Practice Exercises 1 MA2 Solutions - Toán Kinh Tế | Trường Đại học Tôn Đức Thắng

1. Calculate return on investment. ROI = Profit /Capital employed = $8,000 / $40,000 = 20% 2. Calculate residual income. RI = Profit – Cost of capital = $8,000 - $40,000 x 12% = $3,200 3. Calculate net profit margin. Tài liệu được sưu tầm và soạn thảo dưới dạng file PDF để gửi tới các bạn sinh viên cùng tham khảo, ôn tập đầy đủ kiến thức, chuẩn bị cho các buổi học thật tốt. Mời bạn đọc đón xem!

Môn: Toán Kinh Tế (C01120) 81 tài liệu

Trường: Trường Đại học Tôn Đức Thắng 4.5 K tài liệu

Tác giả:

Preview text:

PRACTICE EXERCISES

MANAGERIAL ACCOUNTING 2 CHAPTER 8,9,10

Notes: Student uses two decimals in your answers and must provide detailed solution to get the full mark. CHAPTER 8 EXERCISE 1

Navo, Inc. has collected the following information for the previous financial year:

Sales .......................................................... $200,000

Net operating income ................................ $8,000

Average operating assets .......................... $40,000

Stockholders’ equity .................................. $30,000

Cost of capital ........................................... 12% Requirement:

1. Calculate return on investment. 2. Calculate residual income.

3. Calculate net profit margin 4. Calculate asset turnover. SOLUTIONS

- Net operating income = Profit

- Average operating assets = Capital employed

- Cost of capital (%) = Imputed interest charge (%) = Target ROI (%) = Required return (%)

1. Calculate return on investment.

ROI = Profit /Capital employed = $8,000 / $40,000 = 20%

2. Calculate residual income.

RI = Profit – Cost of capital = $8,000 - $40,000 x 12% = $3,200

3. Calculate net profit margin

Net profit margin = Net profit / Sales = $8,000 / $200,000 = 4% 4. Calculate asset turnover.

