The adjusting process - Toán Kinh Tế | Trường Đại học Tôn Đức Thắng

Accrual accounting records revenues and expenses when they are earned/incurred •Cash-basis accounting records revenues and expenses when cash is received or paid •Accrual accounting requires adjusting entries at the end of the period. Tài liệu được sưu tầm và soạn thảo dưới dạng file PDF để gửi tới các bạn sinh viên cùng tham khảo, ôn tập đầy đủ kiến thức, chuẩn bị cho các buổi học thật tốt. Mời bạn đọc đón xem!

Môn: Toán Kinh Tế (C01120) 81 tài liệu

Trường: Trường Đại học Tôn Đức Thắng 4.5 K tài liệu

Tác giả:

Preview text:

Chapter 3 The adjusting process

201044 - The adjusting process Learning objectives

• Differentiate between accrual and cash-basis accounting

• Explain why adjusting entries are needed

• Journalise and post adjusting entries

• Explain the purpose of and prepare an adjusted trial balance

• Prepare the financial statements from the adjusted trial balance

• Describe the ethical challenges in accrual accounting 1/ 2/ 2020

201044 - The adjusting process 2

3.1. Accrual versus cash-basis accounting

• Accrual accounting records the effect of each transaction as it occurs

• Cash-basis accounting records only cash receipts and cash

payments. It ignores receivables, payables and other items

• In accrual accounting, revenues are recorded when earned, which

is not necessarily in the same accounting period as when the

corresponding cash is received

• Most businesses use the accrual basis as covered in this book 1/ 2/ 2020

201044 - The adjusting process 3

3.1. Accrual versus cash-basis accounting Ex: 1.

Suppose Smart Touch purchases $200 of office supplies

on credit on 15 Jun and pays to supplier on 03 Jul. 2.

Suppose Smart Touch performs services and earns

revenue of $1,000 on 20 Jun but collects no cash (Cash will be collected on 05 Jul)

Indicate the difference in recording above transactions on

the cash-basic accounting and accrual-basic accounting. 1/ 2/ 2020

201044 - The adjusting process 4

3.2. Why we adjust the accounts

• Accrual accounting requires adjusting entries at the end of the period

• Adjusting entries assign revenues to the period when they are

earned and expenses to the period when they are incurred

• Adjustments are needed to properly measure two things: (1) profit

(loss) in the income statement, and (2) assets and liabilities in the balance sheet 1/ 2/ 2020

