Competitive Markets: Tutorial 5 Questions and Discussion | Microeconomics | Trường Đại học Quốc tế, Đại học Quốc gia Thành phố Hồ Chí Minh

For a firm operating in a perfectly competitive industry, total revenue, marginal revenue, and average revenue are all equal. 2. In competitive markets, firms that raise their prices are typically rewarded with larger profits. 3. A firm operating in a perfectly competitive industry will continue to operate in the short run but earn losses if the market price is less than that firm’s average total cost but greater than the. Tài liệu được sưu tầm và soạn thảo dưới dạng file PDF để gửi tới các bạn cùng tham khảo, ôn tập đầy đủ kiến thức, chuẩn bị cho các buổi học thật tốt. Mời bạn đọc đón xem!

Môn: Microeconomics 635 tài liệu

Trường: Trường Đại học Quốc tế, Đại học Quốc gia Thành phố Hồ Chí Minh 1.9 K tài liệu

Tác giả:

Preview text:

Questions for Competitive Markets

Type I: True/False question (give a brief explanation)

1. For a firm operating in a perfectly competitive industry, total revenue, marginal

revenue, and average revenue are all equal.

2. In competitive markets, firms that raise their prices are typically rewarded with larger profits.

3. A firm operating in a perfectly competitive industry will continue to operate in

the short run but earn losses if the market price is less than that firm’s average total

cost but greater than the firm’s average variable cost.

4. A firm will shut down in the short run if revenue is not sufficient to cover all of its fixed costs of production.

5. In a long-run equilibrium where firms have identical costs, it is possible that

some firms in a competitive market are making a positive economic profit.

6. All firms maximize profits by producing an output level where marginal revenue

equals marginal cost; for firms operating in perfectly competitive industries,

maximizing profits also means producing an output level where price equals marginal cost.

7. A firm operating in a perfectly competitive industry will shut down in the short

run but earn losses if the market price is less than that firm’s average variable cost.

8. In the short run, a firm should exit the industry if its marginal cost exceeds its marginal revenue.

9. The supply curve of a firm in a competitive market is the average variable cost

curve above the minimum of marginal cost.

10. The short-run supply curve in a competitive market must be more elastic than the long-run supply curve. Type II: Discussion questions

1. List and describe the characteristics of a perfectly competitive market.

2. Why would a firm in a perfectly competitive market always choose to set its

price equal to the current market price? If a firm set its price higher the current

market price, what effect would this have on the market?

3. Use a graph to demonstrate the circumstances that would prevail in a competitive

market where firms are earning economic profits. Can this scenario be maintained in

the long run? Explain your answer.

