Solutions - Microeconomic Theory | Microeconomics | Trường Đại học Quốc tế, Đại học Quốc gia Thành phố Hồ Chí Minh

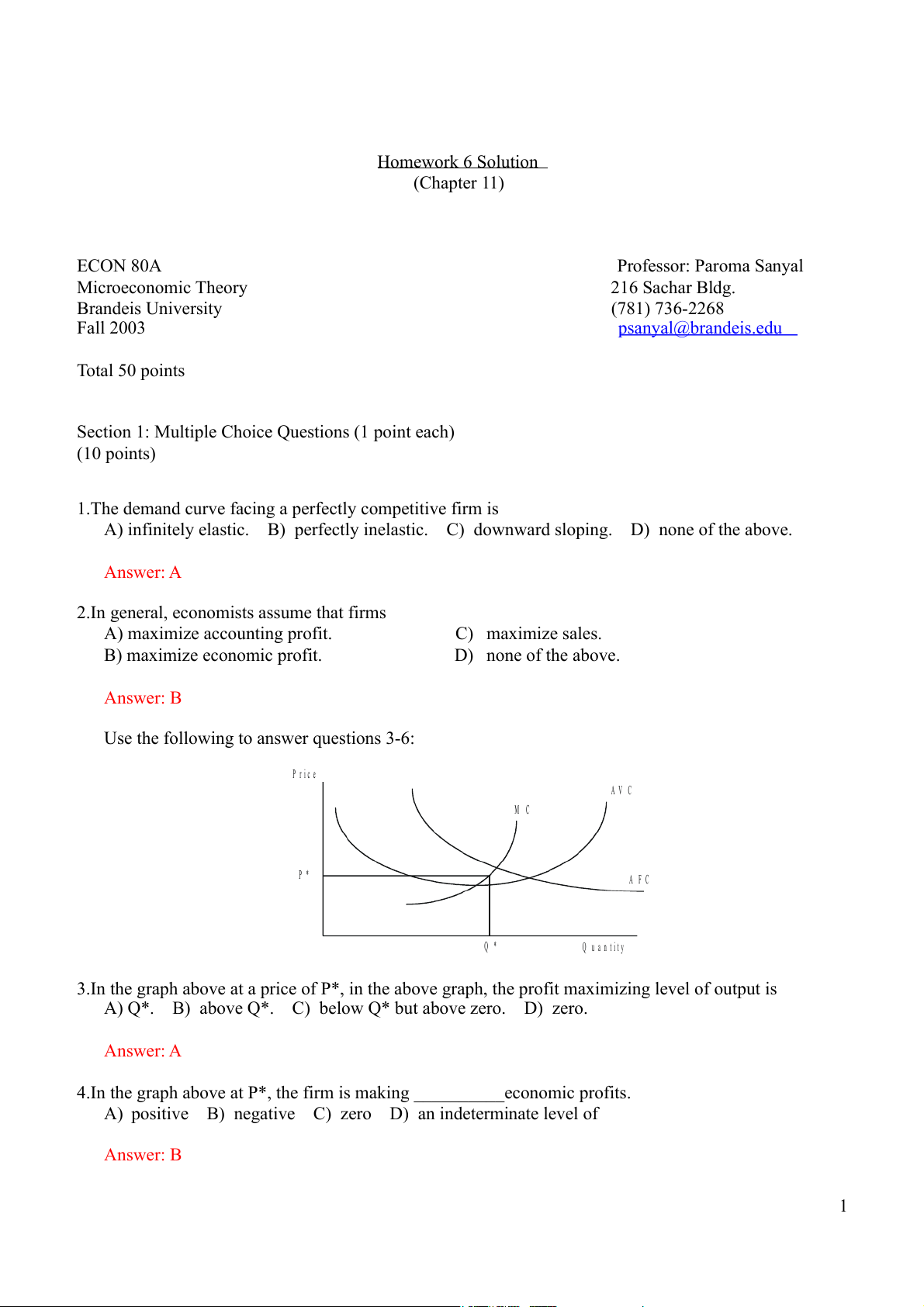

The demand curve facing a perfectly competitive firm is A) infinitely elastic. B) perfectly inelastic. C) downward sloping. D) none of the above. Answer: A 2.In general, economists assume that firms A) maximize accounting profit. C) maximize sales. B) maximize economic profit. D) none of the above. Answer: B Use the following to answer questions 3-6: A F C A V C M C P r i c e Q u a n t i t y P * Q * 3.In the graph above at a price of P*, in the above graph, the profit maximizing level of output is A) Q*. B) above Q*. C) below Q* but above zero. D) zero. Tài liệu được sưu tầm và soạn thảo dưới dạng file PDF để gửi tới các bạn cùng tham khảo, ôn tập đầy đủ kiến thức, chuẩn bị cho các buổi học thật tốt. Mời bạn đọc đón xem!

Môn: Microeconomics 635 tài liệu

Trường: Trường Đại học Quốc tế, Đại học Quốc gia Thành phố Hồ Chí Minh 1.9 K tài liệu

Tác giả:

Preview text:

Homework 6 Solution (Chapter 11) ECON 80A Professor: Paroma Sanyal Microeconomic Theory 216 Sachar Bldg. Brandeis University (781) 736-2268 Fall 2003 psanyal@brandeis.edu Total 50 points

Section 1: Multiple Choice Questions (1 point each) (10 points)

1.The demand curve facing a perfectly competitive firm is

A) infinitely elastic. B) perfectly inelastic. C) downward sloping. D) none of the above. Answer: A

2.In general, economists assume that firms

A) maximize accounting profit. C) maximize sales. B) maximize economic profit. D) none of the above. Answer: B

Use the following to answer questions 3-6: P r i c e A V C M C P * A F C Q * Q u a n t i t y

3.In the graph above at a price of P*, in the above graph, the profit maximizing level of output is

A) Q*. B) above Q*. C) below Q* but above zero. D) zero. Answer: A

4.In the graph above at P*, the firm is making __________economic profits.

A) positive B) negative C) zero D) an indeterminate level of Answer: B 1

5.Which statement is true of the graph shown?

A) The marginal cost curve should not cross the AFC while it is falling.

