Midterm Notes: Hypothesis Testing & Regression Analysis | Môn Econometrics with Financial Application - Trường Đại học Quốc tế, Đại học Quốc gia Thành phố Hồ Chí Minh

Midterm Notes: Hypothesis Testing & Regression Analysis Môn Econometrics with Financial Application. Tài liệu được sưu tầm gồm 27 trang, giúp bạn ôn tập tốt hơn. Mời các bạn đón xem.

Môn: Econometrics with Financial Application (BA174IU) 10 tài liệu

Trường: Trường Đại học Quốc tế, Đại học Quốc gia Thành phố Hồ Chí Minh 2 K tài liệu

Tác giả:

Preview text:

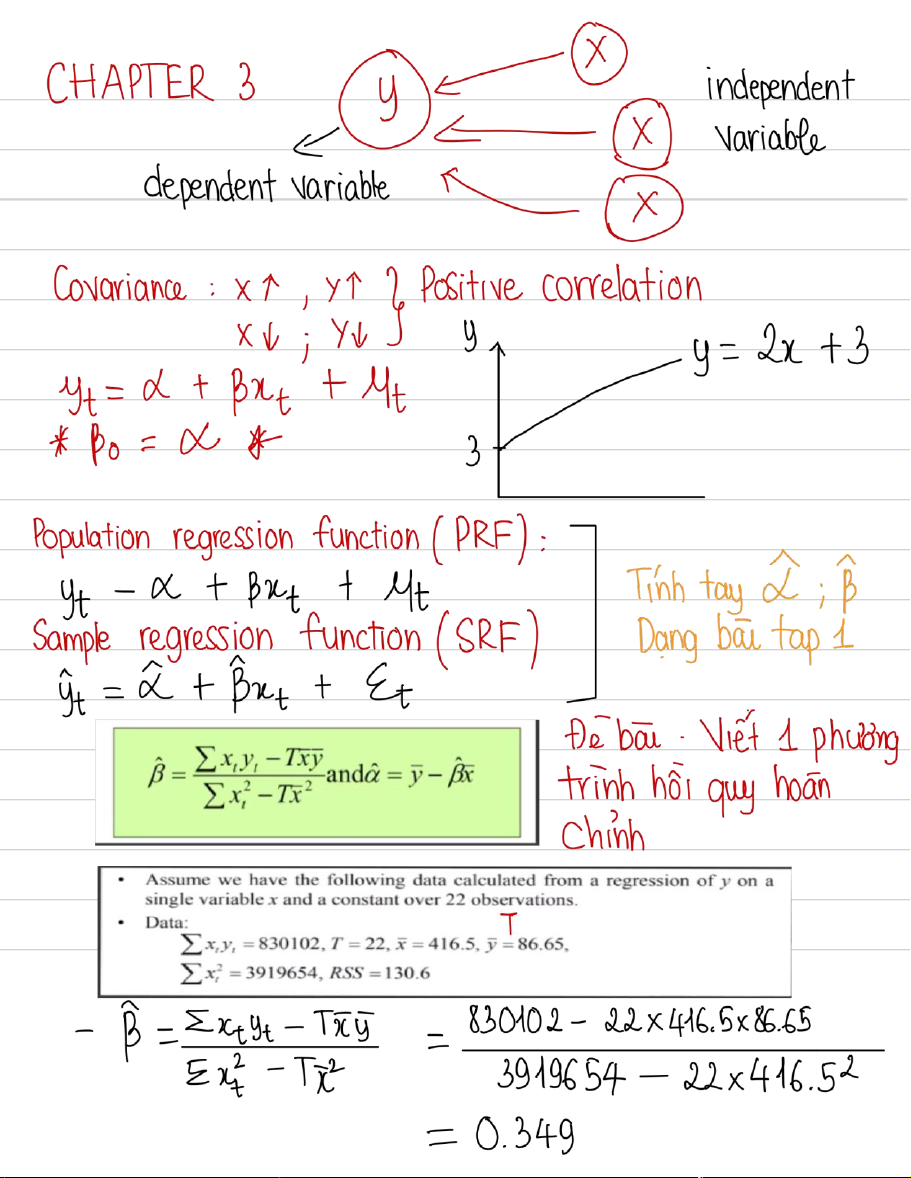

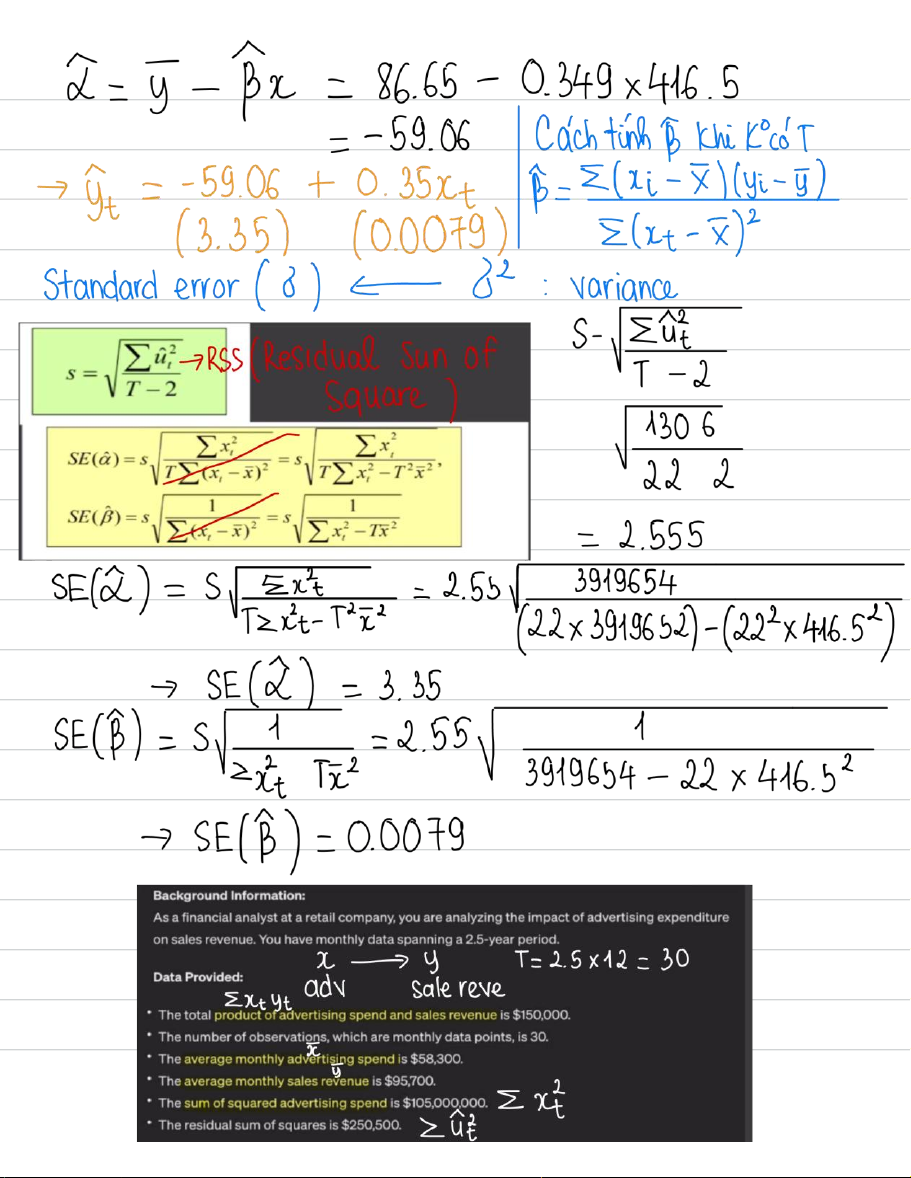

lOMoAR cPSD| 58583460 CHAP3 AND CHAP 4 Br : y = + Baxy (regression CHAP 3 : QMF QM : Normal distribution - M4B : equation : y = 2 x + 3 - .

