Multiple Choice & True/False Questions | Microeconomics | Trường Đại học Quốc tế, Đại học Quốc gia Thành phố Hồ Chí Minh

Choose ONLY ONE best answer for each of the lowing questions ( 0.25 mark/question) QUESTION 1 The economising problem is essentially one of deciding how to make the best use of: A: virtually unlimited resources, to satisfy virtually unlimited wants. B: limited resources, to satisfy virtually unlimited wants. C: unlimited resources, to satisfy limited wants. D: limited resources, to satisfy limited wants. QUESTION 2 Production possibilities (options) Capital goods Consumer go. Tài liệu được sưu tầm và soạn thảo dưới dạng file PDF để gửi tới các bạn cùng tham khảo, ôn tập đầy đủ kiến thức, chuẩn bị cho các buổi học thật tốt. Mời bạn đọc đón xem!

Môn: Microeconomics 635 tài liệu

Trường: Trường Đại học Quốc tế, Đại học Quốc gia Thành phố Hồ Chí Minh 1.9 K tài liệu

Tác giả:

Preview text:

TEST 1.

SECTION A: MULTIPLE CHOICE QUESTIONS

Choose ONLY ONE best answer for each of the lowing questions ( 0.25 mark/question) QUESTION 1

The economising problem is essentially one of deciding how to make the best use of:

A: virtually unlimited resources, to satisfy virtually unlimited wants.

B: limited resources, to satisfy virtually unlimited wants.

C: unlimited resources, to satisfy limited wants.

D: limited resources, to satisfy limited wants. QUESTION 2

Production possibilities (options) Capital goods Consumer goods A B C D E F 5 4 3 2 1 0 0 5 9 12 14 15

Refer to the above data, if the economy is producing at production option C, the opportunity

cost of the tenth unit of consumer goods will be: A: 4 units of capital goods. B: 2 units of capital goods. C: 3 units of capital goods.

D: 𝟏/𝟑 of a unit of capital goods. QUESTION 3:

Which of the following could be expected to produce an increase in the demand for chicken

A. a reduction in the price of chicken food

B. a decrease in the price of chicken

C. an increase in the supply of chicken

D. an increase in the price of pork. QUESTION 4

If the price of K declines, the demand curve for the complementary product J will: A. shift to the left. B. decrease. C. shift to the right. D. remain unchanged. QUESTION 5

Price discounting of 3-star Hotel daily room tariffs has shown that cutting prices by 10%

leads to 12%, more rooms being booked. We can conclude that

A. demand for hotel rooms is price elastic and discounting increases revenue

B. demand for hotel rooms is price elastic and discounting reduces revenue

C. demand for hotel rooms is price inelastic and discounting increases revenue

D. demand for hotel rooms is price inelastic and discounting reduces revenue QUESTION 6

If rice demand is inelastic, a good rice harvest will cause rice growers' revenue to:

A. increase because of the increase in the quantity that farmers can sell

B. remain unchanged, because the increase in the quantity that can be sold will be matched by an equal decrease in price

C. increase because of a downward movement along the supply curve, encouraging an increase in demand

D. decrease because of a percentage fall in price greater than the percentage

increase in quantity sold QUESTION 7

The buyer' tax incidence would be higher if:

A: the price elasticity of demand is higher

𝐵 : the price elasticity of demand is lower

C : the price elasticity of demand is perfectly elastic D: None of the above QUESTION 8

Suppose that a firm's output increase from 910 to 1070 units when it increases its labour

input from 63 to 64 workers. The marginal product of the last worker is: A 1070 B. 910 C. 64 D. 160 QUESTION 9

Marginal cost may be defined as the:

A: rate of change in total fixed cost which results from producing one more unit of output.

B. change in total cost which results from producing one more unit of output.

C: change in average variable cost which results from producing one more unit of output

D: change in average total cost which results from producing one more unit of output QUESTION 10

A firm in a competitive market is producing at the level of output that maximises profit. At this output level:

A. marginal revenue equals price

B. average revenue equals marginal cost

C. marginal revenue equals marginal cost D. all the above QUESTION 11

Consider the following relationship between cost and output for a perfectly competitive firm: Total cost = $20 $30 $41 $54 Q = 3 4 5 6

If the market price of the firm’s output is $12, how many units of output should the firm produce: A. 3 B. 4 C. 5 D. 6 QUESTION 12