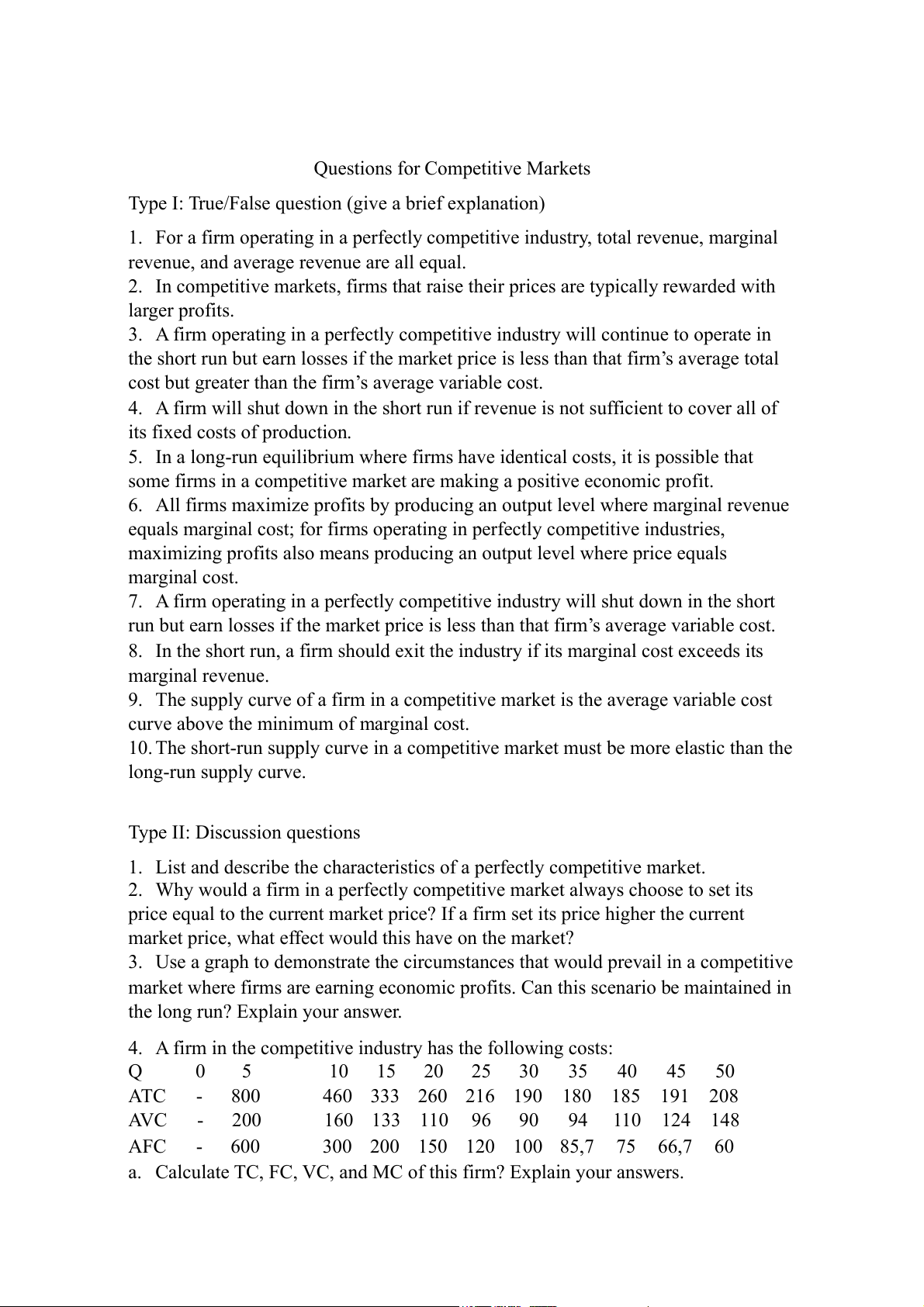

4. A firm in the competitive industry has the following costs: Q 0 5 10 15 20 25 30 35 40 45 50 ATC - 800

460 333 260 216 190 180 185 191 208 AVC - 200 160 133 110 96 90 94 110 124 148 AFC - 600 300 200 150 120 100 85,7 75 66,7 60

a. Calculate TC, FC, VC, and MC of this firm? Explain your answers.

b. At what price dose the firm have profit. Explain your answers.

c. At what price does the firm choose to shut down? Explain your answers.

d. The market price of the production is 239. What is the maximum profit quantity

for this firm? Calculate the maximum profit.