201044 - The adjusting process 5

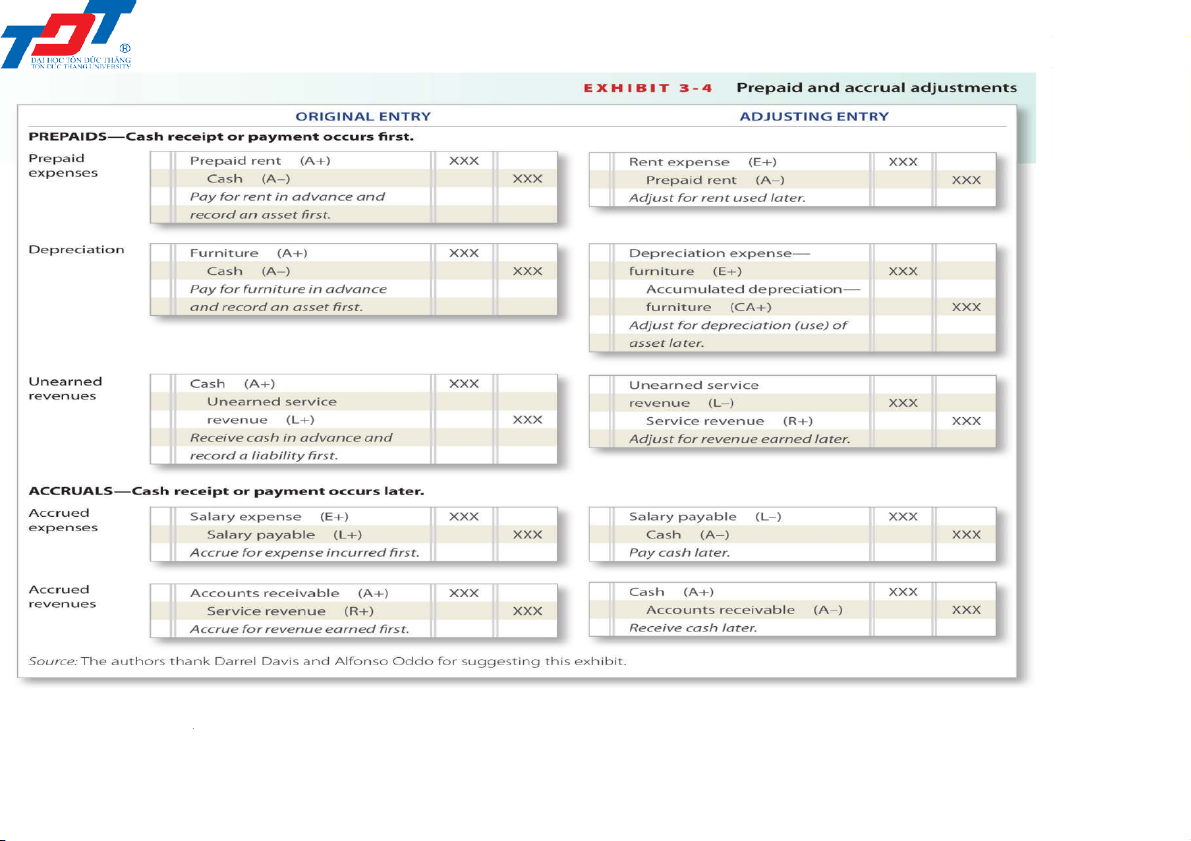

3.3. Two categories of adjusting entries

• The two basic categories of adjusting entries are prepayments (defferals) and accruals

• In a prepaid adjustment, the cash payment occurs before an

expense is recorded or the cash receipt occurs before the revenue is earned

• An accrual records an expense before the cash payment or it

records the revenue before the cash is received

• Adjusting entries fall into five types: prepaid expenses, depreciation

of non-current assets, accrued expenses, accrued revenues, unearned revenues 1/2/2020

201044 - The adjusting process 6

3.3. Two categories of adjusting entries Prepaid expenses

• Prepaid expenses are advance payments of expenses

• Examples include prepaid rent, insurance, supplies

• Prepaid expenses are considered assets rather than expenses

• When the prepayment is used up, the used portion of the asset

becomes an expense via an adjusting journal entry

Ex: Smart Touch prepays three months’ office rent of $3,000 ($1,000

per month x 3 months) on 01 June 201N 1/ 2/ 2020

201044 - The adjusting process 7

3.3. Two categories of adjusting entries Depreciation

• Property, plant and equipment assets are long-lived, non-current,

tangible assets used in the operation of a business

• As a business uses non-current assets, their value and usefulness decline

• The decline in usefulness of a non-current asset is an expense, and

accountants systematically spread the asset’s cost over its useful life

• The allocation of a non-current asset’s value to expense is called depreciation 1/ 2/ 2020

201044 - The adjusting process 8

3.3. Two categories of adjusting entries Depreciation

• The accumulated depreciation account is the sum of all the

depreciation recorded for the asset, and that total increases (accumulates) over time

• Accumulated depreciation is a contra asset

Ex: On 01 June, Smart Touch purchased furniture for $18,000. Its

expected useful life is five years. 1/ 2/ 2020

201044 - The adjusting process 9

3.3. Two categories of adjusting entries Accrued expenses

• The term accrued expense refers to an expense incurred before paying for them

• Examples include accruing salary expense and accruing interest expense

• An accrued expense hasn’t been paid for yet and always creates a liability

Ex: Sheena Bright pays its employee a monthly salary of $1,800 - half

on the 17th and half on the first day of next month. 1/ 2/ 2020

201044 - The adjusting process 10

3.3. Two categories of adjusting entries Accrued revenues

• Businesses can earn revenue before they receive the cash, which creates accrued revenues

• Accrued revenue is revenue that has been earned but for which the

cash has not yet been collected

Ex: Assume that Smart Touch is hired on 16 June to perform e-

learning services for the Central Queensland University. Under this

agreement, Smart Touch will earn $800 monthly.

During June, for work performed from 16 June to 30 June, Smart

Touch will earn half a month’s fee, $400. 1/ 2/ 2020

201044 - The adjusting process 11

3.3. Two categories of adjusting entries

Unearned revenues (Deferred revenue)

• Some businesses collect cash from customers in advance of performing work

• Receiving cash before earning it creates a liability to perform work in

the future called unearned revenue

• The business owes a product or a service to the customer, or it

owes the customer his or her money back

• Only after completing the job will the business earn the revenue.