A firm finds that its MR = MC output, its TC = $1,000, VC = $800, FC = $200 and total

revenue is $900. This firm should:

A. Close down in the short run

B. Produce because the resulting loss is less than its FC.

C. Produce because it will realise an economic profit

D. Liquidate its assets and go out of business QUESTION 13

Which of the following do firms in monopolistic competition, oligopoly and monopoly have in common. All have:

A. Strongly competitive features

B. Downward sloping demand schedules

C. Full control of their output price

D. A small number of producers QUESTION 14

If a firm doubles its output in the long run and its unit cost of production decline, we can conclude that:

A.Technological progress has occurred

B.Economies of scale are being realized

C.The firm is encountering diminishing returns

D.Diseconomies of scale are being encountered QUESTION 15

In a perfect competitive industry, the market price of the product is $12. Firm A is producing

the output at which average cost equals marginal cost, both of which are $10. TO maximize its profit, firm A should: A. decrease output B. expand output C. leave output unchanged D. increase its selling price QUESTION 16

Which of the following best describes the situation of firms in monopolistic competition?

A. they are normally as large as monopolies

B. they enjoy substantial barriers to entry

C. they are typified by inter-dependence between firms

D. they produce similar, but not identical products QUESTION 17

Price will always be greater than marginal revenue for a monopolist because:

A. The firm faces a perfectly elastic demand curve

B. The demand curve is above the ATC curve

C. Since no new firms can enter the market, the firm is not forced to lower price to increase quantity sold

D. The firm must lower price for all units sold in order to increase the quantity sold QUESTION 18

Compare to perfectly competitive firm, a monopolist firm:

A. Produce a higher level of output and make a higher price

B. Produce a lower level of output and make a lower price

C. Produce a lower level of output but make a higher price

D. Produce a higher level of output but make a lower price QUESTION 19

According to the kinked demand curve theory, an oligopolistic firm will:

A. always cam economic profits:

B. be faced with a more inelastic demand curve if it increases price

C. be faced with a more clastic demand curve if it reduces price

D. match price decreases and ignore price increases of rivals QUESTION 20

Price competition among oligopolists ( thiểu quyền/ độc quyền nhóm ) usually:

A. Results in higher profits for all firms as a result of the increase in sales

B. Lowers profits for all firms as total revenue for the industry falls

C. Takes the form of advertising and product differentiation

D. Is frequent because it is a simple way to compete with rivals.

SECTION B: TRUE/FALSE/EXPLAIN QUESTIONS Answer T (true) or

F (false) for each of the following statements. Support your answer with a

clear esplanation and a diagram ( 1.5 points/question)

1. If demand increases and supply simultaneously decreases, equilibrium price will rise.

True. Because when demand increases, and supply decrease simultaneously, there will be

shortage as demand exceeds supply, so the price will rise to eliminate that shortage.