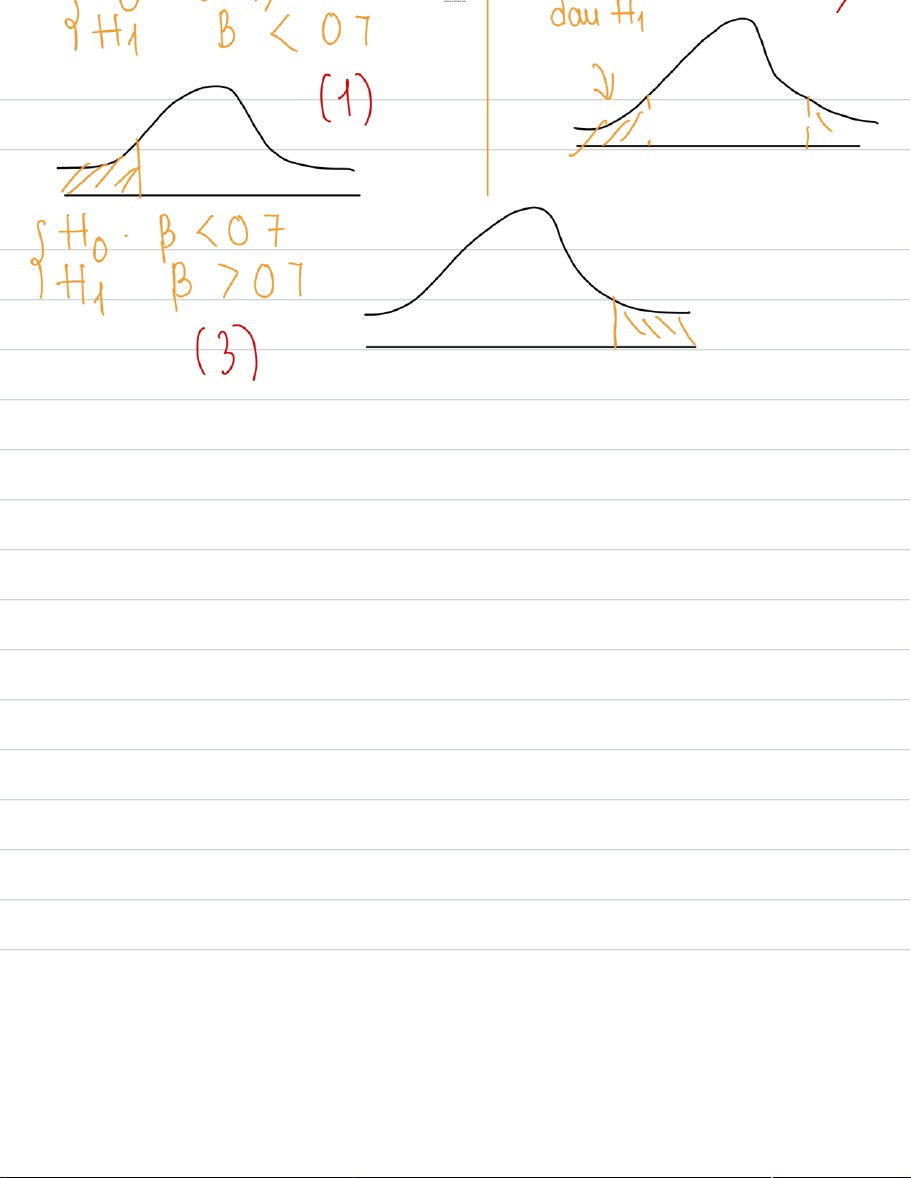

>x = 1 >y = 5 Khi tang 1vi>x = 2 - y = 7 thiy tang 2 vi - - - > x = 3 > y - - = 9 Stat S : Hypothesis testing : Salary = By x grade y = ax + b => Salary $0 = 7 x grade + 10 M . + rade = 0 - 10M : radg = 1 + 10M +$07 . Ho B 07

