Assignment Presentation 8: Monopolist Analysis and Cost Functions | Microeconomics | Trường Đại học Quốc tế, Đại học Quốc gia Thành phố Hồ Chí Minh

Assume government imposes a tax of 8 $ per unit of goods sold, what are the price and optimal quantity that gives the firm maximum profit? What is this maximum profit? As the government imposes a tax of $8. Tài liệu được sưu tầm và soạn thảo dưới dạng file PDF với mục đích hỗ trợ học tập và tham khảo. Nội dung tài liệu được trình bày rõ ràng, dễ tiếp cận, phù hợp cho việc ôn tập và củng cố kiến thức trong quá trình học đại học. Đây sẽ là nguồn tư liệu hữu ích giúp các bạn sinh viên chuẩn bị tốt hơn cho các buổi học, đồng thời mở rộng thêm hiểu biết về môn học. Hy vọng tài liệu này sẽ mang lại nhiều giá trị và hỗ trợ các bạn trong hành trình học tập. Mời bạn đọc cùng tham khảo!

Môn: Microeconomics 635 tài liệu

Trường: Trường Đại học Quốc tế, Đại học Quốc gia Thành phố Hồ Chí Minh 1.9 K tài liệu

Tác giả:

Preview text:

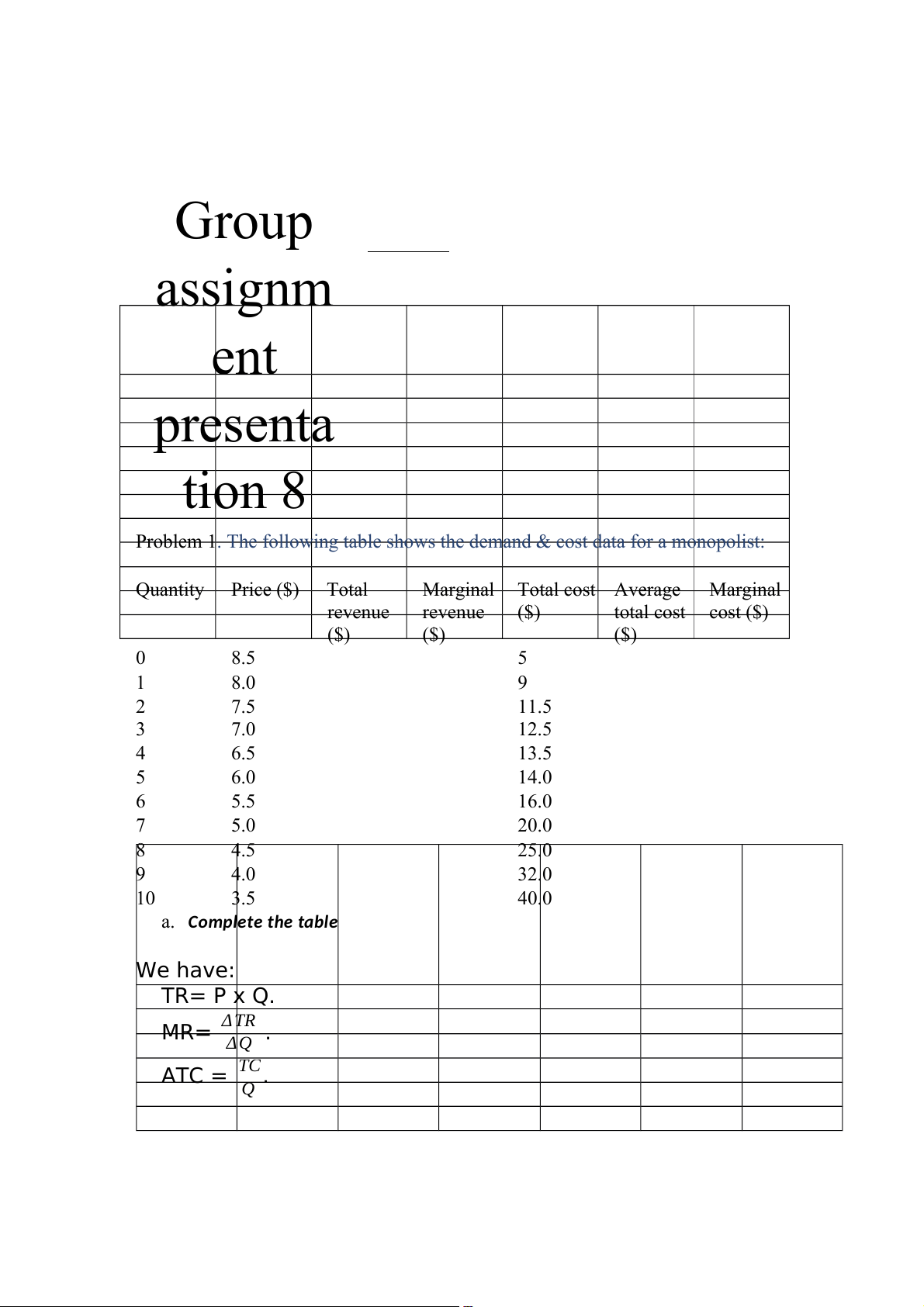

Group assignm ent presenta tion 8

Problem 1. The following table shows the demand & cost data for a monopolist: Quantity Price ($) Total Marginal Total cost Average Marginal revenue revenue ($) total cost cost ($) ($) ($) ($) 0 8.5 5 1 8.0 9 2 7.5 11.5 3 7.0 12.5 4 6.5 13.5 5 6.0 14.0 6 5.5 16.0 7 5.0 20.0 8 4.5 25.0 9 4.0 32.0 10 3.5 40.0

a. Complete the table We have: TR= P x Q. Δ TR MR= . Δ Q TC ATC = . Q Δ TC MC = . Δ Q