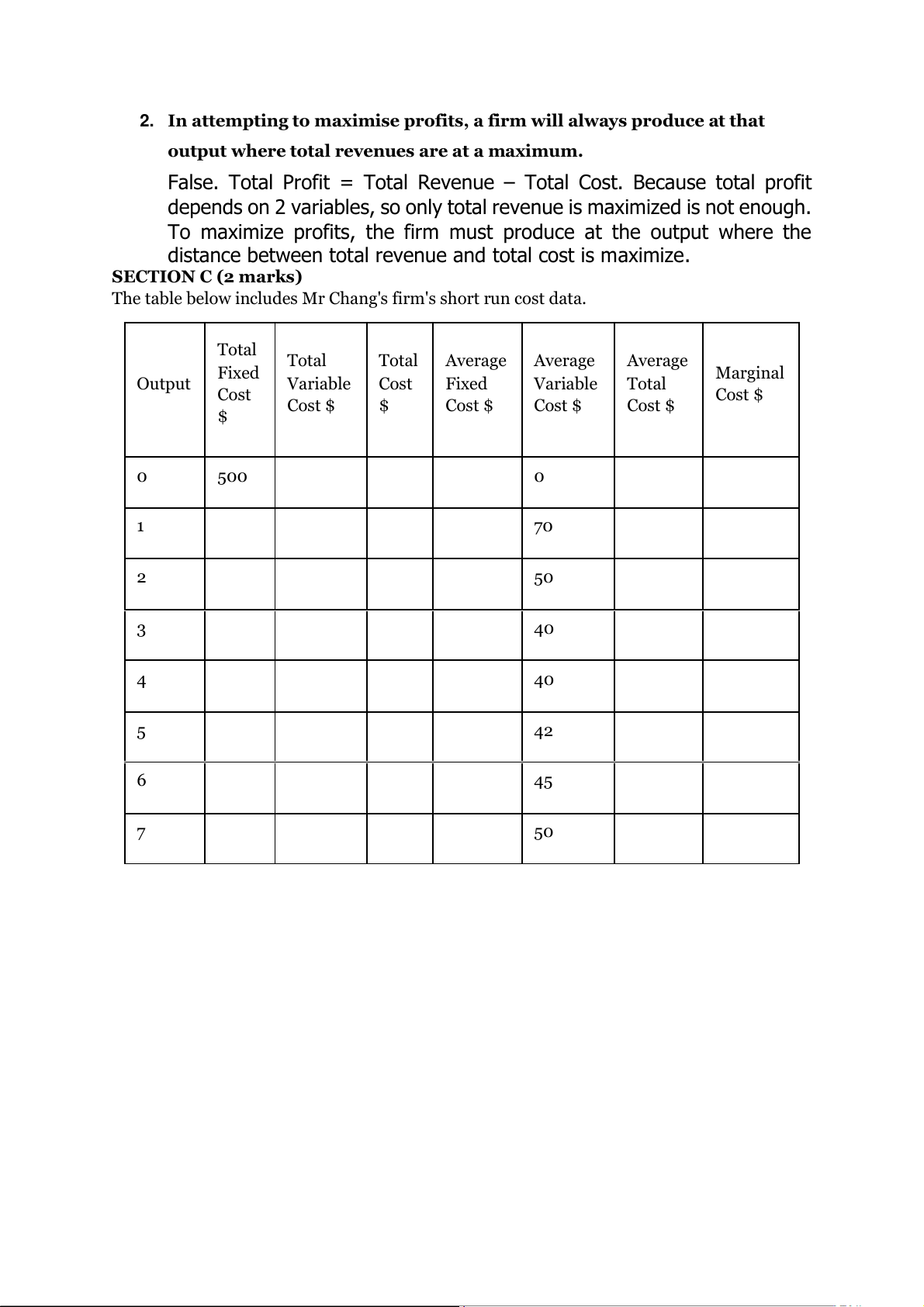

2. In attempting to maximise profits, a firm will always produce at that

output where total revenues are at a maximum.

False. Total Profit = Total Revenue – Total Cost. Because total profit

depends on 2 variables, so only total revenue is maximized is not enough.

To maximize profits, the firm must produce at the output where the

distance between total revenue and total cost is maximize. SECTION C (2 marks)

