Trắc nghiệm ôn kiểm toán giữa kỳ

Trắc nghiệm ôn kiểm toán giữa kỳ trường đại học Tôn Đức Thắng

Môn: Kinh doanh quốc tế (International Business) 19 tài liệu

Trường: Trường Đại học Tôn Đức Thắng 4.5 K tài liệu

Tác giả:

Preview text:

TON DUC THANG UNIVERSITY FACULTY OF ACCOUNTING Chapter 2:

Audit planning and risk assessment Course code: 201106 1/29/2024

201106- Planning and risk assessment 1 Learning objectives

Understand an audit process

Understand risk assessment procedures

Assess risks of misstatements

Understand the concept of materiality 1/29/2024

201106- Planning and risk assessment 2 Contents 2.1 Audit process

2.2 Identifying and responding to the risk of misstatements 1/29/2024

201106- Planning and risk assessment 3 2.1 Audit process Audit Audit Audit preparation performing finishing 1/29/2024

201106- Planning and risk assessment 4 Audit preparation

1) Preliminary Engagement Activities 2) Overall Audit Strategy 1/29/2024

201106- Planning and risk assessment 5 Audit preparation

1) Preliminary Engagement Activities

a) Client Acceptance or Continuance

b) Compliance with Independence and Ethical Requirements c) Engagement Letters 1/29/2024

201106- Planning and risk assessment 6 Audit preparation

a) Client acceptance and continuance

Consider the integrity of management

Professional competency of auditor team Obey professional ethics 1/29/2024

201106- Planning and risk assessment 7 Audit preparation

b) Compliance with Independence and Ethical Requirements

Identify threats to principles of ethics Self-interest threat Self-review threat Advocacy threat Familiarity threat Intimidation threat

Methods to reduce threats to acceptable levels 1/29/2024

201106- Planning and risk assessment 8 Audit preparation c) Engagement Letters

When a new client is accepted or when an audit

engagement continues from year to year, an

engagement letter should be prepared.

Serves as a means of reducing the risk of

misunderstandings with the client and as a means of

avoiding legal liability for claims that the auditors did not perform the work promised Should include:

Objectives of the engagement

Management’s responsibilities

Auditors’ responsibilities

Any limitations of the engagement 1/29/2024

201106- Planning and risk assessment 9 Audit preparation 2) Overall audit strategy a)

The nature, timing and extent of planned risk assessment procedures;

b) The nature, timing and extent of planned further audit procedures. 1/29/2024

201106- Planning and risk assessment 10 Audit preparation

a) Risk assessment procedures:

Understand the entity and its environment

Relevant industry, regulatory, and other external factors; The nature of the entity;

The entity’s selection and application of accounting policies;

The entity’s objectives and strategies, and those related business risks;

The measurement and review of the entity’s financial performance

Understand internal control (Chapter 3)

identify and assess the risks of material misstatement 1/29/2024

201106- Planning and risk assessment 11 11 Audit preparation Industry and External Regulatory Factors Environment

• The market and competition, • Accounting principles and including demand, capacity, industry-specific practices and price competition;

• Regulatory framework for a

• Cyclical or seasonal activity regulated industry • •

Product technology relating to Taxation the entity’s products • . Government policies • • Environmental requirements Energy supply and cost. 1/29/2024

201106- Planning and risk assessment 12 Audit preparation Nature of the entity

Whether the entity has a complex structure

The ownership, and relations between owners and other people or entities 1/29/2024

201106- Planning and risk assessment 13 Audit preparation

The entity’s selection and application of accounting policies

The methods the entity uses to account for significant and unusual transactions.

The effect of significant accounting policies in

controversial or emerging areas for which there is a lack of

authoritative guidance or consensus.

Changes in the entity’s accounting policies.

Financial reporting standards and laws and regulations

that are new to the entity and when and how the entity will adopt such requirements. 1/29/2024

201106- Planning and risk assessment 14 Audit preparation

The entity’s objectives and strategies, and those related business risks Business risk is broader than the risk of material

misstatement of the financial statements, though it includes

the latter. Business risk may arise from change or

complexity. A failure to recognize the need for change may

also give rise to business risk. New products and services Regulatory requirements Expansion of the business Current and prospective

New accounting requirements financing requirements Use of IT

The effects of implementing a strategy 1/29/2024

201106- Planning and risk assessment 15 Audit preparation

The measurement and review of the entity’s financial performance

The measurement and review of performance is directed

at whether business performance is meeting the

objectives set by management (or third parties).