B) If an ATC curve was drawn in the graph it would intersect the MC curve but not any other curve.

C) The shut down point of the firm would be at an output less than Q*. D) Both b and c are correct.

E) None of the above are correct. Answer: D

6.In the graph above if the price persists at P*, the profit maximizing firm will A) shut down immediately. B) shut down in the long run. C) operate indefinitely.

D) has a strategy that can not be predicted without an ATC curve. Answer: B

7.Some people advocate price ceilings in certain markets because they seek to

A) expand the total of consumer and producer surplus which the market generates.

B) redistribute welfare from the producer to the consumer even if overall welfare is sacrificed.

C) redistribute welfare from the consumer to the producer even if welfare is sacrificed.

D) enhance both efficiency and distribution goals with the price ceiling. Answer: B

8.The output where MC = AVC is called the

A) shutdown point. B) break-even point. C) profit maximizing point. D) none of the above. Answer: A

9.The output where MC = ATC = P is called the

A) shutdown point. B) break-even point. C) profit maximizing point. D) none of the above. Answer: B

10.In the long run for a competitive firm,

A) the firm is at the bottom of its short run average cost curve.

B) the firm is at the bottom of its long run average cost curve.

C) marginal cost equals price. D) all of the above. Answer: D 2

Section 2: TRUE OR FALSE (5 points each) (20 Points)

When answering the True or False questions please give an explanation why you think the statement is

either True of False. Use graphs whenever possible. But graphs are not substitutes for explanations. Please

write down the explanation even when you use graphs. For a correct T/F answer you will receive 2 points

and the other 3 points are for your explanation)

1. A firm in a competitive firm has (short-run) total cost function of TC = 0.2Q – 5Q + 30 faces a price 2

of 6. Then the firm should shut down. FALSE MC = 0.4Q – 5 Use P = MC Q = 27.5

= TR – TC = P.Q – TC = 6(27.5) – (0.2(27.5) – 5(27.5) + 30) = 121.25 2

Since the firm earns positive profit, it should stay open.