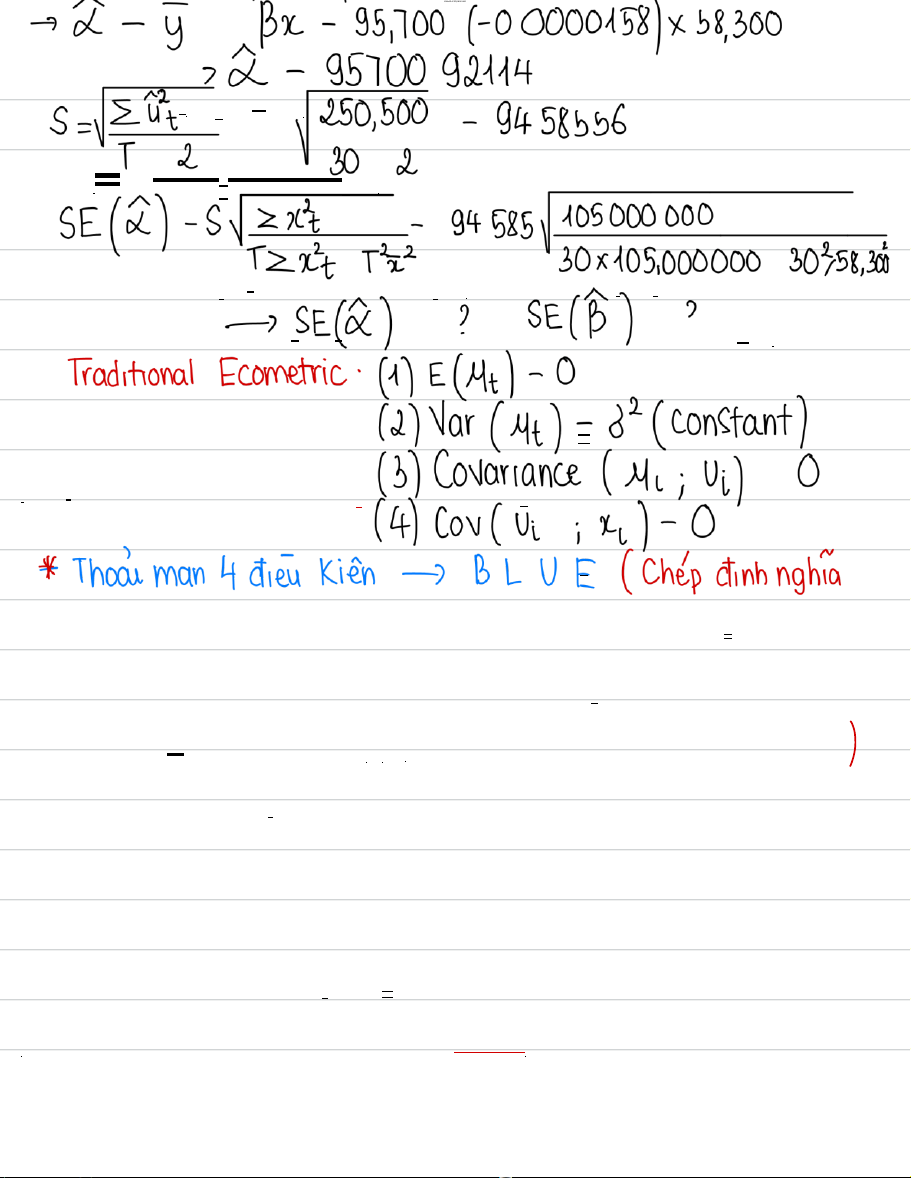

Sto : nulhypothesothesis SHe B :+ : 0 7 = .. ST : B dont (2) lOMoAR cPSD| 58583460 -/ in lOMoAR cPSD| 58583460 S :B07 - /W (3) lOMoAR cPSD| 58583460 lOMoAR cPSD| 58583460 lOMoAR cPSD| 58583460 B > = [14y+ Tiy = 150, 000 30x58 300x95, 700 - - - . IKE Th 105 000 30 3002 - , , 0002 - x 58 . 3 0 0000158 -> = - . - y Bi 1 0000158)x58 = 95 300 = ,700 0 . - - - . lOMoAR cPSD| 58583460 SZit > 2 92114 - = 95700 . /250,500 = 945855 = . SE(X) 5851105 =S, IxE ?= 94 , 000, 000 . TIIt - Th 30x105 000000 30258 30% , - , SE(X) > =? SE(B) =? - Traditional Ecometric (1) E(Mt) - : = 0 (2) Var (Mt) 82 = (constant) (3) Covariance (Mi ; Vi) = 0 (4) (ov(ui = xi) = 0

* Thoai man 4 din Kien >B L U E (Chep dinnnghia - . . . + Best OLS : ordinary least square + Linear + Unbased + Estimator (B , : = X ; B) + Step 2 Dang Hypothesis Testing : - - lOMoAR cPSD| 58583460 + Step 1 :