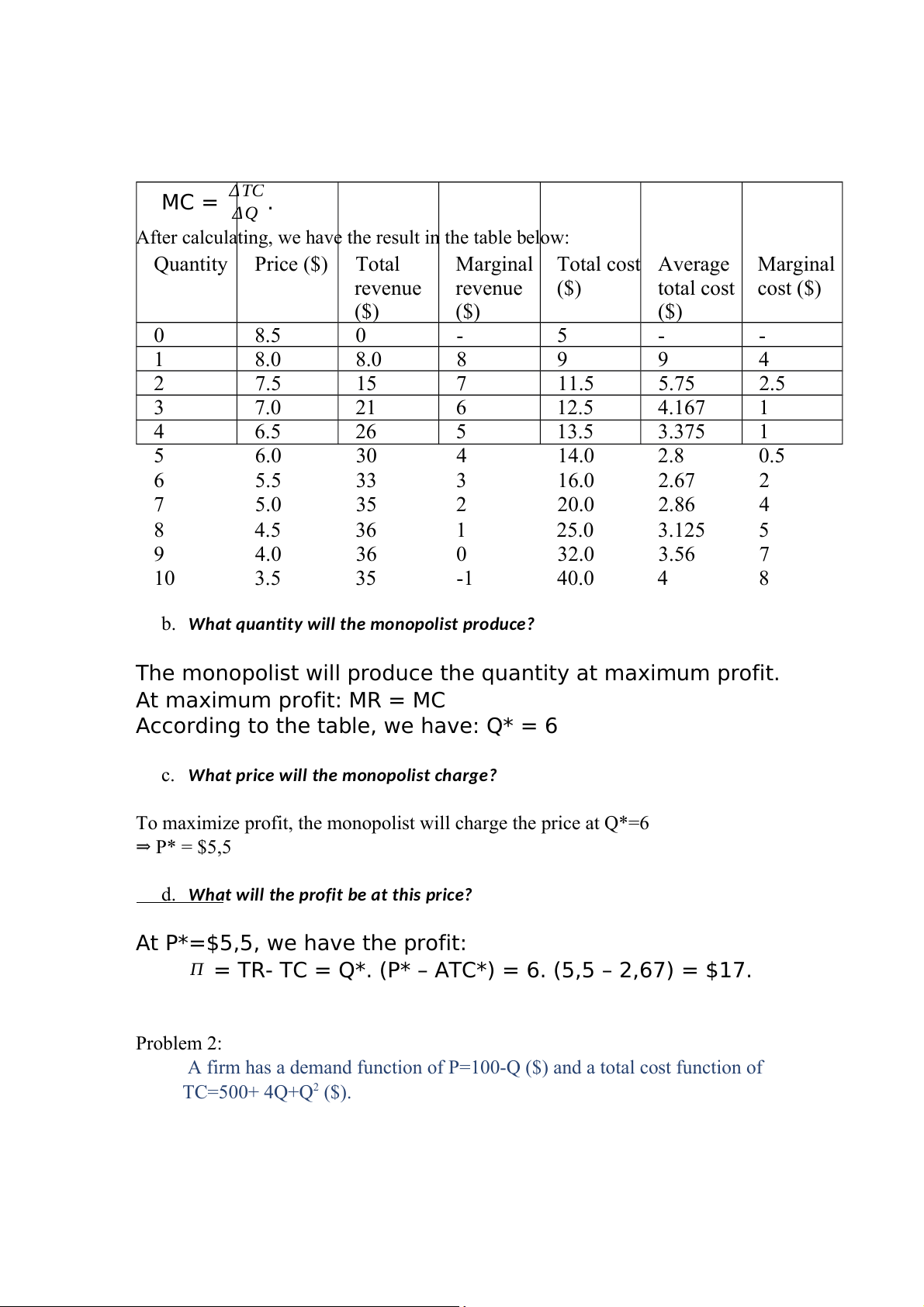

After calculating, we have the result in the table below: Quantity Price ($) Total Marginal Total cost Average Marginal revenue revenue ($) total cost cost ($) ($) ($) ($) 0 8.5 0 - 5 - - 1 8.0 8.0 8 9 9 4 2 7.5 15 7 11.5 5.75 2.5 3 7.0 21 6 12.5 4.167 1 4 6.5 26 5 13.5 3.375 1 5 6.0 30 4 14.0 2.8 0.5 6 5.5 33 3 16.0 2.67 2 7 5.0 35 2 20.0 2.86 4 8 4.5 36 1 25.0 3.125 5 9 4.0 36 0 32.0 3.56 7 10 3.5 35 -1 40.0 4 8

b. What quantity will the monopolist produce?

The monopolist will produce the quantity at maximum profit. At maximum profit: MR = MC

According to the table, we have: Q* = 6

c. What price will the monopolist charge?

To maximize profit, the monopolist will charge the price at Q*=6 ⇒ P* = $5,5

d. What will the profit be at this price?

At P*=$5,5, we have the profit:

Π = TR- TC = Q*. (P* – ATC*) = 6. (5,5 – 2,67) = $17. Problem 2:

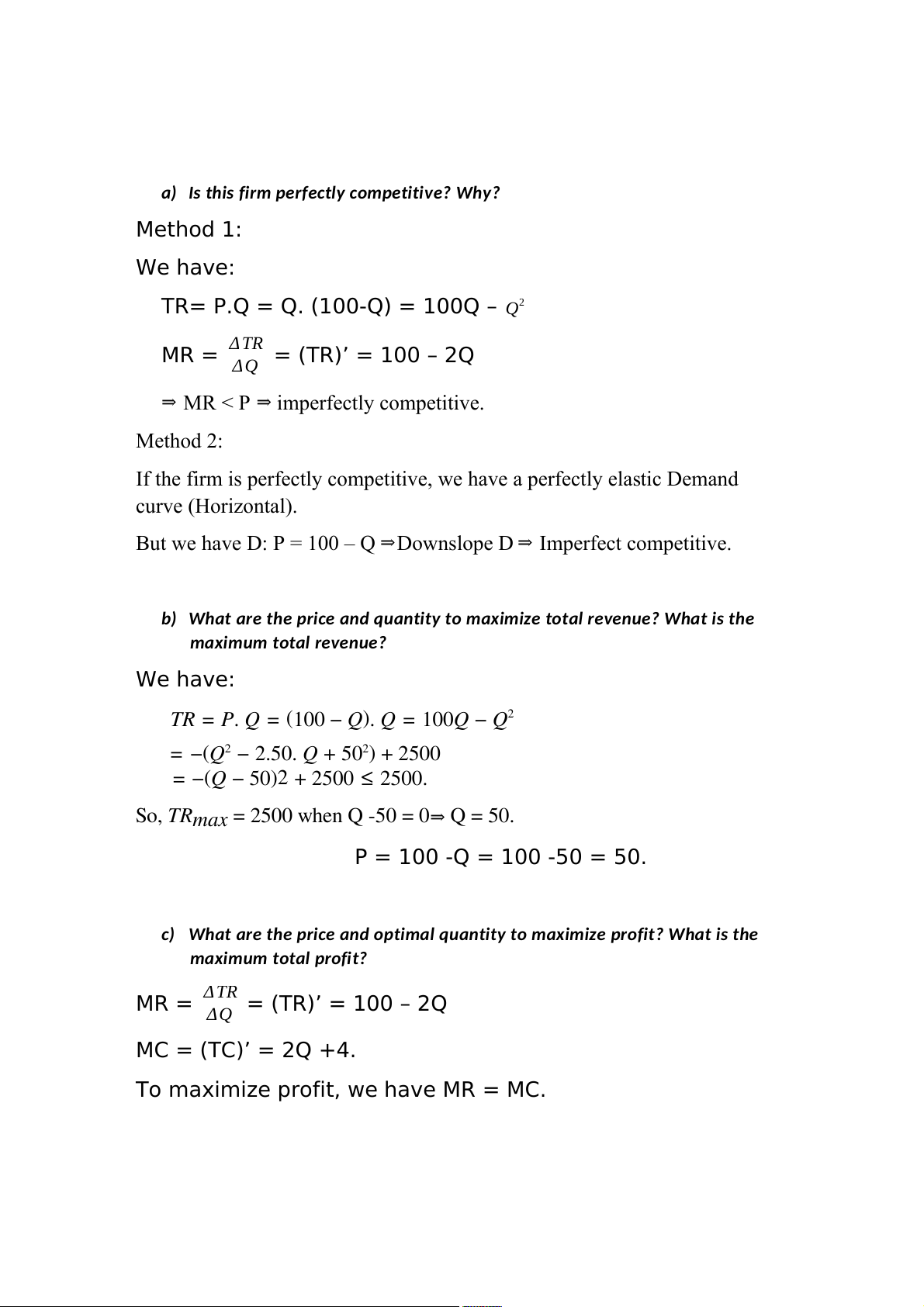

A firm has a demand function of P=100-Q ($) and a total cost function of TC=500+ 4Q+Q2 ($).

a) Is this firm perfectly competitive? Why? Method 1: We have:

TR= P.Q = Q. (100-Q) = 100Q – 2 Q Δ TR MR = = (TR)’ = 100 – 2Q Δ Q

⇒ MR < P ⇒ imperfectly competitive. Method 2:

If the firm is perfectly competitive, we have a perfectly elastic Demand curve (Horizontal).

But we have D: P = 100 – Q ⇒Downslope D ⇒ Imperfect competitive.

b) What are the price and quantity to maximize total revenue? What is the

maximum total revenue? We have:

𝑇𝑅 = 𝑃. 𝑄 = (100 − 𝑄). 𝑄 = 100𝑄 − 𝑄2

= −(𝑄2 − 2.50. 𝑄 + 502) + 2500

= −(𝑄 − 50)2 + 2500 ≤ 2500. So, 𝑇𝑅 = 2500 when Q -50 = 0 𝑚𝑎𝑥 ⇒ Q = 50. P = 100 -Q = 100 -50 = 50.

c) What are the price and optimal quantity to maximize profit? What is the

maximum total profit? Δ TR MR = = (TR)’ = 100 – 2Q Δ Q MC = (TC)’ = 2Q +4.