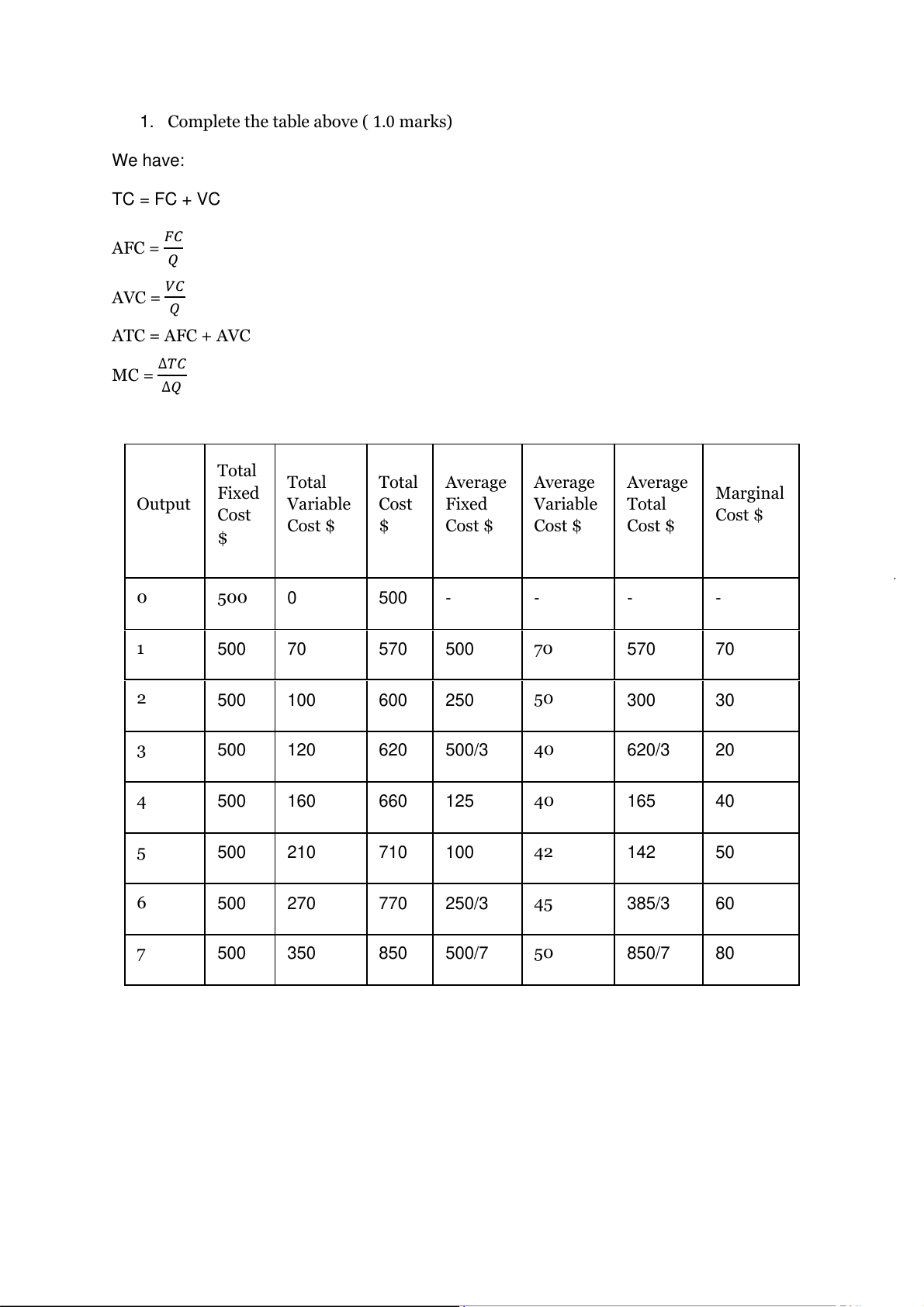

The table below includes Mr Chang's firm's short run cost data. Total Total Total Average Average Average Fixed Marginal Output Variable Cost Fixed Variable Total Cost Cost $ Cost $ $ Cost $ Cost $ Cost $ $ 0 500 0 1 70 2 50 3 40 4 40 5 42 6 45 7 50

1. Complete the table above ( 1.0 marks) We have: TC = FC + VC 𝐹𝐶 AFC = 𝑄 𝑉𝐶 AVC = 𝑄 ATC = AFC + AVC ∆𝑇𝐶 MC = ∆𝑄 Total Total Total Average Average Average Fixed Marginal Output Variable Cost Fixed Variable Total Cost Cost $ Cost $ $ Cost $ Cost $ Cost $ $ 0 500 0 500 - - - - 1 500 70 570 500 70 570 70 2 500 100 600 250 50 300 30 3 500 120 620 500/3 40 620/3 20 4 500 160 660 125 40 165 40 5 500 210 710 100 42 142 50 6 500 270 770 250/3 45 385/3 60 7 500 350 850 500/7 50 850/7 80