2. The total revenue curve always has constant slope for a perfectly competitive firm. TRUE

Generally for downward sloping demand curves, a seller has to

decrease price if he wants to sell more. But the demand curve facing

the perfectly competitive firm is horizontal. This means that a firm in

this market can sell any quantity at the given market price. Thus TR =

PQ = (constant)Q. Thus the slope of the TR curve, which is d(TR)/dQ is constant. (Graphs required)

3. In a perfectly competitive industry with constant costs (CRS), a fixed (constant)

tax per unit of output, will not affect the amount of output sold by each firm in the long run. TRUE

Suppose a tax of T dollars placed on each unit of output. The new industry curve: SLR + T and price

increases by exactly T dollars. The effect of such a tax is to produce a parallel upward movement

in each firm's long-run average cost curve. The output level for which the minimum value of

LAC occurs will thus be the same as before, which means that firms in long-run equilibrium will

each have the same amount of output as before.

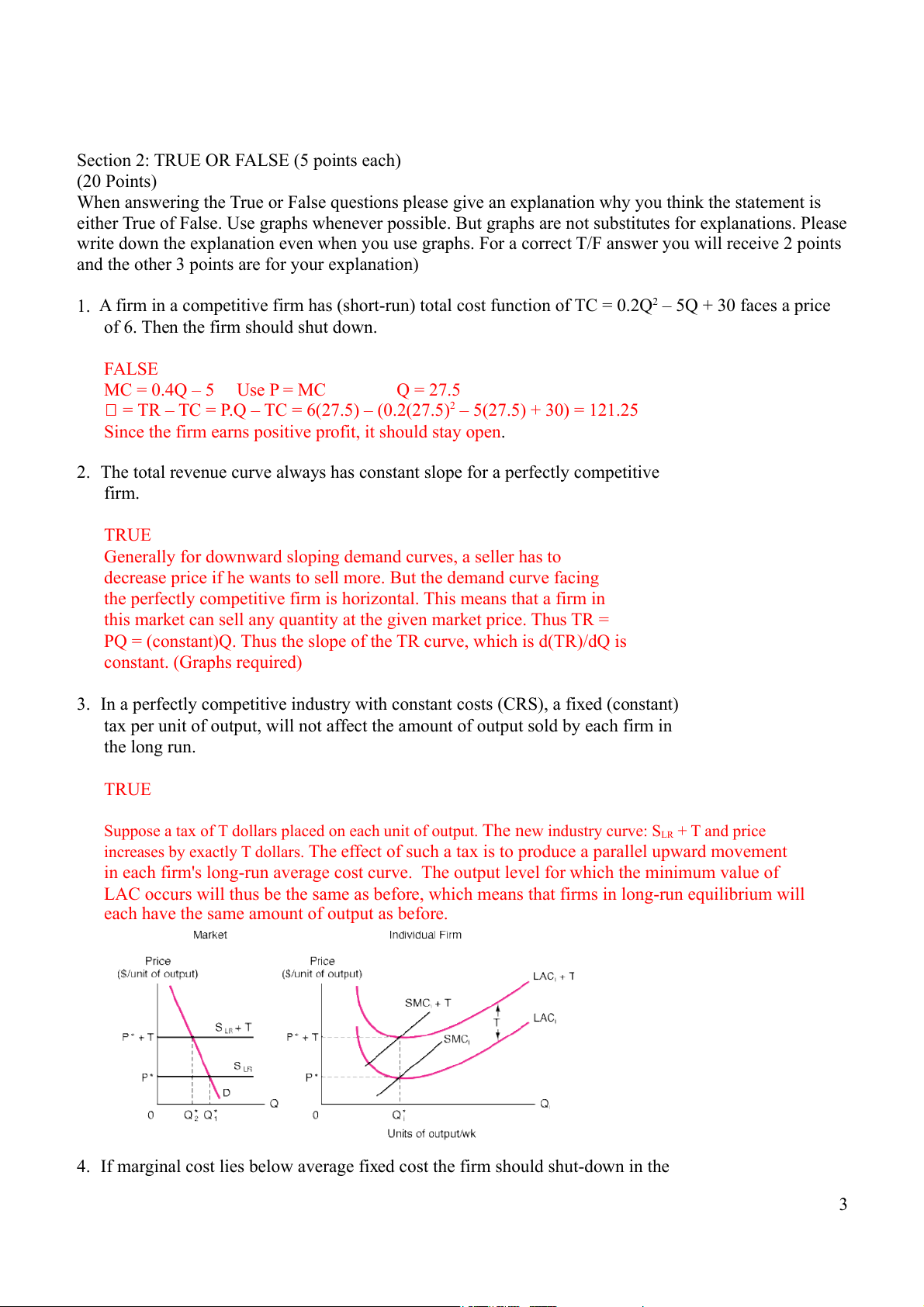

4. If marginal cost lies below average fixed cost the firm should shut-down in the 3 short-run.

UNCERTAIN (Either answer is correct) (1) FALSE

The firm should shut down if and only if its price is below AVC. MC can lie below AFC at the

same time price lies above AVC (see diagram). P AVC P* AFC MC Q Q* (2) TRUE

Usually the AFC is below the AVC. Thus in most cases if the price is below AFC it will generally

be below AVC as well and the firm would shut down.

Section 3: Short Answers & Quantitative Problems (10 points each) (Total 20 points) Question 1

(a) All firms in a competitive industry have long-run total cost curves given by:

LTC = q3 – 10q + 36q, where q is the firm’ 2 s level of output. (5 points)

(i) What is the long-run output level of each firm?

(ii) What is the long-run equilibrium price in the industry? Answer (a)

(i) Long-run equilibrium price for this industry will occur at the minimum value of LAC. LAC= LTC/q= q – 10q + 36 2

d(LAC)/dq = 2q-10 = 0, which solves for q = 5.