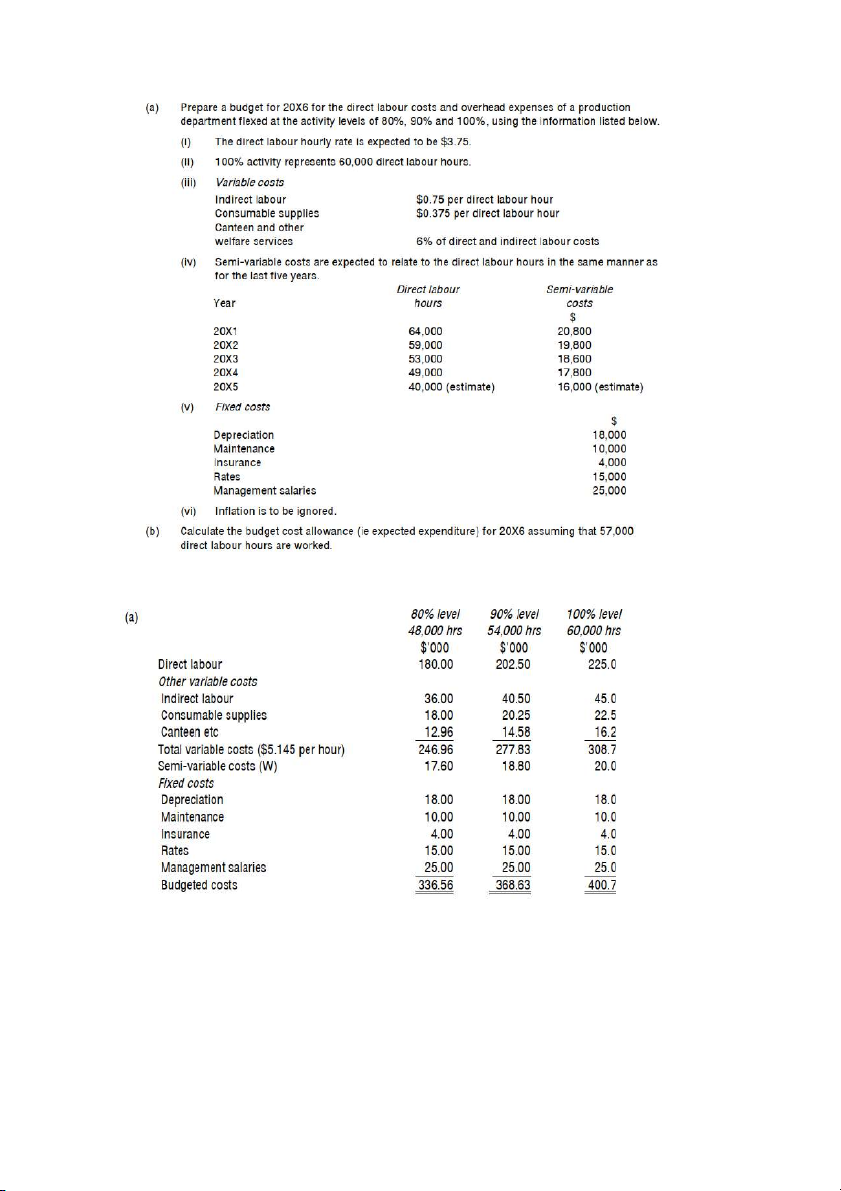

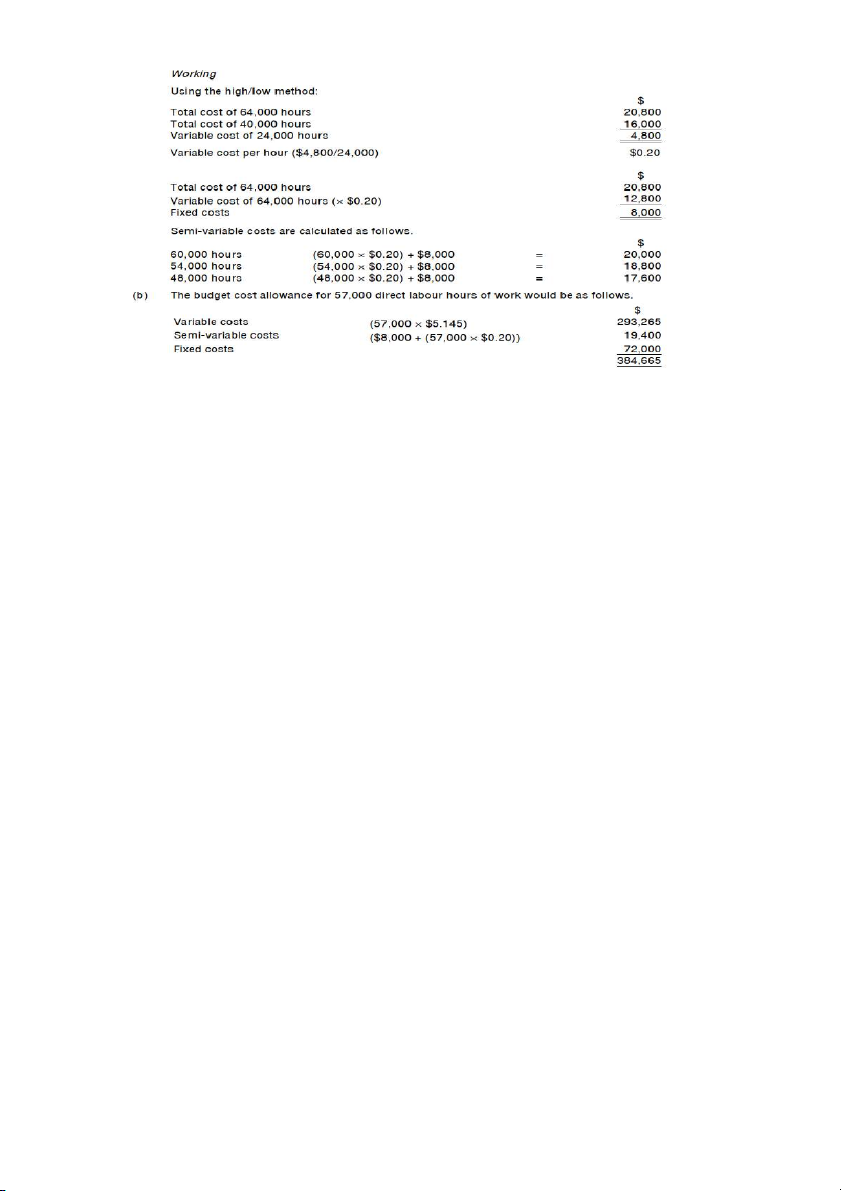

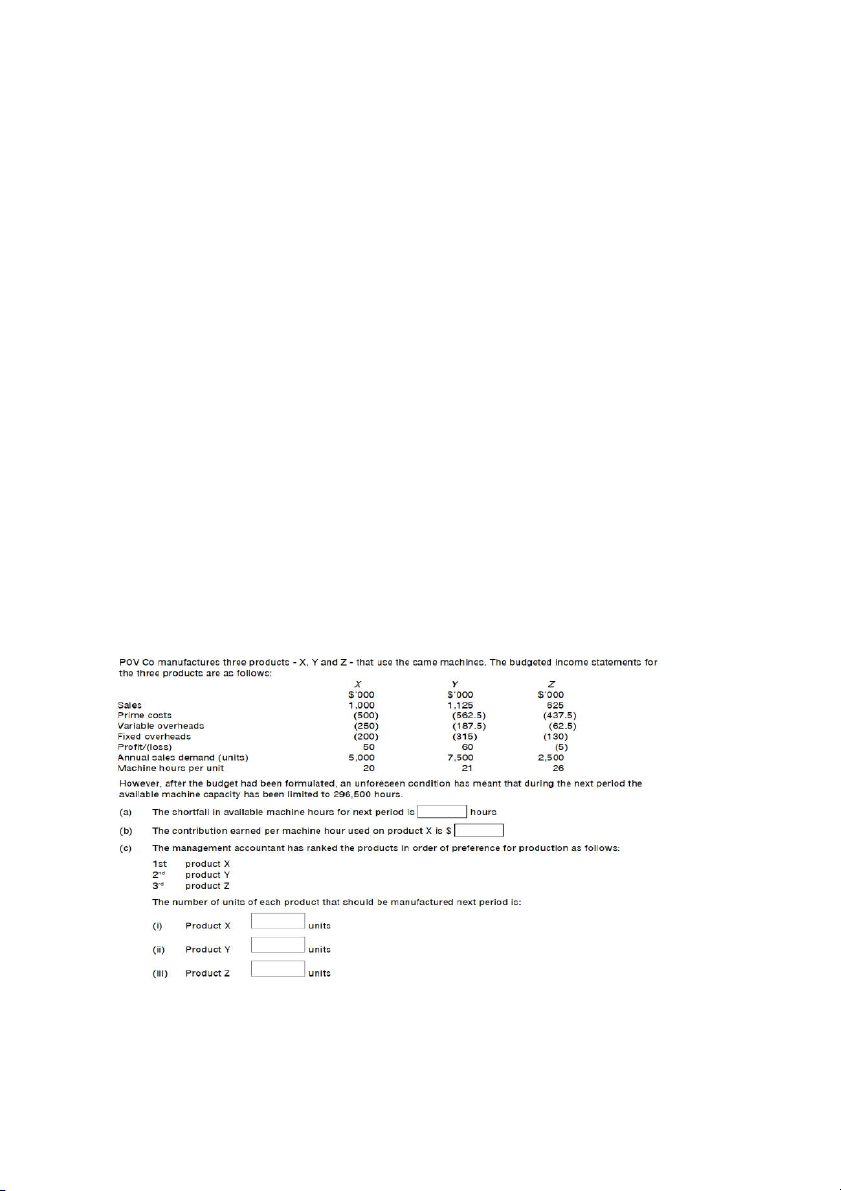

Asset turnover = Sales / Capital employed = $200,000 / $40,000 = 5 1/7 EXERCISE 2 SOLUTIONS 2/7 CHAPTER 9 EXERCISE 3

The following information is taken from Whacker Company January data: Budget Actual

Number of units produced and sold 3,000 units 4,000 units Kilograms of direct material 6,000 kgs 10,000 kgs Number of direct labor hours 9,000 hours 10,000 hours $ $ Sales price 120 115 Direct material costs 60,000 95,000 Direct labor costs 81,000 120,000

Variable production overhead costs 27,000 32,000

Variable selling and administrative costs 42,000 60,000 Fixed overhead costs 195,000 200,000

Requirement: Calculate the following items:

1. The direct material price variance.

2. The direct material usage variance.

3. The direct labor rate variance.

4. The direct labor efficiency variance. 3/7

5. The variable production overhead expenditure variance.

6. The variable production overhead efficiency variance.

7. The standard variable production cost per unit.

8. The standard variable cost per unit.

9. The standard contribution margin per unit. 10. The sales price variance.

11. The sales volume contribution variance.

12. The fixed overhead expenditure variance. SOLUTIONS

1. The direct material price variance.

= (AP – SP) x AQ = AP x AQ – SP x AQ = $95,000 – ($60,000/6,000) x 10,000 = $5,000 F

2. The direct material usage variance.

SQ of DM for actual output = (6,000 kgs/3,000 units) x 4,000 units = 8,000 kgs. SP = $60,000/6,000 kgs = $10

The direct material usage variance.