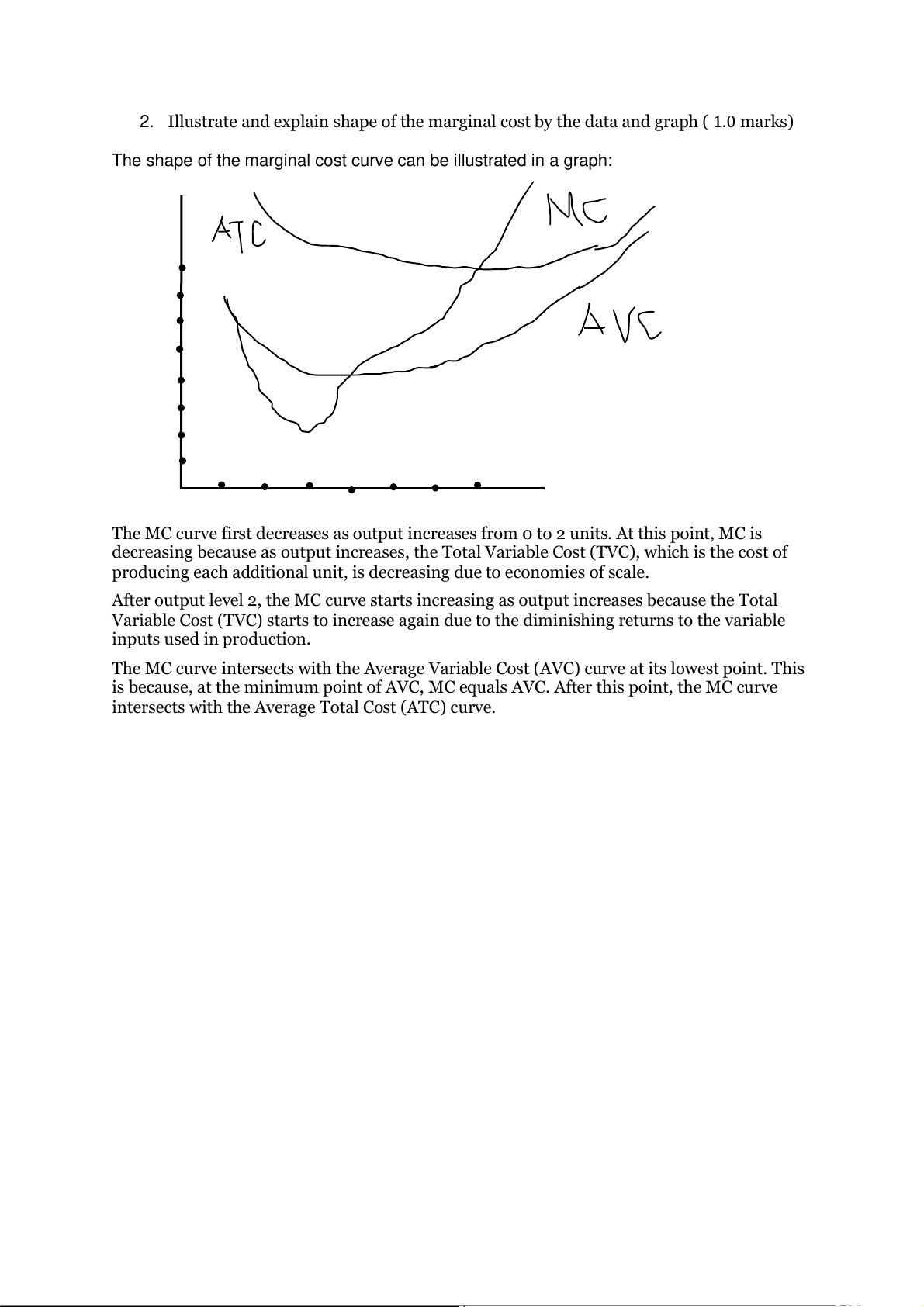

2. Illustrate and explain shape of the marginal cost by the data and graph ( 1.0 marks)

The shape of the marginal cost curve can be il ustrated in a graph:

The MC curve first decreases as output increases from 0 to 2 units. At this point, MC is

decreasing because as output increases, the Total Variable Cost (TVC), which is the cost of

producing each additional unit, is decreasing due to economies of scale.

After output level 2, the MC curve starts increasing as output increases because the Total

Variable Cost (TVC) starts to increase again due to the diminishing returns to the variable inputs used in production.

The MC curve intersects with the Average Variable Cost (AVC) curve at its lowest point. This

is because, at the minimum point of AVC, MC equals AVC. After this point, the MC curve

intersects with the Average Total Cost (ATC) curve.

Tài liệu liên quan:

-

Chương 3: độ co giãn và các nhân tố ảnh hưởng | Microeconomics | Trường Đại học Quốc tế, Đại học Quốc gia Thành phố Hồ Chí Minh

4 2 -

Microeconomics Syllabus | Microeconomics | Trường Đại học Quốc tế, Đại học Quốc gia Thành phố Hồ Chí Minh

4 2 -

Microeconomics Course Syllabus & Assessment Details | Microeconomics | Trường Đại học Quốc tế, Đại học Quốc gia Thành phố Hồ Chí Minh

4 2 -

Assignment 3 - Elasticity MCQs and Key Concepts | Microeconomics | Trường Đại học Quốc tế, Đại học Quốc gia Thành phố Hồ Chí Minh

4 2 -

Assignment 2 - Economic Equilibrium Analysis of Fridges and Motorcycles | Microeconomics | Trường Đại học Quốc tế, Đại học Quốc gia Thành phố Hồ Chí Minh

4 2