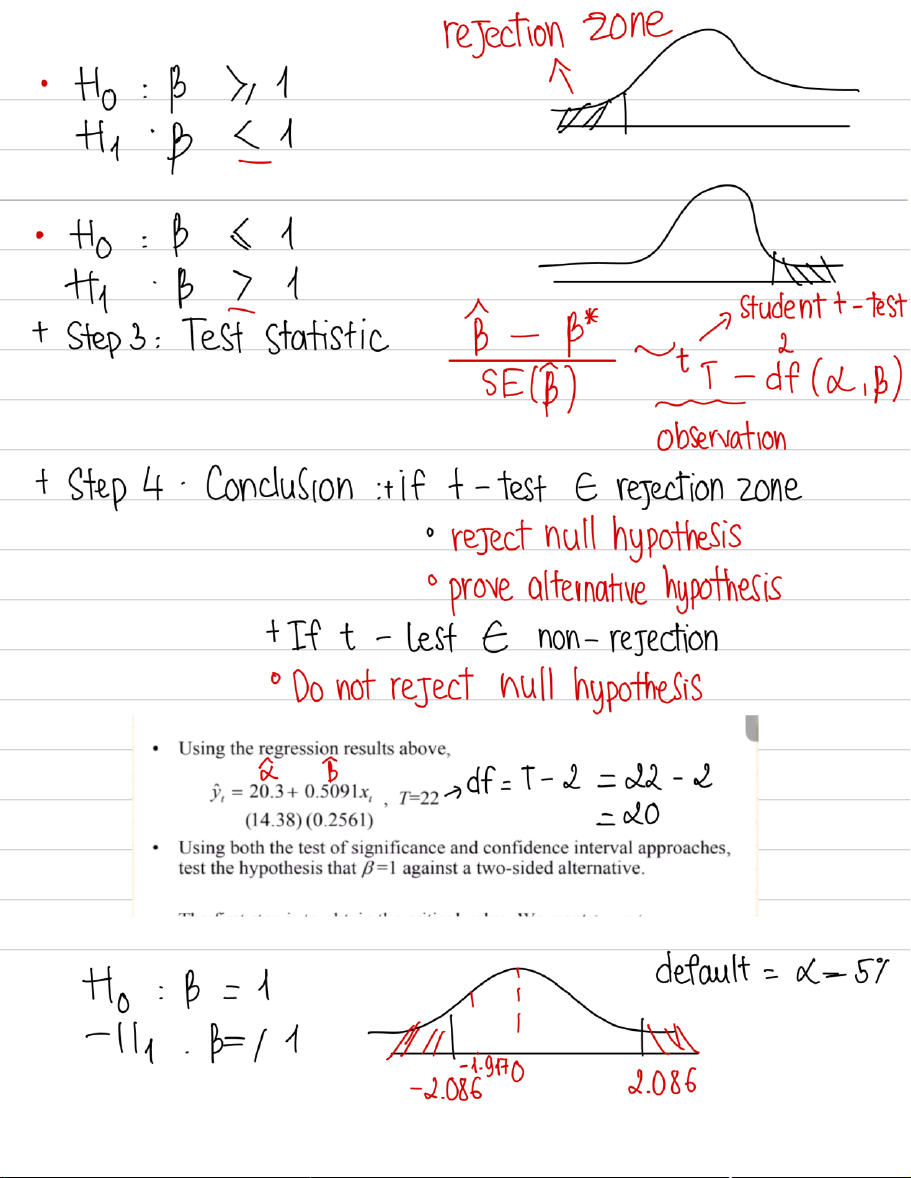

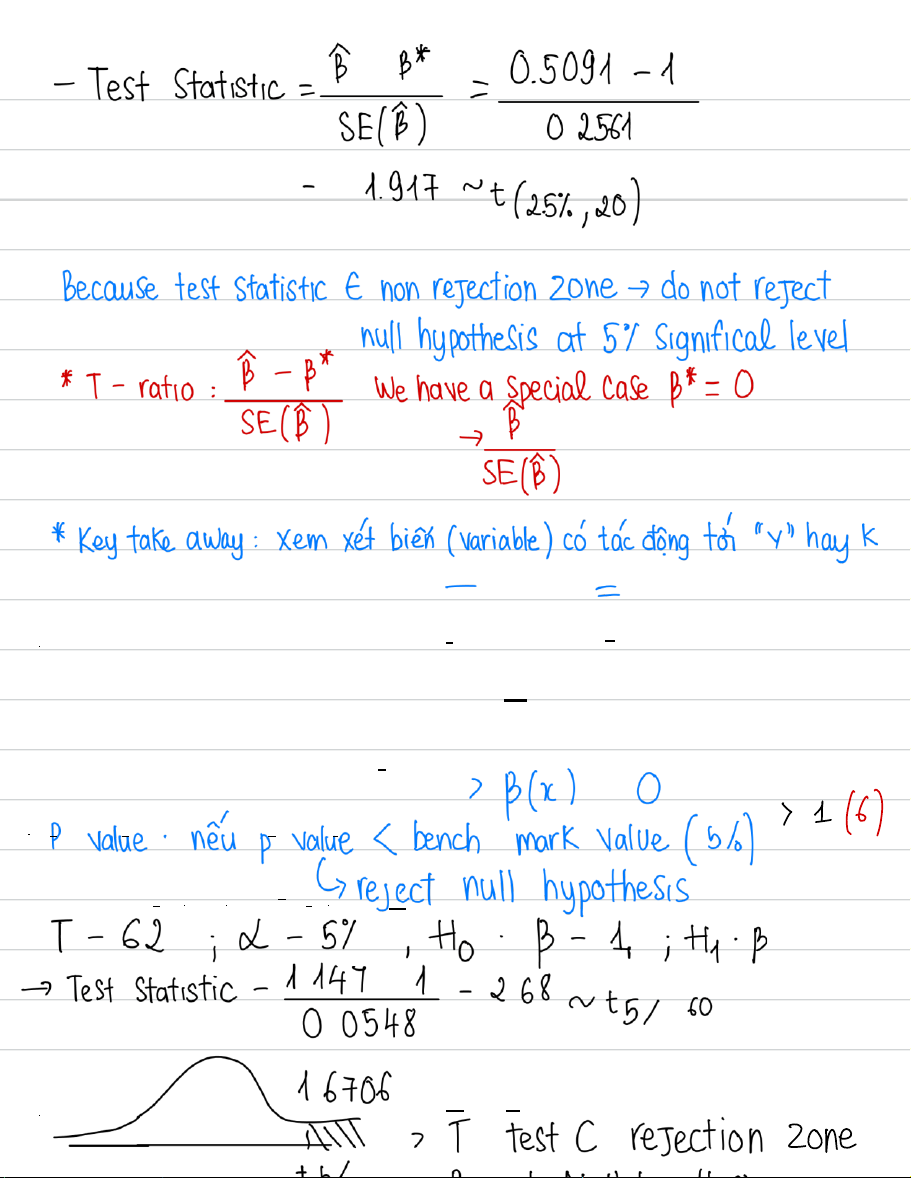

State the hypothesis· Ho:B = 0 (4(-X lOMoAR cPSD| 58583460 (xacinh) H : B + 0 lOMoAR cPSD| 58583460 lOMoAR cPSD| 58583460 new P-value p-value < bench-mark - : value (5%) ↳ reject null hypothesis T B 1 ; + B < 1(6) · = 62 ; < = 5%; Ho : = :

> Test Statistic = 101470548-1 68 ~ +5%:60 - = 2 . . . T-test - rejection zone - lOMoAR cPSD| 58583460 5% >- Reject Nullhypothesis >Prove alternative hypothesis - B7 1

