A+/L–) 10 Accounts receivable (A–) 110

Granted a sales allowance for damaged goods. 201044 - Retailing operations 19 4/6/2022

5.3. Sale of inventory: Sales discounts Date Account title Dr Cr Jul 17 Cash ($4 400 × 0.98) (A+) 4 312

Sales discounts ($4 400 × 0.02 × 10/11) 80 (CR+)

GST clearing ($4 400 × 0.02 × 1/11) 8 (A+/L–)

Accounts receivable (A–) 4 400 4 400

Cash collection within the discount period. Date Account title Dr Cr Jul 28 Cash ($7 150 – $4 400) (A+) 2 750 Accounts receivable (A–) 2 750

Cash collection after the discount period. 201044 - Retailing operations 20 4/6/2022

Tài liệu liên quan:

-

Bài giảng Chapter 6: Audit cash and cash equivalents môn Nguyên lý kế toán | Trường Đại học Tôn Đức Thắng

35 18 -

Bài giảng Chapter 5: Audit completion and audit report môn Nguyên lý kế toán | Trường Đại học Tôn Đức Thắng

33 17 -

Tài liệu Nguyên Lý Kế Toán

36 18 -

Tài liệu NLKT - Trường Đại học Tôn Đức Thắng

32 16 -

Trắc nghiệm ôn tập - Nguyên Lý Kế Toán | Trường Đại học Tôn Đức Thắng

610 305