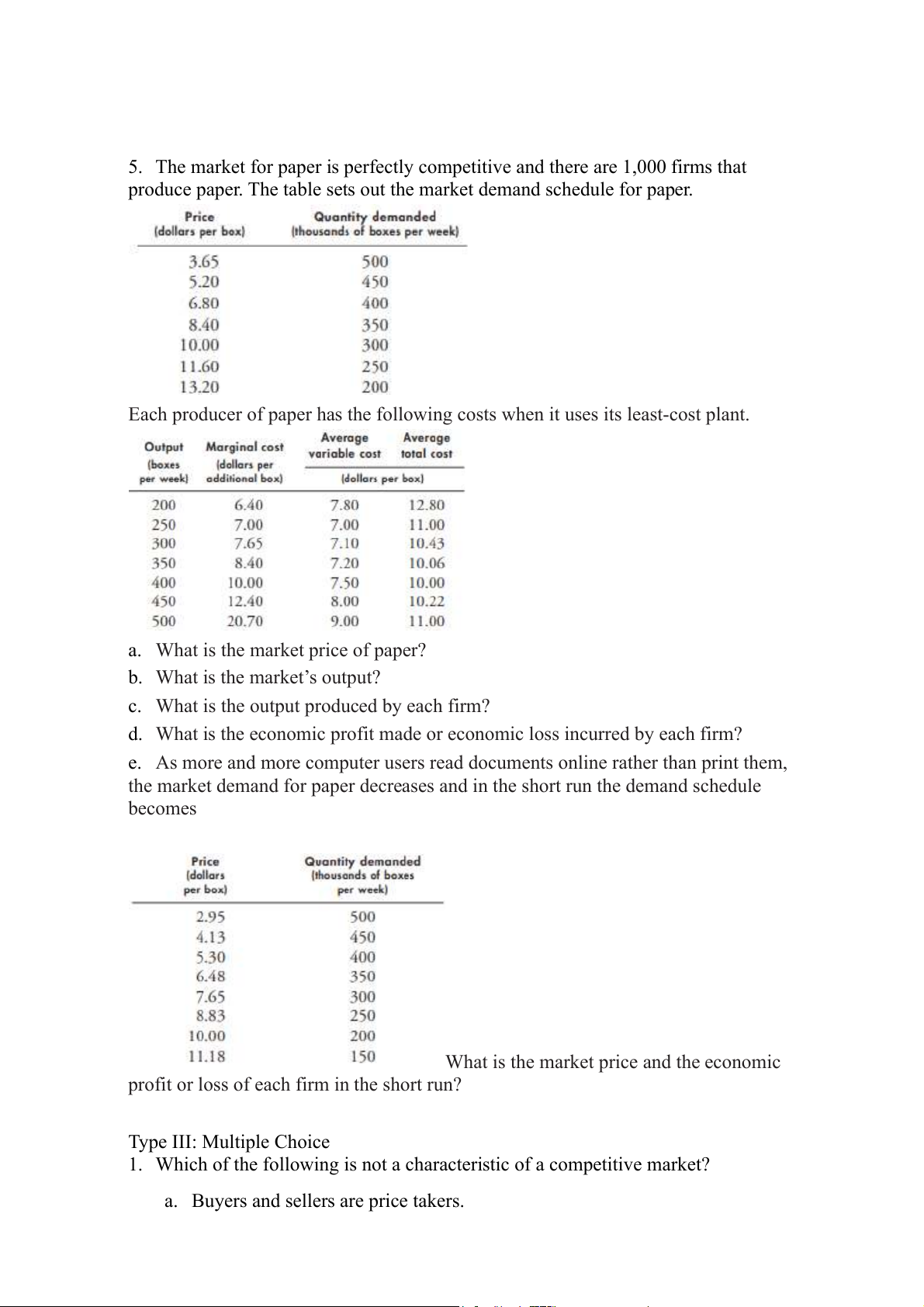

5. The market for paper is perfectly competitive and there are 1,000 firms that

produce paper. The table sets out the market demand schedule for paper.

Each producer of paper has the following costs when it uses its least-cost plant.

a. What is the market price of paper?

b. What is the market’s output?

c. What is the output produced by each firm?

d. What is the economic profit made or economic loss incurred by each firm?

e. As more and more computer users read documents online rather than print them,

the market demand for paper decreases and in the short run the demand schedule becomes

What is the market price and the economic

profit or loss of each firm in the short run? Type III: Multiple Choice

1. Which of the following is not a characteristic of a competitive market?

a. Buyers and sellers are price takers.

2. Which of the following statements best reflects a price-taking firm?

a. If the firm were to charge more than the going price, it would sell none of its goods.

b. The firm has an incentive to charge less than the market price to earn higher revenue.

c. The firm can sell only a limited amount of output at the market price before the market price will fall.

d. Price-taking firms maximize profits by charging a price above marginal cost.

3. For a firm operating in a competitive industry, which of the following statements is not correct?

a. Price equals average revenue.

b. Price equals marginal revenue. c. Total revenue is constant.

d. Marginal revenue is constant.

4. If a competitive firm is currently producing a level of output at which marginal

revenue exceeds marginal cost, then

a. a one-unit increase in output will increase the firm's profit.

b. a one-unit decrease in output will increase the firm's profit.

c. total revenue exceeds total cost.

d. total cost exceeds total revenue.

5. Hung is a gourmet chef who runs a small catering business in a competitive

industry. Hung specializes in making wedding cakes. Hung sells 20 wedding cakes

per month. His monthly total revenue is $5,000. The marginal cost of making a

wedding cake is $200. In order to maximize profits, he should

a. make more than 20 wedding cakes per month.

b. make fewer than 20 wedding cakes per month.

c. continue to make 20 wedding cakes per month.

d. We do not have enough information with which to answer the question.

