Group Assignment Presentation 8 on Monopoly Analysis | Microeconomics | Trường Đại học Quốc tế, Đại học Quốc gia Thành phố Hồ Chí Minh

Assume government imposes a tax of $8 per unit of good sold, what is price and optimal quantity that gives the firm maximum profit? What is this maximum profit? After government imposes a tax of $8 per unit of good sold, we have: TC’ = 500 + 4Q + Q + 8Q = 500 + 12Q + Q. Tài liệu được sưu tầm và soạn thảo dưới dạng file PDF để gửi tới các bạn cùng tham khảo, ôn tập đầy đủ kiến thức, chuẩn bị cho các buổi học thật tốt. Mời bạn đọc đón xem!

Môn: Microeconomics 635 tài liệu

Trường: Trường Đại học Quốc tế, Đại học Quốc gia Thành phố Hồ Chí Minh 1.9 K tài liệu

Tác giả:

Preview text:

Group assignment presentation 8

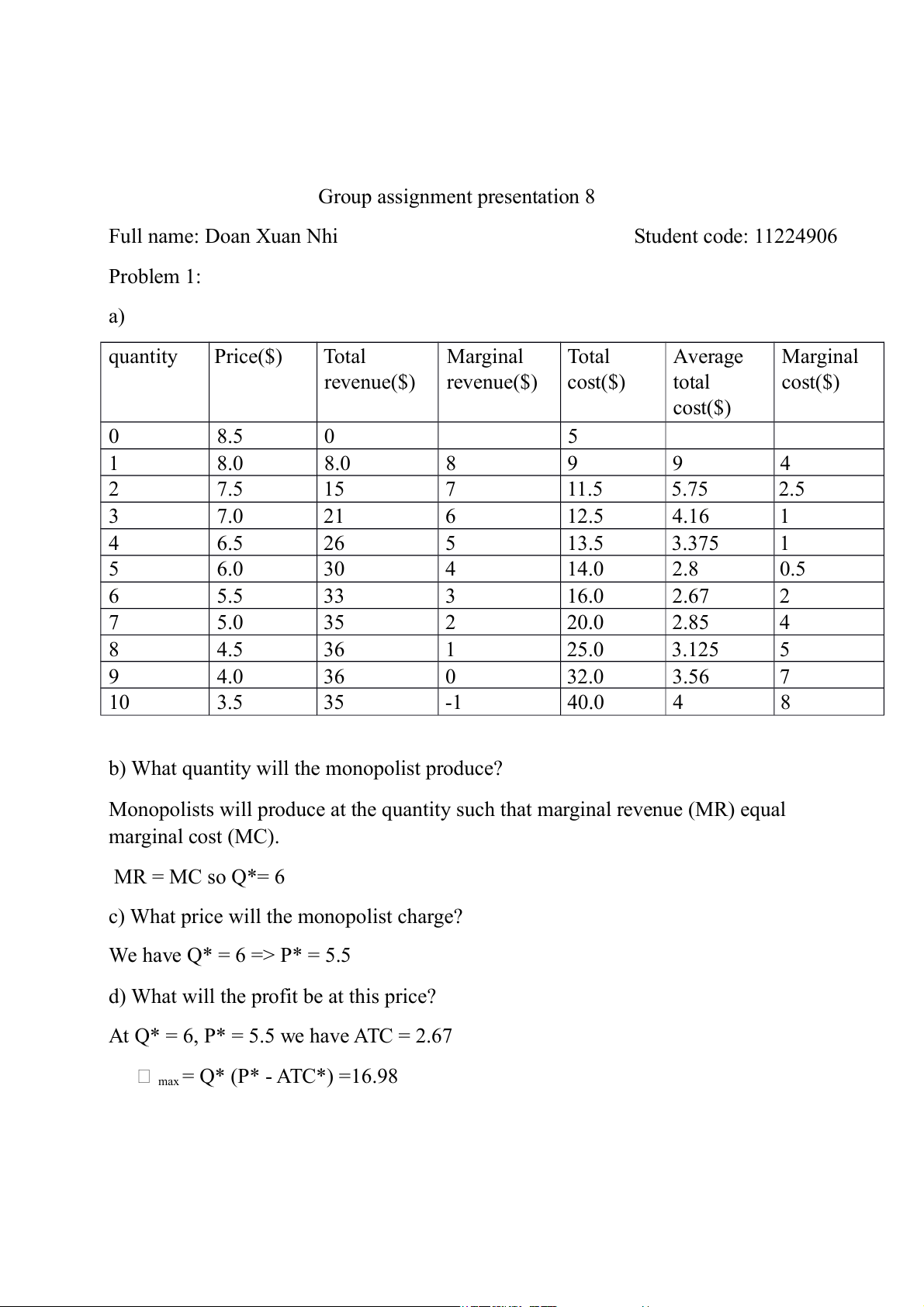

Full name: Doan Xuan Nhi Student code: 11224906 Problem 1: a) quantity Price($) Total Marginal Total Average Marginal revenue($) revenue($) cost($) total cost($) cost($) 0 8.5 0 5 1 8.0 8.0 8 9 9 4 2 7.5 15 7 11.5 5.75 2.5 3 7.0 21 6 12.5 4.16 1 4 6.5 26 5 13.5 3.375 1 5 6.0 30 4 14.0 2.8 0.5 6 5.5 33 3 16.0 2.67 2 7 5.0 35 2 20.0 2.85 4 8 4.5 36 1 25.0 3.125 5 9 4.0 36 0 32.0 3.56 7 10 3.5 35 -1 40.0 4 8

b) What quantity will the monopolist produce?

Monopolists will produce at the quantity such that marginal revenue (MR) equal marginal cost (MC). MR = MC so Q*= 6

c) What price will the monopolist charge? We have Q* = 6 => P* = 5.5

d) What will the profit be at this price?

At Q* = 6, P* = 5.5 we have ATC = 2.67 max = Q* (P* - ATC*) =16.98 Problem 2:

A firm has demand function of P = 100 – Q ($) and total cost function of TC = 500 + 4Q + Q2 ($)

a) Is this firm a perfect competitive firm? Why?

This firm is not a perfect competitive firm. Because if the firm is perfect

competition, D will be perfect elastic. But D in this situation is P = 100 – Q, D is slope down. This firm is a monopoly firm.