Monitoring of controls is specifically concerned with the

effective operation of internal control. 1/29/2024

201106- Planning and risk assessment 16 Case study

You are auditing Brownhouse Limited and are concerned

that a major problem facing the entity in the current year

is that its customer base has dropped by some 50 per

cent as a result of competition from a new entrant to the market. Required:

a. What are business risks would face Brownhouse?

b. Which information of financial statement is affected

by above identified business risks? 1/29/2024

201106- Planning and risk assessment 17 Audit preparation

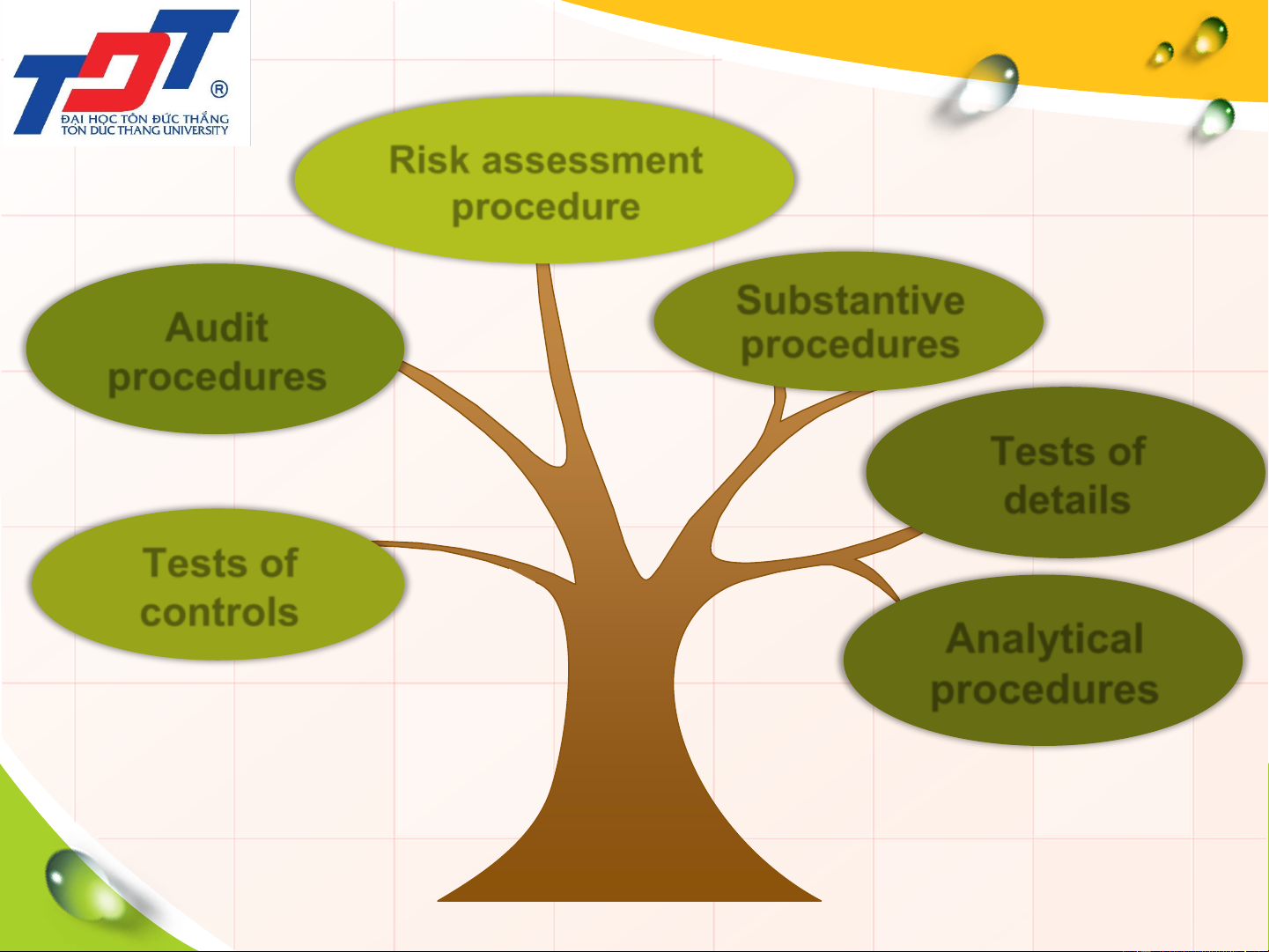

b) Further audit procedures at the assertion level

Tests of Controls: The auditor shall design and perform

tests of controls to obtain sufficient appropriate audit

evidence as to the operating effectiveness of relevant controls . 1/29/2024

201106- Planning and risk assessment 18 Audit preparation

b) Further audit procedures at the assertion level

Substantive Procedures: Tests are used to collect

evidence of material misstatement in financial statements. Include 2 types: Analytical procedures

Tests of detail: are the direct examination of the

transactions or account balances. 1/29/2024

201106- Planning and risk assessment 19 Risk assessment procedure Substantive Audit procedures procedures Tests of details Tests of controls Analytical procedures 20 1/29/2024

201106- Planning and risk assessment