6. A competitive firm has been selling its output for $20 per unit and has been

maximizing its profit, which is positive. Then, the price rises to $25, and the firm

makes whatever adjustments are necessary to maximize its profit at the now-higher

price. Once the firm has adjusted, which of the following statements is correct?

a. The firm's quantity of output is higher than it was previously.

b. The firm's average total cost is higher than it was previously.

c. The firm's marginal revenue is higher than it was previously.

d. All of the above are correct.

7. When profit-maximizing firms in competitive markets are earning profits,

a. market demand must exceed market supply at the market equilibrium price.

b. market supply must exceed market demand at the market equilibrium price.

c. new firms will enter the market.

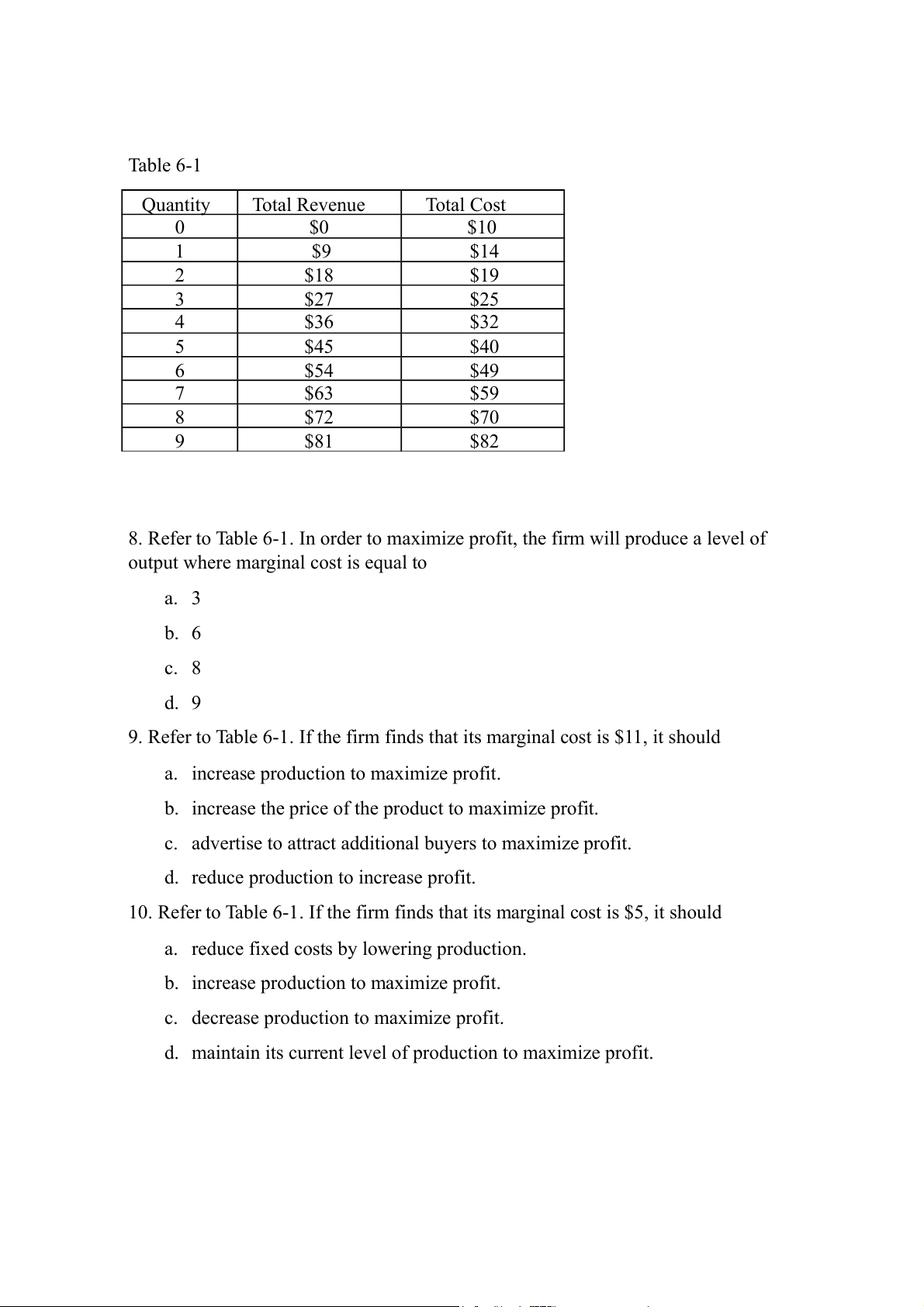

d. the most inefficient firms will be encouraged to leave the market. Table 6-1 Quantity Total Revenue Total Cost 0 $0 $10 1 $9 $14 2 $18 $19 3 $27 $25 4 $36 $32 5 $45 $40 6 $54 $49 7 $63 $59 8 $72 $70 9 $81 $82

8. Refer to Table 6-1. In order to maximize profit, the firm will produce a level of

output where marginal cost is equal to a. 3 b. 6 c. 8 d. 9

9. Refer to Table 6-1. If the firm finds that its marginal cost is $11, it should

a. increase production to maximize profit.

b. increase the price of the product to maximize profit.

c. advertise to attract additional buyers to maximize profit.

d. reduce production to increase profit.

10. Refer to Table 6-1. If the firm finds that its marginal cost is $5, it should

a. reduce fixed costs by lowering production.

b. increase production to maximize profit.

c. decrease production to maximize profit.

d. maintain its current level of production to maximize profit.