Because of this delay, unearned revenue is also called deferred revenue 1/ 2/ 2020

201044 - The adjusting process 12

3.3. Two categories of adjusting entries

Unearned revenues (Deferred revenue)

• Ex: A legal firm engages Smart Touch to provide e-learning

services, agreeing to pay $600 in advance monthly, beginning

immediately. Sheena Bright collects the first amount on 21 June. 1/ 2/ 2020

201044 - The adjusting process 13

3.3. Two categories of adjusting entries 1/ 2/ 2020

201044 - The adjusting process 14

3.3. Two categories of adjusting entries

Ex: I nform at ion for t he adj ust m ent s at 30 June 201N of Sm art Touch

( a) Prepaid rent expired, $1,000 ( b) Supplies used , $100

( c) Depreciat ion on furnit ure, $300

( d) Depreciat ion on building, $200

( e) Accrued salary expense, $900

( f) Accrued int erest on loan, $100

( g) Accrued ser vice revenue, $400

( h) Service revenue t hat was collect ed in advance and now had been earned, $200

Required: Journalising and post ing t o T- account s all t he above adj ust m ent s. 1/ 2/ 2020 15

3.4. The adjusted trial balance

• Prepared after adjusting entries are posted

• Useful step in preparing financial statements

• Often appears on a work sheet 1/ 2/ 2020

201044 - The adjusting process 16