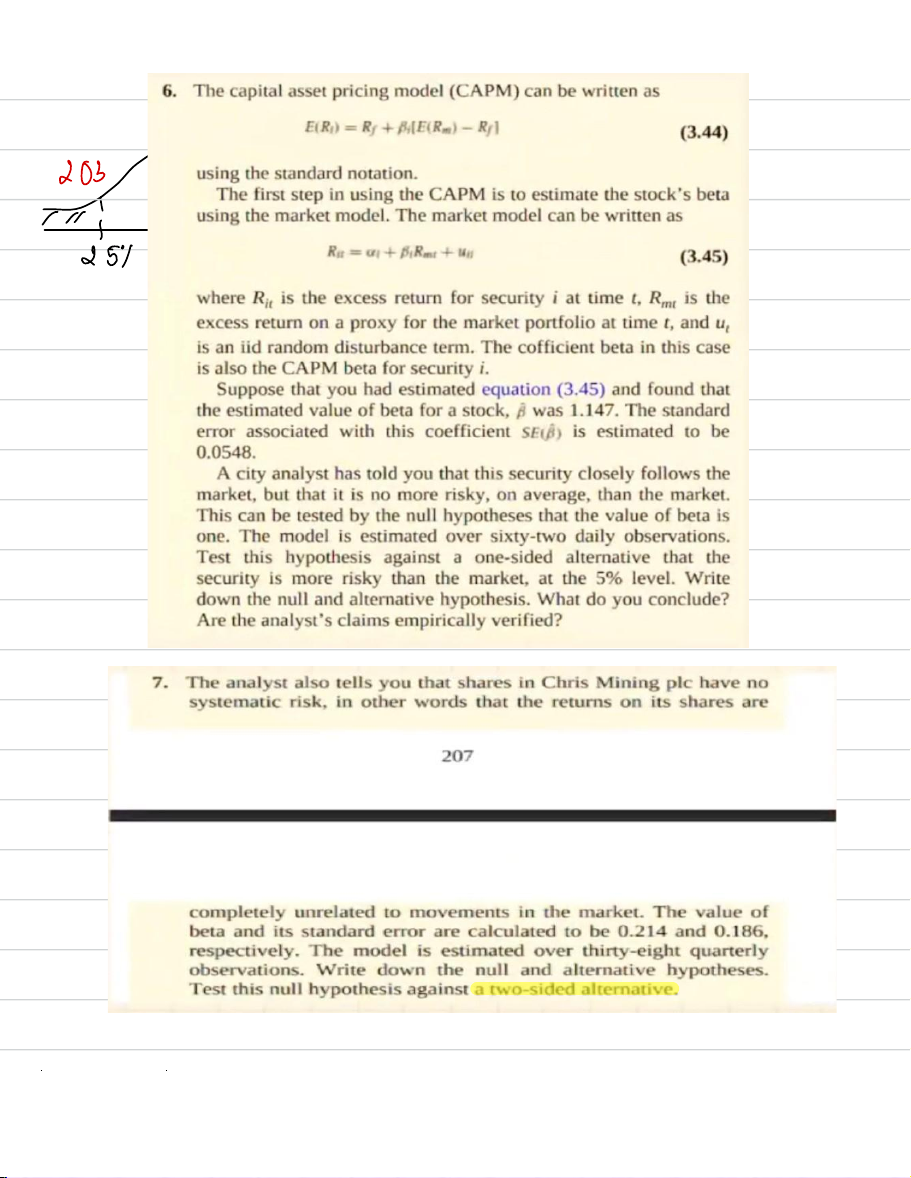

> TheSecurity is more risky than market. - Ho B : = 0 He B : + 0 lOMoAR cPSD| 58583460 ente203 · . lOMoAR cPSD| 58583460 - 5% i n 5 - +2 % . 1 . null hypothesis