11. Why does a firm in a competitive industry charge the market price?

a. If a firm charges less than the market price, it loses potential revenue.

b. If a firm charges more than the market price, it loses all its customers to other firms.

c. The firm can sell as many units of output as it want to at the market price.

d. All of the above are correct.

12. A competitive firm would benefit from charging a price below the market price

because the firm would achieve a. higher average revenue. b. higher profits. c. lower total costs.

d. None of the above is correct.

13. Which of the following statements regarding a competitive market is not correct?

a. There are many buyers and many sellers in the market.

b. Firms can freely enter or exit the market.

c. Price equals average revenue.

d. Price exceeds marginal revenue.

14. Which of the following statements is correct?

a. For all firms, marginal revenue equals the price of the good.

b. Only for competitive firms does average revenue equal the price of the good.

c. Marginal revenue can be calculated as total revenue divided by the quantity sold.

d. Only for competitive firms does average revenue equal marginal revenue.

15. If a firm in a perfectly competitive market triples the number of units of output sold, then total revenue will a. more than triple. b. less than triple. c. exactly triple.

d. Any of the above may be true depending on the firm’s labor productivity.

16. Which of the following statements best expresses a firm’s profit-maximizing decision rule?

a. If marginal revenue is greater than marginal cost, the firm should increase its output.

b. If marginal revenue is less than marginal cost, the firm should decrease its output.

c. If marginal revenue equals marginal cost, the firm should continue

producing its current level of output.