b) What is price and quantity to maximize total revenue? What is that maximum total revenue? TR = P.Q = 100Q – Q2 Total revenue max when: (TR)’ = 0 100 – 2Q =0 Q = 50 P = 100 – 50 =50 TRmax = P.Q = 2500

c) What is price and optimal quantity to maximize profit? What is that maximum total profit? MR = (TR)’ = 100 - 2Q MC = (TC)’ = 4 + 2Q To maximize profit: MR = MC 100 – 2Q = 4 + 2Q Q = 24 P = 76 ATC = = + 4 +Q Q = 24 => ATC = 48.83 max = Q* (P* - ATC*) = 652

d) Assume government imposes a tax of $8 per unit of good sold, what is price

and optimal quantity that gives the firm maximum profit? What is this maximum profit?

After government imposes a tax of $8 per unit of good sold, we have:

TC’ = 500 + 4Q + Q2 + 8Q = 500 + 12Q + Q2 MC’ = 12 + 2Q To maximize profit: MC’ = MR 12 + 2Q = 100 – 2Q Q = 22 P = 100 – 22 = 78 ATC = + 12 +Q = 56.72 max = Q* (P* - ATC*) = 468

e) Assume government imposes a fixed tax of $100, what is price and optimal

quantity that gives the firm maximum profit?

Government imposes a fixed tax of $100, we have:

TC’’ = 500 + 4Q + Q2 + 100 = 600 + 4Q + Q2 MC’’ = 4 + 2Q To maximize profit: MC’’ = MR 4 + 2Q = 100 – 2Q Q = 24 P = 100 – 24 = 76

Tài liệu liên quan:

-

Chương 3: độ co giãn và các nhân tố ảnh hưởng | Microeconomics | Trường Đại học Quốc tế, Đại học Quốc gia Thành phố Hồ Chí Minh

3 2 -

Microeconomics Syllabus | Microeconomics | Trường Đại học Quốc tế, Đại học Quốc gia Thành phố Hồ Chí Minh

3 2 -

Microeconomics Course Syllabus & Assessment Details | Microeconomics | Trường Đại học Quốc tế, Đại học Quốc gia Thành phố Hồ Chí Minh

3 2 -

Assignment 3 - Elasticity MCQs and Key Concepts | Microeconomics | Trường Đại học Quốc tế, Đại học Quốc gia Thành phố Hồ Chí Minh

3 2 -

Assignment 2 - Economic Equilibrium Analysis of Fridges and Motorcycles | Microeconomics | Trường Đại học Quốc tế, Đại học Quốc gia Thành phố Hồ Chí Minh

3 2