(ii) At q = 5, LAC=25-50+36=11. This P = 11

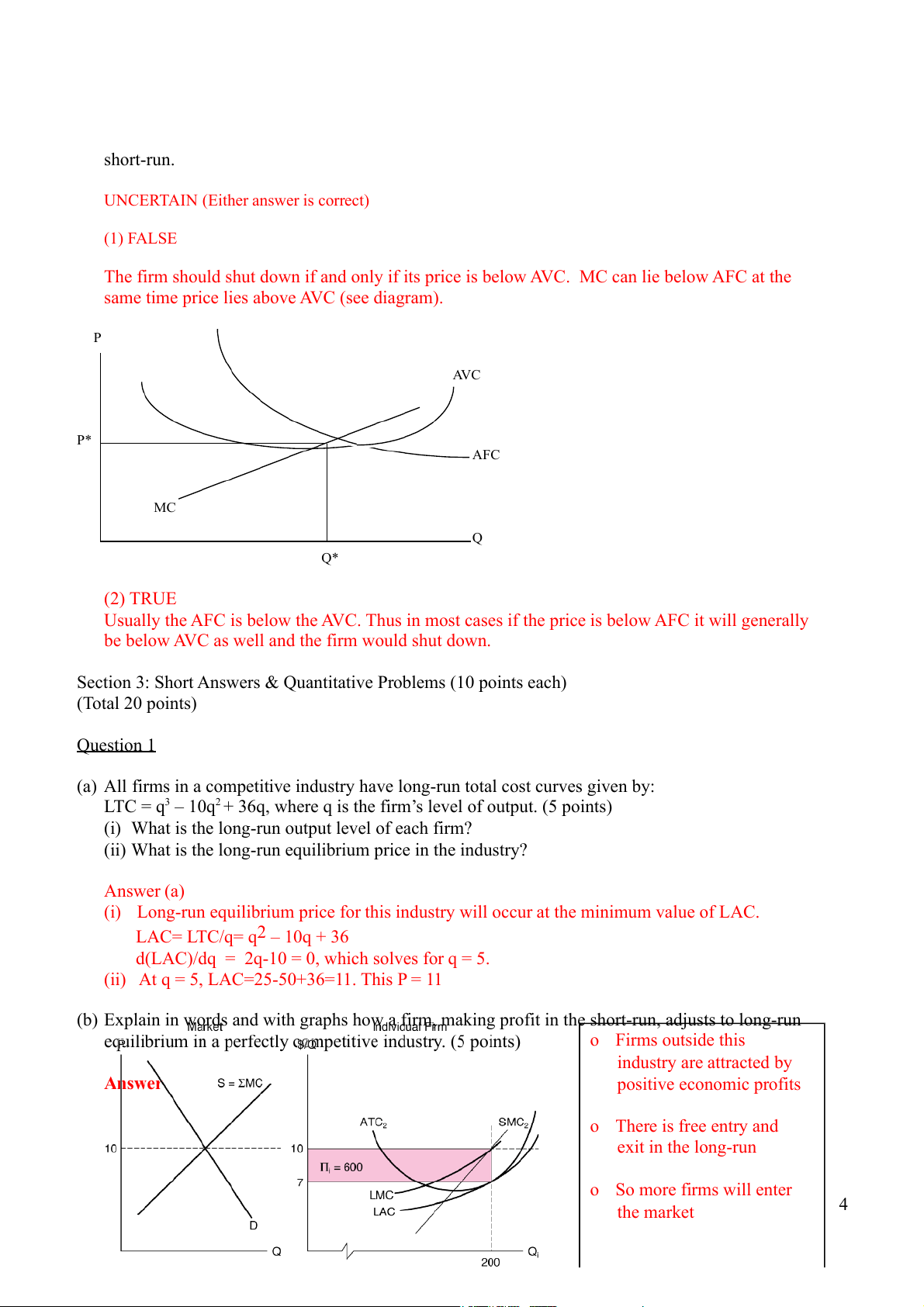

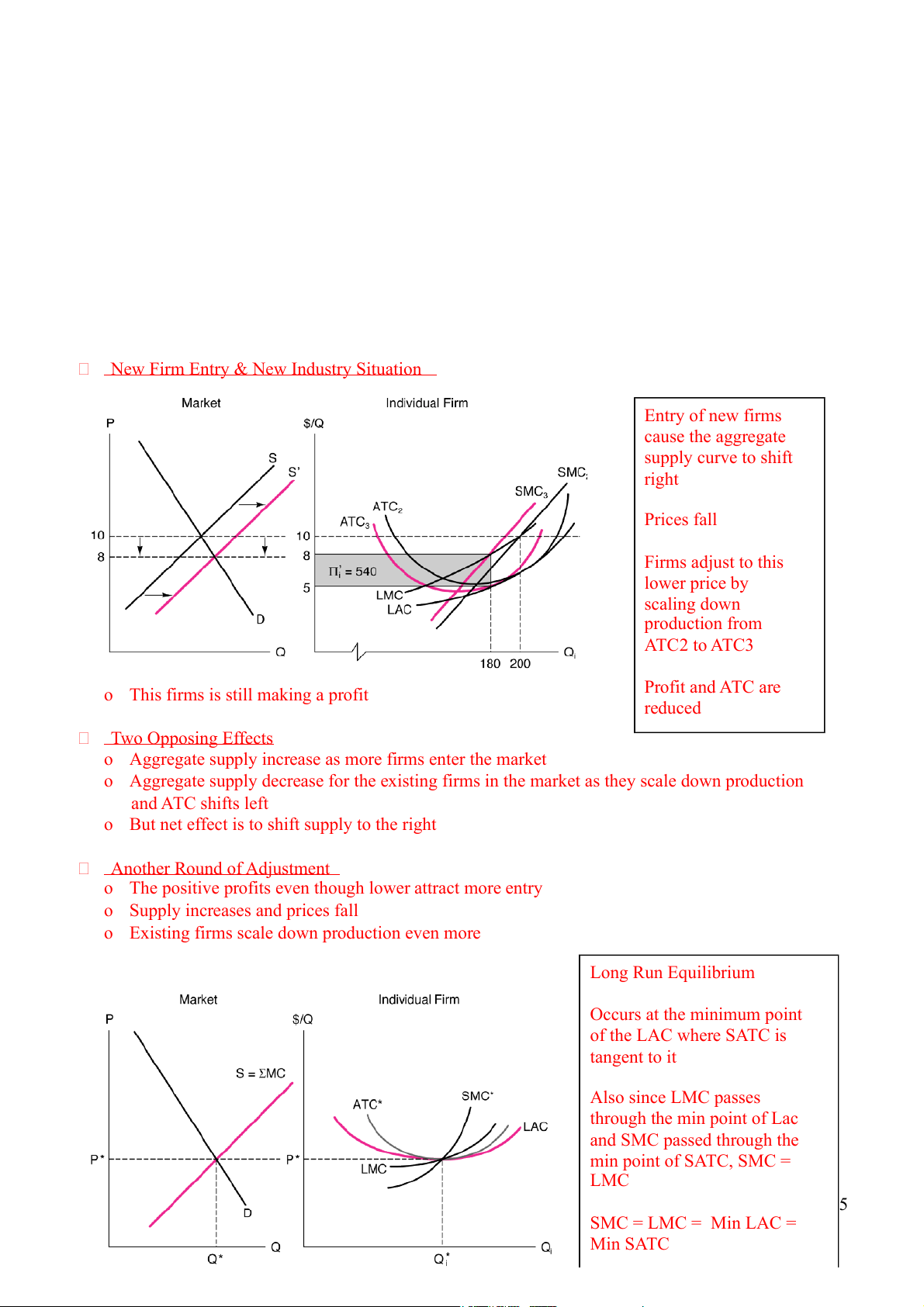

(b) Explain in words and with graphs how a firm, making profit in the short-run, adjusts to long-run o Firms outside this industry are attracted by positive economic profits o There is free entry and exit in the long-run o So more firms will enter 4 the market

New Firm Entry & New Industry Situation Entry of new firms cause the aggregate supply curve to shift right Prices fall Firms adjust to this lower price by scaling down production from ATC2 to ATC3

o This firms is still making a profit Profit and ATC are reduced Two Opposing Effects

o Aggregate supply increase as more firms enter the market

o Aggregate supply decrease for the existing firms in the market as they scale down production and ATC shifts left

o But net effect is to shift supply to the right Another Round of Adjustment

o The positive profits even though lower attract more entry

o Supply increases and prices fall

o Existing firms scale down production even more Long Run Equilibrium Occurs at the minimum point of the LAC where SATC is tangent to it Also since LMC passes through the min point of Lac and SMC passed through the min point of SATC, SMC = LMC 5 SMC = LMC = Min LAC = Min SATC Question 2