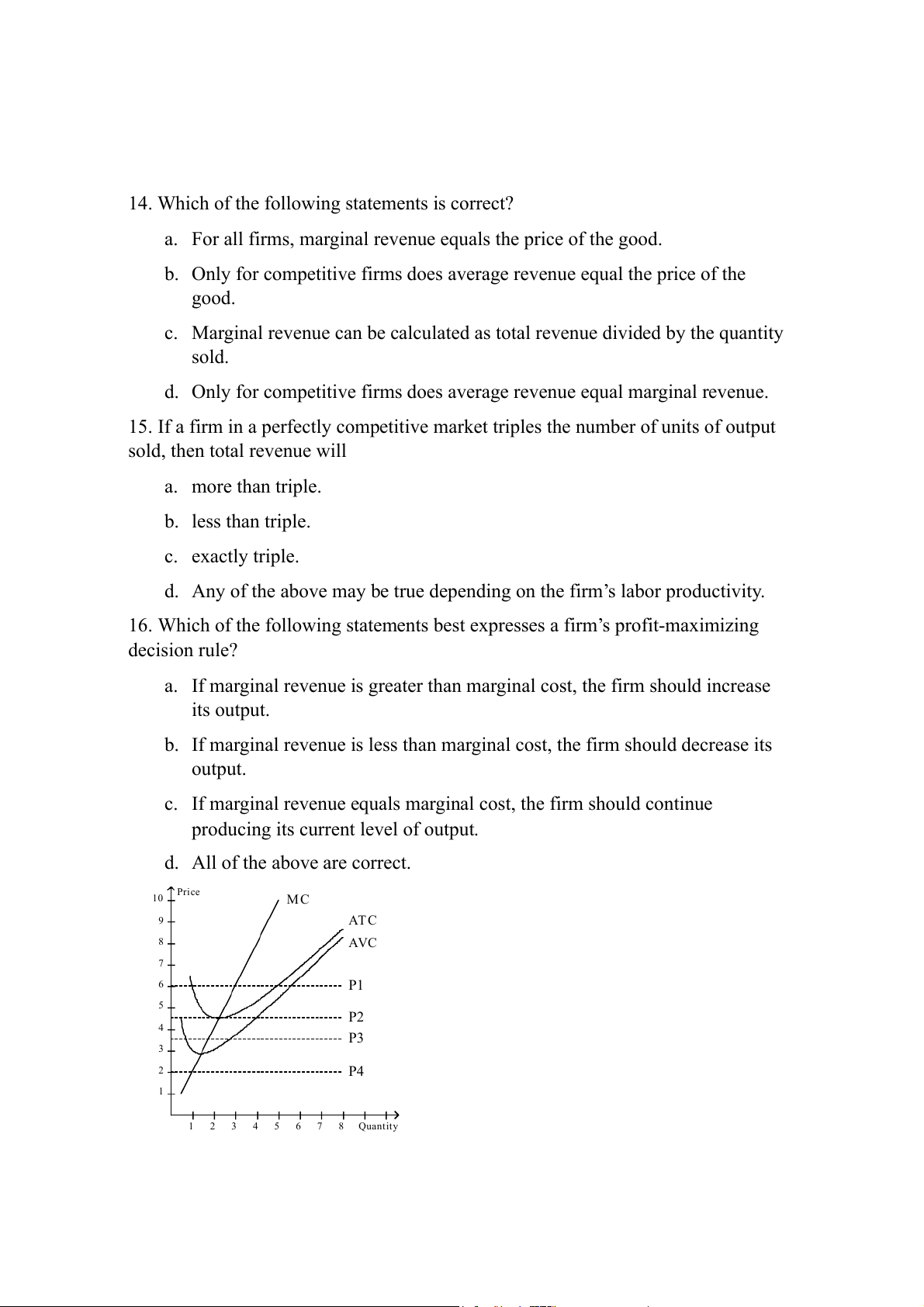

d. All of the above are correct. Price 10 MC 9 ATC 8 AVC 7 6 P1 5 P2 4 P3 3 2 P4 1 1 2 3 4 5 6 7 8 Quantity

17. Refer to Figure. If the market price is P1, in the short run, the perfectly competitive firm will earn a. positive economic profits.

b. negative economic profits but will try to remain open.

c. negative economic profits and will shut down. d. zero economic profits.

18. Refer to Figure. If the market price is P4, in the short run, the perfectly competitive firm will earn a. positive economic profits.

b. negative economic profits but will try to remain open.

c. negative economic profits and will shut down. d. zero economic profits.

19. Refer to Figure. Which of the four prices corresponds to a perfectly

competitive firm earning negative economic profits in the short run but trying to remain open? a. P1 b. P2 c. P3 d. P4

Tài liệu liên quan:

-

Chương 3: độ co giãn và các nhân tố ảnh hưởng | Microeconomics | Trường Đại học Quốc tế, Đại học Quốc gia Thành phố Hồ Chí Minh

5 3 -

Microeconomics Syllabus | Microeconomics | Trường Đại học Quốc tế, Đại học Quốc gia Thành phố Hồ Chí Minh

5 3 -

Microeconomics Course Syllabus & Assessment Details | Microeconomics | Trường Đại học Quốc tế, Đại học Quốc gia Thành phố Hồ Chí Minh

5 3 -

Assignment 3 - Elasticity MCQs and Key Concepts | Microeconomics | Trường Đại học Quốc tế, Đại học Quốc gia Thành phố Hồ Chí Minh

5 3 -

Assignment 2 - Economic Equilibrium Analysis of Fridges and Motorcycles | Microeconomics | Trường Đại học Quốc tế, Đại học Quốc gia Thành phố Hồ Chí Minh

5 3