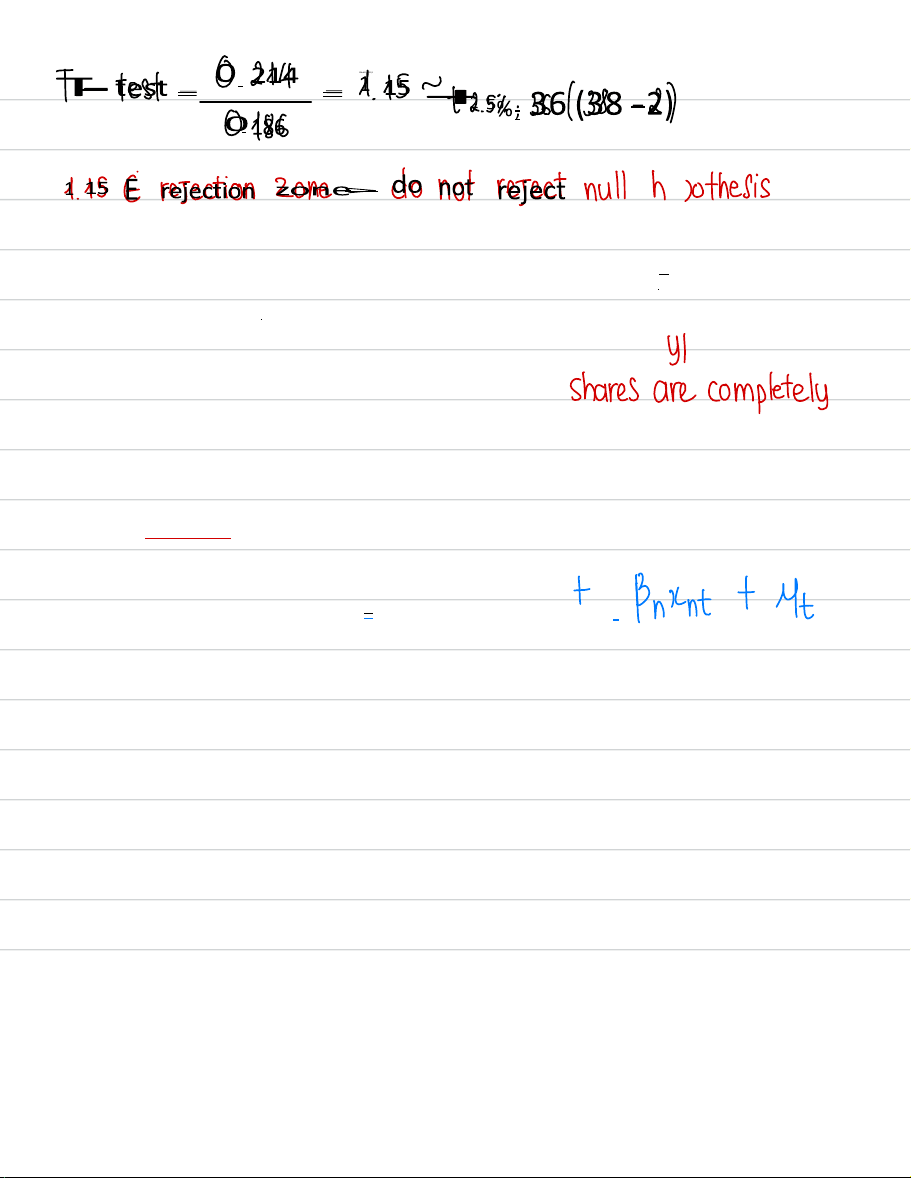

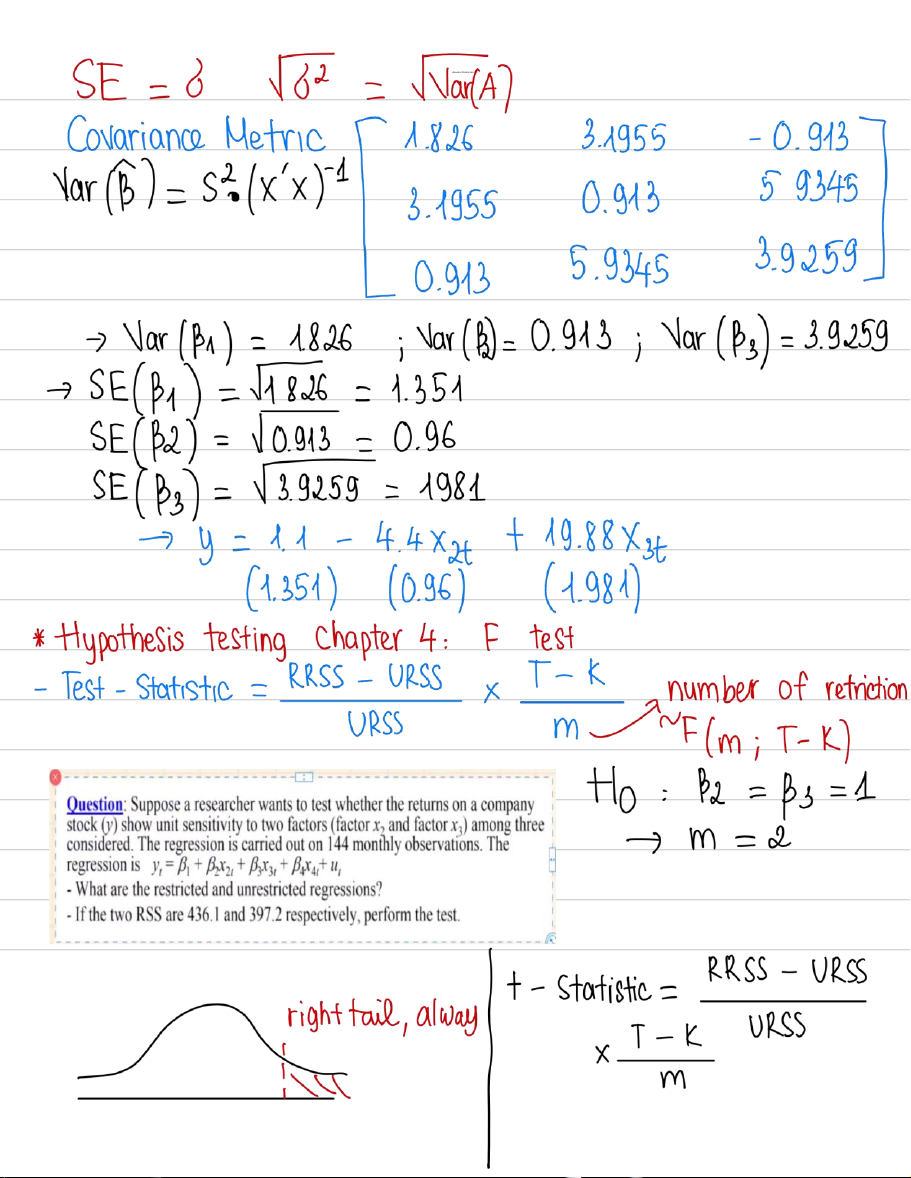

>In other words that the returns on its shares are completely unrelated to - movements in the market. CHAPTER 4 : Multiple linear regression y B =