3.4. The adjusted trial balance 1/ 2/ 2020

201044 - The adjusting process 17

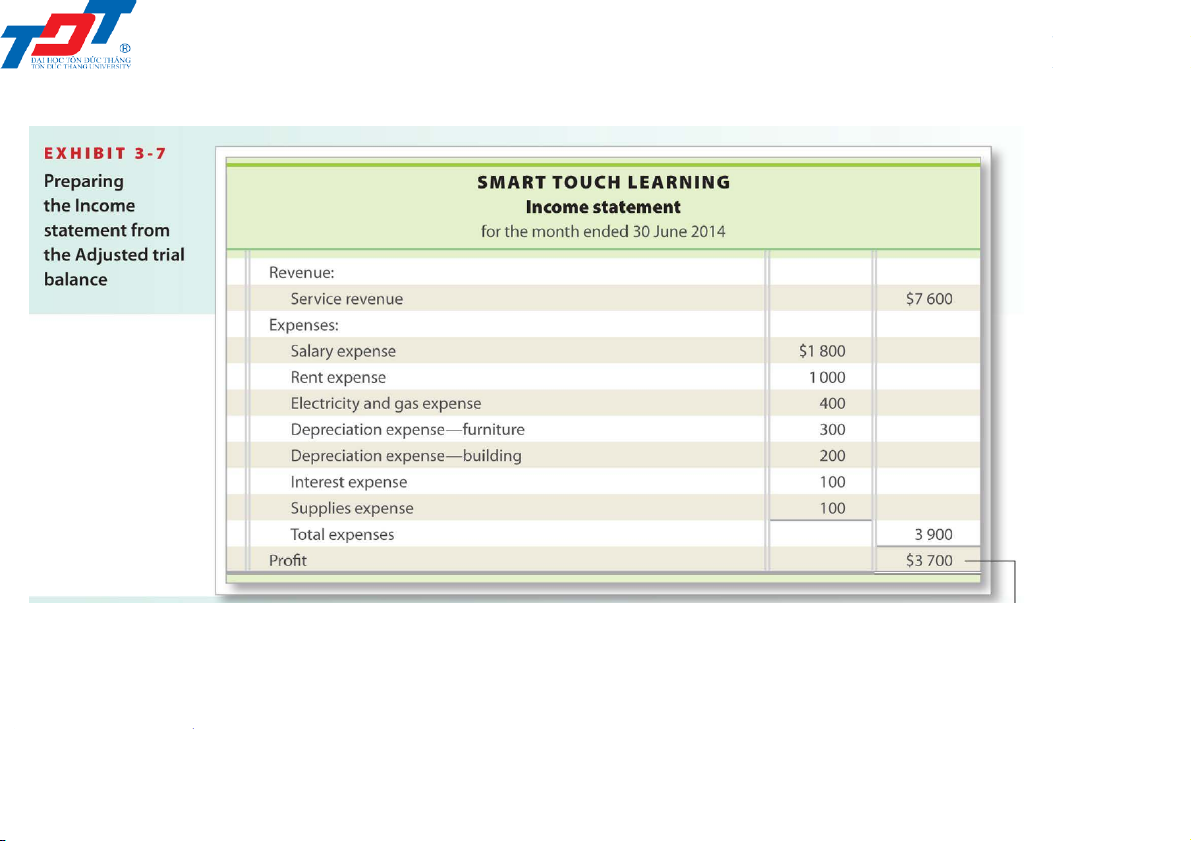

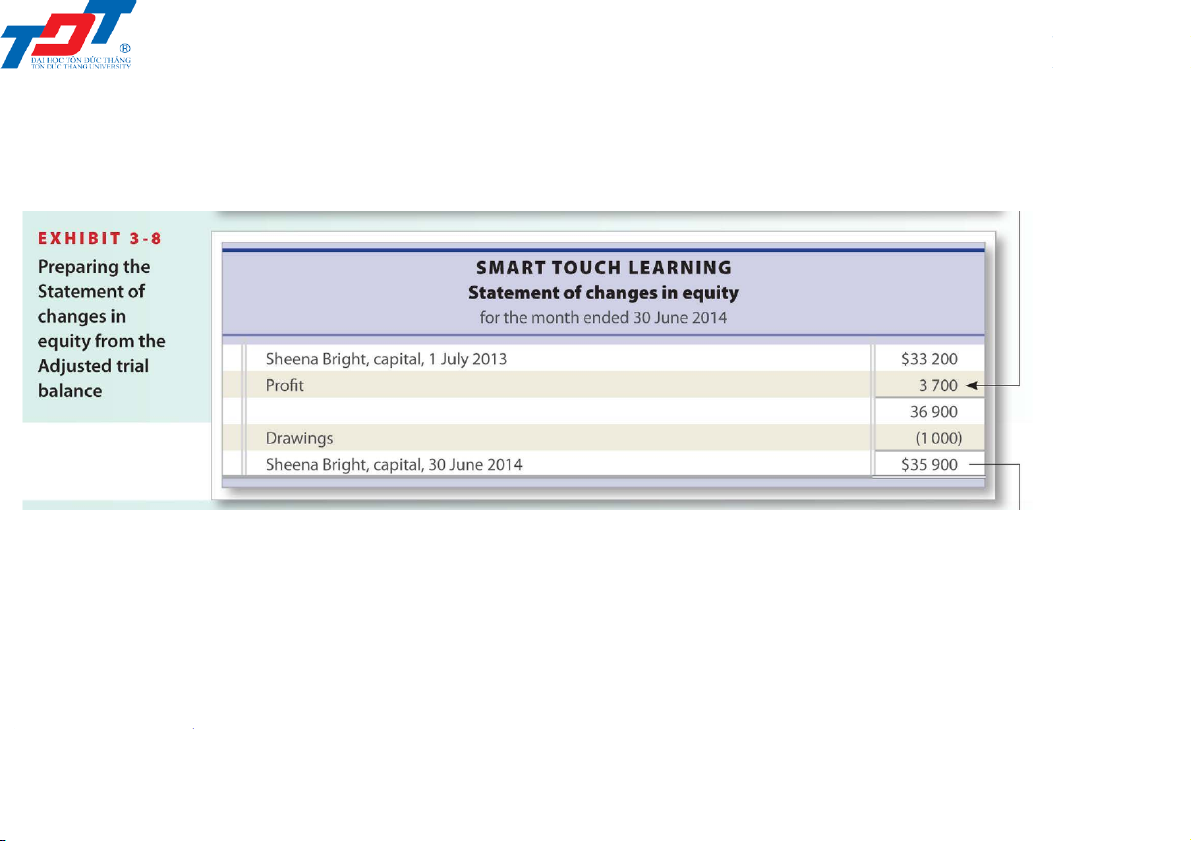

3.5. The financial statements

• The income statement reports revenues and expenses

• The statement of changes in equity shows why capital changed during the period

• The balance sheet reports assets, liabilities and owners’ equity

• The financial statements should be prepared in the following order:

(1) income statement to determine profit or loss;

(2) statement of changes in equity which needs profit or loss from the

income statement to calculate ending capital;

(3) balance sheet which needs the amount of ending capital to achieve its balancing feature 1/ 2/ 2020

201044 - The adjusting process 18

3.5. The financial statements 1/ 2/ 2020

201044 - The adjusting process 19

3.5. The financial statements 1/ 2/ 2020

201044 - The adjusting process 20

Tài liệu liên quan:

-

Chương 1 Ma trận và hệ phương trình

19 10 -

Bài tập Kiểm toán BCTC Chương 2: Hàng tồn kho và Ghi nhận Doanh thu

111 56 -

Bài giảng toán kinh tế chương 3 | Trường Đại học Tôn Đức Thắng

156 78 -

Bài giảng chương 4 hàm hai biến | Toán kinh tế

146 73 -

Bài giảng chương 1: ma trận và các phép toán | Toán kinh tế

123 62