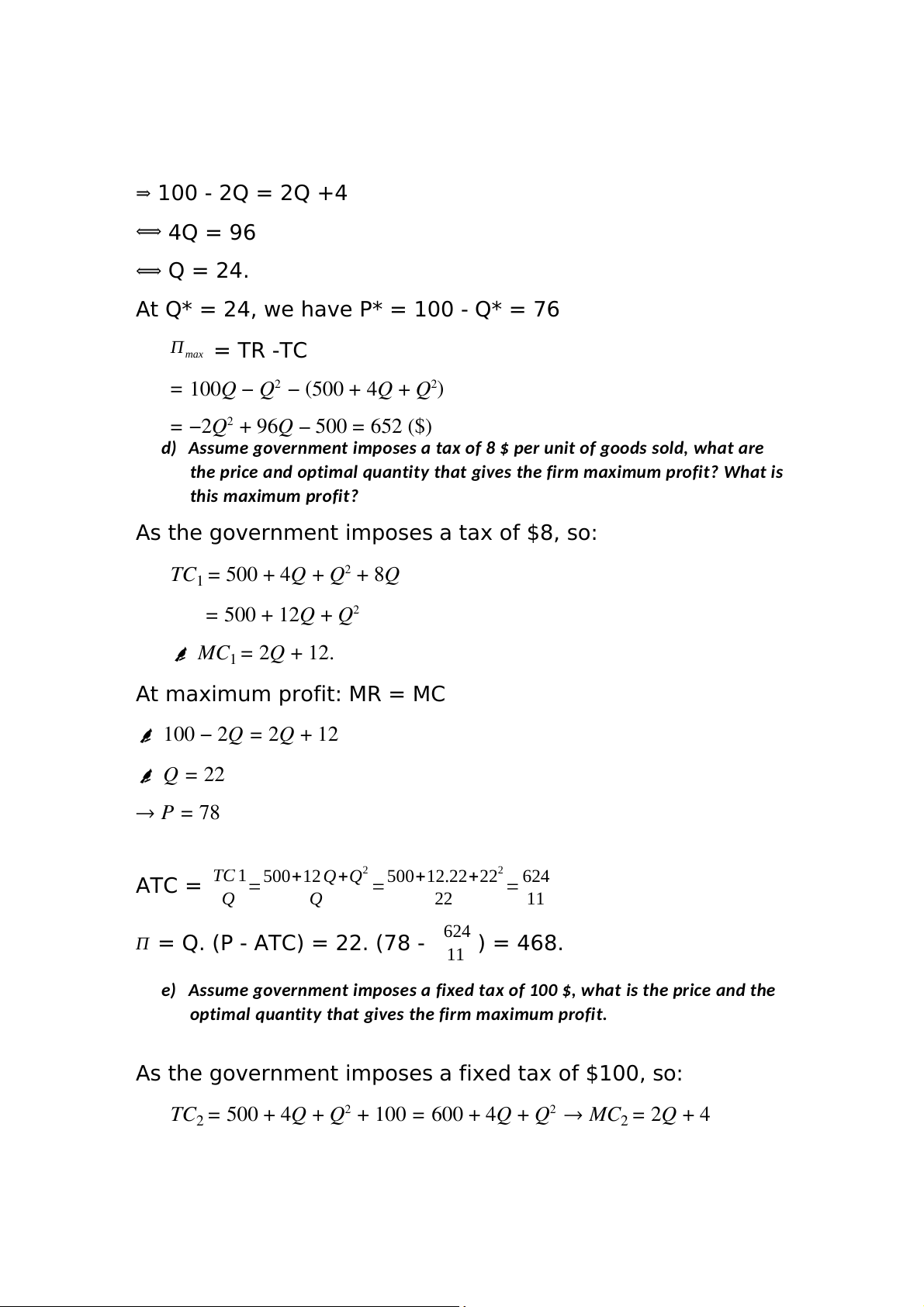

To maximize profit, we have MR = MC. ⇒ 100 - 2Q = 2Q +4 ⟺ 4Q = 96 ⟺ Q = 24.

At Q* = 24, we have P* = 100 - Q* = 76 Π max = TR -TC

= 100𝑄 − 𝑄2 − (500 + 4𝑄 + 𝑄2)

= −2𝑄2 + 96𝑄 – 500 = 652 ($)

d) Assume government imposes a tax of 8 $ per unit of goods sold, what are

the price and optimal quantity that gives the firm maximum profit? What is this maximum profit?

As the government imposes a tax of $8, so: 𝑇𝐶 2

1 = 500 + 4𝑄 + 𝑄 + 8𝑄 = 500 + 12𝑄 + 𝑄2 𝑀𝐶1 = 2𝑄 + 12. At maximum profit: MR = MC 100 − 2𝑄 = 2𝑄 + 12 𝑄 = 22 → 𝑃 = 78 TC 1 2 2 500 500 624 ATC = +12 Q+Q +12.22 22 + = = = Q Q 22 11 624

Π = Q. (P - ATC) = 22. (78 - ) = 468. 11

e) Assume government imposes a fixed tax of 100 $, what is the price and the

optimal quantity that gives the firm maximum profit.

As the government imposes a fixed tax of $100, so: 𝑇𝐶 2 2