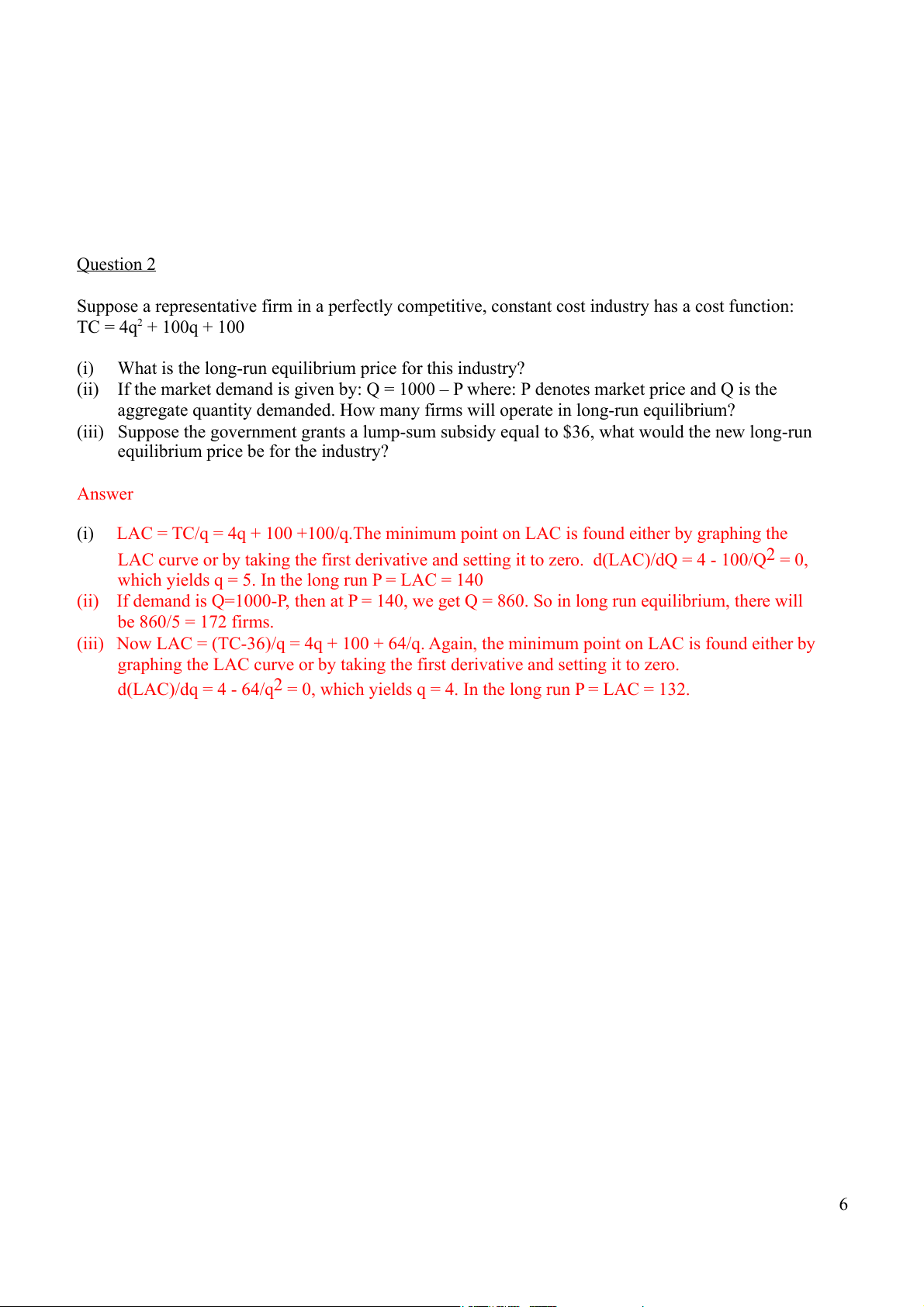

Suppose a representative firm in a perfectly competitive, constant cost industry has a cost function: TC = 4q + 100q + 100 2 (i)

What is the long-run equilibrium price for this industry?

(ii) If the market demand is given by: Q = 1000 – P where: P denotes market price and Q is the

aggregate quantity demanded. How many firms will operate in long-run equilibrium?

(iii) Suppose the government grants a lump-sum subsidy equal to $36, what would the new long-run

equilibrium price be for the industry? Answer (i)

LAC = TC/q = 4q + 100 +100/q.The minimum point on LAC is found either by graphing the

LAC curve or by taking the first derivative and setting it to zero. d(LAC)/dQ = 4 - 100/Q = 0, 2

which yields q = 5. In the long run P = LAC = 140

(ii) If demand is Q=1000-P, then at P = 140, we get Q = 860. So in long run equilibrium, there will be 860/5 = 172 firms.