= (AQ – SQ) x SP = (10,000 – 8,000) x $10 = $20,000 A

3. The direct labor rate variance.

SR = $81,000/9,000 hours = $9/hour

SH for actual output = (9,000 hours/3,000 units) x 4,000 units = 12,000 hours

The direct labor rate variance.

= (AR – SR) x AH = AR x AH – SR x AH = $120,000 - $9 x 10,000 hours = $30,000 A

4. The direct labor efficiency variance.

= (AH – SH) x SR = (10,000 – 12,000) x $9 = $18,000 F

5. The variable production overhead expenditure variance.

SR = $27,000/9,000 hours =$3/hour

SH for actual output = (9,000 hours/3,000 units) x 4,000 units = 12,000 hours

= (AR – SR) x AH = AR x AH – SR x AH = $32,000 - $3 x 10,000 hours = $2,000 A

6. The variable production overhead efficiency variance.

= (AH – SH) x SR = (10,000 – 12,000) x $3 = $6,000 F

7. The standard variable production cost per unit.

= Total variable production costs / units produced 4/7

= ($60,000 + $81,000 + $27,000)/3,000 units = $56

8. The standard variable cost per unit.

= Total variable costs / units produced

= ($60,000 + $81,000 + $27,000 + $42,000)/3,000 units = $70

9. The standard contribution margin per unit.

= Sales price – Variable cost per unit = $120 - $70 = $50 10. The sales price variance.

= (AP – SP) x AQ = ($115 - $120) x 4,000 = $20,000 A

11. The sales volume contribution variance. = (AQ – BQ) x SC

= (4,000 units – 3,000 units) x $50 = $50,000 F

SC: standard contribution margin per unit. BQ: Budget quantity

12. The fixed overhead expenditure variance.

= Actual fixed overhead costs – Budgeted overhead costs

= $200,000 - $195,000 = $5,000 A CHAPTER 10 EXERCISE 4

LN Company provides a single product. The company’s sales and costs for last month follow: Total Per unit

Sales……………………………. $1,200,000 $60

Variable costs…………………... 520,000 26

Contribution margin……………. 680,000 $34

Fixed costs……………………… 312,800

Net operating income…………… $367,200 Requirements:

1. Calculate the monthly break-even point in units sold and in sales dollars.

2. Calculate the target units sold to earn a target profit after tax of $120,000? Corporate income tax rate of 40%.

3. If total sales increase by $100,000 and fixed expenses remain unchanged, calculate the change

of net operating income?

4. Calculate the margin of safety in units and in sales dollars. 5/7 SOLUTIONS

1. Calculate the monthly break-even point in units sold and in sales dollars.

BEP in units = Total fixed costs / CM unit = $312,800/$34 = 9,200 units.

BEP in sales dollars = 9,200 units x $60 = $552,000

2. Calculate the target units sold to earn a target profit after tax of $120,000? Corporate income tax rate of 40%.

Profit before tax = $120,000/(1-40%) = $200,000

Target unit sales = (Total fixed costs + Profit before tax)/ CM unit

= ($312,800 + $200,000)/ $34 = 15,082.35 units.

3. If total sales increase by $100,000 and fixed expenses remain unchanged, calculate the change

of net operating income?

Contribution margin ratio = CM unit/ Sales price = $34/$60 = 56.67%

Increase of net operating income

= Increase of contribution margin = $100,000 x ($34/$60) = $56,666.67

4. Calculate the margin of safety in units and in sales dollars.

Actual units sold = $1,200,000 / $60 = 20,000 units Margin of safety in units

= Actual units sold – BEP in units = 20,000 units – 9,200 units = 10,800 units

Margin of safety in sales dollars

= Actual sales – BEP in sales dollars = $1,200,000 - $552,000 = $648,000 OR

Margin of safety in sales dollars

= Margin of safety in units x sales price = 10,800 units x $60 = $648,000 EXERCISE 5 6/7 SOLUTIONS 7/7

Tài liệu liên quan:

-

Chương 1 Ma trận và hệ phương trình

19 10 -

Bài tập Kiểm toán BCTC Chương 2: Hàng tồn kho và Ghi nhận Doanh thu

111 56 -

Bài giảng toán kinh tế chương 3 | Trường Đại học Tôn Đức Thắng

156 78 -

Bài giảng chương 4 hàm hai biến | Toán kinh tế

146 73 -

Bài giảng chương 1: ma trận và các phép toán | Toán kinh tế

124 62