2 = 500 + 4𝑄 + 𝑄 + 100 = 600 + 4𝑄 + 𝑄 → 𝑀𝐶 = 2𝑄 + 4 2

To maximize profit: 𝑀𝑅 = 𝑀𝐶 100 − 2𝑄 = 2𝑄 + 4 𝑄 = 24 → 𝑃 = 76

Tài liệu liên quan:

-

Chương 3: độ co giãn và các nhân tố ảnh hưởng | Microeconomics | Trường Đại học Quốc tế, Đại học Quốc gia Thành phố Hồ Chí Minh

0 0 -

Microeconomics Syllabus | Microeconomics | Trường Đại học Quốc tế, Đại học Quốc gia Thành phố Hồ Chí Minh

0 0 -

Microeconomics Course Syllabus & Assessment Details | Microeconomics | Trường Đại học Quốc tế, Đại học Quốc gia Thành phố Hồ Chí Minh

0 0 -

Assignment 3 - Elasticity MCQs and Key Concepts | Microeconomics | Trường Đại học Quốc tế, Đại học Quốc gia Thành phố Hồ Chí Minh

0 0 -

Assignment 2 - Economic Equilibrium Analysis of Fridges and Motorcycles | Microeconomics | Trường Đại học Quốc tế, Đại học Quốc gia Thành phố Hồ Chí Minh

0 0