(iii) Now LAC = (TC-36)/q = 4q + 100 + 64/q. Again, the minimum point on LAC is found either by

graphing the LAC curve or by taking the first derivative and setting it to zero.

d(LAC)/dq = 4 - 64/q = 0, which yields q = 4. In the long run P 2 = LAC = 132. 6

Tài liệu liên quan:

-

Chương 3: độ co giãn và các nhân tố ảnh hưởng | Microeconomics | Trường Đại học Quốc tế, Đại học Quốc gia Thành phố Hồ Chí Minh

4 2 -

Microeconomics Syllabus | Microeconomics | Trường Đại học Quốc tế, Đại học Quốc gia Thành phố Hồ Chí Minh

4 2 -

Microeconomics Course Syllabus & Assessment Details | Microeconomics | Trường Đại học Quốc tế, Đại học Quốc gia Thành phố Hồ Chí Minh

4 2 -

Assignment 3 - Elasticity MCQs and Key Concepts | Microeconomics | Trường Đại học Quốc tế, Đại học Quốc gia Thành phố Hồ Chí Minh

4 2 -

Assignment 2 - Economic Equilibrium Analysis of Fridges and Motorcycles | Microeconomics | Trường Đại học Quốc tế, Đại học Quốc gia Thành phố Hồ Chí Minh

4 2