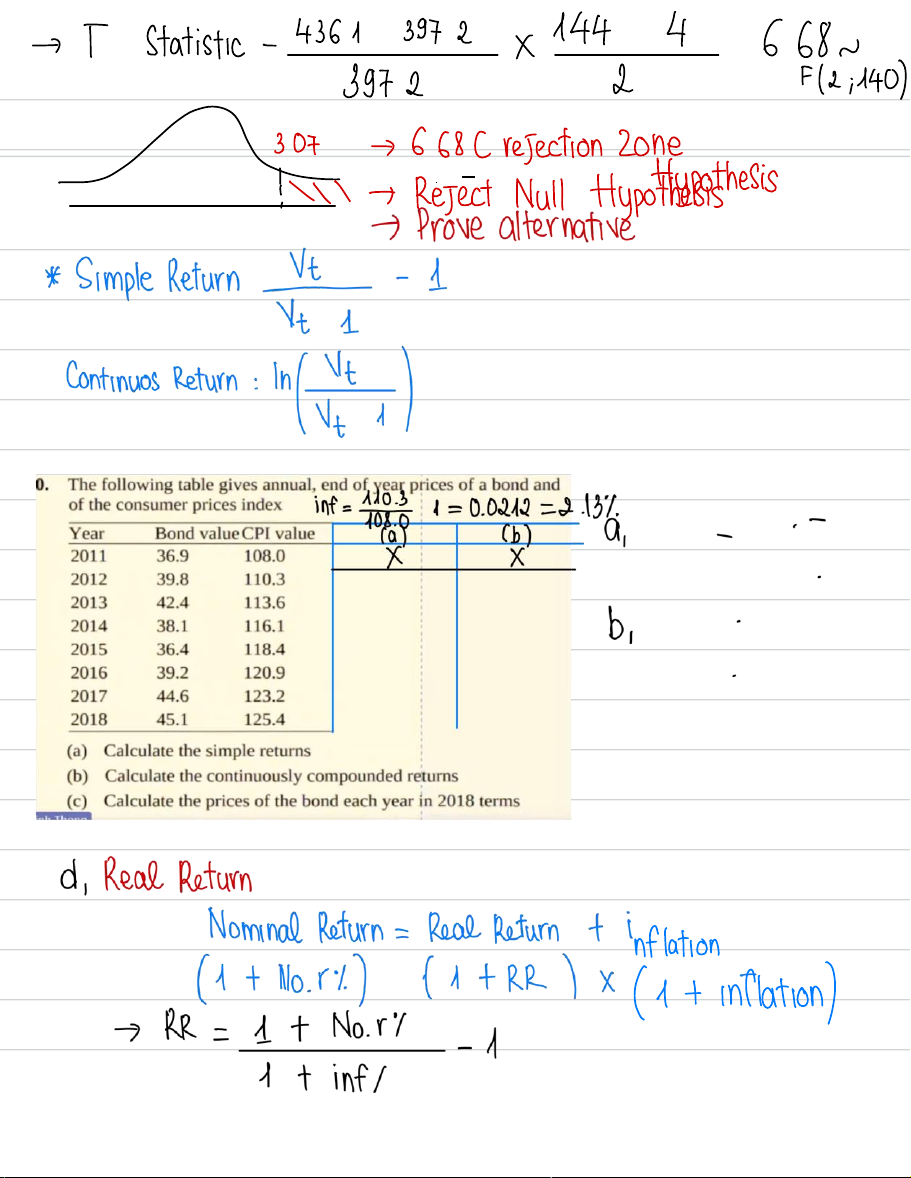

+ B2x2t + Bxt +... + Brint + Mt lOMoAR cPSD| 58583460 : CT [B] 1 XY = (xX) - x lOMoAR cPSD| 58583460 lOMoAR cPSD| 58583460 > T-Statistic 4 6 68 = 436 1 - 397 2 x 144 = - . . - . lOMoAR cPSD| 58583460 397 2 2 F(2 ; 140) . lOMoAR cPSD| 58583460 -3.07 >6 68t rejection Zone - . lOMoAR cPSD| 58583460

Tài liệu liên quan:

-

Econ Review: Probability & Inference Concepts | Môn Econometrics with Financial Application - Trường Đại học Quốc tế, Đại học Quốc gia Thành phố Hồ Chí Minh

91 46 -

Final Report on January Effect in Vietnam Stock Market | Môn Econometrics with Financial Application - Trường Đại học Quốc tế, Đại học Quốc gia Thành phố Hồ Chí Minh

120 60 -

Chapter 5 Eco Solutions: Addressing Methodological Challenges in Regression Analysis | Môn Econometrics with Financial Application - Trường Đại học Quốc tế, Đại học Quốc gia Thành phố Hồ Chí Minh

118 59 -

Syllabus: Econometrics with Financial Applications 2025 | Môn Econometrics with Financial Application - Trường Đại học Quốc tế, Đại học Quốc gia Thành phố Hồ Chí Minh

185 93